Mongkol Onnuan

Elevator Pitch

DXC Technology Company (NYSE:DXC) is rated as a Hold. There are both positives and negatives relating to DXC’s recent financial disclosures that justify a Neutral view of the stock. On one hand, DXC Technology has done a good job in managing costs which translated into an earnings beat for the latest quarter. On the other hand, DXC’s management guidance for the new fiscal year fell short of expectations, as the turnaround of its Global Infrastructure Services segment remains a work-in-progress.

Company Profile

In its media releases, DXC calls itself a “technology services” business that offers solutions like “modernizing IT, optimizing data architectures, and ensuring security and scalability across public, private and hybrid clouds.”

The company has two key business segments, Global Business Services and Global Infrastructure Services. The GBS and GIS segments each accounted for half of DXC Technology’s revenue for the most recent fiscal year, as indicated in its FY 2024 (YE March 31, 2024) earnings presentation slides.

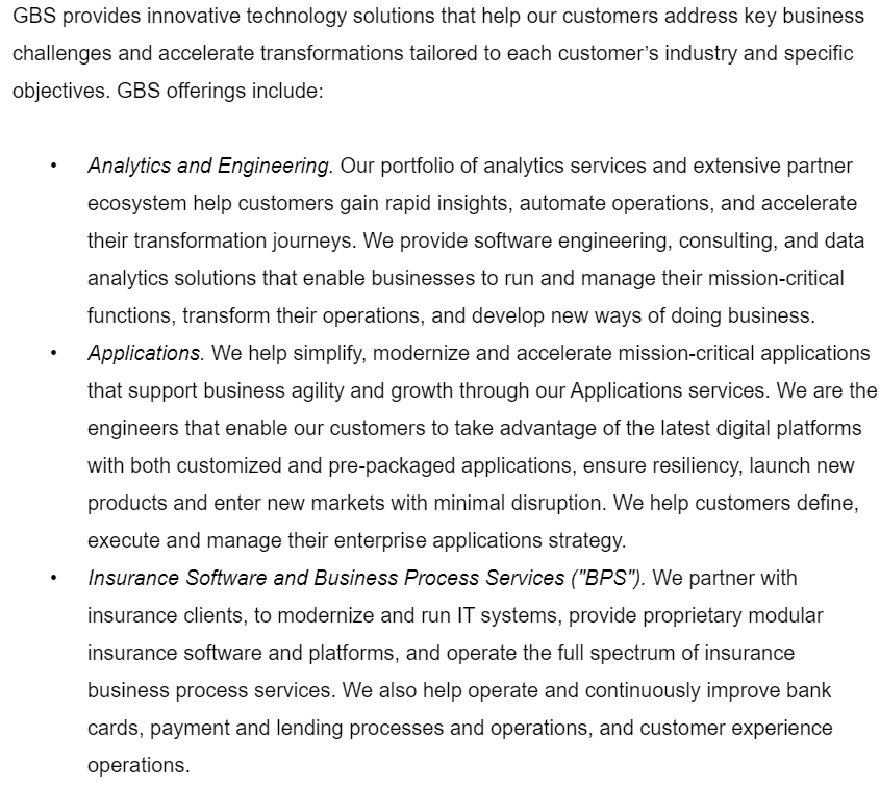

An Overview Of DXC Technology’s Global Business Services Or GBS Segment

DXC’s 10-K Filing

A Brief Description Of DXC’s Global Infrastructure Services Or GIS Segment

DXC’s 10-K Filing

DXC has yet to disclose the company’s sales contribution from different geographical markets for FY 2024, as the company’s FY 2024 10-K filing hasn’t been released. In FY 2023, DXC Technology derived 31% and 30% of its revenue from Europe (excluding the UK) and the U.S., respectively. The UK, Australia, and other foreign markets represented the remaining 13%, 10%, and 16% of DXC’s FY 2023 top line, respectively.

