Evgeny Gromov

Simply over two months in the past, I wrote on Endeavour Silver (NYSE:EXK), noting that any pullbacks under US$1.67 would supply shopping for alternatives. Since dropping into this purchase zone, the inventory has rallied over 70% to its current highs, making it one of the highest performers sector-wide. The view that the inventory was lastly a worthy swing-trading candidate was associated to a lot of the negatives already being priced in, evidenced by the inventory shrugging off the upper capex estimate at its Terronera Venture and one other 12 months of margin compression, with AISC margins plunging to three.5% in FY2023 (FY2022: 9.5%). On this replace, we’ll dig into the This fall and FY2023 outcomes launched final month, current developments, and the place the inventory stands immediately after its sharp rally.

Endeavour Silver January 2024 Replace – Looking for Alpha Premium/PRO, Finbox, TIKR

This fall & FY2023 Outcomes

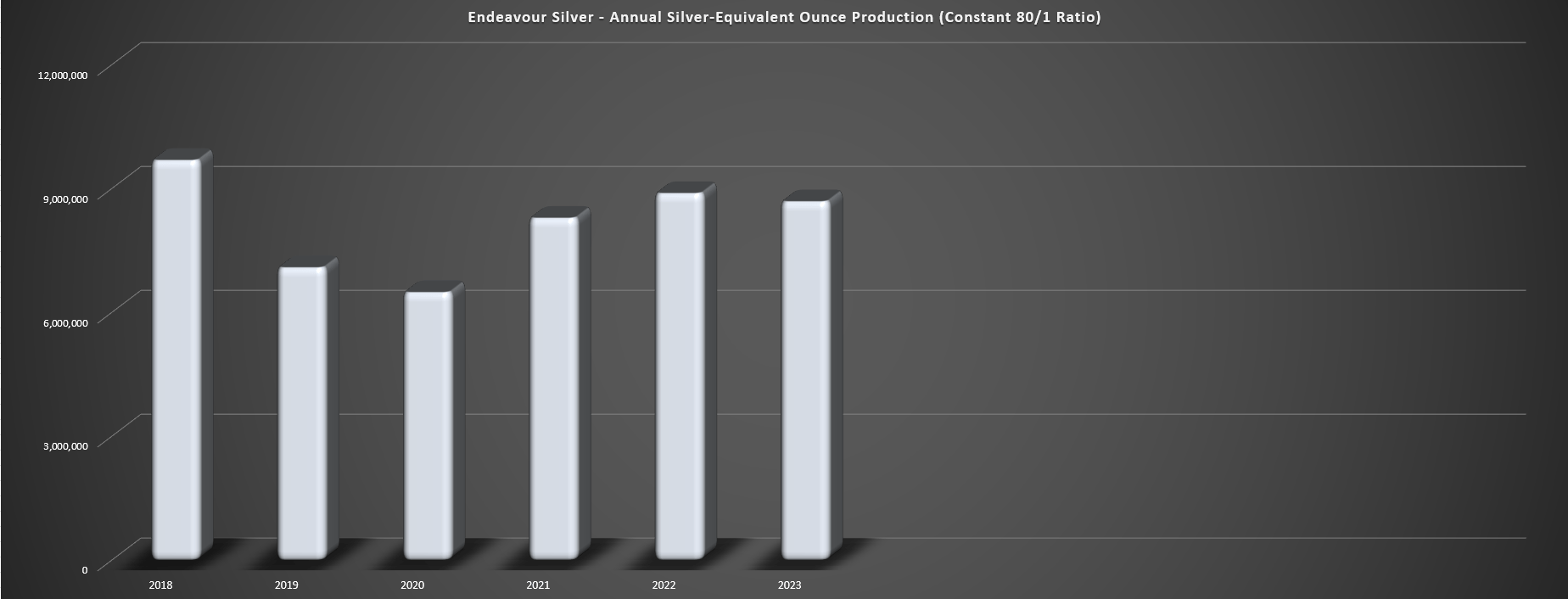

Endeavour Silver launched its FY2023 outcomes final month, reporting annual manufacturing of ~5.67 million ounces of silver and ~37,900 ounces of gold. This translated to a slight miss vs. its steering midpoint of 6.0 million ounces of silver and 38,000 ounces of gold and resulted in decrease income year-over-year ($205.5 million vs. $210.2 million) regardless of greater metals costs. On a per share foundation, the outcomes had been additionally disappointing given the 9% improve in weighted common shares excellent, with silver-equivalent manufacturing per share slipping almost 20% to 0.04 (~8.7 million silver-equivalent ounces produced vs. ~217.2 million shares). Sadly, this determine has solely worsened to start out the 12 months, with Endeavour Silver issuing ~15.9 million shares at US$1.51 beneath its At-The-Market Fairness Facility [ATM] in Q1, placing an additional dent in its per share metrics.

