jetcityimage

Funding Thesis

I consider Eli Lilly (NYSE:LLY) is poised for continuous progress because of the vital demand for weight-loss medication and the rising insurance coverage protection. My perspective is a perception in the way forward for GLP-1 therapies, notably these focusing on weight problems. My important focus is on Eli Lilly’s pioneering drug, Zepbound, which I see tackling weight-related well being issues- we might nearly consider this new division of weight problems administration as a progress section within the firm, no less than that is how I view it. This text discusses past the preliminary buzz round Eli Lilly’s product and solutions why this division is poised for continued progress. I am satisfied that the rising demand and sure insurance coverage protection expansions in 2024 will propel these medication into higher profitability. In order we dive in, I feel this can be a stable thesis to contemplate for a possible funding, one the place the corporate’s modern edge might provide substantial returns as we enter a 12 months of grand potential on this house.

However all through this complete piece, one can find that I intertwine an evaluation that positively highlights the significance of those GLP-1 medication. I hope you take pleasure in studying this text as a lot as I loved writing it.

Eli Lilly: Purchase Score

Continued GLP-1 Success In 2024

Each Eli Lilly and Novo Nordisk (NVO) have launched weight-loss medication they usually have modified the pharmaceutical industry– and the world. Each of their merchandise have been available on the market, some consider that we’re on the peak of their buzz, and others, like myself, see a vivid future for them in 2024 (and different industries, which we are going to focus on later) The FDA’s approval of tirzepatide, marketed as Zepbound, marked a big step within the combat in opposition to weight problems. It’s a promising avenue for these combating weight administration. Zepbound’s energetic compound is shared with the diabetes drug Mounjaro, which has already proven spectacular weight reduction outcomes. Zepbound stands out due to its dual-hormone mimicking mechanism, which is believed to be more practical compared to weight reduction medication like semaglutide. The scientific trials supporting this declare are compelling; sufferers misplaced about 18% of their physique weight on common. I discover this a really giant and promising determine when fascinated by the challenges related to weight problems and its therapy.

Nonetheless, there are numerous unintended effects to contemplate and in addition observe that Zepbound just isn’t a one-size-fits-all answer. People fluctuate of their outcomes, however the drug is especially impactful for these with weight-related well being dangers.

I’m assured that insurance coverage protection can be obtainable for the weight-loss medication, which is the place a lot of my 2024 thesis revolves round. Nonetheless, as of now the excessive out-of-pocket value stays a priority for these with out ample protection. However all in all, with a rising demand (and nearly a necessity) I see this growth as a powerful indicator of the rising marketplace for weight problems medication, highlighting Eli Lilly’s potential progress on this sector.

To dive in deeper, the surge of curiosity in weight reduction medication this 12 months is what I feel illustrates the upside in Eli Lilly. Whereas some suppose the hype is lengthy over, I counsel this market nonetheless holds upward motion; I do not consider it would prime off anytime quickly. However in broad phrases, the significance of those developments is impactful to say the least. Analysts are predicting the load loss drug market to achieve $100 billion by the tip of the last decade. Goldman Sachs (GS) forecasted 15 million U.S. adults to be on weight problems drugs by 2030; the stakes are excessive and I counsel, with these numbers, that everybody take a chunk of the funding pie. I say this due to the rising demand and now rising accessibility of the medication, which we are going to proceed to see rolling into 2024. And like I stated, most of us know that there are present points with provide and insurance coverage protection. For instance, Eli Lilly’s Mounjaro has confronted provide constraints. Nonetheless, the businesses are actively working to scale up manufacturing to fulfill these calls for. This main affect on the medical group and the probability of elevated insurance coverage protection down the street is what additional helps my thesis to contemplate investing in Eli Lilly, the 2 corporations which are most positively main this innovation.

Dangers

I want to observe that it’s important to acknowledge the inherent dangers related to the corporate, and within the gentle of current developments concerning their GLP-1 merchandise, Mounjaro and Zepbound. Firstly, Eli Lilly’s warning against the misuse of those medication for beauty weight reduction raises issues about off-label utilization. I can see this doubtlessly resulting in unfavorable well being results, authorized liabilities, and injury to the corporate’s repute. The authorized actions taken in opposition to compounding pharmacies and healthcare amenities for promoting unapproved variations of their GLP-1 merchandise sign potential regulatory hurdles. This authorized battle implies ongoing authorized prices for Eli Lilly and suggests the existence of a aggressive and argumentative setting throughout the weight reduction {industry}.

