jetcityimage/iStock Editorial by way of Getty Photographs

Though I don’t fancy myself a progress investor, opting as a substitute to deal with the worth strategy to investing, I can’t deny that there’s something alluring about shopping for quickly rising corporations that go on to realize strong returns. One firm that I uncharacteristically grew to become bullish on late final yr was pharmaceutical big Eli Lilly and Firm (NYSE:LLY). The progress that the enterprise had made within the weight problems market, first with the success of its Mounjaro model and later with its launch of the identical drug branded as Zepbound however marketed for weight problems versus these affected by diabetes, made me enthusiastic about what sort of progress the corporate may obtain shifting ahead.

After cautious consideration, I ended up score the corporate a “buy” as a result of I believed that progress would proceed and that shareholders would profit as a consequence. Since my most up-to-date article on the corporate in early November of 2023, shares have seen an upside of twenty-two.9% at a time when the S&P 500 (SP500) has risen by 14.9%. And since I first rated the company a “Buy” in June of final yr, shares have generated upside for traders of 56.2% whereas the S&P 500 has elevated by solely 12.3%. I might name {that a} success.

However, after all, one of many risks of progress investing is that firms can grow to be overvalued. And whereas it stays to be seen whether or not that’s the case for Eli Lilly and Firm, I do suppose that the inventory is priced to such an extent that additional upside relative to the broader market is unlikely right now. Due to this, I’ve determined to downgrade the agency to a “Hold.”