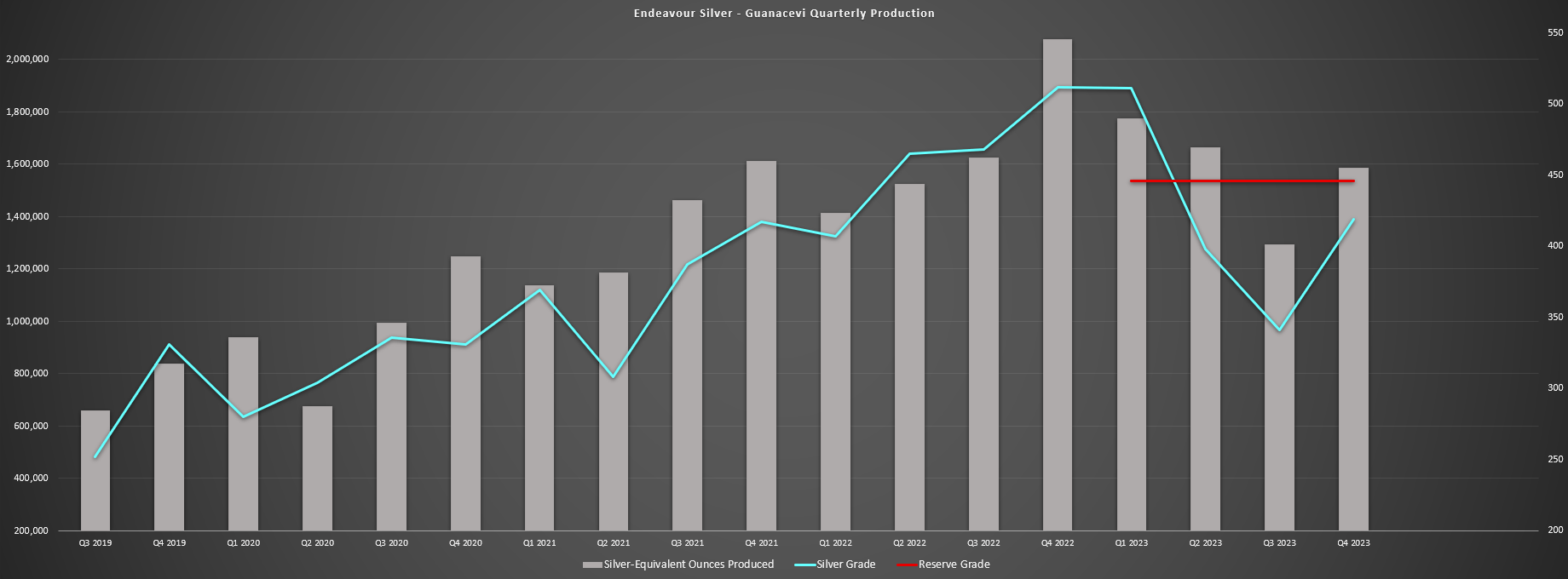

Annual Silver-Equal Manufacturing – Firm Filings, Creator’s Chart Guanacevi Quarterly Manufacturing, Silver Grade & Reserve Grade – Firm Filings, Creator’s Chart

