jetcityimage

Driving the bull market over the last 18 months has been a pair of generational breakthrough factors: AI and GLP-1s. NVIDIA (NVDA) is at the center of chip demand for the former while Eli Lilly (NYSE:LLY) is the poster child for the latter, and what appears to be a weight-loss revolution around the world, particularly in the US. Following yet another very strong quarterly report, the $1 trillion market cap amount could be in the cards over the coming quarters in my view.

I have a buy rating on LLY. I see shares of the largest Pharma company as a buy given the company’s growth path while the stock continues to go through a health consolidation.

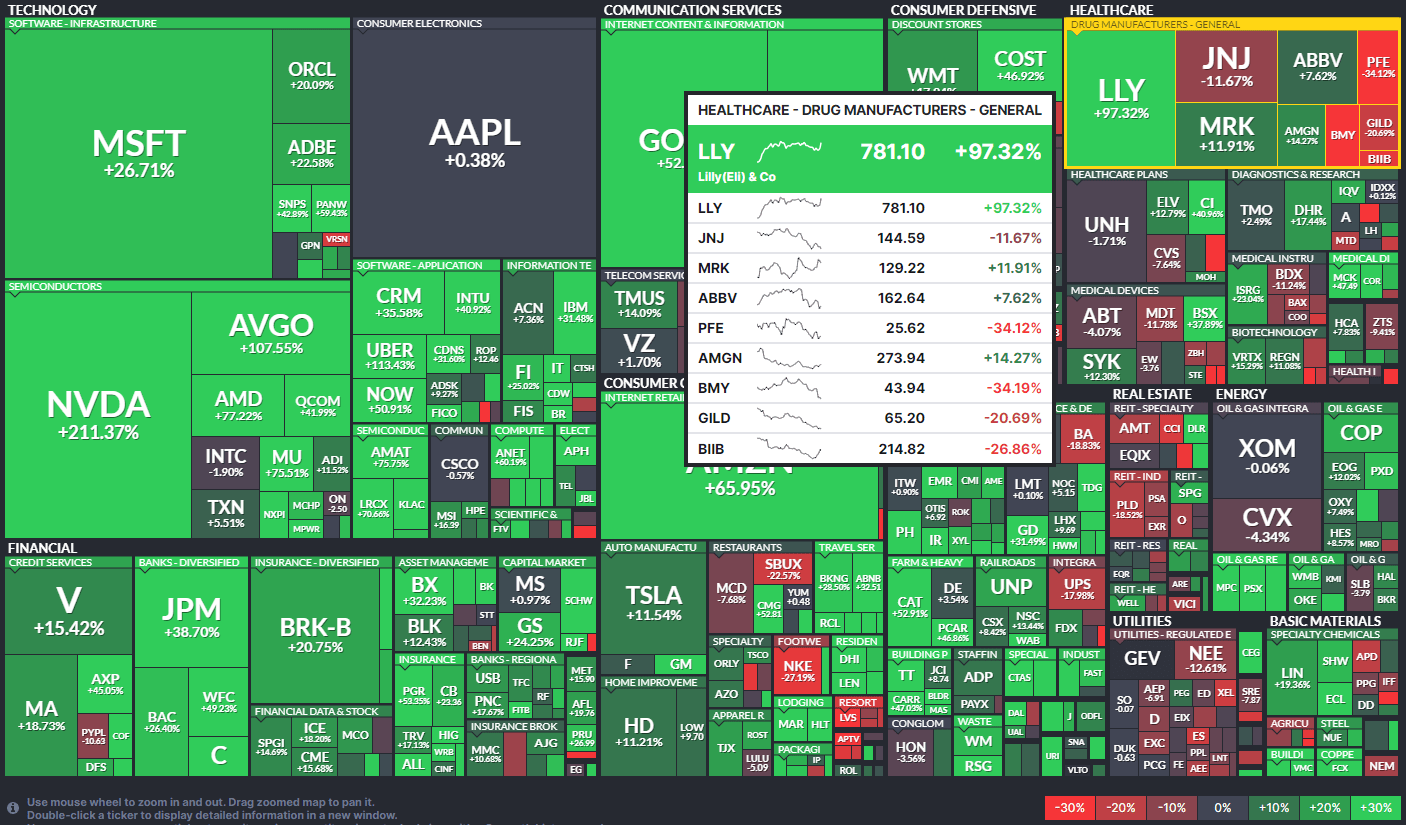

S&P 500 Performance Heat Map: LLY Stands Out in Health Care

Finviz

