matdesign24/iStock by way of Getty Pictures

PaySign, Inc. (NASDAQ:PAYS) continues to ship double digit internet gross sales development pushed by profitable investments in pay as you go card-based cost options concentrating on the plasma donation business. With 465 plasma facilities and 6.4 million cardholders as nicely as sponsorship with giant banks and card firms, I imagine that working margin and FCF may develop within the coming years. As well as, the current acquisition of shares by PaySign could speed up the demand for the inventory and decrease the price of capital. There are clear dangers coming from change within the regulatory framework, decrease internet gross sales development than anticipated, or failed partnerships. With that, I feel that PAYS may commerce a bit extra expensively.

PaySign

PaySign is a North American firm that provides pay as you go card companies and processing companies for company, institutional, and particular person shoppers. These two companies are the principle sources of revenue for the corporate. Considering that processing companies are utilized by public establishments for the group of their inner accounts and personal shoppers to save lots of prices and processing instances, they don’t imply higher revenue for the corporate, reasonably they’re one of many instruments the corporate has to generate loyalty and recognition, with the intention of getting them to contract one of many pay as you go card merchandise.

Merchandise embody present playing cards, company advantages, reloadable debit playing cards, medical or pharmaceutical help, donations, compensation, and withdrawing cash from financial savings accounts. The corporate is presently looking for to develop its product providing in the direction of journey playing cards and companies associated to them.

The enterprise of the corporate is organized by way of a single section, with home attain inside america. Open-Loop Pay as you go Card Market Forecast has long-term development forecasts, with an annual rate of 8% between 2024 and 2027, reaching a capitalization of round $836 billion this yr. On this regard, it’s value noting that different specialists imagine that the worldwide pay as you go card business may develop at a CAGR of 19.5% from 2023 to 2032.

In accordance with the report, the worldwide pay as you go card business generated $2.5 trillion in 2022 and is anticipated to generate $14.4 trillion by 2032, witnessing a CAGR of 19.5% from 2023 to 2032. Supply: Allied Market Research

PaySign’s merchandise have been utilized by giant firms listed within the Fortune 500 in addition to different multinationals and pharmaceutical firms. By the top of 2023, firm had 6.4 million clients, with a minimum of one pay as you go card exercise, in additional than 600 totally different provide applications.

The gross sales channels are managed by the identical firm. Because of the kind of provide that the corporate has, its relationship with pharmaceutical firms is crucial. Furthermore, the provide of reasonably priced costs for shoppers who goal this sector can be very important.