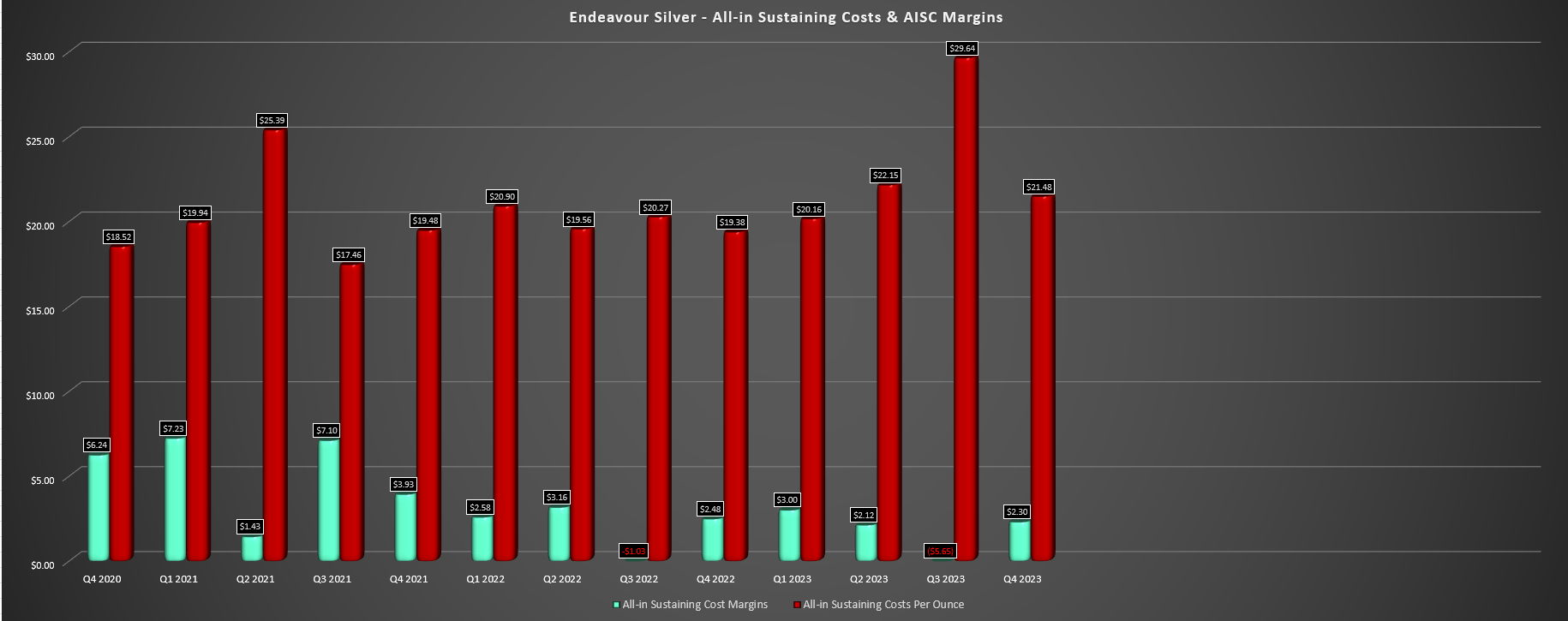

The weaker manufacturing in FY2023 was associated to a dip in grades at its flagship Guanacevi Mine, with the 5% greater throughput (~433,400 tonnes processed) greater than offset by a ten% dip in common silver grades and an 11% decline in gold grades to 417 and 1.19 grams per tonne, respectively. These decrease grades had been partially due to modifications in mine sequencing to deal with enhancing air flow on the underground mine, with grades dipping under price range in Q2 and Q3. And with fewer ounces produced plus the impression of inflationary pressures and persistently sturdy Mexican Peso (MXN/USD), all-in sustaining prices [AISC] at Guanacevi soared to $22.23/ozvs. $18.43/ozwithin the year-ago interval, leading to Endeavour’s consolidated prices coming in over 17% above its steering midpoint of $19.50/oz.

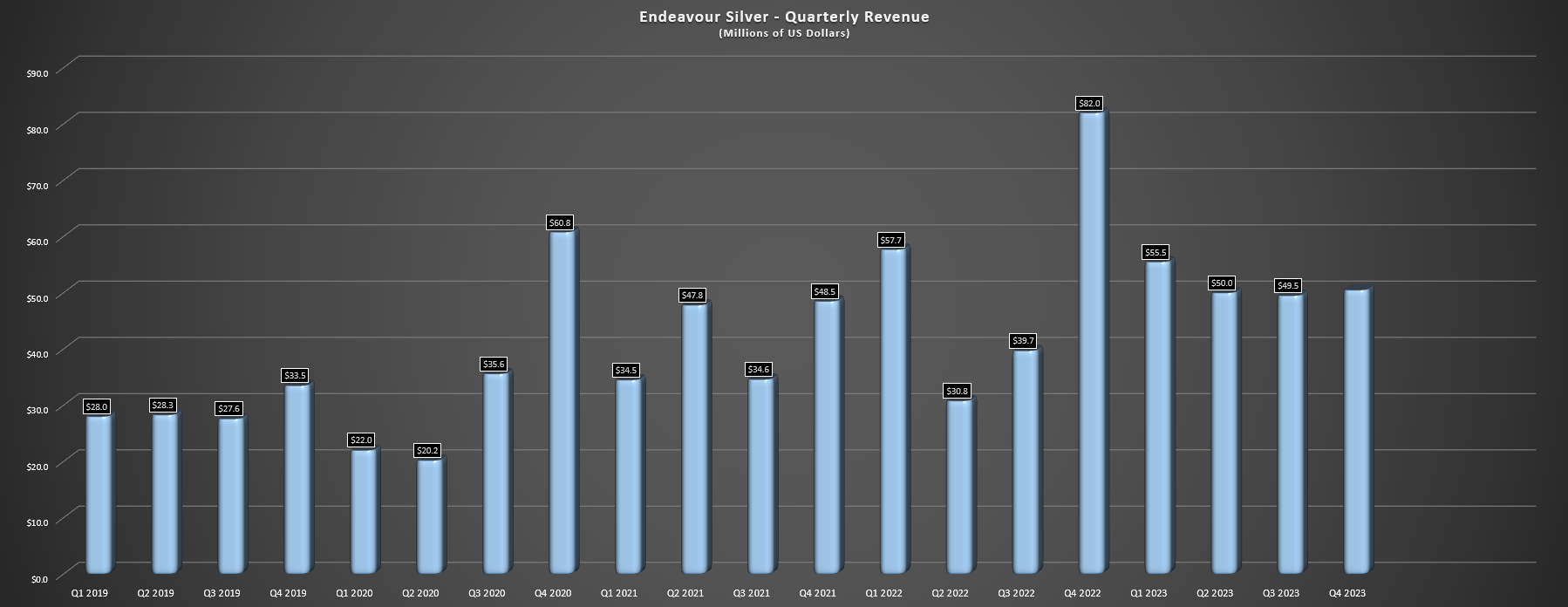

Endeavour Silver Quarterly Income – Firm Filings, Creator’s Chart

Digging into the monetary outcomes, there wasn’t a lot to put in writing dwelling about regardless of the backdrop of rising metals costs, with income declining 2% year-over-year to $205.2 million on the again of decrease gross sales, and working money circulate earlier than working capital plunging 31% to $37.0 million vs. $54.0 million in FY2022. In the meantime, adjusted earnings slipped to $1.7 million (FY2022: $6.9 million), and whereas Endeavour completed the 12 months with ~$35 million in money and a internet money place, it had vital share issuance to thank for its stronger steadiness sheet, with over $62 million in proceeds from fairness gross sales, together with ~23.4 million shares issued beneath its earlier ATM (June to November 2023) at $2.47, and a further ~2.3 million shares bought at $2.06 in December 2023 beneath its new ATM. Sadly, the promoting appears to have continued since its year-end report, with the corporate at present having nearer to 240 million excellent shares.