Eli Lilly (LLY) is a large diversified biopharmaceutical company developing drugs for the treatment of a variety of disorders, including diabetes, migraine, cancer, and a range of inflammatory skin conditions, among others. Lilly has been in the business of developing drugs for more than 140 years, during which time the Company has retained focus almost exclusively on pharmaceuticals.

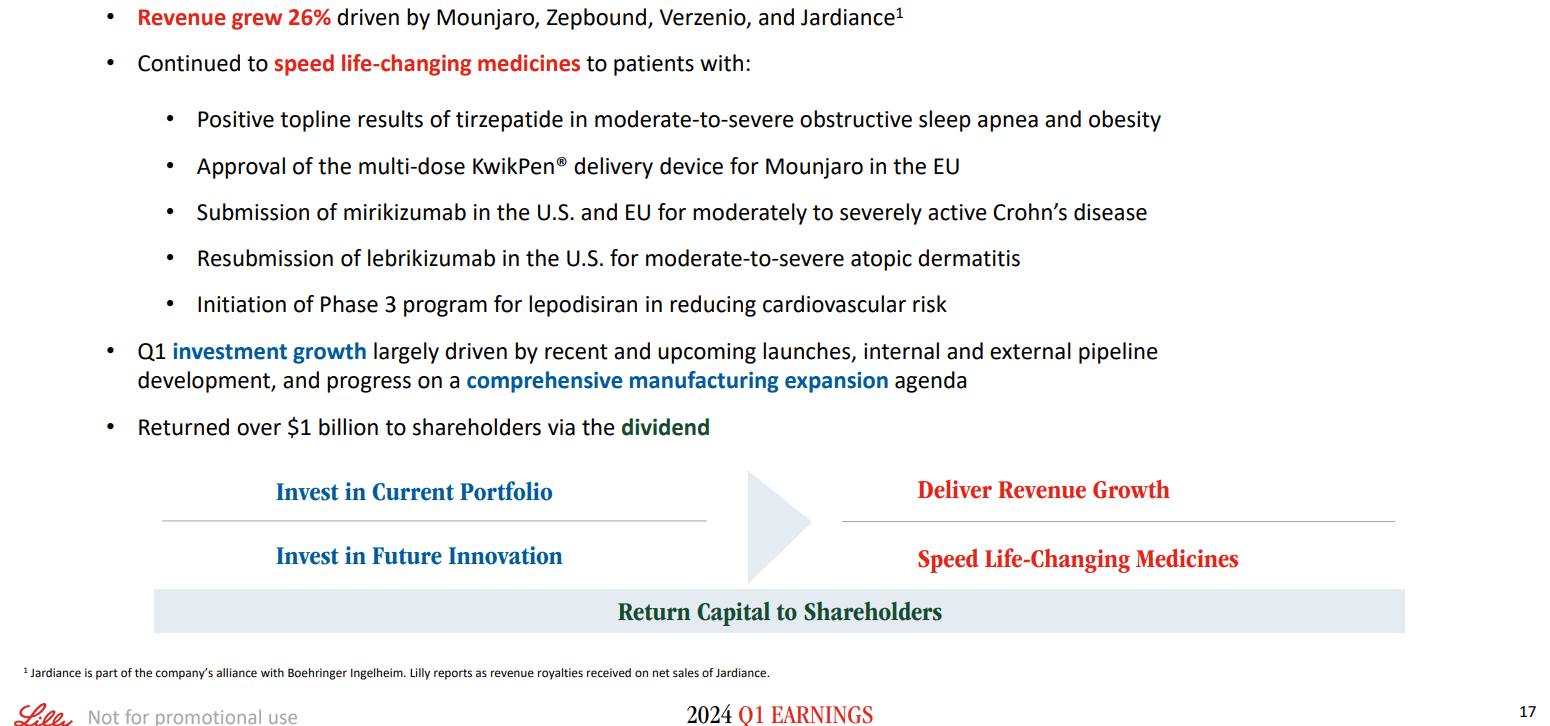

In late April, LLY posted another strong earnings report. Q1 non-GAAP EPS of $2.58 topped Wall Street estimates of $2.49 while revenue of $8.77 billion, up 26% from year-ago levels, was a slight miss. Shares surged 6% following the release, mainly due to upbeat forward guidance around its key drugs Mounjaro, Zepbound, Verzenio, and Jardiance.

