Ethan Miller

Impartial ranking on El Pollo Loco (NASDAQ:LOCO) this month. By way of intensive analysis, evaluation, and insider talks, it grew to become obvious that our preliminary speculation for a “buy” ranking didn’t materialize. Our precept: if we don’t add it to our portfolio, no “buy” ranking. Regardless of missing pleasure, impartial rankings are important for credibility and observe file.

Thesis

El Pollo Loco, a California-based fast-food chain, initially caught our consideration by our particular dividend and worth screens. The preliminary setup appeared promising: the valuation appeared enticing on an absolute foundation, it was a model we had been accustomed to, confirmed progress potential, had diligently lowered substantial debt post-IPO, aligned with sure traits, and the promoting strain from its giant non-public fairness proprietor gave the impression to be waning. Nevertheless, deeper analysis raised doubts, main us to query the enterprise’s sustainability. We underestimated the fierce competitors within the fast-food business, and it wasn’t till we gathered pricing information that we realized El Pollo Loco’s aggressive place fell brief. Regardless of a number of potential alternatives, the record of negatives led us to assign it a impartial ranking.

Firm Background

El Pollo Loco, a well-established fast-food chain based in 1975 by Juan Francisco Ochoa in Guasave, Sinaloa, Mexico, gained recognition through the years within the higher Los Angeles area and throughout California. Nevertheless, progress outdoors of California has been inconsistent, with about 80 models added since going public in 2014.

LOCO Filings

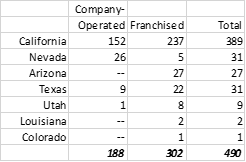

El Pollo Loco distinguishes itself out there by positioning it as a Mexican-style QSR+ (Fast Service Restaurant, aka Quick Meals) model, aiming to bridge the hole between conventional fast-food chains like Taco Bell and fast-casual eating places like Chipotle. They imagine their high quality flame-grilled rooster justifies premium pricing relative to different fast-food chains. The desk under illustrates El Pollo Loco’s common unit economics in comparison with opponents.

Pernas Analysis and Firm Filings

El Pollo Loco’s common verify sizes are notably greater, and its visitors tends to be decrease than opponents. Historically, they’ve adhered to their core choices with restricted menu improvements and have been sluggish to undertake digital improvements like gross sales by kiosks and apps. Roughly 25% of their gross sales come from carry-out, 25% from dine-in, and the remainder from the drive-thru. Gross sales are roughly evenly cut up between lunch and dinner, with supply providers like DoorDash and Uber Eats contributing 8% of gross sales (All information sourced from transcripts and the most recent filings).

The possession of El Pollo Loco has modified palms through the years, with American Securities Capital Companions (ASCP) buying the corporate in 1999 from Denny’s, adopted by its sale to Trimaran Capital Companions in 2005, and later its IPO in 2014. The corporate has witnessed a number of CEO modifications lately and is at present looking for a brand new chief, most definitely from outdoors the group.

Alternatives

Digital Gross sales Penetration

Opponents have seen common verify will increase of roughly 10% when prospects order by digital means like in-store kiosks. Clients are likely to order extra when the menu is available, which makes growing LOCO’s digital penetration a probably vital worth enhancement alternative.

Tendencies

With a concentrate on grilled rooster, El Pollo Loco gives a more healthy possibility in comparison with its QSR friends. Rooster consumption within the U.S. surpassed beef in 1993 and continues to develop. Moreover, the pattern of Hispanicization within the U.S., with Hispanics predicted to make up almost one-third of the inhabitants in 20 years (supply: Pew Analysis), makes it simpler to popularize Mexican delicacies and the El Pollo Loco model.

Enlargement Alternative

El Pollo Loco’s presence in america continues to be underdeveloped. Given the recruitment of high-quality management, the corporate might probably compete efficiently in quite a few new markets, enhancing its economics.

Value Pressures Softening

Whereas the restaurant business has confronted challenges from rising labor and commodity prices, these pressures are beginning to ease. Poultry, which constitutes 40% of El Pollo Loco’s enter prices, is predicted to see value decreases, which can positively influence their backside line. These price reductions have but to completely mirror on margins, as most QSRs have probably locked in provide contracts for a number of quarters.

Headwinds

Competitors

The restaurant business is mature, with progress anticipated to align carefully with GDP progress at round 2%. To attain significant progress, gamers should seize market share. Properly-capitalized opponents with robust digital experiences have outperformed others, particularly within the QSR section. Gamers like YUM manufacturers are investing closely and transferring in direction of 100% digital gross sales. In a high-priced labor market, well-capitalized gamers with scale benefits have the higher hand over smaller opponents like LOCO.

Labor Laws

California’s laws to boost the minimal wage for fast-food staff to $20 an hour, efficient April 1, 2024, will strain LOCO’s margins. Provided that 80% of their models are concentrated in California, we estimate a margin influence of 100-150bps.