Furthermore, the reliance on FDA approvals for his or her medication leaves Eli Lilly susceptible to regulatory modifications and potential setbacks within the drug approval course of. Any delays or rejections by the FDA can affect the corporate’s income streams and progress prospects.

Lastly, the extremely aggressive nature of the load loss {industry}, with Novo Nordisk as a distinguished rival, introduces market share dangers. However I do suppose as every product will get higher and extra folks undertake this weight reduction administration drug, then it would propel every firm. I see Eli Lilly and Novo Nordisk as opponents but in addition complement the brand new, thrilling sector of weight reduction medication. However in zooming in and out extra normal phrases, Eli Lilly should constantly innovate and market its merchandise successfully to take care of its aggressive edge. One thing that I can be watching and I counsel traders to take a look at, too.

The bulls would possibly argue that Eli Lilly’s sturdy monitor file, diversified portfolio, and sturdy analysis and growth efforts can mitigate these dangers. They could emphasize the corporate’s dedication to security and adherence to FDA pointers. Nonetheless, I take a look at all views and welcome all data, so to me, potential traders ought to fastidiously weigh these dangers in opposition to the potential rewards when contemplating an funding in Eli Lilly.

Valuation

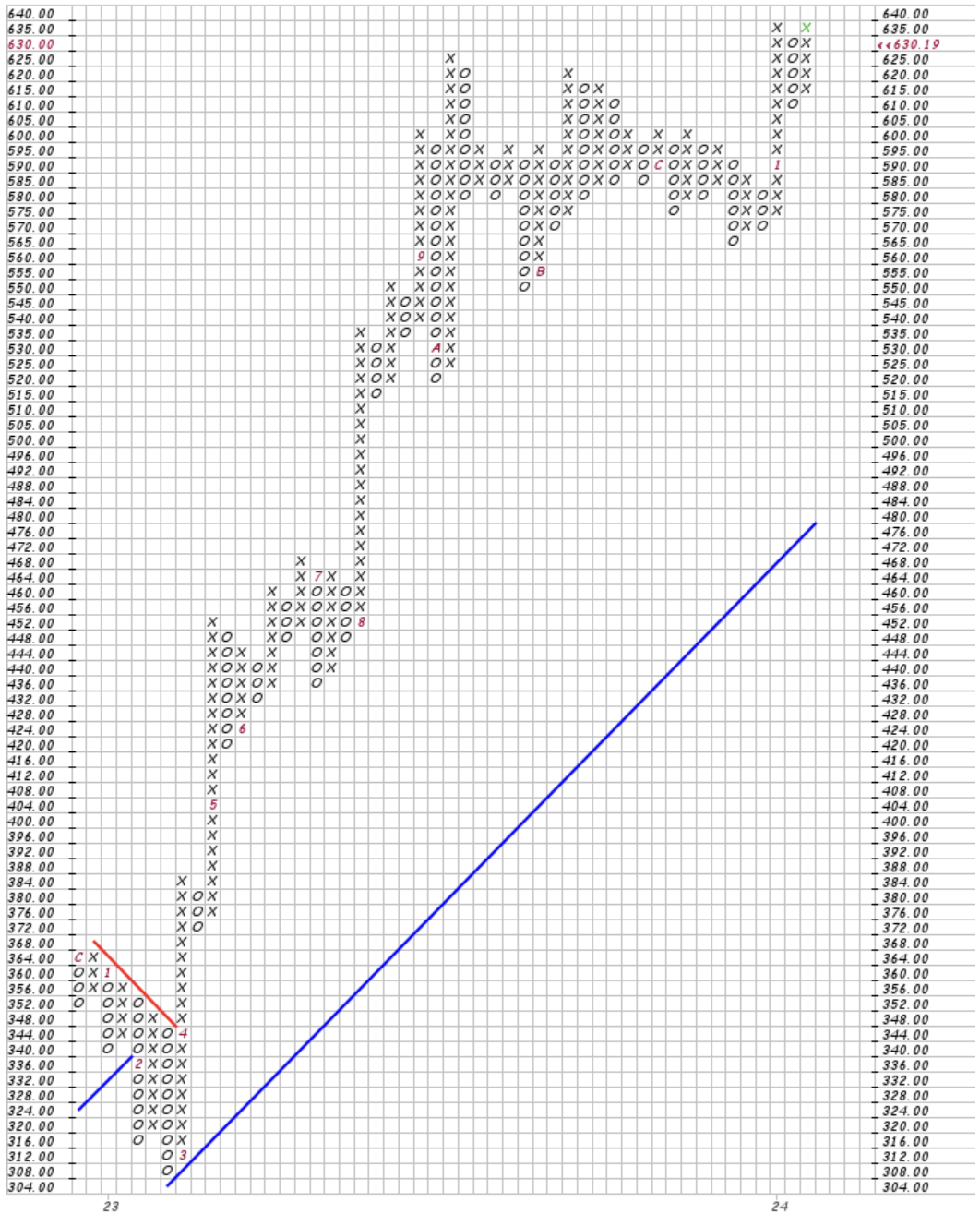

Eli Lilly has had main progress as we take a look again. The stock is up +78.65% in a 1-year timeframe and up +443.55% over the previous 5-year interval. I take pleasure in viewing a degree and determine chart, which I’ve added under. That is the standard three field reversal technique to know assist ranges and pattern traces. What stands proud to me is the momentum in Eli Lilly inventory. As we will see within the chart there’s a main blue-upward pattern line. I strongly consider that if a inventory goes up it is not going to cease till there’s an exterior pressure to shift this momentum. That is a lot associated to Newton’s law- an object will both proceed in movement or keep at relaxation till an exterior pressure modifications this state. So due to this fact, momentum is our pal!

LLY Level & Determine (Inventory Charts)

With that graphical thought in thoughts, let’s transfer to the funding metrics. I feel it’s related to say that these numbers would normally (and nonetheless would possibly) depict a detrimental thesis if we have been to solely take a look at this set of valuation information. Nonetheless, with our level and determine graph within the forefront of our brains, I do consider that the momentum is an element to emphasise. And with my thesis of accelerating insurance coverage protection and rising demand, in my view, I see this momentum persevering with by a elementary lens. It is a key purpose why the information under could appear overvalued, however perhaps we must always simply suppose deeper and in another way.