LLY: Q1 2024 Summary

LLY IR

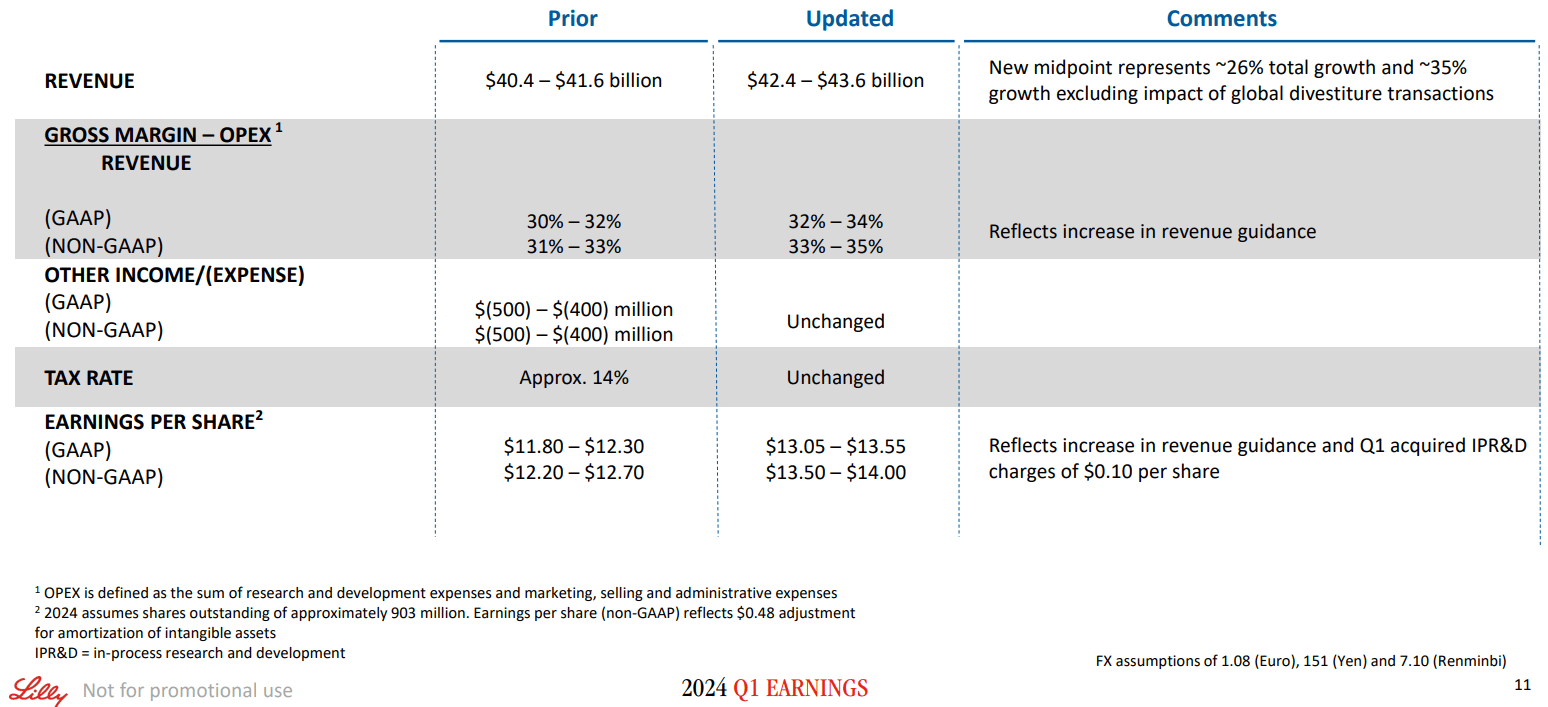

The management team now anticipates 2024 full-year revenue to come in at $2.0 billion with operating EPS to be in the range of $13.50 to $14.00, sharply higher than the $12.46 consensus coming into the Q1 print.

