haydenbird

The Western Asset Global High Income Fund (NYSE:EHI) is a closed-end fund that can be employed by investors who are seeking to earn a very high level of income from the assets in their portfolios. As the name of the fund suggests, the Western Asset Global High Income Fund has a global focus, which can be advantageous during times in which interest rates in foreign countries are higher than they are in the United States. That is not the case today, though, as the United States has the highest benchmark rate of any developed country, but it is still lower than that possessed by most emerging markets. Another advantage that this fund has over that of many other income-focused closed-end funds is that it can help an investor achieve some international diversification in their portfolios. In various previous articles, I have discussed why this is important today. Fortunately, investors in this fund do not need to sacrifice yield to obtain these potentially advantageous features, as the Western Asset Global High Income Fund boasts an 11.77% yield at the current share price. As we can see here, this yield compares very well to that of the fund’s peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Western Asset Global High Income Fund |

Fixed Income-Taxable-High Yield |

11.77% |

|

AllianceBernstein Global High Income Fund (AWF) |

Fixed Income-Taxable-High Yield |

7.37% |

|

PGIM Global High Yield Fund (GHY) |

Fixed Income-Taxable-High Yield |

10.51% |

|

BrandywineGLOBAL – Global Income Opportunities Fund (BWG) |

Fixed Income-Taxable-Global Income |

11.46% |

|

First Trust/abrdn Global Opportunity Income Fund (FAM) |

Fixed Income-Taxable-Global Income |

11.29% |

|

Nuveen Global High Income Fund (JGH) |

Fixed Income-Taxable-Global Income |

9.62% |

As we can see, the Western Asset Global High Income Fund has the highest yield among this group of peers that also invests in speculative-grade debt from issuers that are located all over the world. This is something that many income investors might find appealing. After all, one of our biggest goals is to maximize the income that we can earn from our portfolios. However, an outsized distribution yield can also be a sign that the fund is paying out more money than it actually earns from its assets, so we should investigate the fund further.

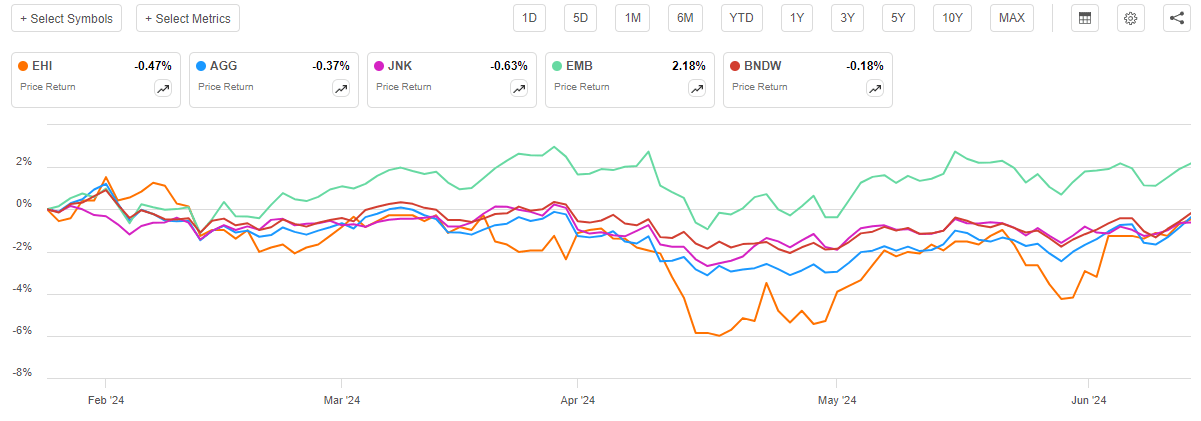

As regular readers can likely remember, we previously discussed the Western Asset Global High Income Fund back in late January 2024. The domestic bond market has been fairly weak since that time, as various market participants have come to realize that they were wrong about the course that interest rates would take in 2024. However, some foreign bond markets have held up pretty well due partly to rate cuts in Canada and Europe plus a declining U.S. dollar that encouraged capital flows into emerging market debt. As such, we might expect that the shares of the Western Asset Global High Income Fund have given a mixed performance since our last discussion. That is indeed the case, as shares of the fund are down 0.47% since the time of our last discussion:

Seeking Alpha

As we can see, this performance is actually pretty much in line with that of most developed market bond indices:

|

Index |

% Return Over Period |

|

Bloomberg U.S. Aggregate Bond Index (AGG) |

-0.37% |

|

Bloomberg High Yield Very Liquid Index (JNK) |

-0.63% |

|

Vanguard World Bond Index (BNDW) |

-0.18% |

However, the Western Asset Global High Income Fund did substantially underperform emerging market bonds (EMB), as that index was up 2.18% over the period in question. We can also see that there are periods in which the Western Asset Global High Income Fund was underperforming the developed market indices to a fairly large degree, but it regained those declines. Overall, the fund’s share price performance was not necessarily what we would have wanted to see over a roughly five-month period, but it was not generally out of line with the market.

With that said, nobody likes to lose money, and the fund’s recent share price performance is certainly disappointing in that respect. However, as I pointed out in a previous article:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

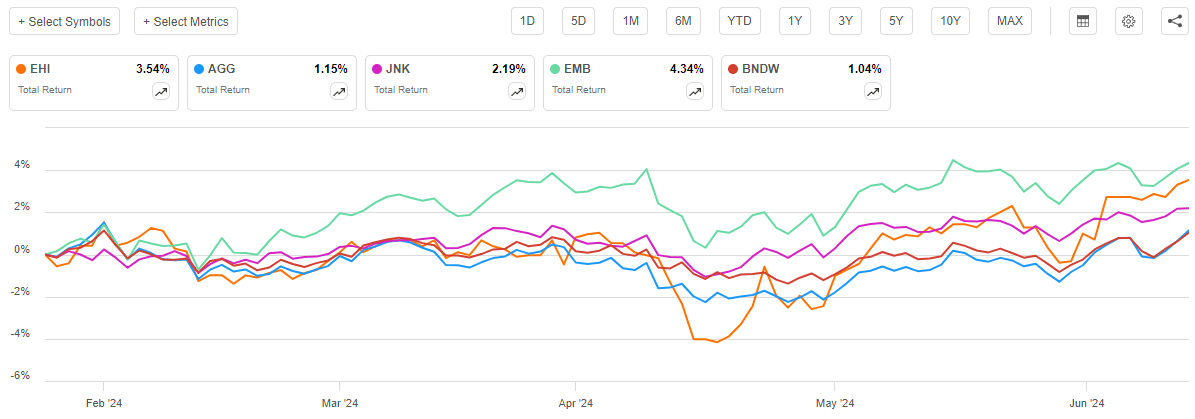

The distributions paid by the Western Asset Global High Income Fund were more than sufficient to offset the small share price decline that we saw over the past five months. As we can see here, on a total return basis, this fund outperformed all of the indices except for emerging market bonds:

Seeking Alpha

This chart also includes all of the distributions paid out by the bond indices, which was also sufficient to offset all of their price declines as well. Clearly, though, the fact that the Western Asset Global High Income Fund has a much higher yield than any of the bond indices worked to its advantage here. The fact that investors ultimately made money over the past five months should provide a certain amount of comfort even to the most risk-averse investors.

While only five months or so have passed since the last time we discussed this fund, a great deal of changes have taken place in the markets. In particular, recent data suggests that the economy of the United States has started to weaken, and the Federal Reserve has made it clear that interest rates will not be decreased to any significant degree this year. Indeed, the dot plot that the Federal Open Market Committee presented after this week’s meeting predicts only a single interest rate cut this year, along with permanently higher interest rates than existed over the past twenty years or so. Most importantly for this fund though is the fact that it released an updated financial report. We will want to pay special attention to this report as we conduct our analysis into whether or not purchasing this fund makes sense today.

About The Fund

According to the fund’s website, the Western Asset Global High Income Fund has the primary objective of providing its investors with a high level of current income. As is usually the case with Franklin Templeton funds (Western Asset is a manager affiliated with Franklin Templeton), the website does not go into any great detail about how the fund will achieve its objective. Rather, all the website states is:

[The Fund] provides a global, leveraged portfolio of investment grade, below investment grade and emerging market fixed-income securities.

