da-kuk

Introduction

In September 2023, I wrote a bullish article on SA about US pump distributor DXP Enterprises (NASDAQ:DXPE) during which I mentioned that I anticipated sturdy outcomes for the second half of 2023 due to excessive oil costs and that share buybacks may present a lift for its share value.

Nicely, the corporate’s EBITDA rose by 37.8% 12 months on 12 months to $170.2 million in 2023 whereas EPS got here in at $3.89 because it repurchased 1.7 million shares through the 12 months. With oil costs remaining sturdy, I feel that 2024 is more likely to be a very good 12 months for DXP Enterprises, and EBITDA may high $200 million. That being mentioned, the share value has soared by 54.71% since my earlier article and has surpassed my $49.28 goal. For my part, the margin of security right here has declined considerably and I’m reducing my score on DXP Enterprises’ inventory to impartial. Let’s evaluation.

Overview of the enterprise

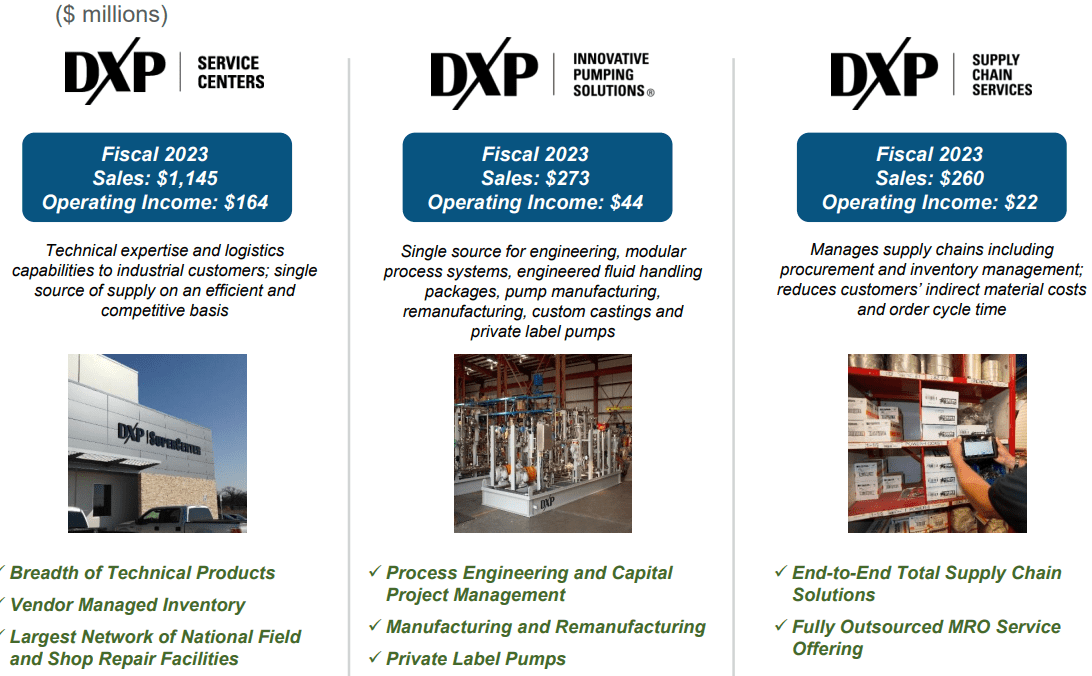

Should you’re not acquainted with the corporate or my earlier protection, this is a quick description of the enterprise. DXP Enterprises is a business-to-business distributor of upkeep, restore and working (MRO) services and products for the oil and fuel, chemical, meals and drinks, and transportation sectors amongst others – centrifugal pumps, mounted and unmounted bearings, reducing instruments, and fluid energy merchandise amongst others. As of December 2023, it had a community of 183 areas and about 95% of its revenues come from the USA. The corporate has three reporting segments – Service Facilities, Provide Chain Companies, and Modern Pumping Options.

DXP Enterprises

DXP Enterprises operates in a extremely fragmented and cyclical market, and it has been increasing by each natural progress and acquisitions over the previous a number of years. In 2022, DXP Enterprises accomplished 4 acquisitions for $64.8 million. In 2023, it purchased three corporations for $13.4 million. Complete gross sales have soared from $125 million in 1996 to virtually $1.7 billion in 2023 and free money move (FCF) conversion charges normally peak on the top of cycles.