An ideal outlook

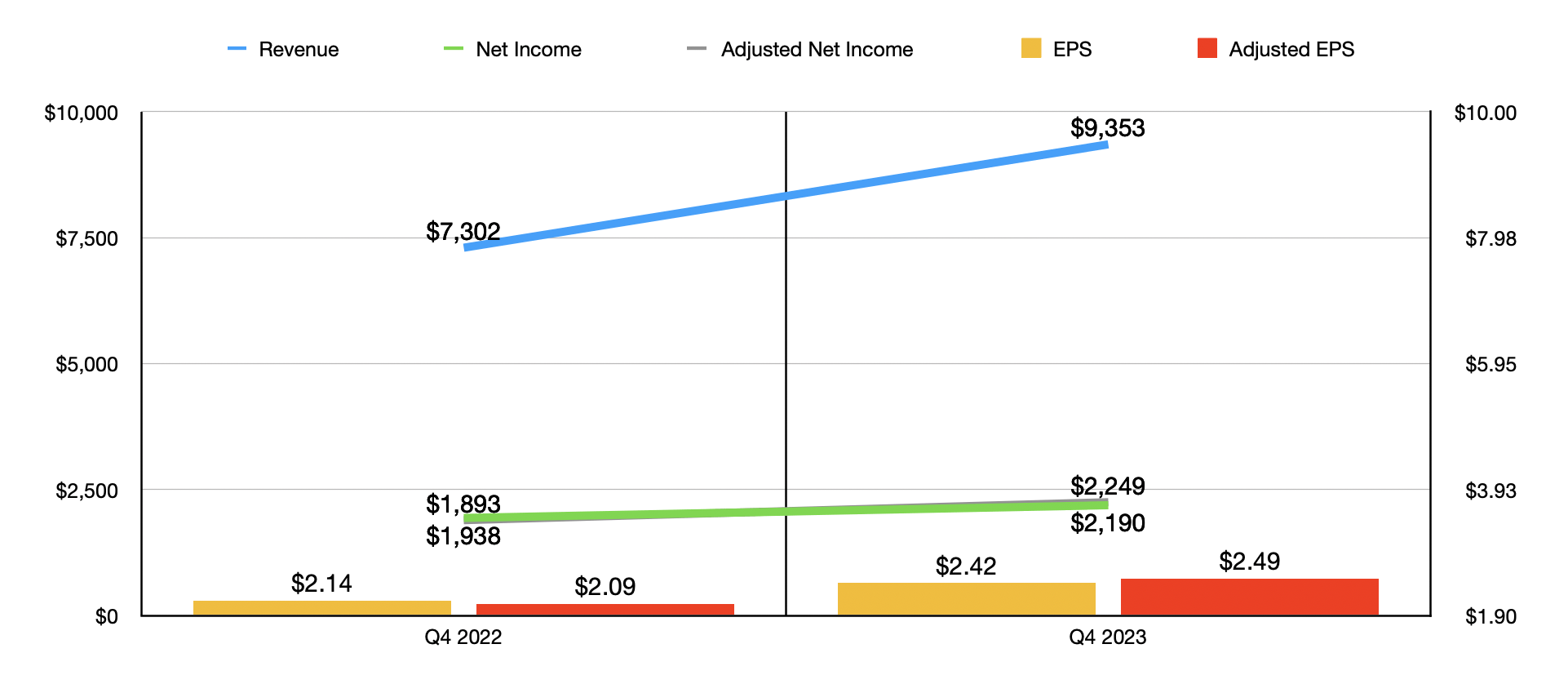

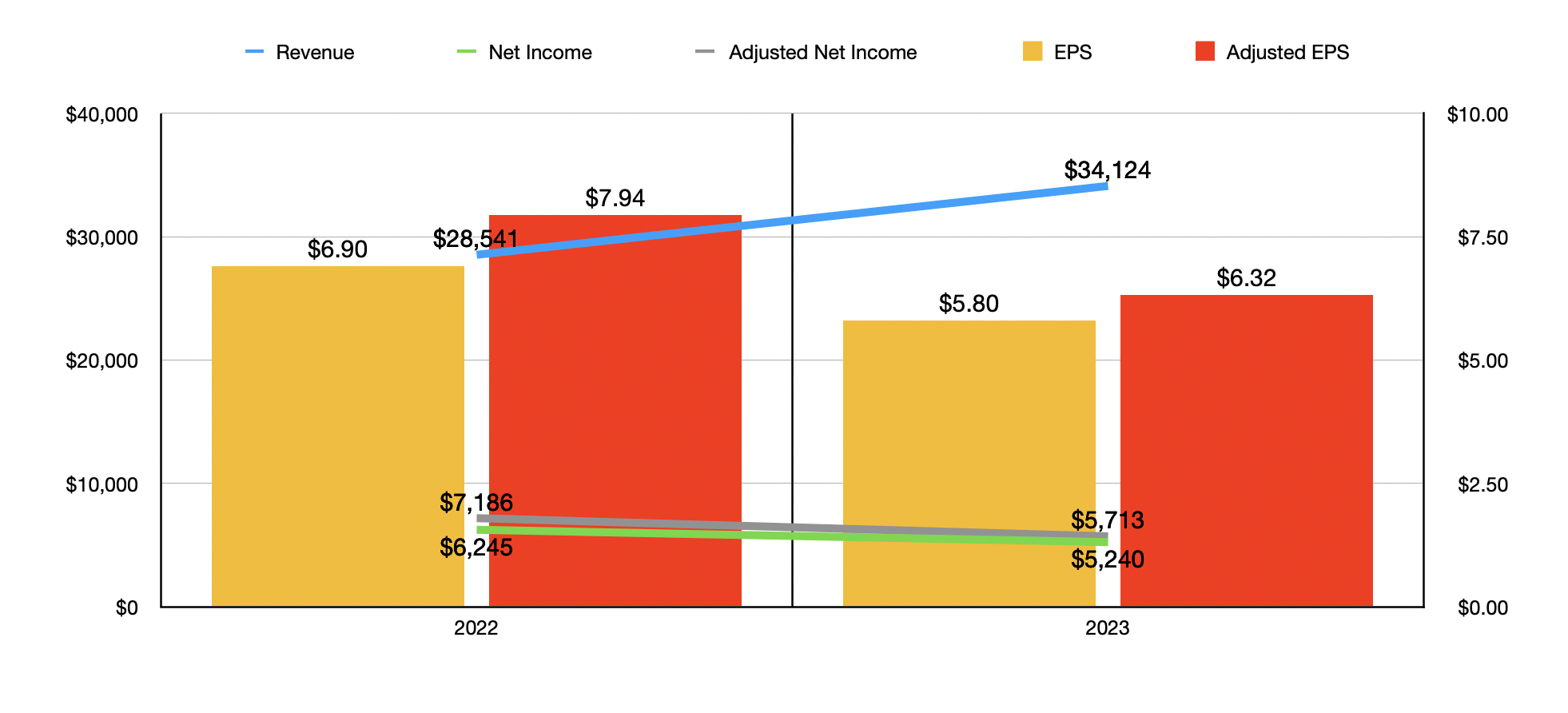

On February sixth, the administration staff at Eli Lilly and Firm announced monetary outcomes overlaying the ultimate quarter of the 2023 fiscal yr for the enterprise. In some respects, the quarter was fairly constructive. In others, it may have been higher. For starters, income got here in at $9.35 billion. That represents a rise of 28.1% over the $7.30 billion the corporate reported one yr earlier. Along with seeing a large improve in gross sales, the income reported by administration truly got here in about $380 million larger than what analysts anticipated.

