Richard Drury

Introduction

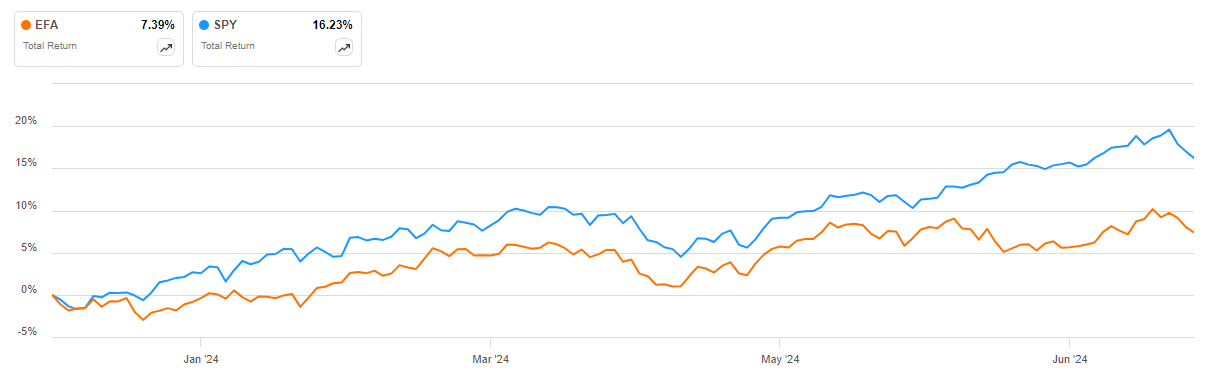

The iShares MSCI EAFE ETF (NYSEARCA:EFA) has underperformed the SPDR S&P 500 ETF (SPY) so far in 2024, delivering a mid-single-digit total return against the circa 16% gain in the benchmark ETF:

EFA vs SPY in 2024 (Seeking Alpha)

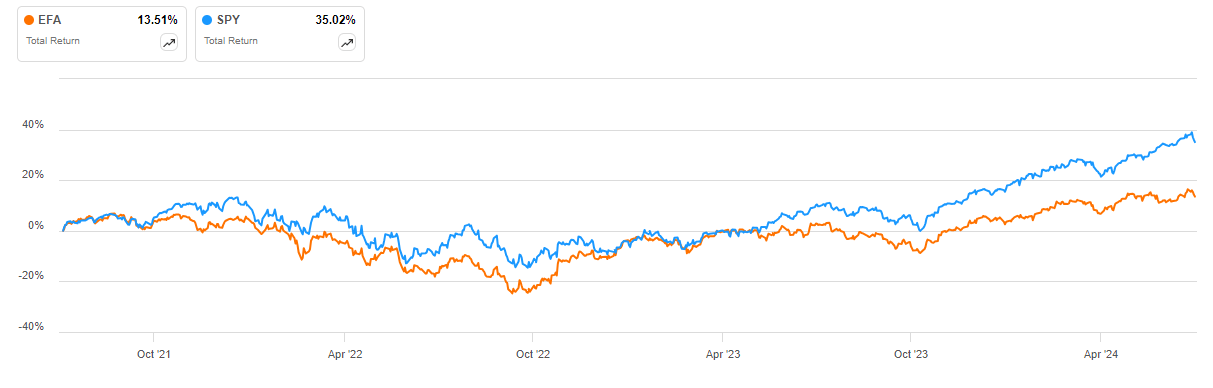

When we go back further in time, in the past three years the underperformance is even greater, at about 21%:

EFA vs SPY over the past three years (Seeking Alpha)

This underperformance has led to a material valuation discount in EFA versus the SPY. Furthermore, the case for adding EFA exposure is strengthened when you consider the strong performance of the US dollar recently and the potential unwind of the carry trade as the Fed cuts rates. As a result, I think the EFA ETF is likely to outperform the SPY ETF over the next few years.

ETF Overview

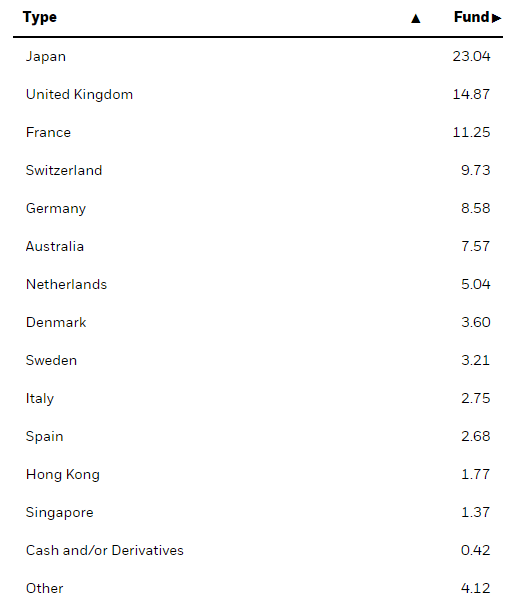

You can access all relevant EFA information on the iShares website here. The iShares MSCI EAFE ETF tracks large and mid-cap companies outside the United States and Canada. From a geographic perspective, the largest allocation is to Japan (23.04% of net assets), followed by the United Kingdom (14.87%) and France (11.25%):

Portfolio breakdown by country (iShares website (Accessed July 2024))

