Joe Hendrickson/iStock Editorial through Getty Pictures

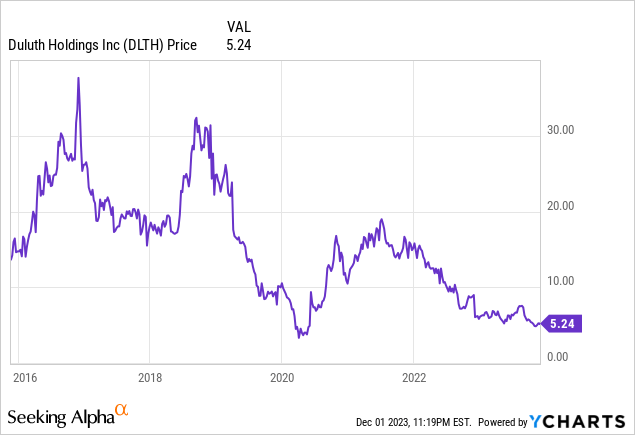

Duluth Holdings Inc. (NASDAQ:DLTH) has struggled by way of a difficult macro surroundings in recent times amid declining gross sales and poor earnings. The attire retailer simply reported its newest quarterly consequence, which missed estimates whereas administration provided gentle steerage. The setup right here would not look good with the inventory down greater than 40% over the previous 12 months.

That being mentioned, the corporate has a turnaround plan and we are able to level to some areas of energy inside its model portfolio. We imagine 2024 shall be crucial for the corporate to show it could possibly stabilize gross sales and drive an earnings rebound to help a extra sustained rally within the inventory.

DLTH Earnings Recap

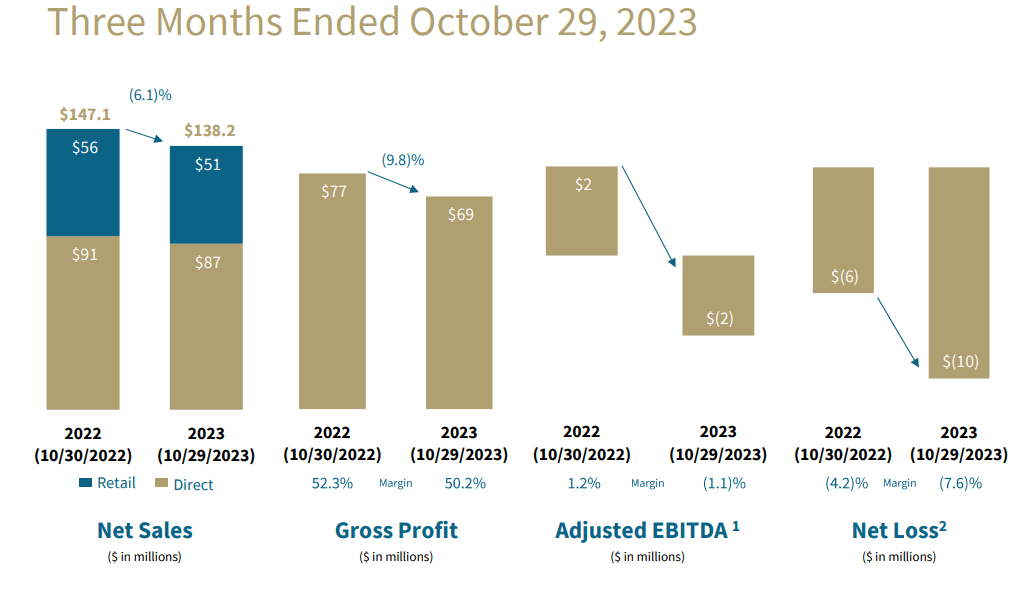

DLTH reported a Q3 EPS loss of -$0.32, $0.08 under estimates, and down from the -$0.19 loss in Q3 2022. Income of $138 million was down by 6.1% y/y, additionally coming in below expectations.

The weak point right here was throughout the board with the direct-to-consumer gross sales of $87.0 million down by -4.4%, with administration citing a decline in web site visits. Equally, foot site visitors was slower throughout the corporate’s 62 retail areas the place gross sales declined by -8.8% to $51.2 million.

We talked about a silver lining, on this case, the corporate has discovered success with its Girls’s “AKHG” sub-brand with gross sales rising by 19% from the interval final 12 months. Duluth has additionally made progress in adjusting its stock ranges, down by 15%, though this has been achieved by way of discounting which was mirrored in a decrease gross margin.