Prices & Margins

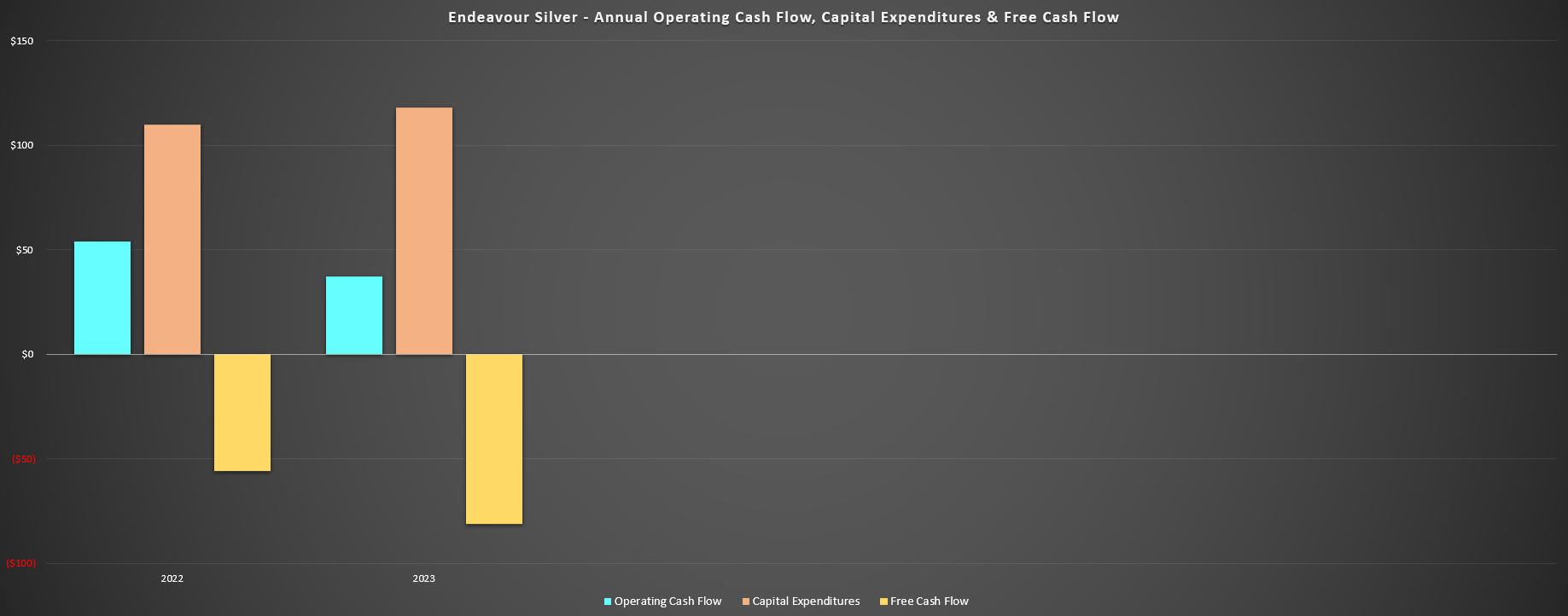

prices and margins, we noticed continued margin compression in FY2023, with AISC margins sinking to $0.83/ozvs. $2.10/ozin FY2022. This translated to a 600 foundation level decline in AISC margins (3.5% vs. 9.5%), impacted by inflationary pressures, a stronger Mexican Peso, and fewer ounces bought, offset by decrease sustaining capital spend for the 12 months. Sadly, this resulted in vital free money outflows when mixed with greater capex due to building at its Terronera Venture, and the rise in annual AISC from $19.97/ozto $22.93/ozwas regardless of the advantage of greater gold by-product credit with a median realized gold worth of $1,968/oz (FY2022: $1,814/oz).

Endeavour Silver – Annual Working Money Movement, Capital Expenditures & Free Money Movement – Firm Filings, Creator’s Chart Endeavour Silver Quarterly AISC & AISC Margins – Firm Filings, Creator’s Chart