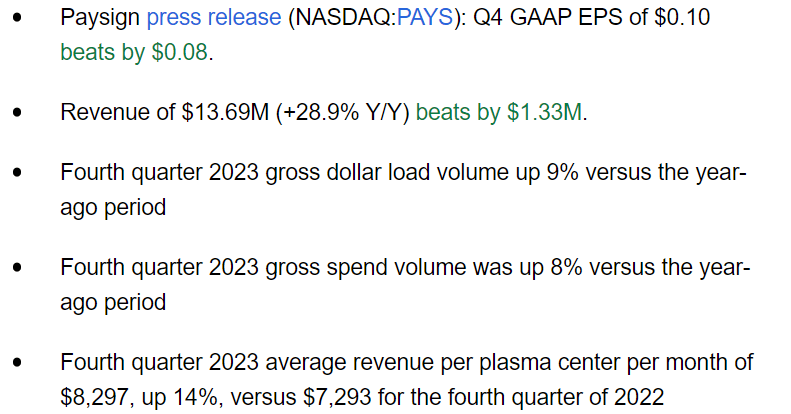

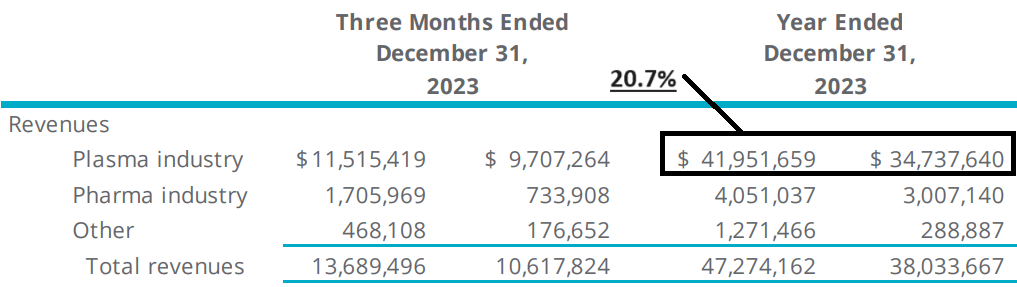

With that in regards to the enterprise mannequin, I imagine that it’s value taking a look on the current quarterly figures, which included better than expected EPS and quarterly internet income. Additionally it is value noting that the income per plasma heart per 30 days continues to extend as in comparison with the identical figures in This fall 2022.

Supply: In search of Alpha

Stability Sheet

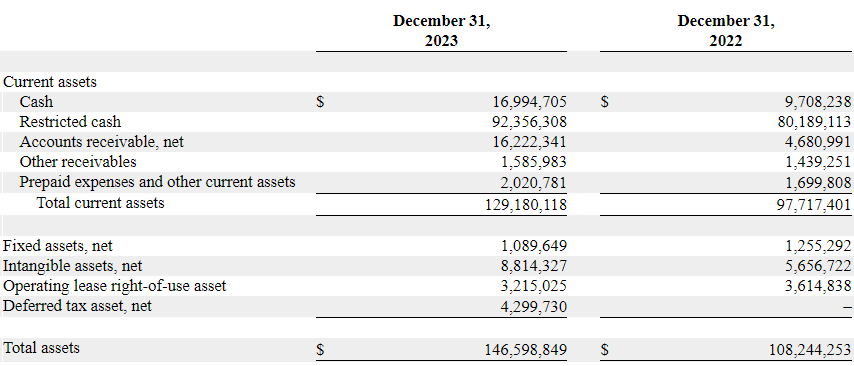

As of December 31, 2023, PaySign reported a steady stability sheet with a substantial amount of money and present ratio bigger than 1x. Moreover, the asset/legal responsibility ratio was additionally bigger than 1x. The corporate stories restricted money value $16 million, which is the cash obtained from pay as you go card holders. I didn’t consider the restricted money for the calculation of the enterprise worth.

Supply: 10-k

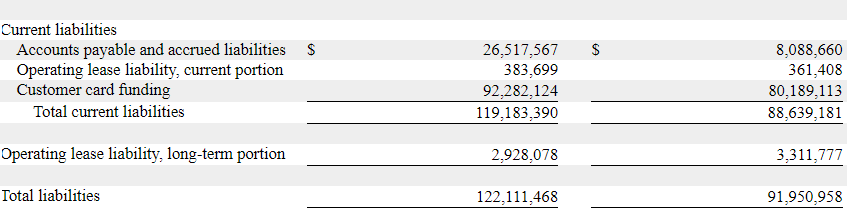

PaySign stories a major quantity of intangibles, so I had a have a look at what they characterize. Most of intangibles reported embody belongings associated to the platform in addition to buyer lists and contracts. I imagine that these are belongings that the corporate acquired previously. Additionally it is value noting that amortization of those belongings seems important. Specifically, in 2023, collected amortization elevated from near $9 million to about $13 million.

Supply: 10-k

With regard to the listing of liabilities, probably the most related is that PaySign doesn’t present debt. Accounts payables and buyer card funding appear sufficient to finance the operations of PaySign.

