Vithun Khamsong/Second through Getty Photos

Enbridge (NYSE:ENB) and Enterprise Merchandise Companions (NYSE:EPD) are each well-known infrastructure gamers within the standard vitality house. Their focus is usually within the mid-stream section, which brings secure and predictable revenues. The contracts are often underpinned by wholesome and established our bodies that assist de-risk the top-line even additional.

Relating to the stability sheet, each ENB and EPD are secure and may clearly entry chep and versatile financing because of the wholesome leverage and protection metrics.

The mix of secure income element and powerful monetary profile, permits these two corporations to accommodate actually engaging yield-levels that ought to fulfill most dividend-seeking buyers.

Furthermore, the financial outlook for Enbridge and Enterprise Merchandise Companions is vibrant. One of many key drivers for the midstream infrastructure is the movement and manufacturing of pure gasoline, which is projected to not solely stay on the present ranges, that are already favorable, but additionally to proceed advancing greater all through 2024.

International X Administration Firm

Lastly, as these companies are per definition capital-intensive that requires to ceaselessly faucet into the financing markets, the truth that SOFR is projected to decrease ought to present extra increase right here.

With that being mentioned, let’s discover these two corporations in a bit extra element and decide, which one in every of these are set to ship extra attractive returns going ahead. Each are nice, however one is best if we have a look at the character of money flows, stability sheets and valuations.

Enbridge has extra diversified and defensive money flows

Enbridge and Enterprise Merchandise Companions function primarily throughout the next segments:

- Liquid pipelines

- Pure gasoline pipelines

- Gasoline utilities and storage

Consequently, the lion’s share of revenues are price based mostly and contracted in opposition to “cost of service” kind of agreements. This introduces fixed-income like dynamics, which permits to simpler plan future CapEx spend, capital allocation within the M&A entrance, and, most significantly, facilitate secure dividends.

In ENB’s case, 98% of EBITDA stems from these “cost of service” contracts, whereas for EPD the relevant share is circa 77%.

An extra benefit for ENB is the Firm’s presence within the renewable vitality section that injects variety within the general income combine. For Enterprise Merchandise Companions there are not any materials capital allocations on this house.

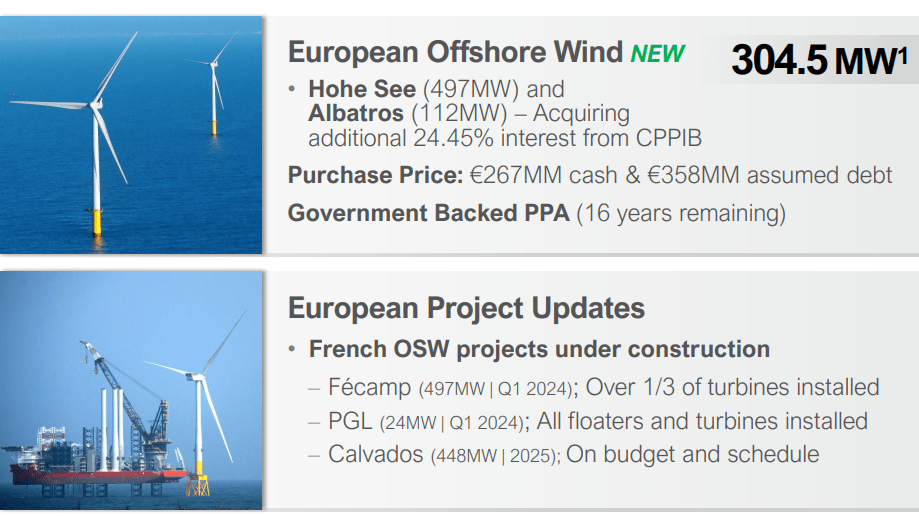

So, if we have a look at ENB’s renewable vitality portfolio, most of those belongings are related to offshore wind that provides uncorrelated publicity to the important thing segments round midstream verticals.

