Jetta Productions Inc/DigitalVision via Getty Images

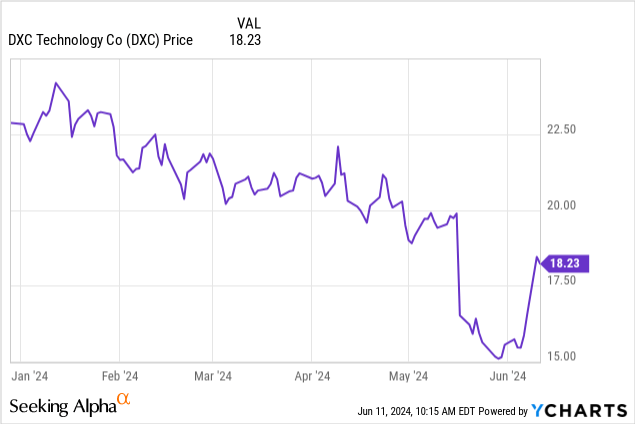

Shares of DXC Technology Company (NYSE:DXC) have rallied more than 15% on a report that private-equity group Apollo Global Management, Inc. (APO) and Kyndryl Holdings, Inc. (KD) are in discussions for a joint bid acquisition.

Kyndryl appears as a natural acquirer, operating in the same IT infrastructure services space as DXC, but supported by stronger fundamentals. Reuters cites a potential offer price for DXC between $22 and $25 per share representing a nearly 30% premium from the company’s current $3.3 billion market value.

While nothing has been confirmed, we believe DXC investors should welcome the news as the latest operating and financial results suggest the need for a deeper restructuring. Sales and earnings are sharply lower without a clear sign of a turnaround.

We highlighted some of these trends when we last covered the stock in 2023. Ultimately, the takeover could be a good option to unlock value for now with an upside in shares from the current level.

DXC Financials Recap

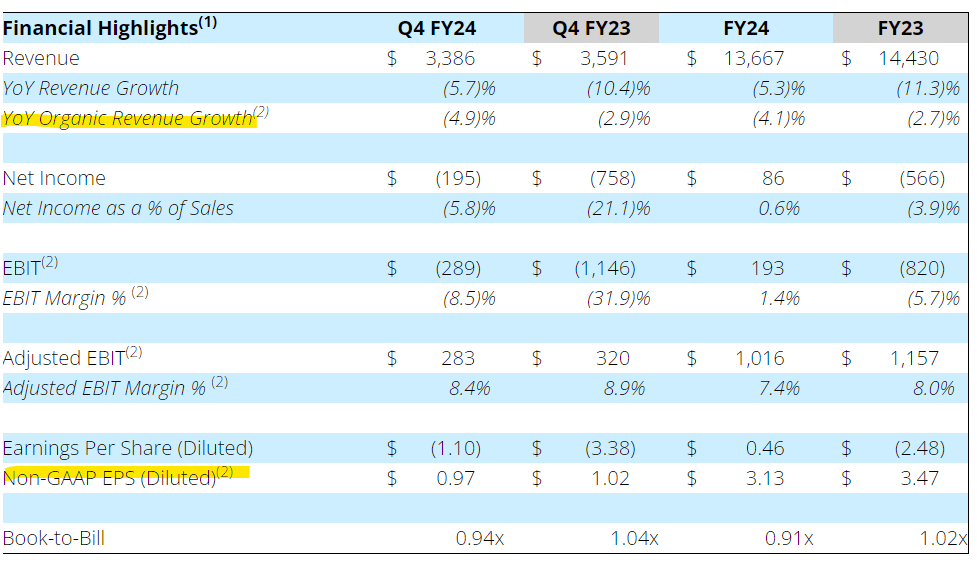

DXC reported its 2024 fiscal Q4 earnings on May 16 with a headline EPS of $0.97, coming in $0.14 ahead of what had been a low bar of expectations.

While the adjusted net income of $178 million in the quarter was down 24% from the period last year, DXC has been active with buybacks, repurchasing 18% of its outstanding share count for $883 million over the past year which reconciles the narrower 5% EPS decline. At the same time, those efforts have not supported the actual share price as DXC stock is down more than 30% over the period.

The story here has been an ongoing decline in sales across most segments. Q4 revenue of $3.4 billion was down by 5.7% year over year, or 4.9% on an organic basis. Even as the company has made efforts to control costs and realign corporate functions, the adjusted EBIT margin of 8.4% was down by 50 basis points from 8.9% in Q4 fiscal 2023.

source: company IR

What we’re seeing here is a continuation of soft client activity, where some of the weakness can be blamed on macro volatility but likely also reflects the competitive landscape where smaller emerging players may be taking market share for certain solutions.

