neilkendall

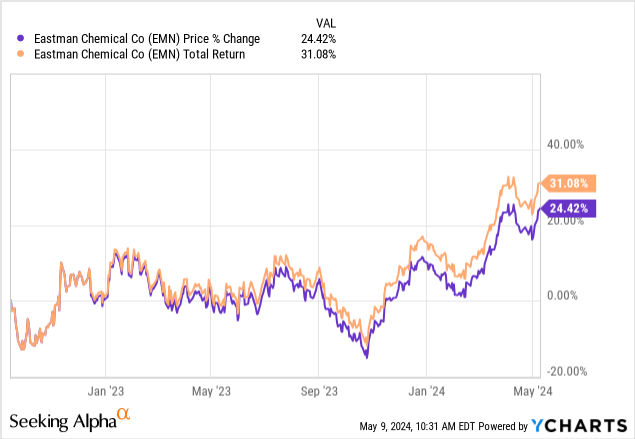

One of my kids is taking high school chemistry this year, and with the good fortune of having a teacher that makes the content understandable and engaging, my kid is now, all of a sudden, considering pursuing chemistry or related majors in college. As a dad looking to pay for college, this has sent me down a bit of a rabbit hole, looking into the differences between majoring in chemistry, biochemistry, chemical engineering, etc., with the goal of better understanding what sort of job prospects a bachelor’s degree in those areas might look like. To that end, I have looked at the job postings at assorted chemical and materials manufacturers (amongst other possible employers), including a company whose shares I’ve been invested in since September 2022, the Eastman Chemical Company (NYSE:EMN). I currently consider the shares a “hold” as shares are fairly valued. They have done very well for me on a total return basis, but I have paused adding to my position over the last 6 months.

Eastman Chemical, of course, carries the famous “Eastman” name of “Eastman Kodak” from photography, and that is not a coincidence, as it was spun out from the Kodak corporation in 1994, now some 30 years ago. Its origins, however, were tied to Kodak’s need for chemicals for developing photographs when such chemicals were difficult to come by during the First World War, but the chemical division has expanded far beyond that niche in the hundred years since then. Today, it is a significant supplier of specialty chemicals and materials, boasting an $11.5 billion market cap and over $9 billion in sales in 2023.

Review of 2023 Financial Results and Q1 2024

First quarter 2024 results were just released on April 25th, and management provided some guidance for full year 2024. Before getting into the 2024 early results, let me set the stage with a quick review of full year 2023.

Starting at a high-level overview, last year was not a topline growth year for Eastman Chemical, as revenue slipped to $9.2 billion, whereas the prior two years both had sales over the $10 billion threshold. Regardless, 2023 was a profitable year for the company; gross margins improved from 20% to 22%, SG&A expenses were kept in line, R&D expenses declined modestly, and there was a $323 million net benefit from the divesting of parts of the business, most significantly the sale of it Texas City operations that closed in December 2023. The ultimate result for shareholders in 2023 was diluted earnings per share of $7.49 on net income of $894 million.

Turning briefly to the Q1 2024 P&L, revenue was $2.3 billion, about $0.1 billion less than Q1 of 2023, with sales declining in each reporting segment (see below), but with stronger EPS of $1.39 versus $1.12 for the same period a year ago. Cash used in operations during Q1 was ($16 million).