Supply: 10-k

Speculation 1: Plasma Income Might Speed up Internet Gross sales Progress Below My Base Case Situation

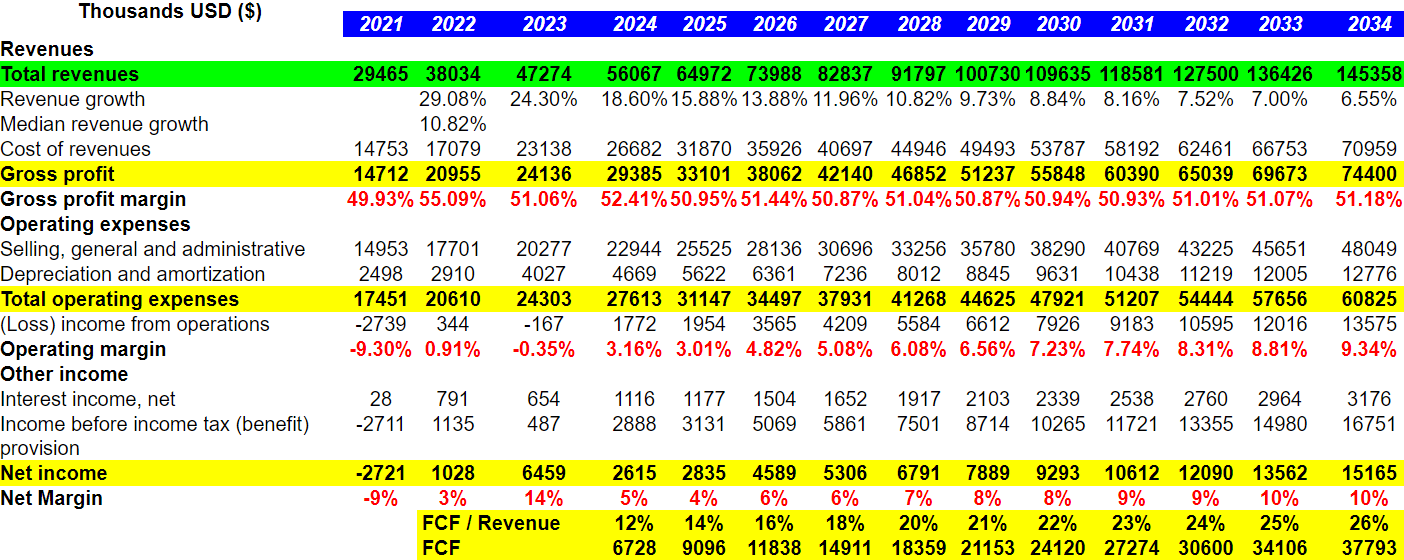

For the yr 2024, the forecasts are positive for the corporate, with the expectation of reaching revenues near $54.6 million and $56 million in annual price, with a 100% improve within the pharmaceutical sector and in addition important, though smaller, improve within the provide of plasma merchandise. Given the current improve in internet gross sales development within the Plasma business, I imagine that we may count on additional momentum development within the coming years.

In 2011, we started advertising and marketing a company incentive pay as you go card-based cost answer concentrating on the plasma donation business. Supply: 10-k

Supply: Quarterly Press Launch

The corporate is anticipated to proceed increasing its provide channels, because it did in 2023, acquiring optimistic outcomes, from the opening of 465 new plasma facilities and greater than 20 applications for shoppers within the pharmaceutical sector. For that reason, as famous beforehand, the corporate’s relationships and investments in these areas are a cornerstone to proceed sustained development. For my part, the brand new plasma facilities will most definitely convey FCF acceleration and FCF margin development.

Speculation 2: New Pharmaceutical Options Improve Internet Gross sales Progress, And Carry Economies Of Scale

I imagine that additional improvement of merchandise for the pharmaceutical business may additionally convey internet gross sales acceleration and sure economies of scale. With cash obtained from giant firms within the pharmaceutical firm, I feel that the variety of merchandise supplied may develop within the coming years.

Let’s observe that proper now the corporate doesn’t solely provide pay as you go playing cards, but in addition shopper name heart service and help, pharmacy claims adjudication, and CRMs. Below my base case situation, these new merchandise could convey median internet gross sales development of about 10.8%.