As I pointed out in the previous article on this fund, fixed-income securities in general are income vehicles:

This strategy does fit pretty well with an income-focused objective. After all, bonds are by their very nature income vehicles since the only net investment returns that they deliver over their lifetimes are coupon payments made to their owners. These coupon payments essentially provide a source of income for the owner of the bond, which in this case is the fund. The fund collects these payments and distributes them to its shareholders. While it is true that bond prices will vary with interest rates and other factors and that allows for the possibility of earning capital gains by trading bonds, over the life of a bond, these gains and losses all net out to zero. This is because anyone who purchases a new issue bond and holds it until maturity will receive nothing more than the regular coupon payments.

The fund’s description states that it can invest in pretty much any fixed-income securities that it wants, with no requirements that the issuers come from the United States, a developed nation, or an emerging nation. The fund’s description also does not appear to differentiate between corporate and sovereign issuers, which suggests that it can invest in either. However, the third-quarter 2024 holdings report strongly implies that the Western Asset Global High Income Fund invests in corporate bonds. According to this document, the fund had the following asset allocation on February 29, 2024:

|

Asset Type |

% of Net Assets |

|

Corporate Bonds |

109.3% |

|

Sovereign Bonds |

20.4% |

|

Senior Loans |

4.4% |

|

U.S. Government and Agency Obligations |

2.8% |

|

Convertible Bonds and Notes |

1.7% |

|

Collateralized Mortgage Obligations |

1.6% |

|

Warrants |

0.0% |

|

Common Stocks |

0.0% |

|

U.S. Treasury Bills |

3.9% |

|

Money Market Funds |

0.6% |

We can clearly see the effects of the leverage employed by the fund as the corporate bonds alone account for more than 100% of the fund’s holdings. This is fairly typical for closed-end bond funds though, so there is nothing unusual here.

One thing that is very important to note is that the Sovereign Bonds category shown in the table above only consists of foreign government bonds. The U.S. bonds held by the fund are entirely broken down into separate categories. For the most part, the sovereign bonds are very well diversified, as there are no countries whose sovereign debt accounts for a particularly large proportion of the fund’s total:

|

Country |

% of Net Assets |

|

Angola |

0.6% |

|

Bahamas |

0.2% |

|

Columbia |

1.4% |

|

Costa Rica |

0.3% |

|

Dominican Republic |

1.4% |

|

Ecuador |

0.1% |

|

Egypt |

0.9% |

|

Indonesia |

0.6% |

|

Ivory Coast |

0.8% |

|

Jamaica |

0.4% |

|

Jordan |

0.5% |

|

Kenya |

0.3% |

|

Mexico |

4.3% |

|

Nigeria |

1.2% |

|

Oman |

1.0% |

|

Panama |

0.8% |

|

Peru |

1.2% |

|

Philippines |

0.4% |

|

Qatar |

0.9% |

|

Senegal |

0.2% |

|

Supranational |

0.5% |

|

Turkey |

1.3% |

|

Ukraine |

0.3% |

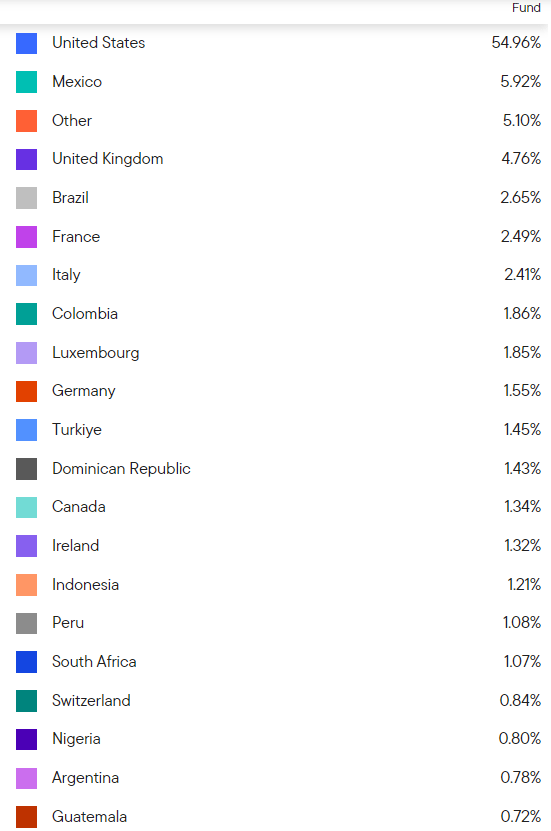

With the notable exception of the Mexican sovereign bonds, all of which mature between 2031 and 2034, there is no individual country whose representation exceeds 1.5% of net assets. However, the corporate bonds that are held by this fund also come from issuers that are located around the world. The Western Asset Global High Income Fund does not invest solely in American issuers. When we include those entities, we get a somewhat different country allocation:

Franklin Templeton

We see quite a few countries here whose sovereign bonds are not even included in the fund. Perhaps the most notable of these are the United Kingdom, several countries in the Eurozone, Switzerland, and Canada. It is admittedly a bit surprising that the fund would invest in corporate debt issued by these nations, but not in their sovereign debt. One possible reason for this might be that most developed nation sovereign debt has unattractive interest rates. For example, let us take a look again at the list of countries whose debt is included in the fund, this time adding their benchmark interest rates to the list:

|

Country |

% of Net Assets |

Benchmark Interest Rate |

|

Angola |

0.6% |

19.50% |

|

Bahamas |

0.2% |

4.00% |

|

Columbia |

1.4% |

11.75% |

|

Costa Rica |

0.3% |

4.75% |

|

Dominican Republic |

1.4% |

7.00% |

|

Ecuador |

0.1% |

10.87% |

|

Egypt |

0.9% |

27.25% |

|

Indonesia |

0.6% |

6.25% |

|

Ivory Coast |

0.8% |

5.50% |

|

Jamaica |

0.4% |

7.00% |

|

Jordan |

0.5% |

7.50% |

|

Kenya |

0.3% |

13.00% |

|

Mexico |

4.3% |

11.00% |

|

Nigeria |

1.2% |

26.25% |

|

Oman |

1.0% |

6.00% |

|

Panama |

0.8% |

N/A |

|

Peru |

1.2% |

5.75% |

|

Philippines |

0.4% |

6.50% |

|

Qatar |

0.9% |

6.25% |

|

Senegal |

0.2% |

5.50% |

|

Supranational |

0.5% |

N/A |

|

Turkey |

1.3% |

50.00% |

|

Ukraine |

0.3% |

13.00% |

Panama does not have a central bank, so it does not have a benchmark interest rate. The Panama sovereign debt held by the fund has a coupon rate of 2.252%. The current yield is obviously well above that, as they have a face value of $1.89 million but only traded at $1.329 million on February 29, 2024.

Admittedly, these benchmark interest rates will only apply to local currency bonds, but the Western Asset Global High Income Fund invests solely in hard currency bonds that are denominated in U.S. dollars. In many cases, these bonds have lower interest rates than the local currency bonds but they are still much higher than developed nation sovereign bonds. Let us have a look at the interest rates of the sovereign nations that I pointed out just a few minutes ago:

|

Nation |

Benchmark Interest Rate |

|

United Kingdom |

5.25% |

|

Eurozone |

4.25% |

|

Canada |

4.75% |

|

Switzerland |

1.50% |

We can very quickly see how investing in sovereign bonds from emerging market nations provides this fund with a much higher level of interest income than it would get from purchasing sovereign securities from any developed market nation. Corporate bonds tend to have higher interest rates than sovereign nations, so including them can still make sense for the fund’s objective of maximizing its income.

One thing that eagle-eyed readers might notice is that the fund’s allocation to the United States has increased since the last time that we discussed it. As we saw back in January, the Western Asset Global High Income Fund only had 50.66% of its assets invested in the United States on that date. As we saw in the introduction to this article, both the Vanguard World Bond Index and the JPMorgan EMBI Global Core Index (emerging market bonds) outperformed domestic bonds over the period since we last discussed this fund so the increased allocation to American bonds appears to be a deliberate choice on the part of the fund’s management.