Tormented by Poor Technique

Whereas monetary info has been publicly obtainable since their 2014 IPO, prior debt safety registrations reveal substantial pre-IPO info. Over the past 20 years, LOCO has skilled flat to 2% visitors progress, with most same-store gross sales will increase attributed to cost hikes. Beneath is from the newest CEO early this yr discussing their pricing technique:

“I go back historically….we’ve never played the discount game that others play. Others may go really aggressive on discounts and we just haven’t gone there just because it’s detrimental to the brand. And quite frankly, we believe our consumers understand the value they’re getting for the way we prepare our food in restaurant”

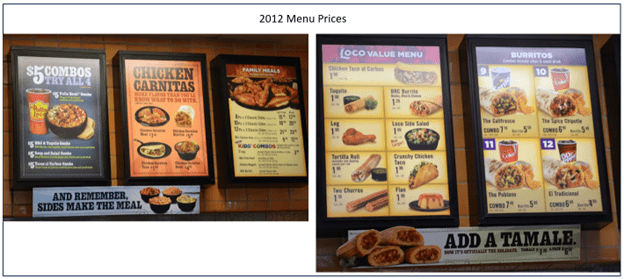

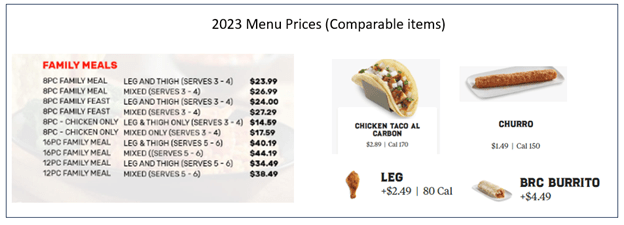

On the floor, this technique seems affordable, however provided that the standard certainly surpasses that of the competitors and the pricing aligns with this perceived worth. Whereas we acknowledge that El Pollo Loco gives greater meals high quality than most QSRs, we contend that their pricing has escalated considerably past the worth. This case arguably makes El Pollo Loco some of the aggressive value takers within the QSR class over the previous decade. As an example this level, we will look at two snapshots: pricing information from El Pollo Loco captured by a blogger in 2012 in comparison with the newest obtainable pricing (hyperlink here).

LOCO menu LOCO menu

Worth menu objects just like the Taco Al Carbon have seen a cumulative improve of 189% over the interval, a single drumstick has risen by 149%, and the BRC burrito has surged by 248%! Burritos and churros have skilled a extra modest improve of roughly 50% over the identical interval. Their core household meal providing, the 12-piece combined, has jumped by roughly 60%, going from $24 to $38. (Sooner or later, fast-food costs of $40 or greater for a household meal could generate sticker shock.) Whereas a good portion of those value hikes may be attributed to post-COVID inflation and pre-IPO changes, LOCO has constantly employed value will increase to counterbalance sluggish visitors progress. We estimate that, on most objects, they’ve averaged annual value will increase of 4-8% over the past 11 years.

Above all, to stay aggressive, QSRs should allocate a portion of their menu to cater to value-conscious customers. LOCO’s failure to take action has led them into direct competitors with fast-casual chains like Chipotle, identified for providing higher-quality meals. What makes their mistake much more obtrusive is the competitors from grocery shops that promote a comparable merchandise to their bone-in chickens—rotisserie chickens. Notably, Costco has effectively managed its rooster provide chain, sustaining a $4.99 rotisserie rooster value for many years. These chickens sometimes function as loss leaders for many grocery shops and are priced considerably decrease in comparison with LOCO.

To their credit score, they’ve made latest makes an attempt to introduce extra value-oriented objects like their five-dollar rooster bowls. Nevertheless, we contemplate these efforts to be inadequate and arriving too late. El Pollo Loco faces a deeply rooted notion drawback that may solely be addressed by menu innovation, substantial advertising funding, and efficient administration. Sadly, the corporate has displayed restricted indications that it’s ready for this problem.

Conclusion

There are too many negatives for us to justify an initiation. In the end, El Pollo Loco’s story is one in every of missed alternatives. With the suitable administration, they may have outpaced Chipotle and gained nationwide recognition, however they did not seize the second. Timing is essential within the QSR business, particularly for franchises, the place increasing during times of rising model recognition attracts the very best franchisees, improves retailer economics, drives recognition, and attracts extra franchisees in a virtuous cycle. Sadly, for El Pollo Loco, this cycle seems to be working in opposition to them, and our best-case state of affairs for the corporate is acquisition by a bigger participant prepared to make substantial investments to revitalize the model. Given its low a number of on an absolute foundation, we assign LOCO a impartial ranking.

INVESTMENT DISCLAIMERS & INVESTMENT RISKS

Previous efficiency shouldn’t be essentially indicative of future outcomes. All investments carry vital danger, and it’s vital to notice that we aren’t within the enterprise of offering funding recommendation. All funding choices of a person stay the particular duty of that particular person. There is no such thing as a assure that our analysis, evaluation, and forward-looking value targets will lead to income or that they won’t lead to a full loss or losses. All buyers are suggested to completely perceive all dangers related to any type of investing they select to do.