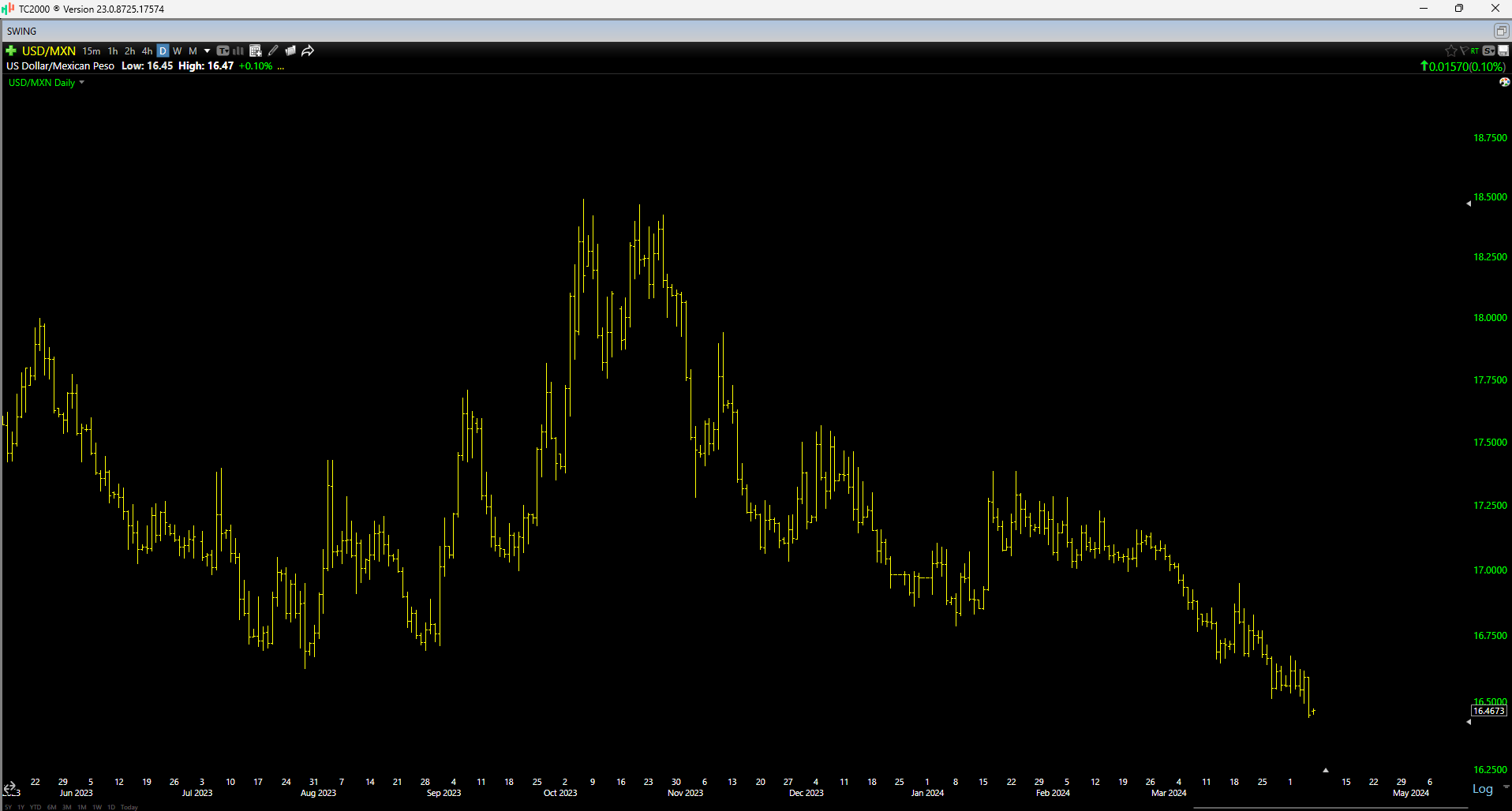

Digging into the This fall outcomes, Endeavour centered on the truth that prices improved sequentially from Q3 2023 ranges, however this was largely due to being up in opposition to straightforward comparisons. And whereas This fall AISC improved from $29.64/ozto $21.48/oz, prices had been nonetheless effectively above the business common and margins had been razor skinny at simply $2.30/oz. Plus, prices had been up sharply on a year-over-year foundation from $19.38/ozand direct prices per tonne elevated 10% year-over-year to ~$171/tonne, with Endeavour calling out “increased labor, power, and consumables costs”. The one excellent news is that Guanacevi is again into higher grades as of This fall and FY2024 steering has been set at $22.50/oznet of by-product credit, with the potential to come back in under this determine if the gold worth can proceed to climb. On a unfavourable word, the MXN/USD continues to energy excessive, making one other set of latest highs, which is not any assist to Terronera building prices (which have already increased materially) nor its working prices at Guanacevi and Bolanitos.