As regular readers know, my general thesis right now is that the U.S. dollar is likely to decline in value over the coming years as inflationary pressures from high Federal deficits push it down against emerging market currencies that have balanced government budgets and more rapidly growing economies. Adherents to this thesis would tell you that the fund increasing its allocation to U.S. debt is a mistake. In the long term, it will very well be.

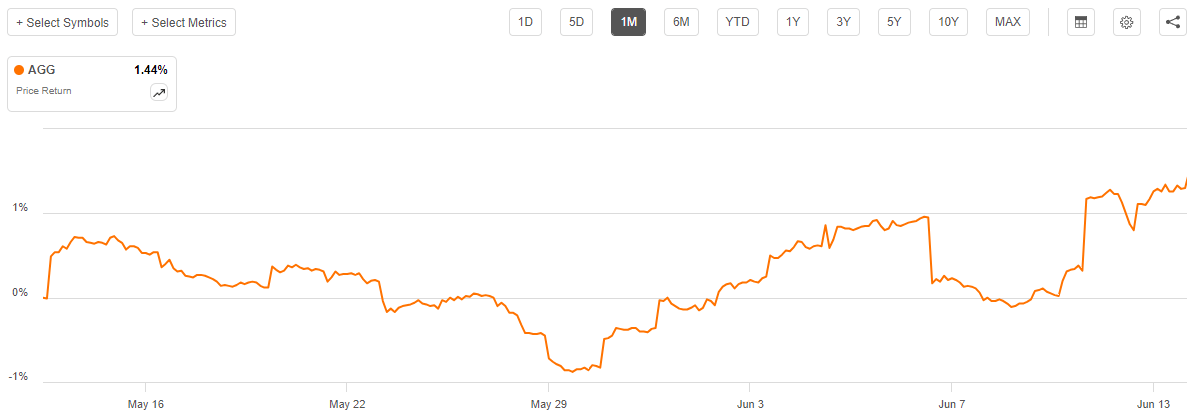

However, that does not mean that the fund’s management increasing its exposure to American debt is a bad move as a short-term trade. In a recent article, I pointed out that there has been something of a fear trade going on over the past few days. There are signs that the American economy has started to slow down, and the recent interest rate cuts by the Bank of Canada and European Central Bank have imparted downward pressure on their currencies. The Federal Reserve made it very clear this week that it will be standing pat, which has resulted in a carry trade opportunity. Investors who are fearful will frequently sell off risk assets and buy U.S. bonds, and this seems to be happening right now. This will push up the price of domestic bonds. The Bloomberg U.S. Aggregate Bond Index is up 1.04% over the past month, and it has risen over the past few days despite the Federal Reserve being very clear that the market is far too optimistic about the potential for near-term interest rate cuts:

Seeking Alpha

Thus, there could be a trading opportunity here that the fund could take advantage of by increasing its exposure to domestic bonds. The increase in U.S. bonds that we see in the fund today compared to a few months ago is therefore not necessarily problematic for our overarching thesis as it may simply be a short-term trade.

Leverage

As we saw earlier, the Western Asset Global High Income Fund employs leverage in its investment strategy. I explained how this works in my previous article on the fund:

Basically, the fund borrows money and then uses that borrowed money to purchase debt securities issued by entities located in both the United States and various foreign nations. As long as the yield that the fund receives from these purchased securities is higher than the interest rate that it has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, it is important to note that the use of leverage as a method of boosting yields is less effective today than it was a few years ago. This is because it is much more expensive to borrow money today than it has been over most of the past decade, which has resulted in the difference between the yield of the purchased assets and the interest rate that the fund has to pay on the borrowed money being narrower than it once was.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage in its strategy since that would expose us to an unacceptable level of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