Funds are offered by the sponsoring pharmaceutical firm to be used at retail pharmacies, specialty pharmacies, hospitals, medical doctors’ workplaces and clinics nationwide. Supply: 10-k

Our choices additionally enable shoppers to instantly handle extra of their pharmacy advantages and embody pharmacy claims adjudication, community and cost administration, shopper name heart service and help, reporting, rebate administration, in addition to implementation, coaching and account administration. Supply: 10-k

Speculation 3: Sponsorship And New Partnerships With Banks Improve Internet Gross sales Progress And Working Margin

PaySign obtains sponsorship from related banking entities, and its revenue is derived from the varied operations that embody the provide of its companies similar to charges to be used, fee expenses in transactions, and administration charges amongst others.

PaySign’s open-loop pay as you go playing cards provide the opportunity of integrating into the worldwide community wherein the principle credit score and card firms function, similar to Visa (V), Mastercard (MA), or Maestro, amongst others, providing a wide range of doable makes use of. Moreover, using this kind of playing cards is rising attributable to new phenomena in relation to bodily and digital cash, and it’s a rising possibility for these individuals who wouldn’t have the necessities to open a financial institution financial savings account.Below my base case situation, new partnerships with card firms and banks will most definitely convey internet gross sales development and working margin development. Consequently, below my base case situation, I assumed a 2034 working margin of about 9%.

Speculation 4: Repurchase Of Shares Leads To A WACC Of 6.7%

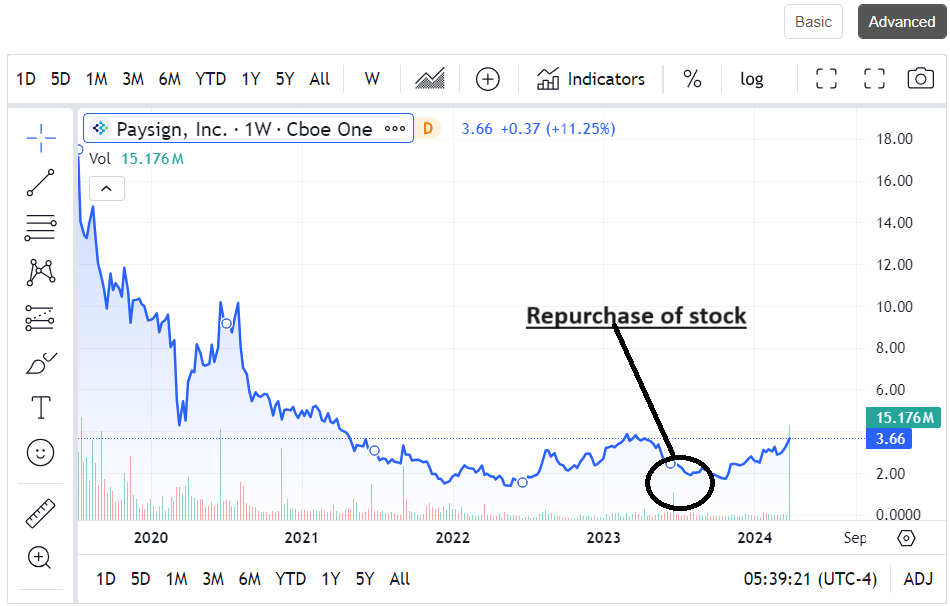

Given the current acquisition of 394,558 shares of widespread inventory for $1,127,884, I imagine that demand for the inventory may speed up quickly. Clearly, the truth that the corporate is shopping for shares on the present value marks means that there’s some undervaluation within the inventory.

Supply: In search of Alpha

On March 21, 2023, our Board approved a inventory repurchase program to repurchase as much as $5 million of our widespread inventory, topic to sure situations, within the open market, in privately negotiated transactions, or by different means in compliance with Rule 10b-18 below the Alternate Act. This system is anticipated to be accomplished inside 36 months from the graduation date. As of December 31, 2023 the Firm repurchased 394,558 shares of widespread inventory for $1,127,884 at a weighted common value of $2.86 per share. Supply: 10-k

Below my base case situation, I assumed that the demand for the inventory may decrease the price of capital. Consequently, I assumed a WACC of 6.7% in my base case situation. Within the worst case situation, I included a WACC of seven.5%.