USD/MXN – TC2000

Latest Developments

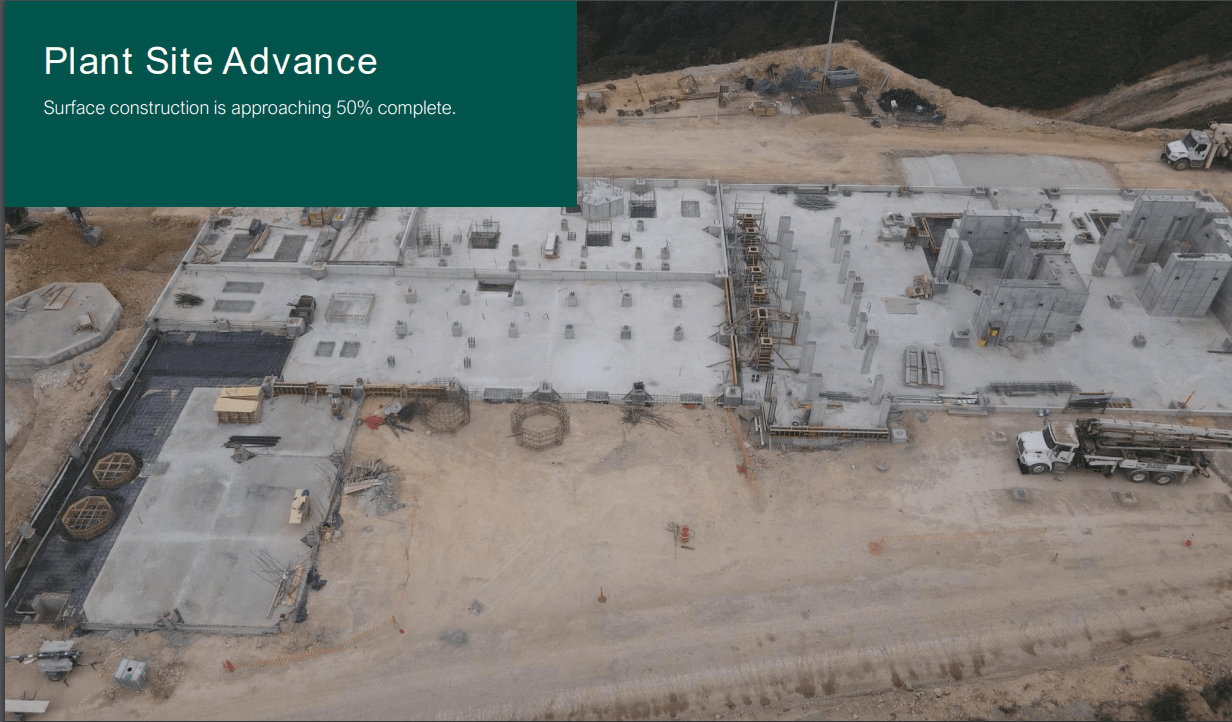

Happily, there may be some excellent news. This information comes within the type of its Terronera Venture, which is nearing 50% completion, albeit at greater capital expenditures of ~$271 million vs. ~$230 million beforehand. For these unfamiliar, Terronera is a excessive margin silver-gold undertaking in Jalisco state, Mexico, with a 10-year mine life, and estimated annual manufacturing of ~4 million ounces of silver and ~7 million silver-equivalent ounces [SEOs]. Endeavour has spent over $120 million on direct growth thus far, with over 60% of the up to date capital price range dedicated and continues to anticipate This fall 2024 commissioning, suggesting industrial manufacturing ought to begin in Q2 2025. Per the latest replace, floor building is 50% full, growth charges proceed to enhance, with 2,200 meters accomplished in 2023 and the primary ore growth is anticipated in Q2, with long-hole mining set to start in Q3 to construct a stockpile forward of commissioning.

Terrona Venture Building – Terronera.com

Though we’re nonetheless a 12 months away from industrial manufacturing, Terronera is without doubt one of the better-undeveloped silver belongings that is set to have working prices within the backside quartile of the price curve. And whereas the undertaking’s estimated all-in sustaining prices [AISC] of ~$9.80/ozare trying far too bold given the place the Mexican Peso sits immediately and the impression of inflationary pressures, even ~$12.00/ozAISC can be a really stable final result for an organization at present struggling to carry prices under the $22.00/ozAISC degree. And whereas Endeavour will see one other 12 months of serious free money outflows because it sits within the coronary heart of the construct out section in 2024, 2025 will likely be a much better with the potential to generate upwards of $60 million in free money circulate even at conservative metals worth assumptions. So, whereas the present monetary outcomes go away loads to be desired, Terronera is a significant improve for the corporate.

Valuation, Per Share Progress & Technical Image

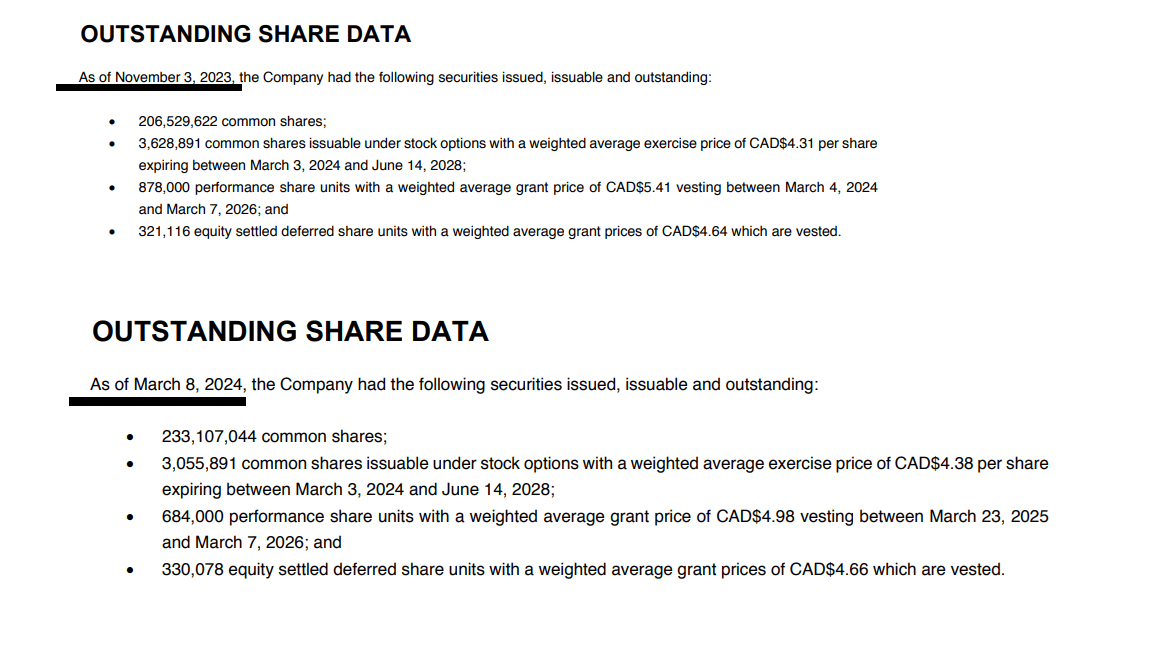

Based mostly on ~243 million absolutely diluted shares and a share worth of US$2.85, Endeavour Silver trades at a market cap of ~$695 million. It is a vital improve from the place I highlighted the inventory as a Purchase under US$1.67 earlier this 12 months at a market cap of ~$350 million. The fabric improve out there cap is partially associated to the truth that we have seen a pointy rally within the share worth, however we have additionally seen over 13% share dilution since November 2023, with the absolutely diluted share rely rising from ~211 million to over 240 million shares at present. Therefore, even on a continuing share worth foundation, the inventory is sort of 15% dearer given the share dilution that buyers have seen at depressed ranges.