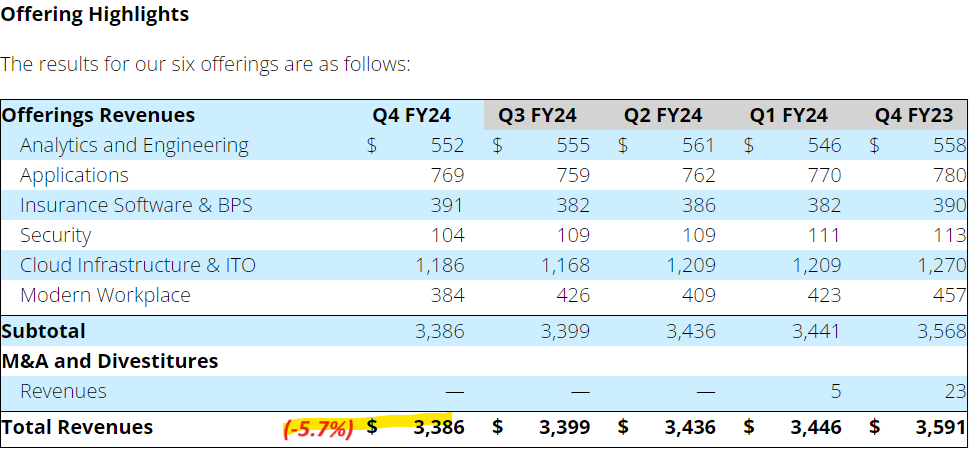

Five of the six major offerings posted a sales decline in Q4, with the lone exception being the “Insurance Software and Business Process Services” (BPS) with $391 million in sales essentially flat from $390 million in the period last year.

DXC notes that it is a market leader and “largest provider of insurance software and insurance BPS globally from origination to claims processing” with certain applications within the segment still generating growth.

Maybe the most telling metric across DXC results is a firm-wide book-to-bill ratio of 0.94x. This indicator is important as a level below 1.0 implies weak demand with fewer orders for new business coming in than being fulfilled.

source: company IR

The company’s strategy moving forward is to address what may be some excess capacity adding to unnecessary costs. The effort is to improve margins and at least stabilize sales by focusing on the company’s strong points is seen as materializing into fiscal 2026

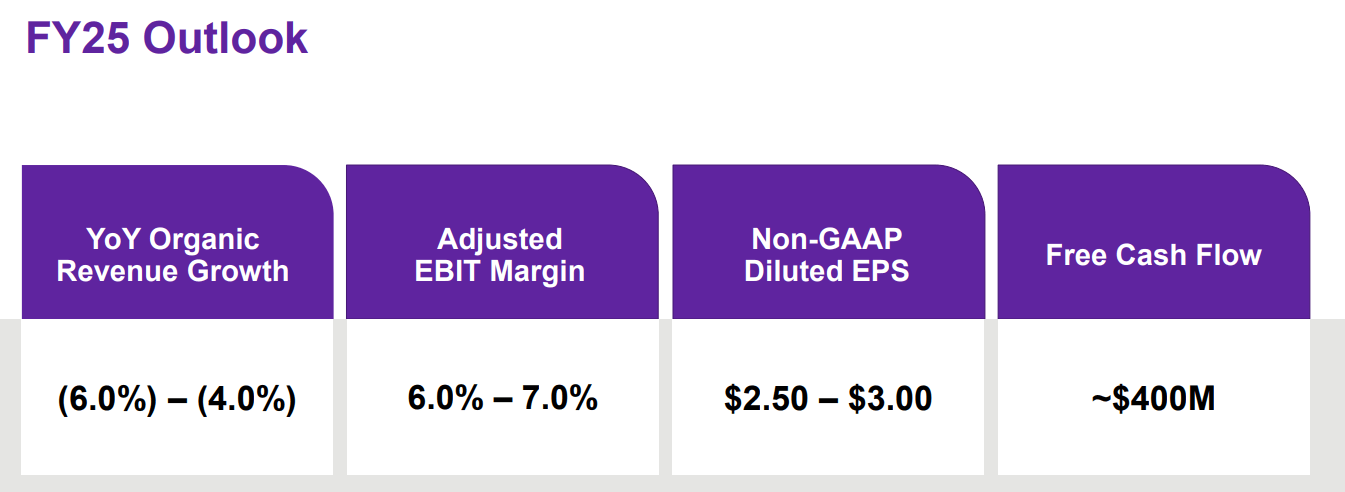

In terms of guidance for this year, fiscal 2025, DXC expects a decline of organic revenue between -6% and -4%, as well as a lower adjusted EBIT margin of around 6.5% compared to the 7.4% result in 2024. The non-GAAP EPS target between $2.50 and $3.00, if confirmed, would represent a drop compared to $3.13 this past year and $3.47 in fiscal 2023

source: company IR

Kyndryl Could Unlock Value in DXC Technology

As underwhelming as the trends from DXC have been, keep in mind the company is still generating nearly $13 billion in annual revenue and on track to deliver $400 million in free cash flow this year. The point here is to say that there is some underlying value in DXC’s core operation.