Within the report, sales of Zepbound, the key GLP-1 weight-loss drug, were stellar though Mounjaro sales were light, but supply issues were cited for the low number, which is actually a bullish sign in my opinion. With a strong new-product cycle and pipeline, LLY continues to fire on all cylinders, though bulls must always be on guard for new entrants into the space.

LLY Updated Guidance Post-Q1 Earnings

LLY IR

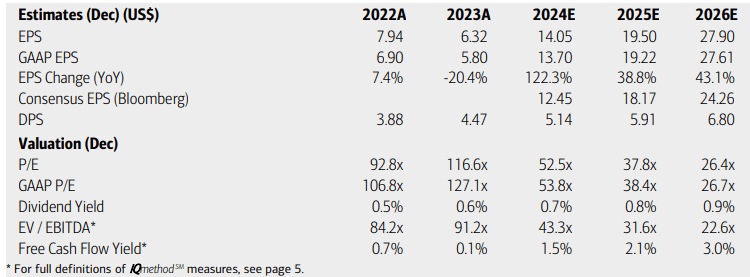

On valuation, analysts at BofA see earnings more than doubling this year. And following strong Q1 numbers posted earlier this week, the sanguine growth trajectory appears to be on track. EPS in the out year is seen rising nearly 40% while growth holds that level through 2026. The Seeking Alpha consensus numbers are close to what BofA, one of the more bullish on the street, sees. Revenues are seen rising at a 26% annual rate this year with 18% to 21% growth over the out years.

Dividends, meanwhile, are forecast to rise at a steady clip, though with shares having surged in the past 14 months, the yield is paltry. What’s not low is the P/E multiple, but stellar profitability trends warrant a high valuation. Shares also trade not far from 3x the EV/EBITDA of the S&P 500 while LLY’s free cash flow is solidly in the black.

LLY: Earnings, Valuation, Dividend Yield, Free Cash Flow Yield Forecasts

BofA Global Research

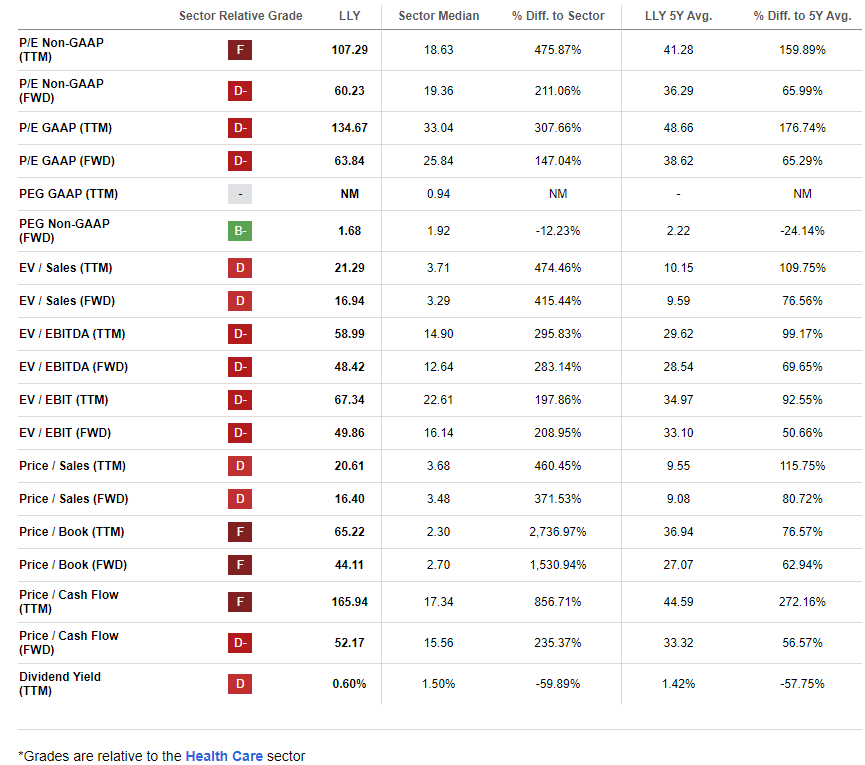

LLY stands apart from its peers on valuation, but take a look at the forward non-GAAP PEG ratio in the table below. It is just 1.7, significantly below the stock’s 5-year average. Priced in terms of growth expectations, shares are not all that expensive. Moreover, if we assume a 2.0 PEG ratio and a normalized growth rate near 20%, then shares would have a 40x P/E if we assume $25 of operating EPS by 2026, potentially putting this growth stock near $1000 per share, which would be about a $1 trillion market cap.