“Subsequent to December 31, 2023, the Company issued an additional 15,861,552 common shares under the December 2023 ATM Facility at an average price of $1.51 per share for gross proceeds of $23.9 million, less commission of $0.5 million.”

Excellent Share Knowledge – Firm Filings

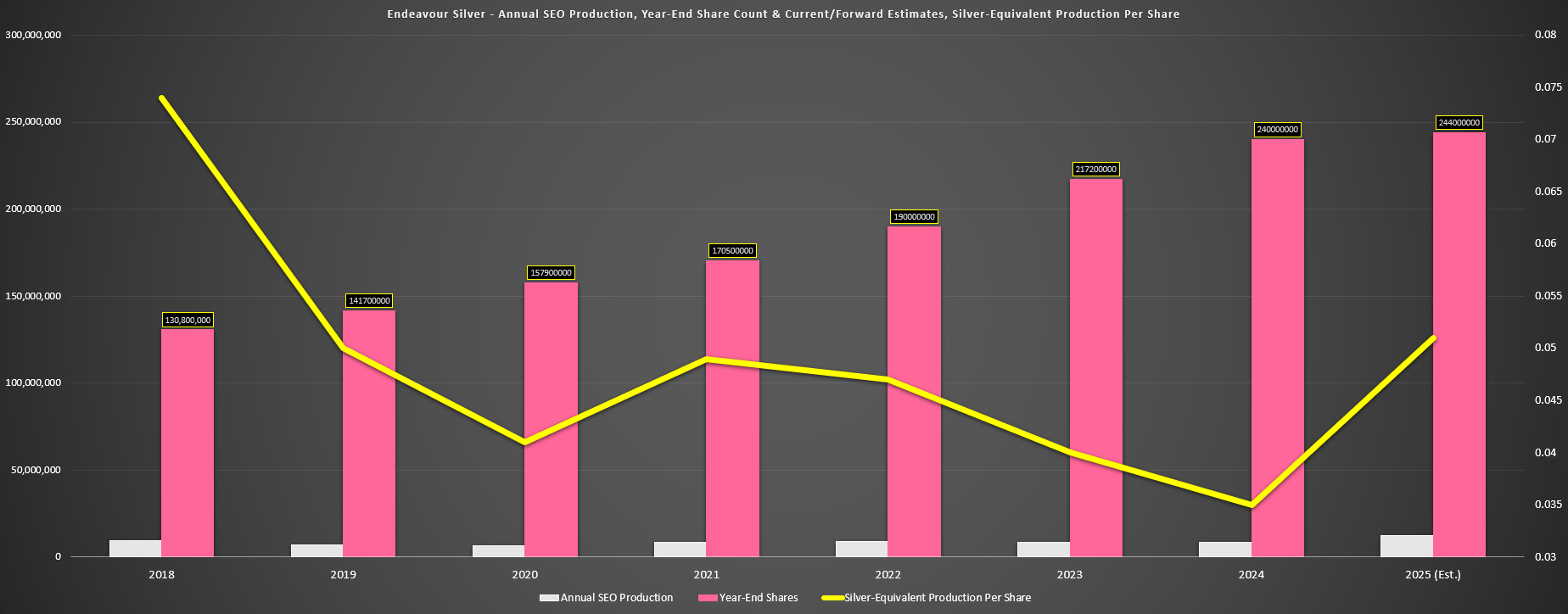

As discussed in past updates, the addition of a bigger and lower-cost operation (Terronera) is actually a constructive, however the monsoon of share dilution that is rained on buyers has meant that the advantages of Terronera should not being felt as a lot as buyers may need hoped. That is evidenced by silver-equivalent manufacturing per share being down materially from 2018 ranges, even when factoring within the manufacturing increase from Terronera. In actual fact, whereas Terronera will present a 60% plus increase to annual web optimization manufacturing, EXK’s share rely has almost doubled up to now six years from ~130 million shares to 240+ million shares. Therefore, buyers are not seeing the advantage of this manufacturing development on a per share foundation, which is all that ought to matter to buyers.

Endeavour Silver – Silver-Equal Manufacturing, Yr-Finish Share Rely & web optimization Manufacturing Per Share – Firm Filings, Creator’s Chart & Estimates

In case you are investing in valuable metals, it’s probably since you want to protect the buying energy of your wealth and keep away from the erosion attributable to fixed inflation of the cash provide over time. Holding bodily gold and silver bullion will help present that long-term safety. If one desires further leverage on that very same thesis, the logical extension is to personal the mining corporations discovering and extracting that gold and silver. Nevertheless, this latter technique solely works if these gold & silver producers are not less than holding the road or ideally rising their per-share metrics, that means that manufacturing, reserves/sources, internet asset worth and money circulate per share are rising. And whereas business leaders like Agnico Eagle (AEM) and Alamos Gold (AGI) have excelled on this division and constantly grown their per share metrics, this isn’t the case for Endeavour Silver.

This doesn’t imply that the inventory doesn’t make swing-trading car, and it has actually rallied sharply off its lows. Nevertheless, names that can’t develop per share metrics and have a poor monitor document of delivering shareholder worth are trades, not investments, and they’re greatest handled as scorching potatoes. Because of this when they’re not providing a margin of security, it is typically greatest to cross them on and lock in not less than some earnings. And whereas a rising tide (silver worth) will elevate all boats, EXK now trades at ~1.3x NAV which is a premium to extra diversified and better-run producers in superior jurisdictions like Agnico Eagle, and a premium to some higher-margin royalty/streaming corporations like Sandstorm Gold (SAND).