Beginning with the ahead P/E at 101.75, which can increase eyebrows in comparison with the sector median of 29.27. This lofty P/E is not a purple flag to me, it’s illustrating the very progress we’re talking of within the alpha views. Transferring to the ahead Value to Gross sales ratio, we land at 16.75, hanging previous the sector median of 4.13. Now, this D+ grade right here would possibly make some traders suppose twice as it might be an indication of overvaluation. However I see it supporting the inventory’s premium high quality. To say that Eli Lilly is a progress firm could be fascinating at least, however I feel its valuation metrics are instantly associated to what you’d see within the higher-end progress corporations. I’d say that this division of weight reduction medication, in my eyes, is the expansion section that could be inflicting the hype (and what I feel can be continued hype).

Lastly, the ahead Value to Money Movement ratio. This metric tells us how a lot the market values each greenback of money operations are anticipated to generate. A ratio of 92.03 in opposition to a median of 16.32, once more with a D- grade, might sound alarming. But when the corporate’s money move is projected to balloon as a consequence of modern methods or market enlargement, this ratio in my perspective is a second earlier than the inventory hits its progress spurt.

|

Value / Earnings (FWD) |

Value / Gross sales (FWD) |

Value / Money Movement (FWD) |

|

|

Novo Nordisk |

101.75 |

16.75 |

92.03 |

|

Sector Median |

29.27 |

4.13 |

16.32 |

|

% Distinction |

247.64% |

305.81% |

463.94% |

So, what do these metrics imply for my purchase thesis? Effectively, I do not see them as discouraging indicators. I view this information as an illustration of higher than anticipated efficiency and what I feel will promise. The inventory has nice upside and these numbers are displaying one thing large. The metrics are excessive as a result of expectations are excessive, sustaining my confidence in Novo Nordisk going ahead.

The Key Takeaway

The emergence of GLP-1 weight-loss medication like these from Eli Lilly is reshaping the pharmaceutical {industry}. The important thing takeaway is that Eli Lilly is poised to make a rise in 2024 because of the rising demand and sure likelihood of insurance coverage protection. These medication are making main impacts within the weight problems administration market. Via this text, I’ve outlined not simply the promise of their merchandise however the wider affect on healthcare and investments. As we glance to 2024, I stay assured within the firm’s modern drive and the numerous function it performs in shaping a more healthy future, making Eli Lilly a compelling alternative for traders in search of progress and affect of their subsequent funding.

Remark under what you consider Eli Lilly and the GLP-1 medication, I’d love to interact together with your ideas and opinions!

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.