Base Case Situation: Profitable Hypotheses Lead To A Valuation Of $6.29 Per Share

Below my base case situation, I assumed that the listing of hypotheses was appropriate. Consequently, the corporate stories internet gross sales development, working margin development, and important FCF/internet income development. I additionally took into consideration earlier figures reported by PAYS.

Supply: In search of Alpha

Supply: In search of Alpha

Supply: In search of Alpha

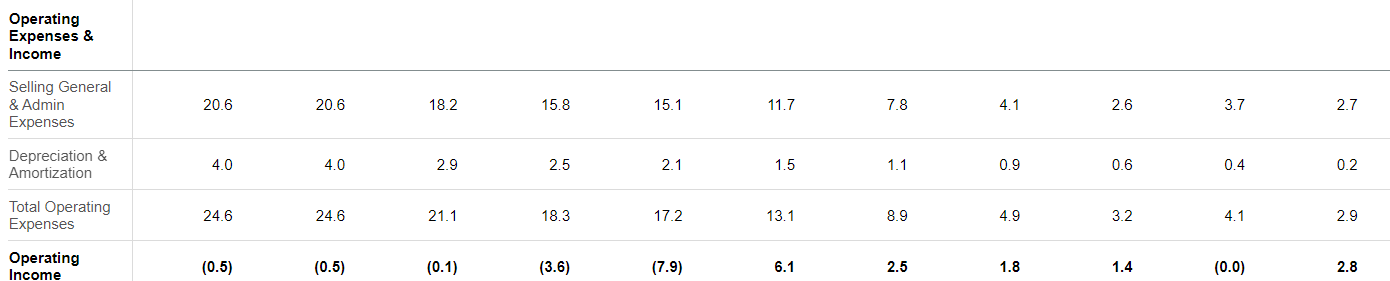

I included the next revenue assertion gadgets. First, 2034 whole revenues can be near $145 million, with value of income value $70 million and gross revenue of $74 million.

As well as, with promoting, normal, and administrative bills of $48 million in addition to depreciation and amortization near $12 million, whole working bills stand at $60 million. The outcomes would come with revenue from operations of $13 million. Furthermore, with curiosity revenue of $3 million, internet revenue can be near $15 million. Word that I assumed an working margin between about 3% and 9% in addition to internet margin near 10%.

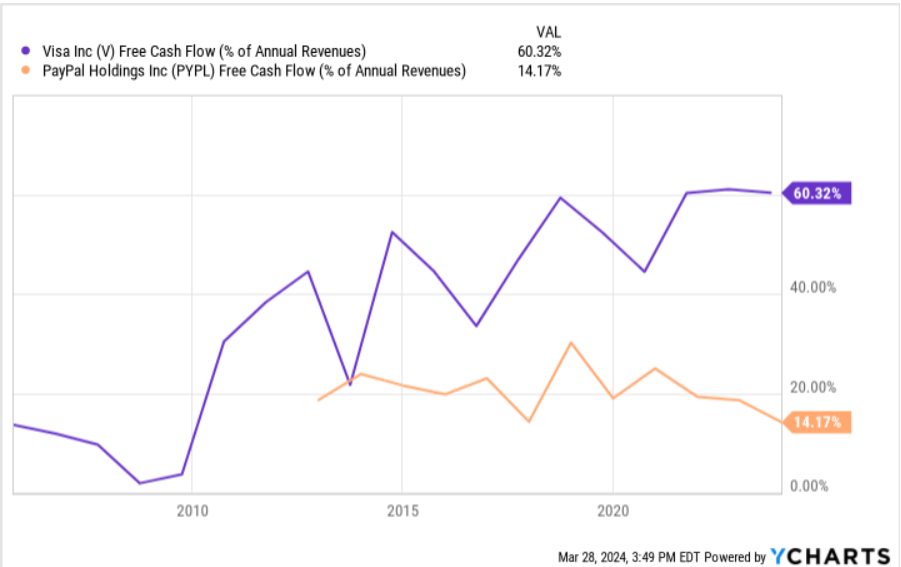

Lastly, if we additionally embody FCF/income near 26%, income would stand at $37 million. Word that Visa (V) trades at near 60%, and Paypal (PYPL) stories FCF/income of 14%. If PaySign continues to develop, I feel that the corporate could possibly be comparable to those giant firms. For my part, the FCF/income ratio near 26% seems affordable for a base case situation. I additionally imagine that my figures are conservative given the web gross sales reported in the newest years.