Earnings Beat Points To Good Expense Management

On May 16, 2024, after the market closed, DXC issued a press release disclosing its Q4 FY 2024 (January 1, 2024, to March 31, 2024) results.

The company’s top line decreased by -5.7% YoY to $3,386 million in the final quarter of fiscal 2024. DXC Technology’s most recent quarterly revenue was in line with expectations. Its actual Q4 FY 2024 sales were just marginally higher (+0.6%) than the consensus estimate of $3,366 million (source: S&P Capital IQ).

However, it is worth noting that DXC Technology’s latest quarterly bottom line of $0.97 per share beat the consensus forecast of $0.83 per share by a substantial +16.9% as per S&P Capital IQ data. DXC’s actual normalized EPS for Q4 2024 was also much better than the company’s non-GAAP adjusted EPS guidance in the $0.80-0.85 range. Furthermore, the company’s bottom-line contraction narrowed from -8.4% YoY in Q3 FY 2024 to -4.9% YoY for Q4 FY 2024.

It was better-than-expected operating profitability driven by good cost control that allowed DXC to register a significant earnings beat for the recent quarter.

DXC’s normalized EBIT margin expanded by +0.8 percentage points QoQ to 8.4% in Q4 FY 2024. This was also +1.2 percentage points higher than the consensus operating margin projection of 7.2% (source: S&P Capital IQ).

At the company’s Q4 FY 2024 results briefing, DXC Technology attributed its operating profitability improvement to “cost reduction initiatives.” DXC noted at its recent quarterly earnings call that the company’s expense control measures included “consolidating our five acquired enterprise business systems, and optimizing our back-end office functions.”

In a nutshell, DXC has taken actions to cut the company’s costs, and this has paid off in the form of EBIT margin expansion and above-expectations earnings. I touch on DXC Technology’s outlook in the next section.

But Disappointing Guidance Means Turnaround Will Take Time

In contrast with its Q4 FY 2024 bottom-line beat, DXC’s financial outlook for the new fiscal year was a disappointment.

DXC Technology is anticipating that it can register a revenue and normalized EPS of $12,810 million and $2.75, respectively in FY 2025 as per the mid-point of its guidance. The company’s FY 2025 top line and bottom-line guidance turned out to be -3.0% and -21.9% below the consensus forecasts of $13.2 billion and $3.52, respectively. DXC’s guidance also translates into expected revenue and earnings contraction of -6.3% and -12.1%, respectively, in this fiscal year.

In its FY 2023 10-K filing, DXC acknowledged that certain “technological developments” have “reduced and replaced some of our traditional services and solutions and may continue to do so in the future.” The company was most likely referring to its underperforming GIS or Global Infrastructure Solutions segment when it touched on the risks for its “traditional services and solutions.” Notably, DXC Technology mentioned at its Q4 analyst call that it “will execute a restructuring program to address excess capacity largely concentrated in the GIS” segment.

For the fourth quarter of fiscal 2024, the GIS segment’s organic revenue decreased by -9.3% YoY. Looking ahead, DXC Technology expects its GIS segment to record a “low double-digit” percentage contraction in organic revenue for full-year FY 2025 as per its earnings call management commentary. It is apparent that the continued weakness of the GIS segment has hurt DXC’s FY 2025 prospects.

In other words, the turnaround of DXC, in particular its GIS segment, will take time, and this is reflected in the company’s below-expectations FY 2025 guidance.

Closing Thoughts

A Hold rating for DXC Technology Company is warranted, considering the mixed read-throughs from its Q4 FY 2024 performance and FY 2025 guidance.

DXC Technology is now trading at a forward P/E multiple of 5.6 times, based on its FY 2025 EPS guidance of $2.75 and its last done share price of $15.49 at the end of after-hours trading on May 16.

A depressed mid-single P/E ratio for DXC Technology seems fair in my opinion. DXC’s top line and bottom line are still expected to decline in the new fiscal year, and it is uncertain how long it will take for the turnaround of the company’s GIS segment to be completed.