Creator – SEC EDGAR Information

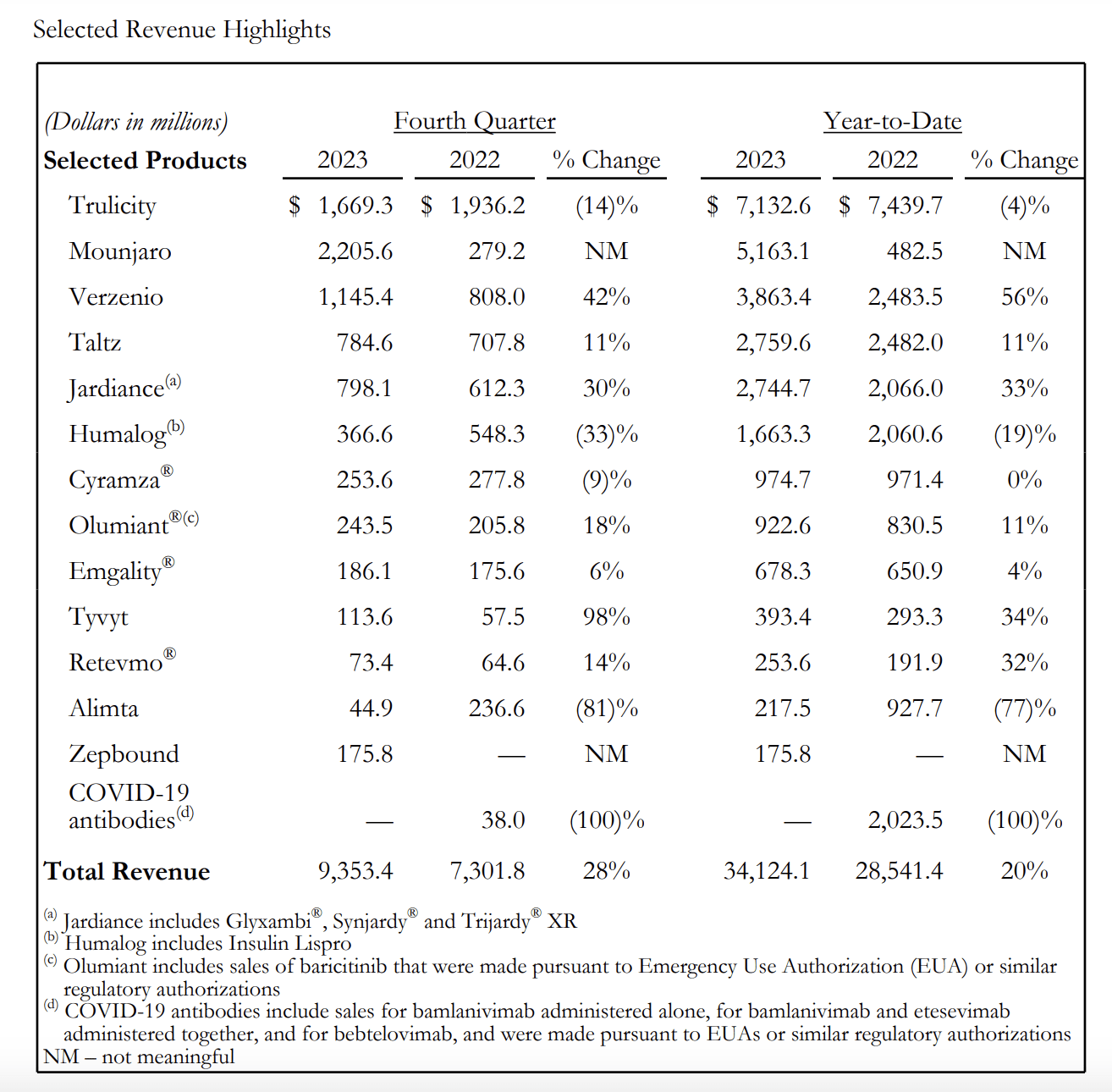

One of many downsides of the pharmaceutical house is that, as a result of a lot of the analysis that they conduct falls underneath a selected class, the success of a brand new drug can imply the cannibalization of an older drug. Whereas income for the corporate got here in sturdy, what had beforehand been its most important drug, Trulicity, has been on the decline as a result of, fairly frankly, it pales compared to what has come out not too long ago. Though for the 2023 fiscal yr in its entirety, Trulicity remained the biggest income for the enterprise, accounting for $7.13 billion, or 20.9% of general income, the ultimate quarter of 2023 was not nice for it. Income throughout that point totaled $1.67 billion. That represents a decline of 13.8% from the $1.94 billion generated one yr earlier.