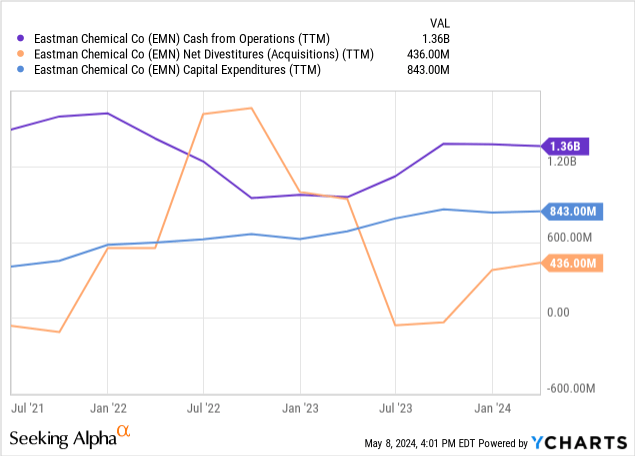

The 12/31/23 balance sheet did not see large changes compared to the year-end 2022 figures; most notable was the good working capital management on receivables and inventory and the $304 million increase to the book value of the firm’s equity to a total of $5.53 billion; other changes were fairly negligible in my estimation. In terms of cash flows, operating cash flow was a strong $1.37 billion for the year, versus $0.98 billion for 2022, on the back of the divestiture and working capital management benefits. With net CapEx of $432 million, free cash flow amounted to ~$942 million. This would prove to be more than enough to cover the dividend of $376 million, share buybacks of $150 million, extinguish some debt along the way, and add $55 million to the cash on hand at year-end.

The cash balance went in reverse during Q1 by ($49 million), ending at a balance of $499 million, as operations used ($16 million) and capex investing required an additional ($179 million). Cash was brought in from financing, with a net $148 million of cash after dividends of ($95 million).

Just going a little deeper, Eastman Chemical segments its reporting into four categories: 1) Advanced materials, 2) Additives and functional products, 3) Chemical intermediates, and 4) Fibers. Advanced materials and additive/functional products are the largest segments by sales, accounting for 32% and 31% of total sales, respectively, in 2023, with chemical intermediates then at 23% and fibers rounding out the list at 14%. For Q1, these breakdowns were essentially unchanged.

However, the sales proportions do not directly carry over to the profitability contributions; on an earnings before interest and taxes (EBIT) basis, advanced materials was the smallest contributor in 2023 at $343 million, while additives/functional products was the greatest at $436 million, essentially even with chemical intermediates at $434 million. Even fibers generated EBIT of $393 million off of sales of $1,295 million. So while advanced materials comprised the largest contribution to revenue for the year, they had the worst margin profile.

Recent and Ongoing Developments

The most significant of Eastman Chemical’s recent decisions has been to pour investment into greater recycling capacity for plastics that can be otherwise difficult to recycle. To that end, it has built molecular recycling capacity in Tennessee that recently began generating revenue, and Eastman intends to build two more of these plants: the world’s largest such facility will be in France, at an investment of about ~$1 billion, and another will be located in Texas, where Eastman has an existing plant, and that specific development is negotiating for as much as $375 million from US taxpayers through the Department of Energy’s disbursement of Inflation Reduction Act infrastructure funds.

As a specific example of the market opportunity for their process, when an automobile has reached the end of its useful life, the plastics were about the only thing that couldn’t be recycled. To quote their press release, their recycled automotive plastics were just as good as newly sourced plastics for going back into automotive uses:

These technologies break down plastic waste at the molecular level, so these recycled materials can be built back into new polymers that are indistinguishable from virgin materials with no trade-offs in performance or safety. Eastman’s carbon renewal technology (CRT) can recycle almost any plastic and was used to demonstrate closed-loop recycling for ASR [automotive shredder residue – the plastics and fibers taken from vehicles at the end of their useful life]. . . Using CRT, Eastman converted the ASR into materials used downstream in the production of new plastic resins. Finally, Yanfeng [a manufacturer of automobile interiors] molded Eastman resins into new automotive parts that met a variety of requirements established by three OEMs: Ford, GM and Stellantis.

There is opportunity here beyond the auto industry, but gives a bit of an idea of the quality of the process results, and clearly, the decision to invest substantial capital in expanding the availability signals Eastman’s confidence in the returns on that capital. The initial target is for ~$75 million in incremental EBITDA from the Tennessee facility even in 2024, signaling a clearly immediate and measurable contribution.

Allocation Priorities and Valuation

With the investment in the new recycling capacity referenced above costing well over $1 billion over the next couple of years, and being in addition to normal CapEx spending, checking in on the total picture of capital allocation priorities is a helpful place to start looking into the current valuation.

As far as how Eastman is managing to fund the $840 million in capex over the last year, it is variety of sources. Most significantly, operating cash flows were $1,360 million over that same period, supplemented by $440 million from divested assets and cash available of $599 million at the beginning of Q1 in 2023, for a total cash pool (not including financing) of something like $2,399 million. That’s a tidy sum to work from and allowed not only the necessary $840 million in investments, but $377 million in dividends returned to shareholders plus an additional $150 million in share repurchases, while simultaneously knocking down the debt load from $5,745 million a year ago, to $4,936 million at 3/31/24 (debt load being short-term borrowings, current portion of long-term debt, and long-term debt).