Supply: Ycharts

Supply: My Expectations

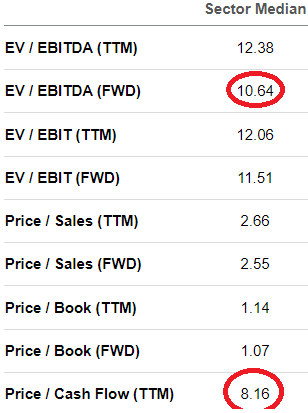

I assumed a WACC of 6.7%, which is consistent with the price of capital reported by different firms. On this regard, I’d seek the advice of the next desk offered by other analysts.

Supply: Gurufocus

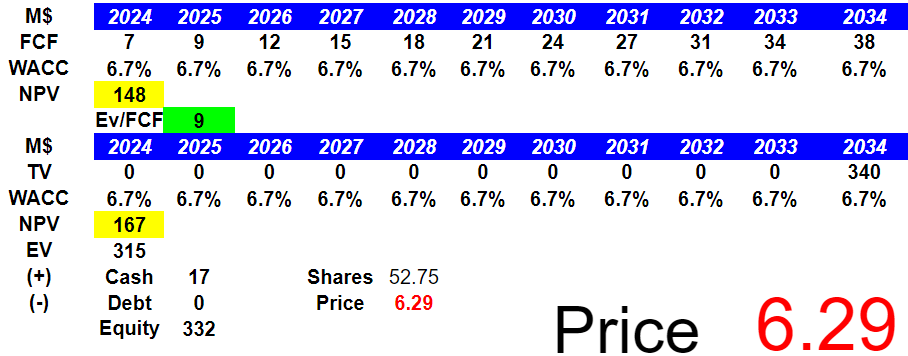

With EV/ TTM EBITDA within the sector of near 10x and value/money stream near 8x, I assumed an EV/FCF ratio of about 9x. I imagine that my figures are fairly conservative.

Supply: In search of Alpha

My outcomes would come with enterprise worth near $315 million and an fairness valuation of $332 million. Lastly, the implied value would stand at about $6.29 per share.

Supply: My Expectations

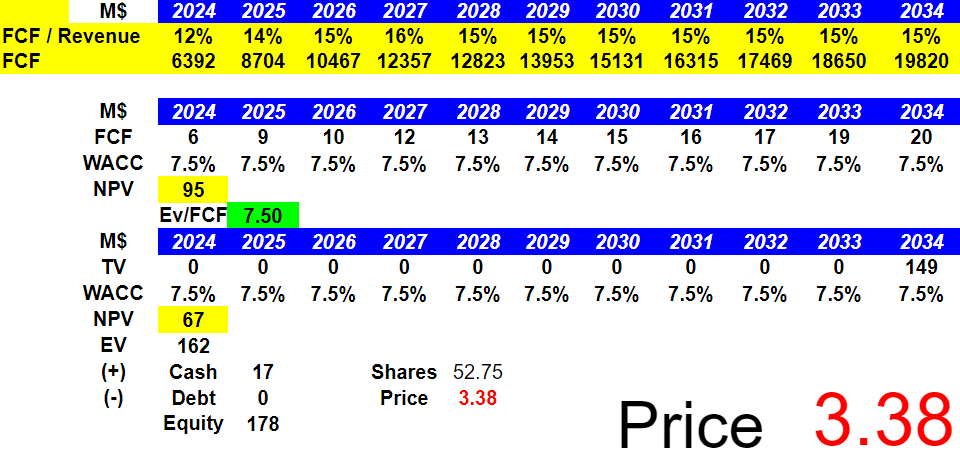

My Worst Case Situation Contains Failure Of Hypotheses, Which Implied A Valuation Of $3.38 Per Share