Eli Lilly & Co.

Though income related to Trulicity is now slated to fall within the years to come back, there have been some actually vivid spots for the enterprise. Most notable is the Mounjaro model, which has been described by many as a miracle for these trying to drop extra pounds. Income throughout the closing quarter of the yr was $2.21 billion. That is nearly eight instances greater than the $279.2 million generated the identical time one yr earlier. Much more thrilling is the model of that drug devoted particularly to these with weight problems who haven’t been identified with diabetes. The drug began promoting late final yr and nonetheless generated income of $175.8 million for the quarter. Whereas this may appear small in comparison with the remainder of the income the corporate generated, think about that it was solely accredited on November eighth of final yr and was solely obtainable beginning on December fifth.

Mounjaro and Zepbound will not be the one medication doing effectively. The corporate has seen enticing progress elsewhere. Most notably, there was a 41.8% surge in income related to Verzenio, a drug that’s used to deal with sure forms of breast most cancers. Income jumped from $808 million to $1.15 billion. One other progress space for the enterprise concerned Jardiance, which is used to decrease blood sugar for these with sort 2 diabetes with the objective of lowering the chance of heart problems. Its income went from $612.3 million to $798.1 million. That could be a 30.3% improve year-over-year.

Creator – SEC EDGAR Information

With income rising, income additionally improved. Though earnings per share fell wanting analysts’ expectations by $0.04, they nonetheless managed to develop from $2.14 to $2.42. That introduced internet income up from $1.94 billion to $2.19 billion. On an adjusted foundation, nevertheless, income per share exceeded forecasts by $0.12. That resulted in adjusted internet income of $2.25 billion, in comparison with the $1.89 billion reported one yr prior. Different profitability metrics, sadly, haven’t but been offered by administration. That knowledge will come out when the agency releases its official annual report. But when this yr is like final yr was, it may very well be across the finish of February earlier than that knowledge comes out.

This does current a difficulty with regards to valuing the corporate. As an example, we do not know what internet debt is, nor do we all know what useful money move figures are. For the aim of valuing the corporate, the very best I may do is assume that the balance sheet regarded the identical within the closing quarter of the yr because it did within the third quarter. I additionally assumed that the year-over-year progress price for EBITDA for the primary 9 months of the yr relative to the identical time of 2022 continued for the ultimate quarter of the yr and utilized to adjusted working money move as effectively.

Eli Lilly & Co.

However earlier than we get into how shares are priced, we must always speak extra concerning the future. Even ignoring the prospect of extra medication which might be within the firm’s pipeline, which is a subject I wrote about in my first article on the corporate, the longer term appears to be fairly constructive. We sadly do not know what sort of progress to anticipate of Zepbound, however in all probability, its prospects match into the $25 billion income alternative that the corporate is being uncovered to.

