Mario Tama/Getty Photos Information

Introduction

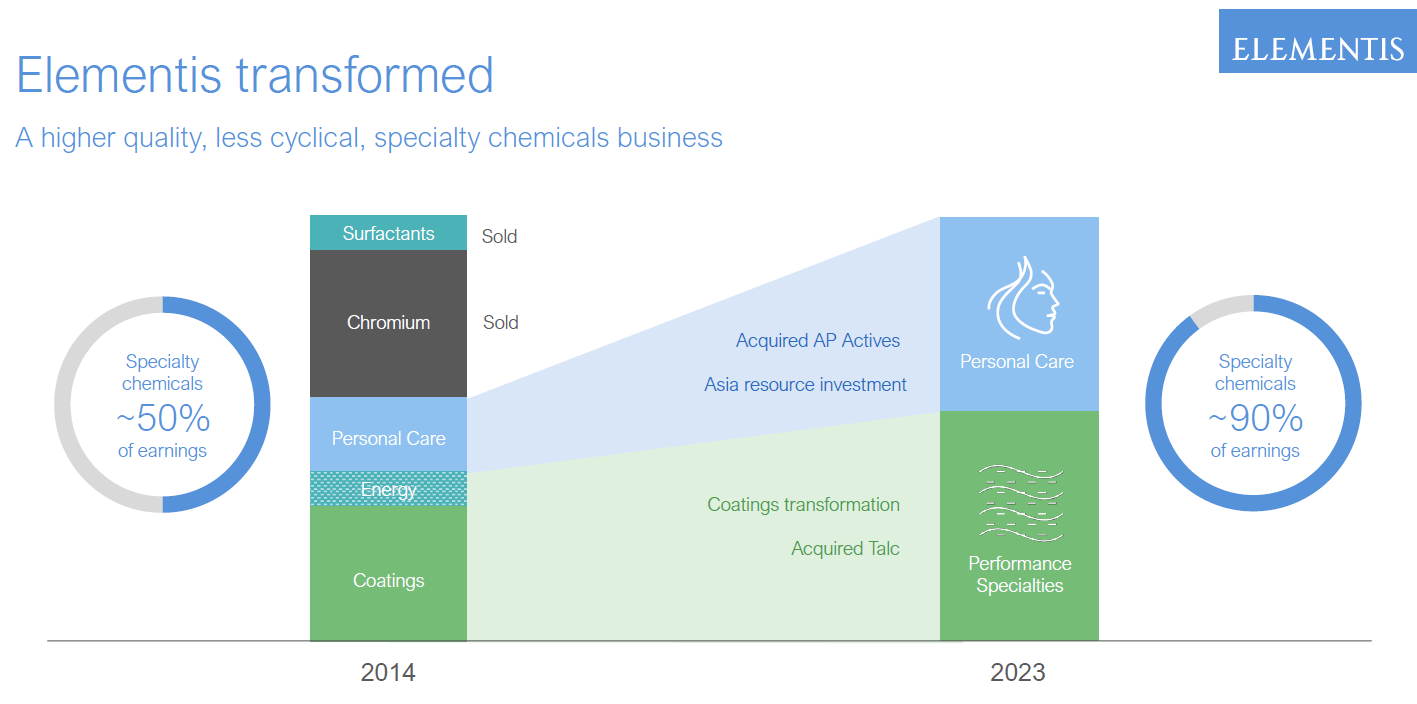

Elementis (OTCPK:ELMTY) (OTCPK:EMNSF) is a specialty chemical compounds firm with a worldwide presence. The corporate needed to reinvent itself in the past few years and is now predominantly specializing in private healthcare and coatings. The corporate provides rheology modifiers and hectorite applications because it operates the world’s solely high-grade hectorite mine (which has a remaining mine life of roughly 50 years). Hectorite is for example utilized in antiperspirant aerosols.

Elementis Investor Relations

As you’ll be able to see above, the corporate is now totally specializing in its specialty chemical compounds enterprise after selling the chromium division within the first quarter of final 12 months for $139M in money.