That dynamic is what brings up the company as a compelling acquisition target. Kyndryl Holdings, which split off from International Business Machines Corporation (IBM) back in 2021, appears to have an overlapping business model where the combined group would likely generate several synergies while leveraging new growth opportunities.

In contrast to DXC, Kyndryl is projecting sharply stronger earnings growth this year with a book-to-bill ratio of 1.1x last quarter. The Kyndryl Consult segment has been a standout with accelerating double-digit growth, outperforming not only DXC but other consulting peers such as Accenture plc (ACN) and Cognizant Technology Solutions Corporation (CTSH) that have struggled with lackluster demand.

source: company IR

Shares of KD have doubled over the past year as a reflection of its improving outlook while the fortunes of DXC have faded. With a current market cap of $6 billion, KD is larger than DXC but notably less leveraged.

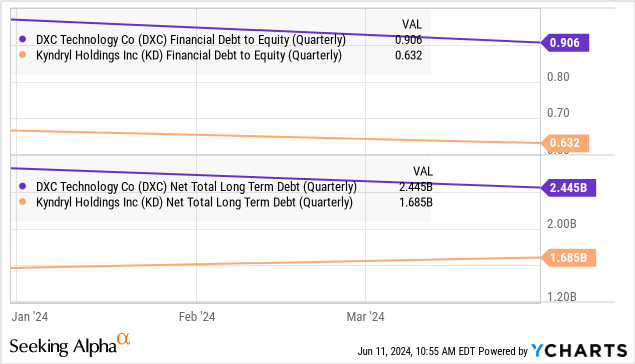

Even as DXC has made progress in paying down debt, its debt-to-equity ratio of 0.9x is well above KD at 0.6x. DXC’s net total long-term debt near $2.5 billion is well above the $1.7 billion level last reported by KD.

Presumably, Apollo Group involved with negotiations could engineer a merger transaction, leaving the new combined company on an even stronger financial footing.

By restructuring DXC assets, Kyndryl would absorb an extensive performing client base while entering new verticals. Given DXC’s underlying profitability and positive free cash flow, there is also potential that the transaction is accretive to KD’s EPS.

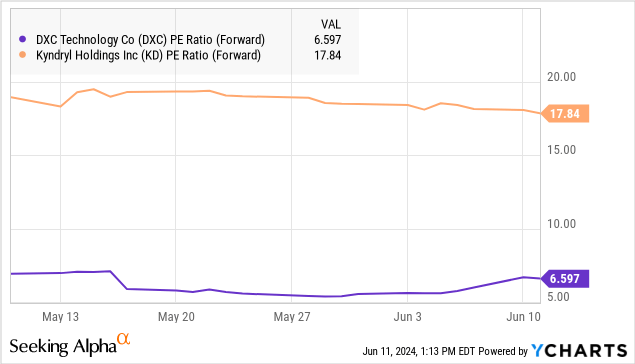

DXC currently trades at a depressed 7x forward P/E multiple while KD has seen an expansion of its growth premium toward 18x this year following the better-than-expected results and its positive financial outlook.

Final Thoughts

While no details have been announced or confirmed, a deal between DXC and KD remains speculation. Still, we sense that shareholders from both companies stand to benefit from reaching an agreement.

DXC has struggled amid a shifting competitive landscape and this opportunity could be a lifeline to stem any further deterioration in the business outlook. For KD, this mega-acquisition or merger could catapult the company to a significantly larger global footprint and work to reinforce the company’s long-term growth potential.

Ultimately, we rate DXC as a buy sticking to the midpoint of the rumored offer price of around $23.50 per share as a baseline of fair value and upside potential for the stock under the current circumstances. Even if the deal falls through, the recent low in shares now represents a strong area of technical support where other buyers and offers may be willing to step in.

There is also the scenario where DXC manages to turn around organically, with stronger results over the next few quarters could drive a new wave of positive sentiment. The main risk to consider when looking at DXC is its exposure to macro trends. A global slowdown of business conditions could force a reassessment of the earnings potential and open the door for a deeper selloff.