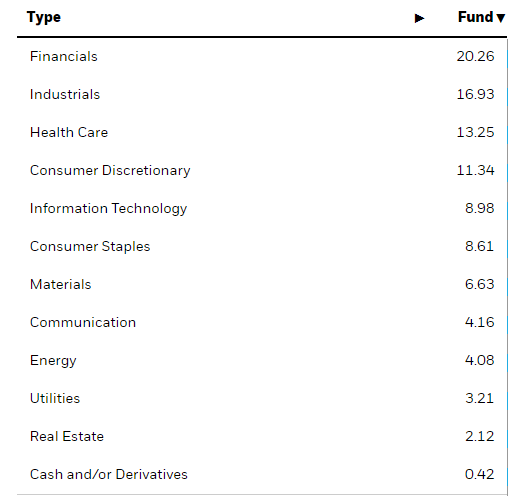

From a sector perspective, the main allocation is to financials (20.26% of net assets), followed by industrials (16.93%) and health care (13.25%):

Portfolio breakdown by sector (iShares website (Accessed July 2024))

Holdings and diversification

The portfolio is spread across some 745 positions, with the full list available here. The top ten positions account for about 15.29% of all net assets, lower than the current 35.01% allocation to the top ten positions in the SPDR S&P 500 ETF. As a result, the EFA ETF is much more diversified. You have to pay a bit for the superb diversification though – the expense ratio of EFA stands at 0.33%, still acceptable for a long-term passive holding but well above the 0.0945% SPY expense ratio.

Valuation

The current P/E ratio of EFA holdings stands at just 15.86, implying an earnings yield of 6.31%, about 6% adjusted for the elevated expense ratio. In contrast, the SPY P/E sits at 23.10, or an earnings yield of about 4.2% after expenses. Clearly, S&P 500 earnings would have to grow by about 1.8% higher annually to compensate for the current valuation gap – something I don’t think is likely over the long term.

Currency considerations

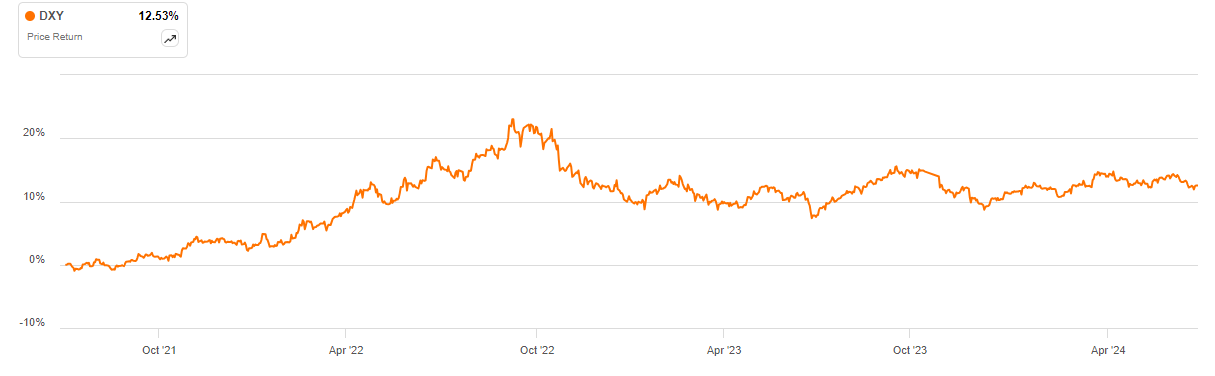

The US Dollar Index (DXY) has gained about 12.5% in value over the past three years:

US Dollar Index over the past three years (Seeking Alpha)

As a result, not only have US large caps outperformed their international competitors over the past three years, but the dollar has appreciated as well (of course since EFA is traded in USD some of the outperformance is due to dollar strength). I think this may be due to the large interest rate differential that emerged with the Fed rate rising cycle in 2022-2023. While rates in the United Kingdom are comparable to those set by the Fed, they are lower in the Eurozone and materially lower in Japan. As a result, as the Fed looks set to cut interest rates over the next few years, some of this interest rate differential may diminish, potentially unwinding part of the carry trade that fueled the US Dollar Index’s rise over the past three years.

Distributions

The iShares MSCI EAFE ETF pays a dividend twice a year – in June and December. The current dividend of about 2.92% is considerably more attractive than the 1.25% yield on the SPY. Of course, part of the difference can be explained not only by lower valuations, but also by the domination of share buybacks in the US markets – something which is not the case for international equities.

Risks

One key risk to consider when investing in EFA is that it has a 20.26% allocation to financial stocks, considerably higher than SPY’s 12.87% allocation to the sector. Given the outlook for interest rates to decline across the globe, EFA earnings may suffer to a greater extent compared to the SPY.

Another risk to mention is the quite significant allocation of EFA to Japan, which has low potential growth due to its declining population. In contrast, the US is expected to see strong population growth, largely due to immigration.

The issue of earnings growth is potentially central to the EFA investment case. If SPY earnings growth does outperform EFA over the long term (by at least 1.8% annually, as highlighted above), the low P/E ratio of EFA stocks may turn out to be a value trap.

Conclusion

The iShares MSCI EAFE ETF has underperformed the SPY ETF both in 2024 and over a three-year time frame. This outperformance of US stocks was combined with a strong dollar. While there is an argument to be made that growth in the United States will be higher than in international markets, specifically Japan, the discount the EFA ETF trades at is arguably too high. As a result, I think it may be wise for US investors to add some international exposure with the EFA ETF. The potential return is in the high single digits, driven by a mid-single-digit earnings yield, an inflationary component of about 2%, and perhaps some pullback in the US dollar as the Fed cuts interest rates.

For international investors, it may also make sense to increase their allocation to the EFA ETF as it may shield them from potential dollar weakness, especially if they have benefitted from the SPY outperformance in 2024 and over the past three years.

Thank you for reading.