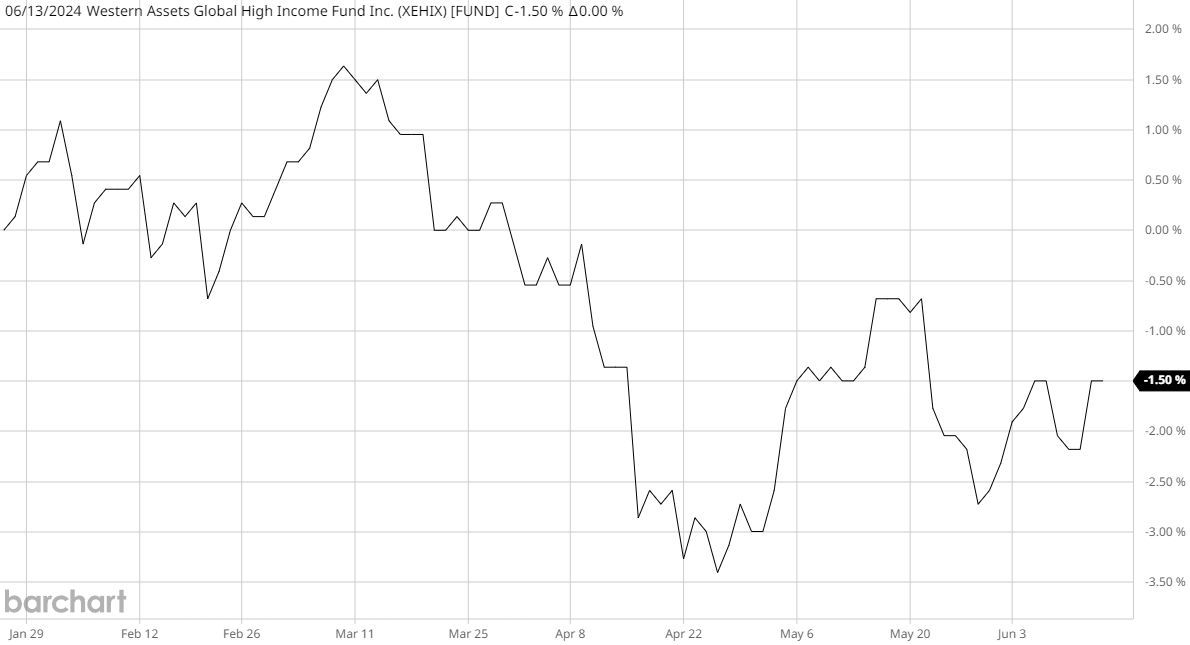

As of the time of writing, the Western Asset Global High Income Fund has leveraged assets comprising 34.53% of its portfolio. This is a very steep increase from the 31.31% leverage ratio that the fund had the last time that we discussed it. One reason for this is that the fund’s net asset value declined since the time of our previous discussion:

Barchart

As we can immediately see, the fund’s net asset value declined by 1.50% since our discussion on January 25. This is greater than the decline in the fund’s share price, which has an impact on the fund’s valuation. We will discuss that later. For now, though, the decline in the net asset value means that the same amount of borrowed money is now a higher percentage of the portfolio. It seems unlikely that a 1.50% decline in the fund’s net asset value would increase its leverage by 3.22% though, so the fund might have borrowed more money at some point over the past few months. This naturally could increase its volatility.

Here is how the current leverage ratio of the Western Asset Global High Income Fund compares to that of its peers:

|

Fund Name |

Leverage Ratio |

|

Western Asset Global High Income Fund |

34.53% |

|

AllianceBernstein Global High Income Fund |

19.01% |

|

PGIM Global High Yield Fund |

21.54% |

|

BrandywineGLOBAL – Global Income Opportunities Fund |

42.31% |

|

First Trust/abrdn Global Opportunity Income Fund |

19.78% |

|

Nuveen Global High Income Fund |

27.92% |

(all figures from CEF Data)

This could be somewhat concerning. As we can see, the Western Asset Global High Income Fund has a significantly higher level of leverage than all except for one of its peers. This might suggest that the fund is using too much leverage and exposing its investors to a higher level of risk than it should. Potential investors may want to keep this in mind before purchasing shares of the fund.