ENB Investor Presentation

At present, 3 of 4 offshore tasks are with already signed PPAs (which primarily present the identical degree of income stability as the opposite belongings) or very near touchdown at their CODs (business operation dates).

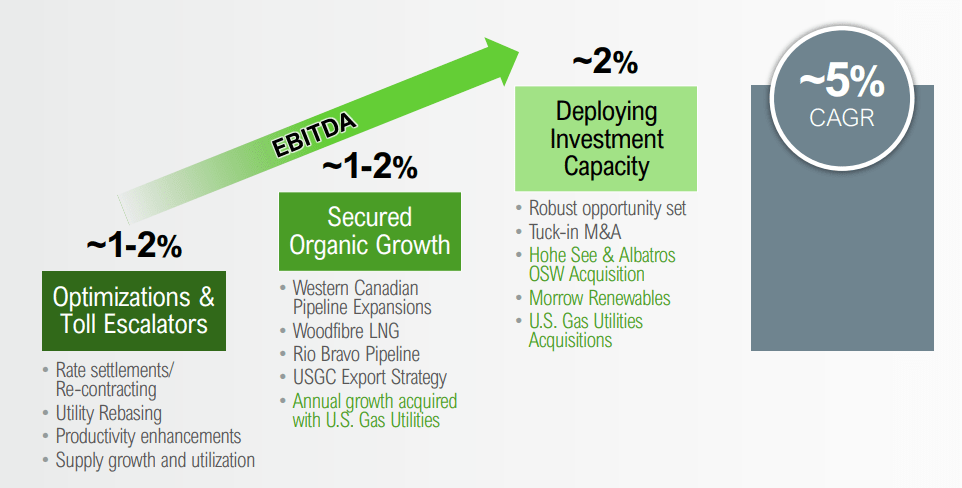

Trying ahead on the medium-term horizon, ENB’s EBITDA is projected to advance by ~5% CAGR, the place about half is defined from embedded escalators (e.g., ~80% of EBITDA is inflation-protected) and natural development alternatives, and the opposite half from M&A and renewables.

ENB Investor Presentation

On the EPS level, Enterprise Merchandise Companions are set to advance at fairly comparable vogue over the following 3 12 months interval.

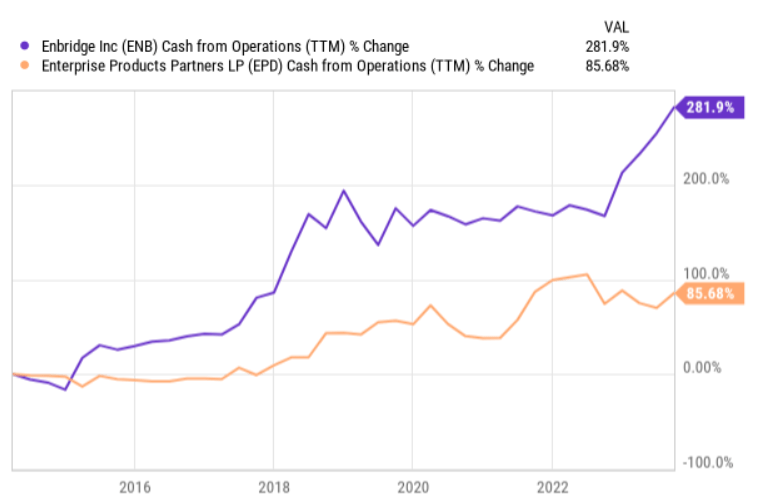

Nevertheless, with regards to the underlying money conversion and development within the money era facet, Enbridge has registered approach higher outcomes than Enterprise Merchandise Companions.

Ycharts

Granted, a few of that is defined by the motion within the stock and there are results from the exterior development channel, however, on the core, ENB has clearly delivered extra improved money flows to its investor base relative to EPD.

Lastly, we have now to additionally respect the truth that Enbridge generates roughly 18% extra in EBITDA (TTM) than Enterprise Merchandise Companions, which in flip renders stronger foundation from which to diversify income sources and fund natural development alternatives.