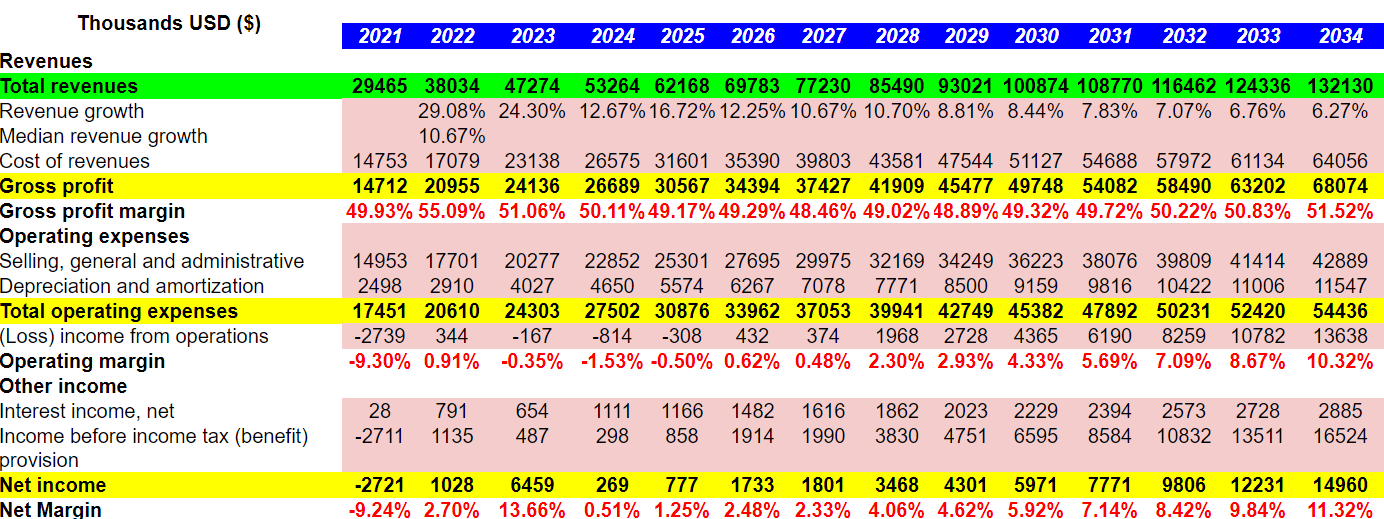

My worst case situation consists of internet gross sales development, however the FCF/income is a bit decrease than that within the base case situation. Internet revenue development would even be decrease than that within the earlier case situation. Lastly, I embody a WACC that could be a bit increased than that within the earlier case situation. I assumed that decrease demand for the inventory may result in will increase in the price of capital.