Distribution Analysis

The primary objective of the Western Asset Global High Income Fund is to provide its investors with a high level of current income. To that end, the fund pays a monthly distribution of $0.0700 per share ($0.84 per share annually). This gives the fund an 11.77% yield at the current share price.

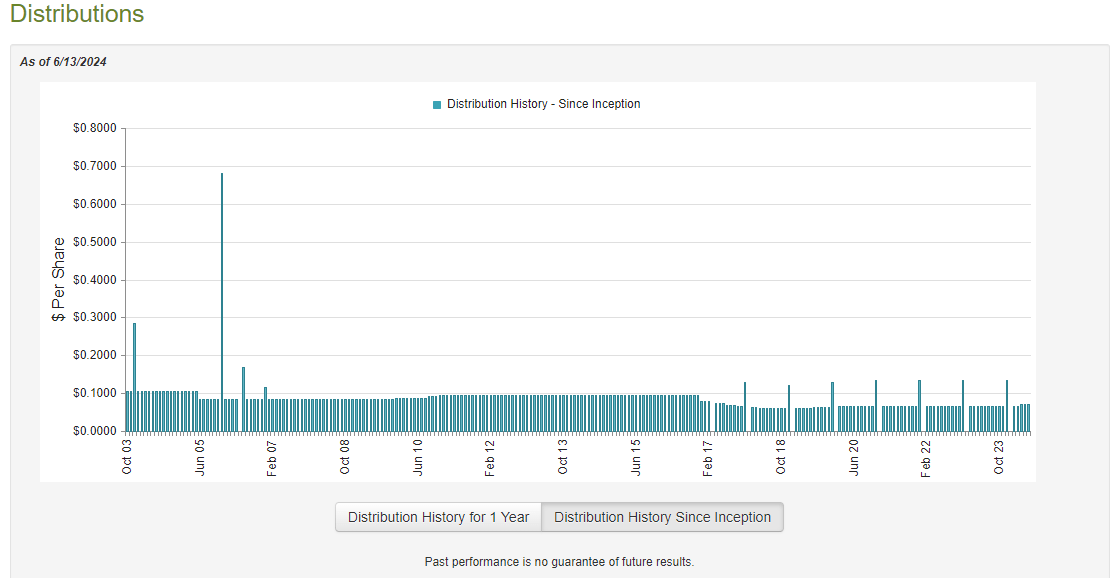

The fund has been somewhat consistent with respect to its distribution over the years, but it has not been perfect:

CEF Connect

As I stated in the previous article on this fund:

This distribution history might reduce the fund’s appeal in the eyes of those investors who are seeking to earn a safe and consistent income to use to pay their bills or finance their lifestyles. However, it is not nearly as bad as other bond funds that have changed their distribution on a much more frequent basis. In particular, we can see that the fund did not change its distribution in response to the global change in monetary policy in 2022, which makes it one of the few funds that invests in fixed-rate bonds that managed to maintain a stable distribution in that environment. This is something that we should investigate though, as it seems strange that this fund was able to accomplish a feat that few of its peers were able to accomplish.

The fund increased its distribution slightly (from $0.067 per share to $0.070 per share monthly) since the last time that we discussed it, so that makes it even more important that we have a look at its finances and see how well it is covering its distributions.

As of the time of writing, the most recent financial report available for the Western Asset Global High Income Fund is the semi-annual report that corresponds to the six-month period that ended on November 30, 2023. This report is, unfortunately, not as new as we might like because it does not include any information about the fund’s performance over the past six months. However, it is still newer than the report that we had available to us the last time that we discussed this fund, so it should be able to provide us with an update.

For the six-month period that ended on November 30, 2023, the Western Asset Global High Income Fund received $10,864,986 in interest and $37,751 in dividends from the assets in its portfolio. From this total, we subtract the money that the fund had to pay in foreign withholding taxes. This gives it a total investment income of $10,883,655 for the period. The fund paid its expenses out of this amount, which left it with $7,279,893 available for shareholders. That was not sufficient to cover the $9,132,906 that the fund paid out in distributions during the period.