Yahoo Finance

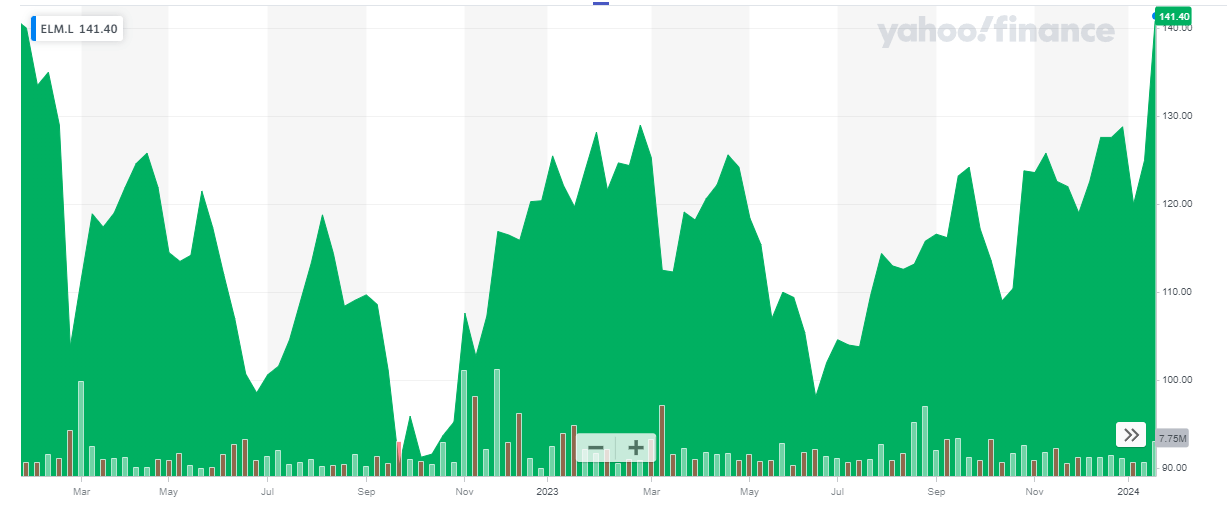

Elementis has its main itemizing on the London Inventory Trade the place the corporate is buying and selling with ELM as its ticker image. The average daily volume in London is almost 1 million shares. As Elementis at present has 585 million shares excellent, its market capitalization is roughly 825M GBP. That’s roughly $1.05B on the current GBP/USD exchange rate.

Elementis’ free money move profile is fairly sturdy

Whereas the corporate will launch its full-year monetary ends in March, Elementis has already printed a buying and selling replace which is useful to finetune my expectations based mostly on the detailed H1 outcomes. As such, I feel it is smart to first look again on the H1 outcomes earlier than leaping to the full-year expectations and the outlook for 2026 as supplied by the corporate on its most up-to-date capital markets day.

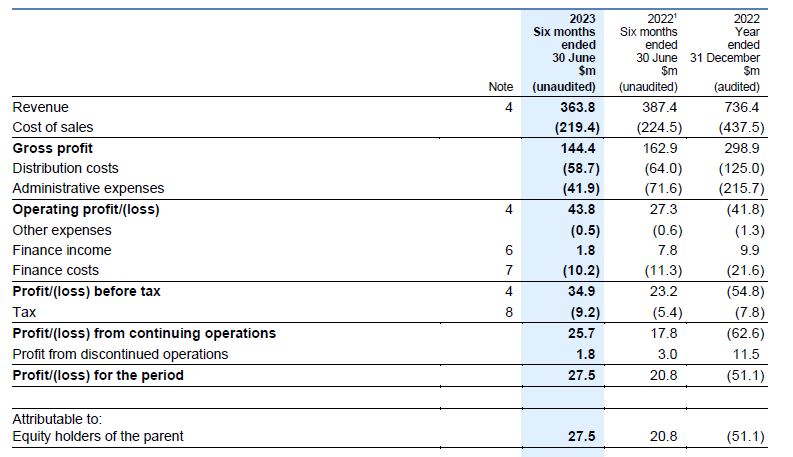

The entire income within the first half of 2023 was just below $364M. And though this resulted in a lower of the gross revenue by in extra of 10%, the working revenue truly elevated by greater than 50% because of a considerable discount in its distribution and G&A expense. The corporate posted an operating profit of just under $44M which resulted in a pre-tax revenue of virtually $35M in the course of the first half of 2023.