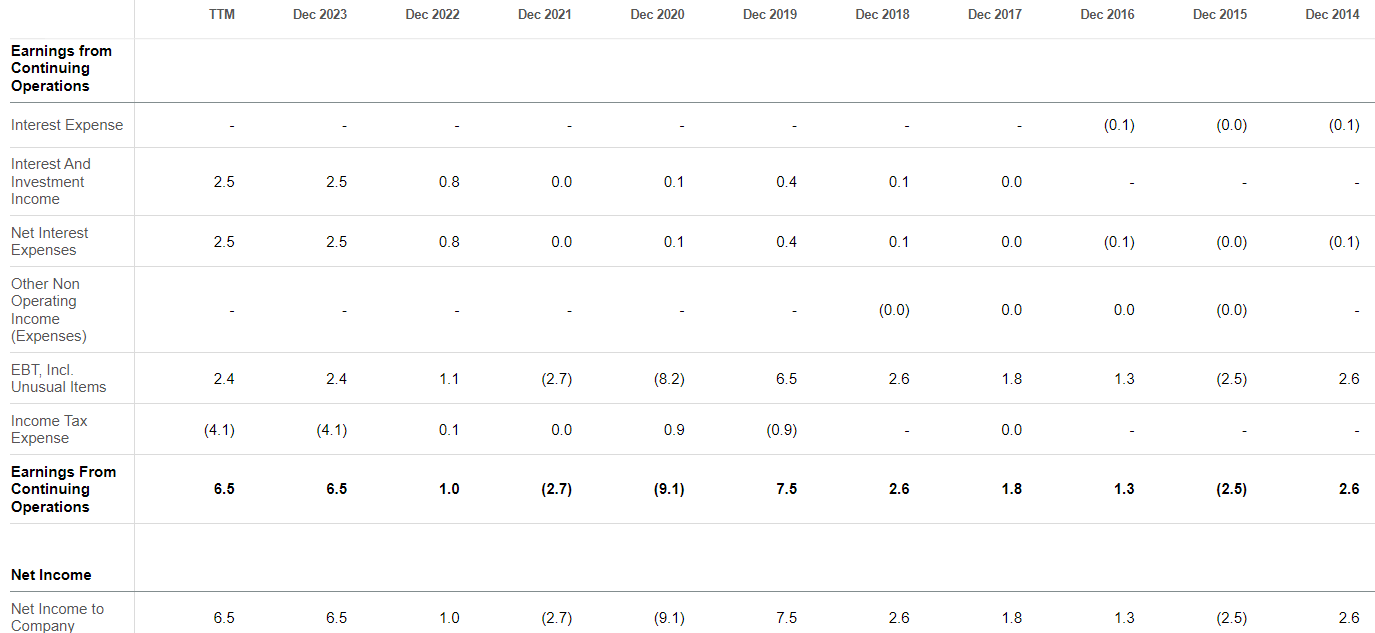

Below this situation, I additionally included 2034 whole revenues of $132 million, income development of about 6.2%, and median income development of about 10%. I additionally assumed a value of income of about $64 million and gross revenue near $68 million.

As well as, I included promoting, normal, and administrative prices of $42 million, with depreciation and amortization of about $11 million. 2034 whole working bills would stand at $54 million, and revenue from operations can be $13 million. Lastly, with a 2034 working margin of about 10%, curiosity revenue of $2.8 million, and revenue earlier than revenue tax of $16 million, I obtained internet revenue near $14 million.

Supply: My Expectations

If we assume a FCF/income ratio of 15%, 2034 FCF can be near $19 million. As well as, with a WACC of seven.5% and terminal EV/FCF ratio of seven.5x, the implied truthful value would stand at about $3.38.

Supply: My Expectations

Opponents, And Dangers

Throughout the market wherein it participates, PaySign maintains minority positions in comparison with historic firms within the sector which have higher sources and market capitalizations. In some segments, similar to cost options and pharmaceutical choices, competitors is extremely fragmented, as there are a number of members with particular merchandise or regional attain. Along with pay as you go card firms, we should additionally contemplate banking entities with traces of credit score and comparable companies in addition to pay as you go drugs and associated firms.

Above and past aggressive dangers, it have to be thought of that any change within the regulatory frameworks inside the markets wherein the corporate participates may have an effect on the present operation of the corporate. Inside this, the expansion goal and the forecasts couldn’t attain the estimated values.

After all, an financial disaster or discount within the cost capability of shoppers may scale back the demand for the corporate’s companies, along with the evolution that exists within the markets for digital media and digital instruments for cost of companies, which poses an innovation which may render the corporate’s present technological capabilities out of date.

Conclusion

PaySign continues to ship double digit internet gross sales development, and I imagine that the current 465 new plasma facilities may speed up development within the coming years. For my part, administration intelligently financed pay as you go card-based cost options concentrating on the plasma donation business. I additionally suppose that new sponsorship with giant banks or card firms may convey further FCF development and working margin development pushed by economies of scale and new potential shoppers. There are apparent dangers coming from decrease internet gross sales development than anticipated, adjustments within the regulatory framework, or failed partnerships with card firms. With that, I feel that PaySign may commerce a bit costlier within the coming years.