DXP Enterprises

The corporate has been attempting to create a moat by a concentrate on extremely engineering options, however the enterprise stays susceptible to downturns within the oil and fuel trade because the latter accounts for near 1 / 4 of revenues.

DXP Enterprises

DXP Enterprises

The 2023 monetary outcomes

Turning our consideration to the 2023 outcomes, we are able to see that it was a very good 12 months for DXP Enterprises as gross sales elevated by 13.4% to $1.68 billion due to respectable natural progress throughout all enterprise segments (acquisitions added $33.1 million to gross sales). The corporate benefitted from sturdy financial progress within the USA in addition to excessive oil costs. The EBITDA margin expanded to 10.4% due to economies of scale and I anticipate it to stay above 10% in 2024. As you’ll be able to see from the desk beneath, the FCF of DXP Enterprises may be erratic. The advance in FCF in 2023 in comparison with 2022 may be attributed to the lower of receivables which had been partially offset by decreased stock purchases and accrued bills. The typical free money move conversion fee for the previous 15 years has been about 60% as this can be a enterprise with low CAPEX necessities. CAPEX in 2023 got here in at $12.3 million in comparison with $4.9 million a 12 months earlier.

DXP Enterprises

Many of the FCF went into share buybacks as DXP Enterprises repurchased shares for $56.2 million in 2023 in comparison with $47.9 million in 2022.

Trying on the stability sheet, I feel that DXP Enterprises may speed up share buybacks and acquisitions in 2024 as money soared to $173.1 million as of December 2023. The corporate additionally had credit score facility availability of $132.1 million on the finish of the 12 months. Total, I feel the stability sheet seems to be sturdy as web debt went right down to $353.1 million from $367.5 million a 12 months earlier. This interprets right into a web leverage ratio of solely 2.1x. But, it’s attainable that this ratio is increased as of the time of writing as DXP Enterprises has already introduced three acquisitions in 2024 – Hennesy Mechanical Sales, Kappe Associates, and Pro-Seal. It’s nonetheless unknown how a lot DXP Enterprises paid for these companies.

Way forward for the corporate

With US GDP progress remaining sturdy in early 2024 and manufacturing PMI nonetheless in growth territory, the enterprise of DXP Enterprises carries a whole lot of optimistic momentum in the intervening time. As well as, oil costs stay above $80 per barrel, and I feel that the corporate may e book natural income progress of near 10% for the 12 months, with the EBITDA margin more likely to surpass 11% (EBITDA of about $200 million). Additionally, inorganic progress is more likely to be a lot stronger in comparison with 2023 as Hennesy Mechanical Gross sales, Kappe Associates, and Professional-Seal have mixed TTM gross sales and EBITDA of $55.4 million and $6.5 million, respectively. CAPEX for 2024 is predicted to be between $10 million and $20 million, and my conservative expectation for FCF is round $70 million.

Valuation

As you’ll be able to see from the chart beneath, DXP Enterprises has traded at above 14x EV/EBITDA throughout peak years akin to 2014 and 2018, however the ratio dropped to beneath 8x in 2019 regardless of this being one other sturdy 12 months with EBITDA ranges just like 2018. Whereas DXP Enterprises doesn’t look costly in the intervening time at 7.6x EV/EBITDA, the margin of security right here appears a lot decrease in comparison with my earlier article in September. It appears that evidently a whole lot of the optimistic momentum for 2024 is already priced in by the market.

Searching for Alpha

As well as, I’m involved that the value to tangible e book worth has hardly ever been this deep into detrimental territory and that the value to earnings ratio is now the very best it has been since August 2022. If the US economic system slows down when the Fed begins reducing rates of interest or oil costs plunge within the coming months, DXP Enterprises may change into a price entice.

Searching for Alpha

Investor takeaway

DXP Enterprises booked sturdy monetary outcomes for 2023 and I feel 2024 is shaping as much as be a very good 12 months for the corporate, with EBITDA probably surpassing the $200 million degree. That being mentioned, this can be a cyclical enterprise that has generated losses throughout three years up to now decade and I feel the margin of security has shrunk considerably through the previous a number of months. For my part, this may very well be a very good time for buyers to trim or shut their positions.