Elementis Investor Relations

After paying the related taxes and deducting the portion of the online revenue that’s attributable to the discontinued operations, the online earnings was $25.7M (the discontinued operations added $1.8M in web earnings), leading to an EPS of $0.044. That’s roughly 3.5 pence per share.

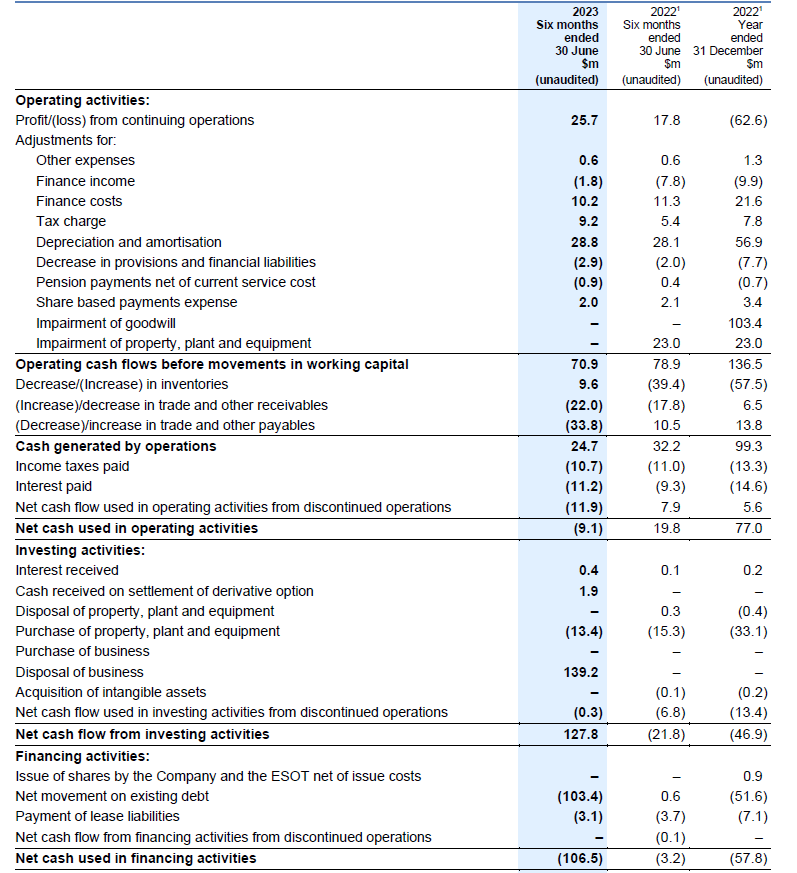

In my earlier articles on Elementis I at all times seemed on the firm as a money move story, and that also is my method proper now. The picture under reveals the H1 money move assertion whereby the corporate reported an working money move earlier than adjustments within the working capital place of virtually $71M. After deducting the $22M in taxes and curiosity funds and the $3M in lease funds, the underlying working money move was $46M.

Elementis Investor Relations

The picture above reveals the corporate spent roughly $13M on capital expenditures, leading to an underlying free money move results of $33M. As there are 585M shares excellent, the online free money move per share was roughly $0.056 or 4.4 pence per share. A powerful consequence in comparison with the reported web earnings. That’s primarily brought on by the distinction between the depreciation and amortization bills ($29M) and the capex + lease funds ($16.5M). Sadly the investments within the working capital place have been a drain on the money place however this needs to be reversed within the second semester.