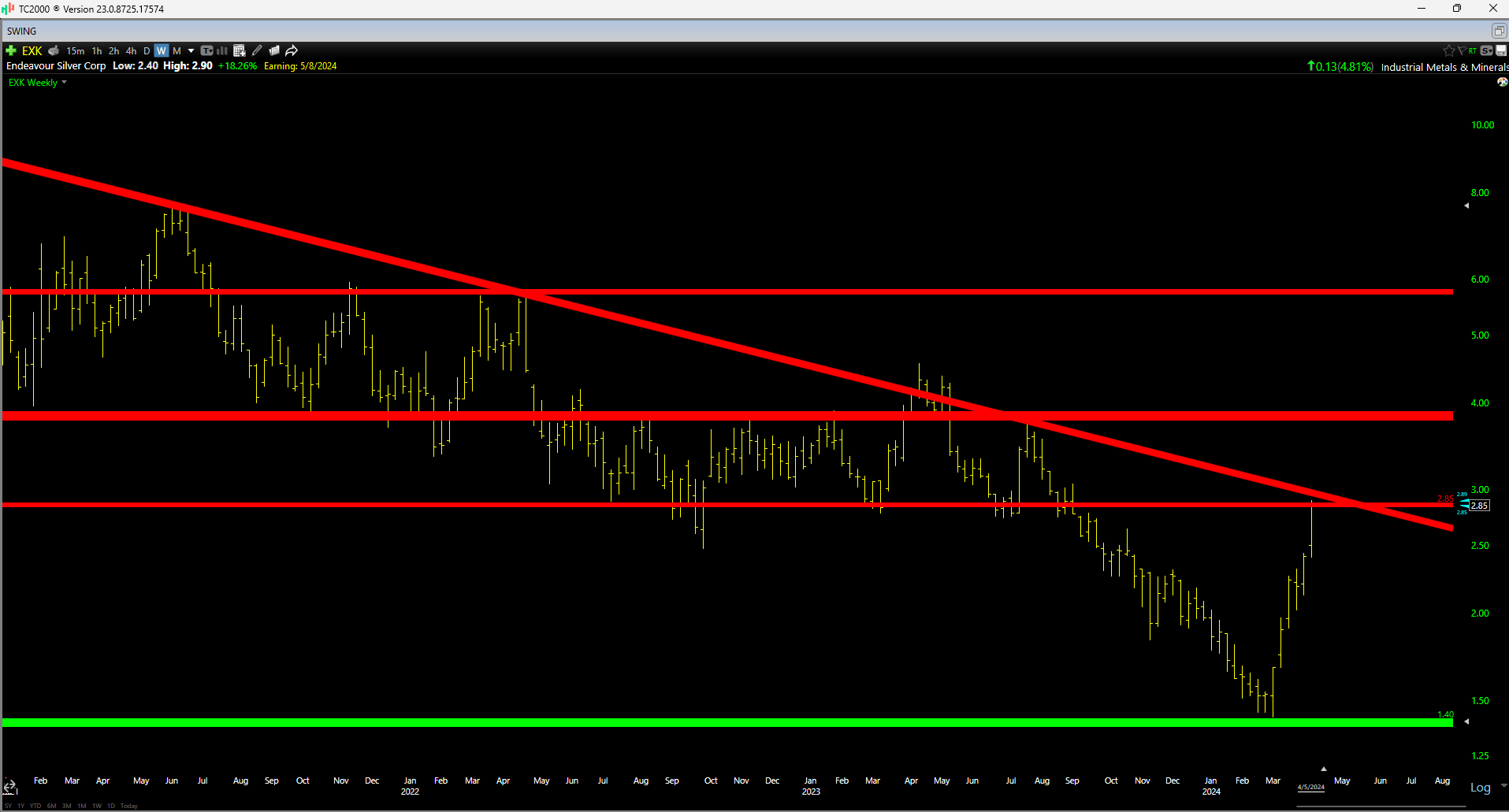

EXK Weekly Chart – TC2000

Wanting on the technical image, this corroborates this view, with EXK working straight into its prior damaged assist degree within the US$2.85 – US$3.00 area. This space could also be a sticky level for the inventory as those that purchased at these ranges over the previous two years is perhaps anxious to get out at break-even, and it does not assist that the inventory is not oozing worth prefer it was one quick month in the past under US$1.70 per share. So, whereas EXK may head greater medium time period, I do not see any method to justify chasing the inventory above US$2.90.

Abstract

Endeavour Silver is lower than a 12 months away from industrial manufacturing at Terronera, a milestone that may assist morph the corporate from a high-cost producer right into a extra aggressive producer. Nevertheless, not like another corporations including new operations which might be seeing a jurisdictional enchancment like Calibre (OTCQX:CXBMF), Terronera does not present diversification exterior Mexico or protect the corporate from the sturdy Mexican Peso. And as a solely Mexican producer, I feel it is tough to make a case for paying over 1.30x P/NAV for the inventory immediately. So, whereas I might contemplate EXK if we had been to see it transfer onto a brand new technical purchase sign, I proceed to see way more enticing bets elsewhere within the sector, with one identify being i-80 Gold (IAUX) that trades at ~0.25x P/NAV in a Tier-1 ranked jurisdiction with one high-grade mine and three high-grade tasks (Cove, Ruby Hill, Granite Creek Open Pit) and a path to manufacturing of ~400,000 gold-equivalent ounces later this decade.