Overall, the growth story is solidly intact in my view. You could apply a lower earnings figure for 2025, but then I assert that the EPS growth percentage would have to be ratcheted up, which would still augur for a decently priced GARP play.

LLY: Strong EPS Growth Warrants a Premium P/E PEG Ratio Favorable.

Seeking Alpha

Compared to its peers, LLY features a poor valuation rating given its very lofty multiples as I described earlier. But with industry-leading earnings growth recently and likely in the offing, the stock clearly stands out within the Health Care sector.

Profitability trends have proven to be very strong, despite challenges meeting total potential demand. It is thus not surprising that there has been a slew of sellside EPS upgrades in the last 90 days while share-price momentum has merely consolidated in the last three months.

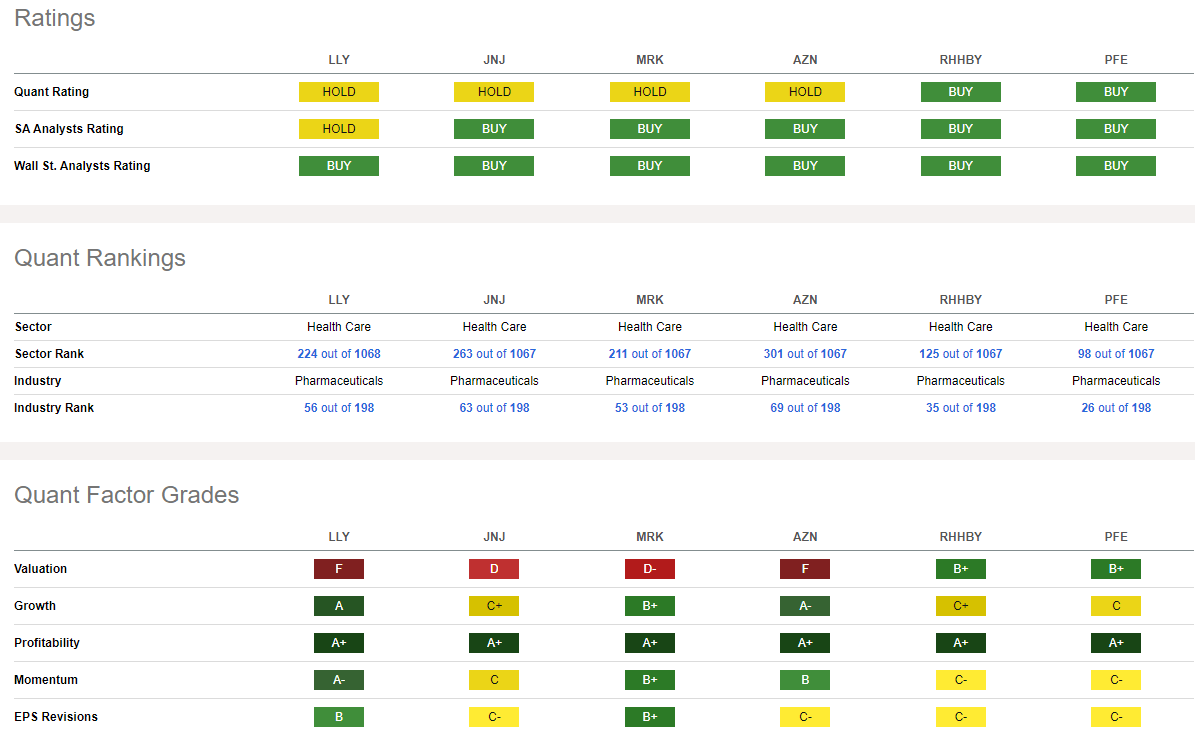

Competitor Analysis

Seeking Alpha

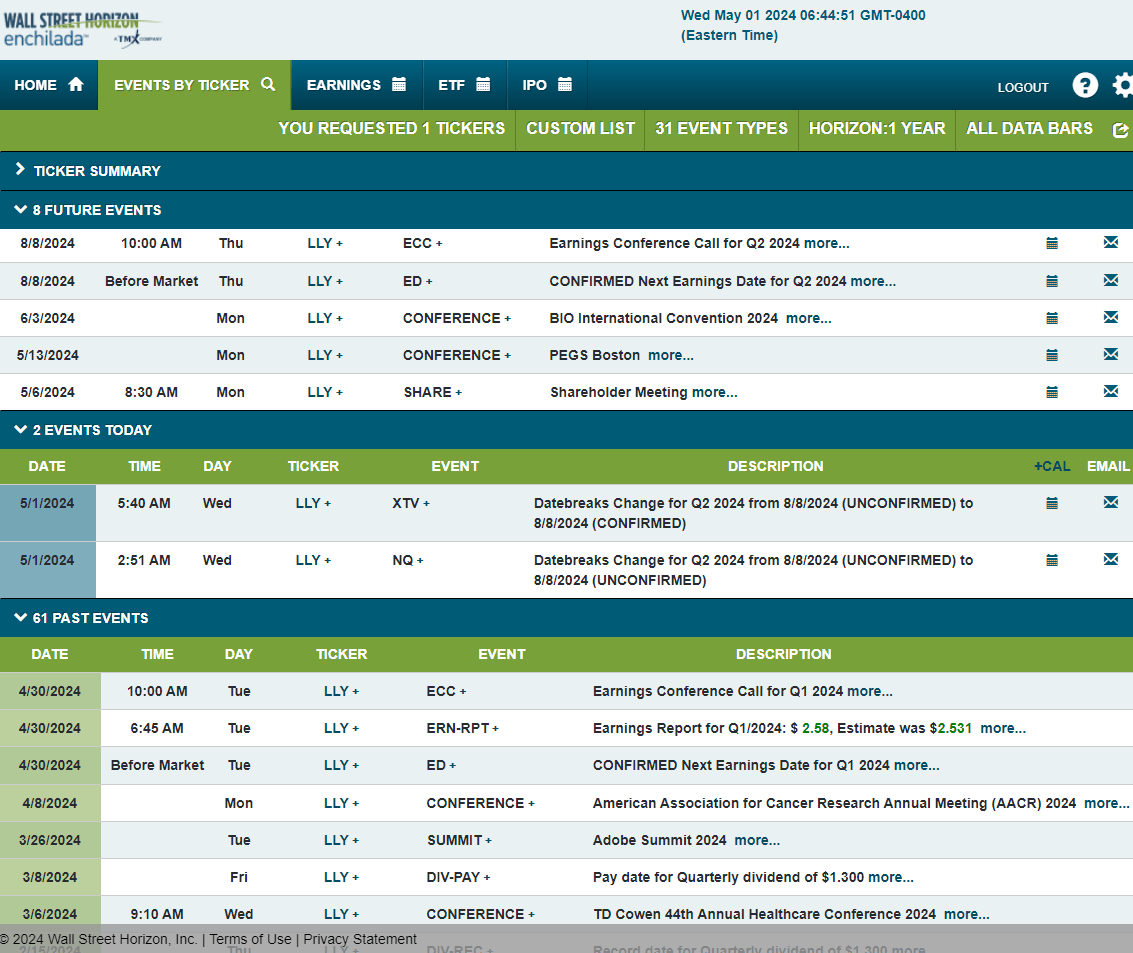

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q2 2024 earnings date of Thursday, August 8 with a conference call later that morning. You can listen live here.