Fortunately, the fund was able to make up the difference through capital gains. For the six-month period, the Western Asset Global High Income Fund reported net realized losses of $12,212,716 but these were fully offset by net unrealized gains of $14,693,860. Overall, the fund’s net assets increased by $762,561 after accounting for all inflows and outflows during the period.

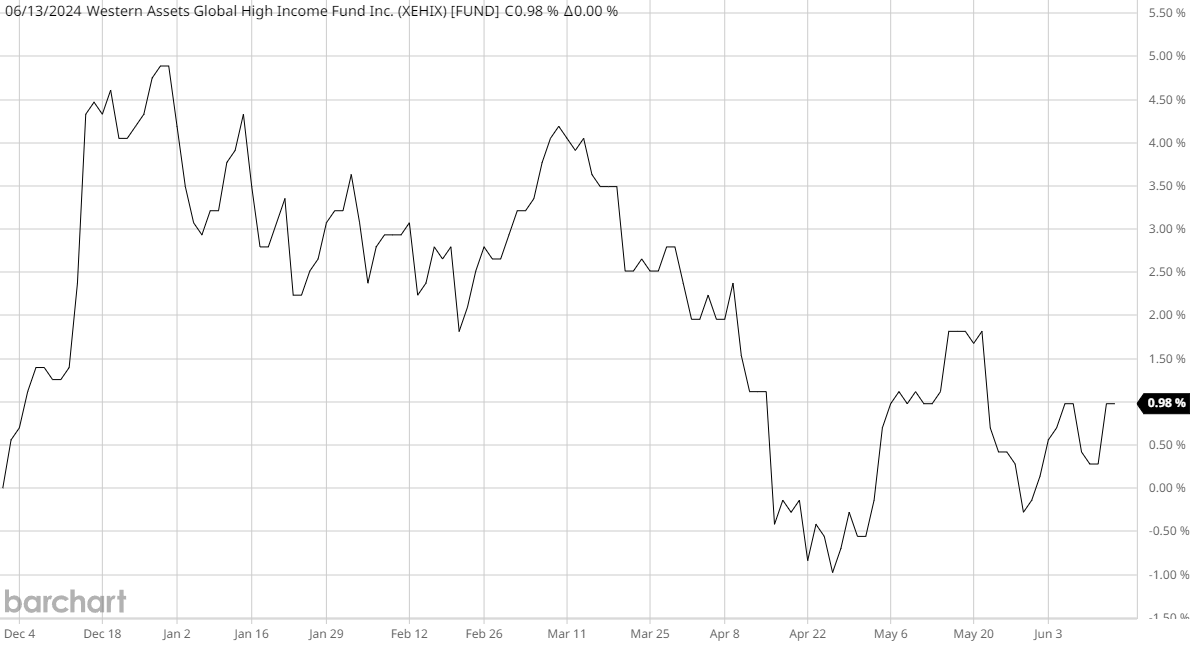

Thus, it appears as though the fund managed to fully cover its distributions during the period. However, as we all know, unrealized capital gains are not necessarily permanent as they can be erased by adverse market movements. Fortunately, this does not seem to be the case with this fund right now. This chart shows the fund’s net asset value from November 30, 2023 (the closing date of its most recent financial report) until today:

Barchart

As we can see, the fund’s net asset value has increased by 0.98% since the close of its most recent financial report. This means that the fund has fully covered all of the distributions that it has paid out since that date.

Valuation

Shares of the Western Asset Global High Income Fund are currently trading at a 1.38% discount on net asset value. This is a lot more expensive than the 2.93% discount that the shares have had on average over the past month. As such, potential investors might be able to obtain a more attractive entry price by waiting for a bit. The current price is still a discount, though, so it is not horrible.

Conclusion

In conclusion, the Western Asset Global High Income Fund is a reasonable way for investors to gain a very high level of income along with some international exposure. The fact that the fund only has a bit more than half of its assets invested in domestic bonds is nice for those seeking to improve this aspect of their portfolios. The fund has, however, increased its domestic exposure over the past few months. It is not certain if that will be permanent, or if it is simply trying to take advantage of the flight to safety that seems to be occurring in the market right now. The fund is also fully covering its distribution and trades at a discount, so it is definitely worthy of a hold rating.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.