Earlier this month, the corporate released a trading update and because of a robust closing quarter, the corporate now expects to report an working revenue of $102-104M on an adjusted foundation. The midpoint of that steerage represents a 2.5% enhance in comparison with the adjusted working revenue reported in 2022.

This permits me to calculate the free money move for 2023. We all know the corporate will generate roughly $2.5M in further working revenue however it can additionally should make increased curiosity funds which is able to probably are available $5M increased than in 2022. Moreover, the capex will probably be round $40M which can also be barely increased than the $33M it spent in 2022.

The web revenue will probably are available at $60-62M. In the meantime the overall depreciation and amortization bills will exceed $55M whereas the overall capex + lease funds will probably be simply round $45M. This implies the free money move consequence will probably be round $10M increased and will very nicely are available at $70M in 2023. That’s roughly $0.12 per share, which is the equal of 9.4 pence.

And as we must always see a working capital launch in the course of the second semester, the online debt will probably lower. Elementis has guided for a web debt of $201M which represents “approximately” 1.5 occasions EBITDA. All these parts make the corporate’s ambition to restart dividend funds extra credible.

The latest capital markets day supplied extra particulars on Elementis’ long-term plans

I like capital markets days as they often present glorious insights in the way in which an organization’s administration staff thinks. In Elementis’ case, it needed to supply an replace as we at the moment are reaching the top of the interval that was the spotlight of the 2019 capital markets day. Sadly the corporate has solely met one of many goals. The picture under predates the This fall buying and selling replace and whereas the debt ratio is “orange,” it now feels like that concentrate on will probably be met. The three targets sadly have been too optimistic.

Elementis Investor Relations

This doesn’t actually imply we should not have any confidence within the new steerage. In any case, Elementis was dealt an unfair hand as shortly after its capital markets day the world modified when the COVID pandemic had an enormous impression on the world economic system. And because the pandemic was straight adopted by an inflationary interval, I’m prepared to chop the corporate some slack.

Elementis has recognized the potential to increase its revenue by $90M above market growth by 2026. This might lead to a full-year income of $800M (once more, this excludes the impression from different progress initiatives). Extra importantly, Elementis goals to realize an working margin of 19%. This means an working revenue of $152M which is roughly 50% increased than the working revenue generated in 2023.

Elementis Investor Relations

If I’d now assume the curiosity bills stay unchanged (I truly count on them to lower as the corporate will deploy a few of its free money move to additional scale back the online debt stage on the steadiness sheet), the pre-tax revenue can be $132M leading to a web revenue of $98M or $0.17 per share. And as you realize, the sustaining capex is barely decrease than the depreciation and amortization bills so the underlying free money move will probably be roughly 10% increased on a sustaining foundation. That may symbolize $0.185 per share or 14.5 pence. As there isn’t any actual motive for Elementis to proceed to scale back its debt (sustaining the present web debt stage would lead to a leverage ratio of simply 1), there’s loads of money out there for Elementis to finish a buyback and/or restart the dividend funds.

Funding thesis

On the present share value of 141 pence, Elementis is buying and selling at a $1.05B market cap and an enterprise worth of $1.25B (assuming a year-end web debt of round $200M). This means the present EV/EBITDA a number of is 8 whereas the corporate has set its sights on 2026 the place the EBITDA needs to be round $205M. Even when we might assume the corporate received’t pay down a single greenback in debt, the enterprise worth of $1.25B compares fairly favorable to the anticipated EBITDA.

Whereas I used to be writing this text, the corporate acquired a letter from Franklin Mutual Advisers urging the Elementis to consider selling the company. Whereas that’s not a central thesis for this text nor my funding coverage, it is an fascinating nudge from a big shareholder.

I’ve a small place in Elementis and was trying to enhance this within the 120 pence vary earlier than the shareholder letter pushed the share value increased. The share value could come down within the subsequent few days and weeks.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.