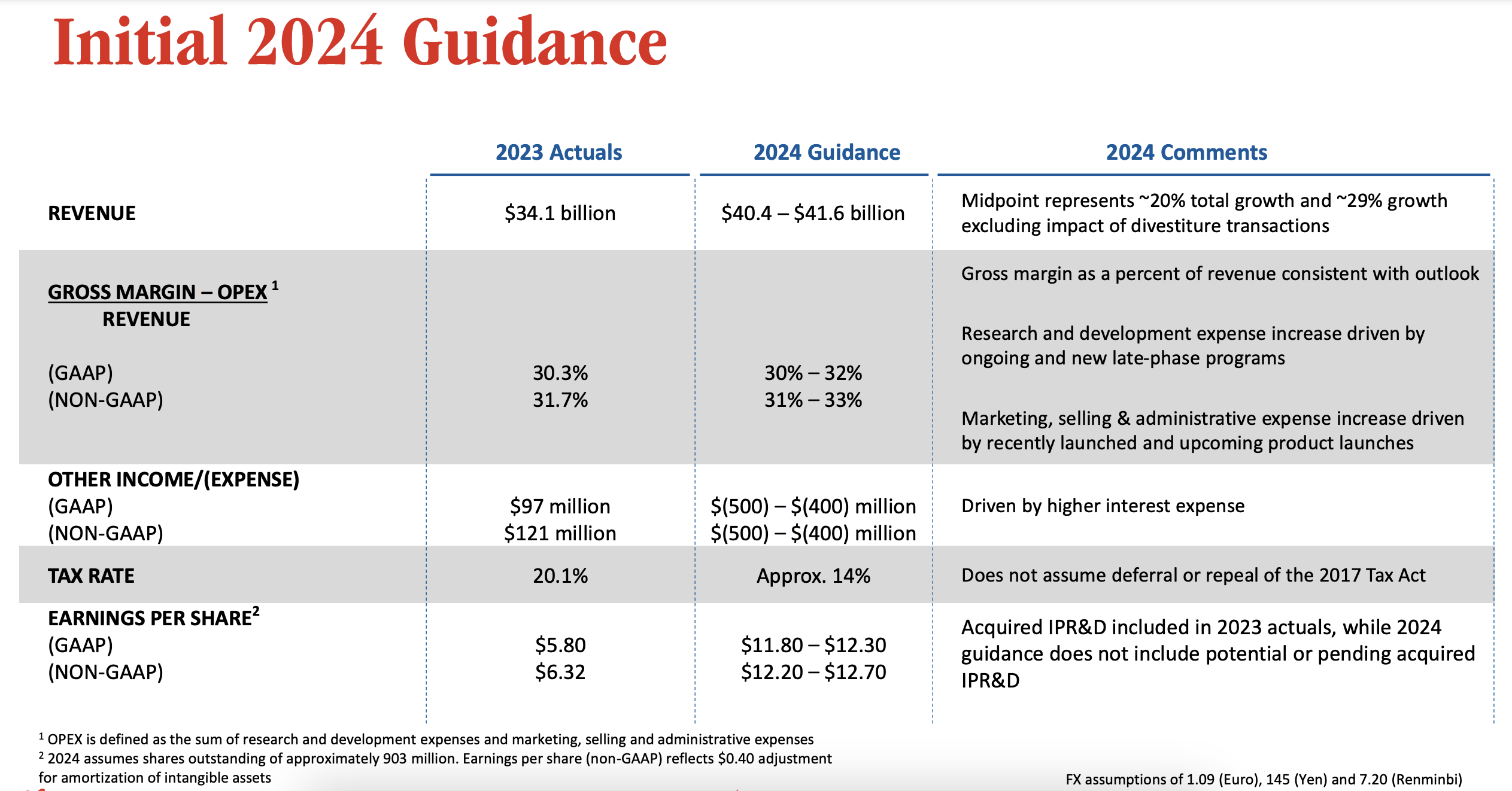

After all, this won’t happen in a single day. It’ll take a while to play out. The excellent news is that administration has offered some steering for what 2024 will appear to be. They at present forecast that income will are available at between $40.4 billion and $41.6 billion. On the midpoint, that ought to symbolize a year-over-year improve of 20.1% in comparison with the $34.1 billion the corporate reported for 2023 in its entirety. Earnings per share are forecasted to come back in between $11.80 and $12.30. That is a large improve over the $5.80 per share reported for 2023.

Creator – SEC EDGAR Information

If this earnings steering comes true, traders ought to anticipate income of about $10.88 billion. That implies an adjusted working money move of round $16.96 billion and EBITDA of $24.30 billion. However once more, that’s with out full knowledge from the 2023 fiscal yr.