Enterprise Merchandise Companions has stronger monetary danger profile

Whereas on the money era entrance each corporations are certainly comparatively comparable with some slight benefits for Enbridge, when it comes the stability sheet and the general monetary danger, Enterprise Merchandise Companions takes the lead right here.

First, EPD carries an upper-investment grade credit standing, which isn’t just one notch greater than for ENB, but additionally a relative exception in your complete midstream, MLP section. In follow, it takes fairly of an effort to transition from BBB+ (the case of ENB) to A- (the case of EPD). This isn’t solely a testomony of EPD’s sturdy monetary profile, but additionally an enabler for the Firm to entry cheaper financing at extra versatile phrases.

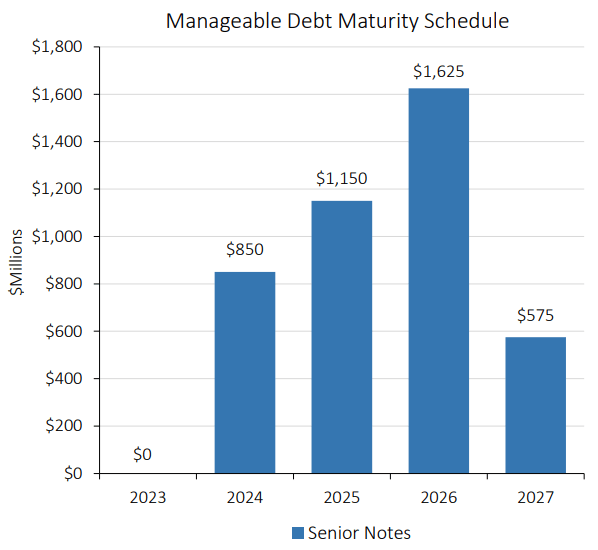

Second, Enterprise Merchandise Companions has extra favorable construction of debt maturities. Each corporations have attracted moderately long-dated financing proceeds, the place majority of those are based mostly on mounted charges under the present market ranges, however in EPD’s case the near-term maturity profile is simply higher.

As we will see within the graph under, EPD has about ~$1 billion of debt to refinance in 2024 and 2025, which collectively account for lower than 7% of the entire excellent borrowings.

EPD Investor Presentation

But, for Enbridge the corresponding annual determine over 2024 and 2025 lands at ~$6 billion, which in flip constitutes ~25% of the entire curiosity bearing debt portfolio.

In sensible phrases, which means that within the subsequent couple of years EPD will be capable to keep away from notable refinancing danger and preserve the presently “locked-in, below market level” financing for longer time period.