Whilst SG&A declined by -2.9% y/y by way of some company effectivity efforts, this was nonetheless not sufficient to stability the weaker prime line. The adjusted EBITDA at -$1.6 million reversed a optimistic $1.7 million in Q3 2022.

supply: firm IR

When it comes to steerage, administration expects full-year 2023 internet gross sales of between $640 and $655 million. Notably, this was revised decrease in comparison with the prior goal between $645 and $660 million introduced with the Q2 outcomes. If confirmed, the pattern represents a decline of round 2% from 2022.

The complete-year adjusted EBITDA goal between $35 and $39 million is down from the prior $41 million midpoint estimate. On a GAAP foundation, an EPS loss between -$0.25 and -$0.15, reverses a revenue of $0.07 reached final 12 months.

In the course of the earnings conference call, administration tried to challenge some confidence by specializing in an bettering gross sales combine that’s anticipated to help margins into the spring season whereas noting that stock ranges at the moment are wholesome. The early learn into This fall is that tendencies through the Black Friday purchasing week had been “solid”.

Lastly, we are able to point out that the corporate ended the quarter with $8.2 million in money towards $36.2 million in long-term debt. Contemplating the adjusted EBITDA trajectory, a internet leverage ratio below 1x suggests the stability sheet is secure.

What’s Subsequent For DLTH?

It is clear that the tendencies should not shifting in the best course, and there are many causes to be skeptical of any turnaround alternative. Duluth has disillusioned buyers going again to a interval even earlier than the pandemic and there may be some concern that the model momentum is lacking.

Ideally, we wish to see a situation the place progress re-accelerates with a path for earnings to pattern increased. Whether or not or not that is doable will begin with the flexibility of administration to execute its “Big Dam Blueprint” progress methods. The concept right here is for the corporate to kickstart some operational momentum by specializing in its strengths by focusing on value-added alternatives.

Duluth needs to push its attain throughout digital whereas optimizing its retail footprint with additional effectivity efforts. On that time, a current improvement has been the rollout of a brand new automated achievement middle anticipated to enhance order processing and stock administration. Finally, the plan is to ship sustainable progress and profitability.

supply: firm IR

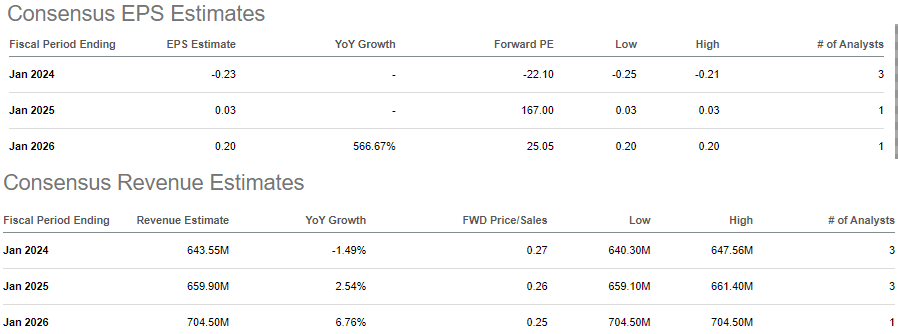

Based on consensus estimates, Duluth gross sales are seen rebounding by way of 2024 whereas the corporate reclaims profitability subsequent 12 months in the direction of an EPS of $0.03. Once more, we are able to take these estimates with a grain of salt and acknowledge the numerous uncertainty. Step one shall be for gross sales to cease declining whereas a 2024 steerage replace anticipated with the following quarterly outcomes shall be necessary to set the stage for the 12 months forward.

Looking for Alpha

The opposite subject comes right down to valuation. Taking the administration steerage for the present 12 months adjusted EBITDA of round $37 million, DLTH is buying and selling at an EV to ahead EBITDA a number of of roughly 11x.

Whereas this stage just isn’t essentially “expensive”, the ratio is at a premium to the broader attire retailer trade. The issue is that just a few extra quarters of disappointing outcomes might open the door for a bigger repricing decrease and selloff within the inventory.

Looking for Alpha

Last Ideas

We price DLTH as a maintain, giving the corporate the advantage of the doubt that the worst is over and the turnaround technique can work. It is honest to imagine the weak point in shares over the previous 12 months has already integrated most of the weak factors with the outlook.

The bullish case for DLTH is that outcomes going ahead outperform expectations with the potential of the corporate benefiting from an bettering macro surroundings.

However, the danger {that a} gross sales rebound fails to materialize would possible drive a extra in depth restructuring effort that will undermine the earnings outlook. And not using a clear enchancment in monetary situations, we count on shares to stay unstable.