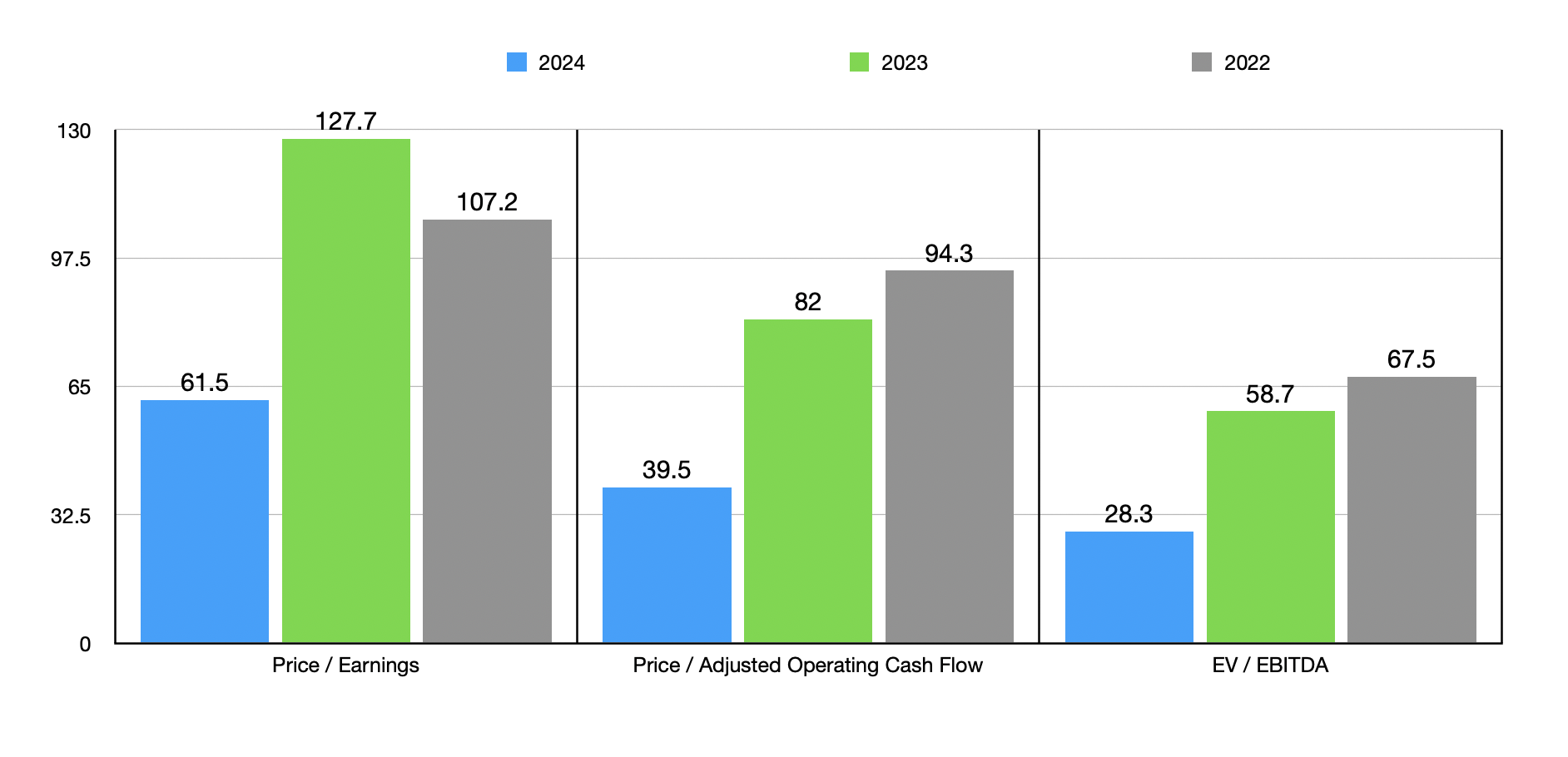

Utilizing these estimates, in addition to estimates for 2023 and historic outcomes from 2022, I valued Eli Lilly & Co. as proven within the chart above. Even on a ahead foundation, the inventory does look very costly. I then, within the desk beneath, in contrast it to 5 related corporations. In comparison with the 2023 estimates, Eli Lilly & Co. ended up being the most costly of the group utilizing two of the three valuation metrics, with 4 of the 5 firms being cheaper than it with regards to the price-to-earnings strategy. However even when we use the ahead estimates for 2024, three of the 5 firms could be cheaper than it utilizing each the value to earnings strategy and the EV to EBITDA strategy, whereas the value to working money move strategy would nonetheless see it’s essentially the most expansive of the group.

| Firm | Value/Earnings | Value/Working Money Stream | EV/EBITDA |

| Eli Lilly & Co. | 127.7 | 82.0 | 58.7 |

| Johnson & Johnson (JNJ) | 13.1 | 20.2 | 17.4 |

| Merck & Co. (MRK) | 907.8 | 16.2 | 58.0 |

| Pfizer (PFE) | 76.4 | 13.7 | 18.5 |

| AstraZeneca (AZN) | 35.4 | 20.2 | 16.5 |

| Novo Nordisk (NVO) | 43.5 | 33.4 | 31.3 |

Takeaway

Transferring ahead, I’ve little doubt that Eli Lilly and Firm will proceed to do effectively for itself. The agency ought to go on to generate vital earnings and money move progress. However even when we take administration’s assumptions, Eli Lilly and Firm inventory seems to be relatively costly. It is unlikely that we’ll see additional upside from right here until one thing sudden comes out of the woodwork. So, due to how shares are at present priced, and due to how a lot the inventory has already risen up thus far, I do consider that downgrading it from a “Buy” to a “Hold” is prudent.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.