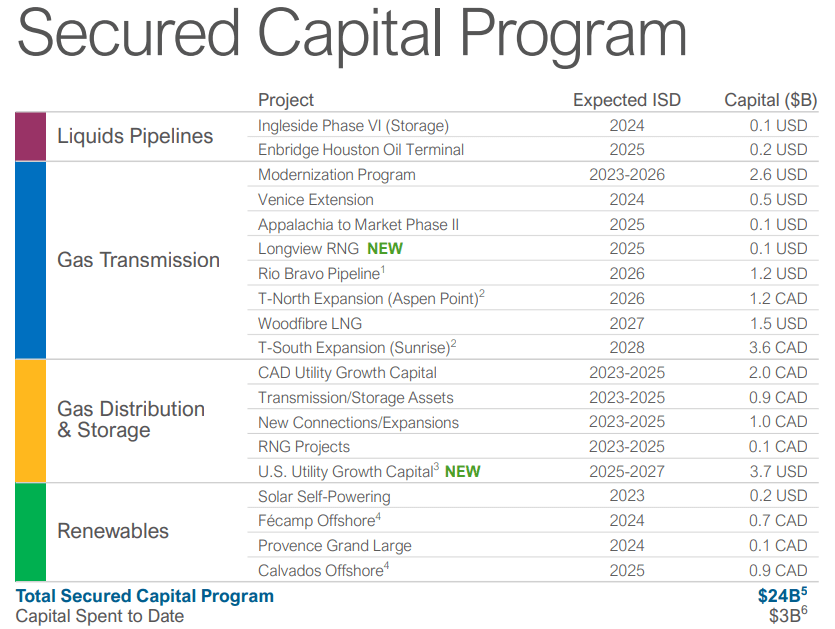

Lastly, when talking concerning the monetary danger, we have now to issue sooner or later CapEx spend that in ENB’s case is moderately astronomical. The desk under highlights that there’s roughly $21 billion of natural CapEx program to finish over the following a number of years.

ENB Investor Presentation

That is large and clearly would require Enbridge to imagine sizeable debt proceeds (throughout an atmosphere of elevated SOFR) even with its cash flow retention of 40%.

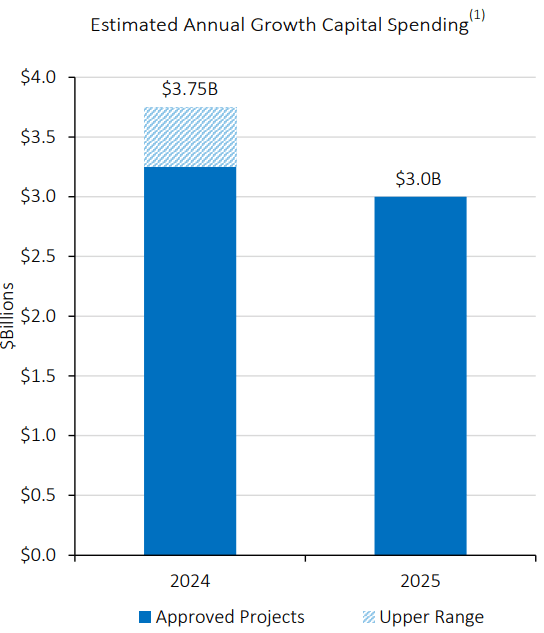

For Enterprise Merchandise Companions, nevertheless, the near-term CapEx plan is far more balanced, indicating much less of a reliance to incremental debt.

4Q 2023 EPD Earnings Slides

In a nutshell, from the monetary danger perspective, EPD is best positioned throughout the important thing areas that matter: greater credit standing, extra back-end loaded debt maturities and decrease monetary strain from the dedicated CapEx plans.

Valuations make the selection straightforward

Given the relative homogeneity within the top-line, however considerably extra balanced monetary danger publicity for EPD, one would anticipate greater dividend yield and perhaps decrease valuations for ENB.

But, as of now, each corporations supply comparable dividend yield ranges at 7.4 – 7.7% (i.e., the distinction is de facto simply ~30 foundation factors). The TTM money movement payout ratio for EPD is 50%, whereas for ENB it stands at 60%. Once more, higher for EPD.

Equally, if we have a look at the important thing valuation metrics, Enterprise Merchandise Companions come out as extra engaging funding case but once more: (evaluating TTM multiples of EPD vs ENB)

- EV/EBITDA of 10.03x vs 13.4x

- P/E of 10.51x vs 17.06x

- P/S (value to gross sales) of 1.18x vs 2.13x

The underside line

There are professionals and cons for each of those corporations, however placing all of it collectively and contextualizing it with the prevailing valuations, Enterprise Merchandise Companions stands out as a superior funding case.

The important thing benefit for Enbridge is that it carries a bit extra diversified top-line together with bigger share of the EBITDA stemming from contracted (regulated) gross sales channels. Nevertheless, Enterprise Merchandise Companions additionally embodies these traits (albeit at lesser diploma), and on the similar time gives a lot stronger monetary profile and extra attractive multiples.

Consequently, I’m recommending to go lengthy Enterprise Merchandise Companions L.P., whereas protecting Enbridge Inc. at maintain largely because of the greater valuations and dangers which are related to additional leverage that might come from its appreciable CapEx program.