The firm also hosts its annual shareholders’ meeting on Monday, May 6, so be on the lookout for potential volatility early next week. LLY’s team is slated to present at a pair of conferences over the coming weeks as well.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

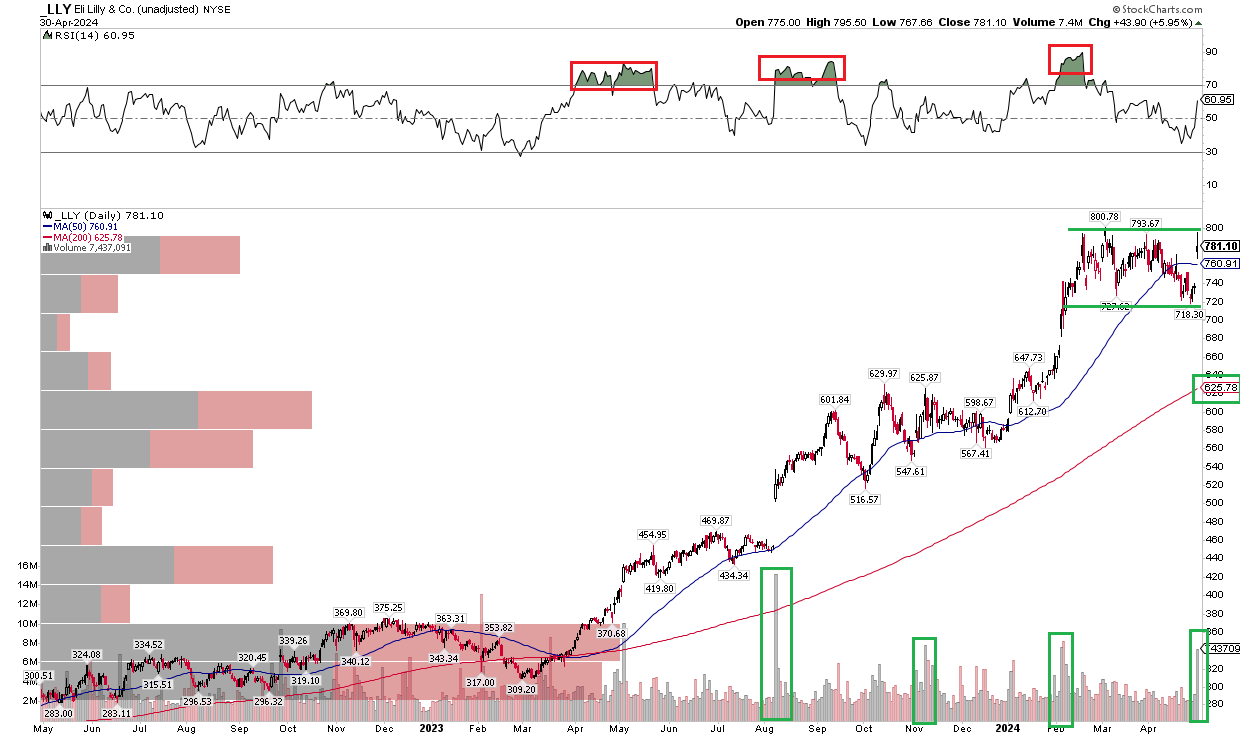

With one of the best earnings growth outlooks in the world, LLY’s technical chart is strong, though shares have been flat since the middle of February. Notice in the graph below that it’s quite common to see LLY pause after hitting sharply overbought conditions. The RSI momentum oscillator at the top of the chart has routinely printed north of 75 for extended periods with price then moving sideways for many weeks. That is what price and momentum trends are currently experiencing. But with a rising long-term 200-day moving average and LLY holding key support in the $715 to $730 range, a breakout above $800 would portend a measured move upside price objective to near $880 based on the $80 current range.

On the downside, a gap developed from after the Q1 earnings release just recently, so the bulls must be on guard for a pullback to about $735 to fill that gap with the April low of $718 being important support. Also take a look at the volume spikes at the bottom of the graph – we have seen repeated strong upward price thrusts happening concurrently with high volume. Technicians like to see that price/volume confirmation.

Overall, the trend is up over the intermediate and long-term views while near-term price action remains in consolidation mode after the Q1 results.

LLY: A Healthy Consolidation, A Breakout Would Target $880, Rising 200dma

Stockcharts.com

The Bottom Line

I have a buy rating on LLY. I like that this high-growth Pharma play has consolidated in the last three months as it grows into its high valuation. A leader in the GLP-1 race, I see more upside ahead with a fundamental fair value of about $1000 per share when considering growth estimates.