While relative to the end of Q1 in 2023, Eastman Chemicals is sitting on $100 million less in cash now than it had then, I believe it is operating from an overall position of strength.

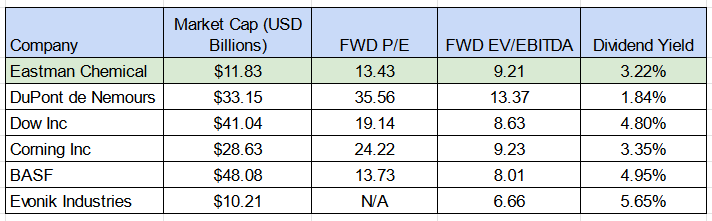

Of course, if the market already assumes that, then the company’s equity will be fairly valued if not valued at a premium. For a mature company within a fairly stable sector of the economy, I do think the forward P/E ratio and EV/EBITDA multiples are each reasonable starting points to think about valuation and see how Eastman Chemicals compares to some peers.

Select Valuation Comparisons for Eastman Chemicals (Author’s spreadsheet; data sourced from Seeking Alpha)

There is a wide array of public companies in the materials and chemicals sector, and I’ve just picked a handful from a cross-section. Eastman Chemicals does not especially stand out – an inexpensive P/E multiple, with an EV/EBITDA that is exactly at the average of this particular grouping, and a slightly below-average yield from its dividend. I think the main message here is that there is no glaring red flag suggesting the company is overvalued, but rather appears to be priced in line for its sector.

Risks

I believe the major risk for Eastman Chemical over the next year or so is that it will face ongoing major capex requirements involved in building two new recycling plants. This investment back into the business represents an exciting growth opportunity in an otherwise fairly stable and mature industry. However, like any major investment in physical facilities, there can be delays, cost overruns, and other uncertainties; many of the analyst questions on the Q1 earnings call with management revolved around these questions, specifically for the planned recycling plant in France which is delayed due to some shifting European Union regulations.

At the current timeline, the Texas plant would not be up and running until 2027, while the France facility is more up in the air. Market conditions can change a lot over the course of a few years – new technologies and competitors can pop up, or the expected economics payoff from the investments can falter for other unforeseen reasons. With the significant use of cash required, there would be an additional risk for shareholders that returns to shareholders from dividends or share buybacks could be constrained.

In the Q&A with analysts on the first quarter call, the Jeffries analyst posed the question to clarify around managing the balance sheet going forward, and received the following responses from Mark Costa, the CEO, and William McClain, the CFO (edited for length and clarity):

Mark Costa (CEO)

There’s always CapEx around [core maintenance], call that in the $350 million range. And then . . . investments we’re making in growing our capacity to serve all the different specialty markets we have . . . that takes you to with maintenance $500 million to $600 million range on CapEx. . . And we believe we have a balance sheet and a cash flow in place to fund all that. So, we don’t have to take on debt to do it, just to answer that question.

William McLain (CFO)

You’re seeing that as we updated our guidance on capital this year of being $700 million to $750 million and expecting share repurchases of $200 million to $300 million. . . We will continue to be disciplined in that capital allocation, and we expect to generate the cash flow to fund our strategy.

So the current plan is that the required investments in the new plants will not bring the share repurchase plan to a halt. The cash flow historically has been strong enough to cover all the claims on it, which mitigates the risks in my view.

Concluding Thoughts

I established a long position in Eastman Chemicals starting in the fall of 2022 and buying in small tranches in the fall of 2023, at prices more or less ranging between $72 and $82 per share, and have not been adding to my position since then, other than dripping the dividends. At the current value, I believe Eastman is fairly priced and does not represent an alpha-generating opportunity over the next 12 months. That said, I do like what the company is doing in terms of cutting-edge technology in polymer recycling and going after a unique growth window. From a valuation standpoint, I am comfortable recommending Eastman Chemical as a “hold,” but would likely be a buyer again on dips under $85, all else being equal.