Difydave/E+ via Getty Images

Introduction

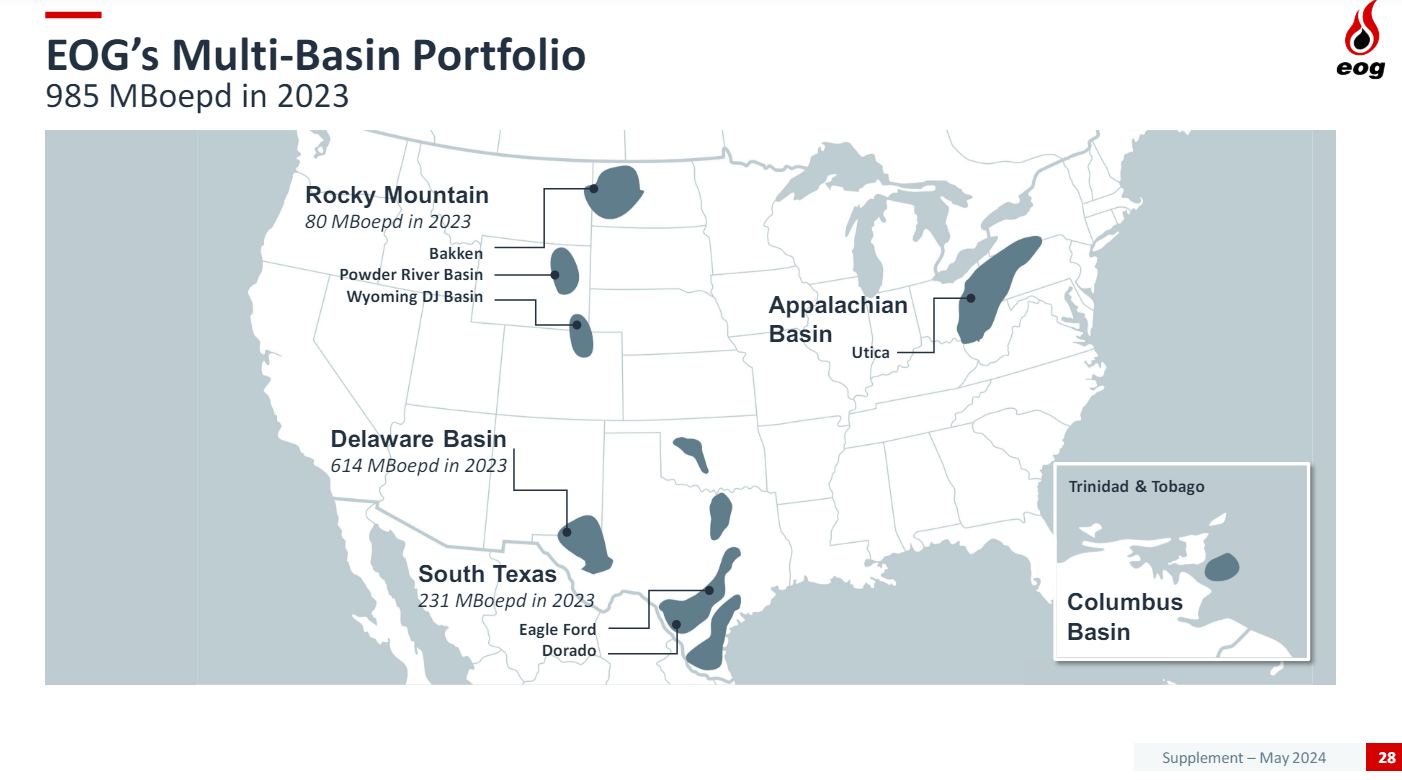

EOG Resources, Inc. (NYSE:EOG) ticks most of the boxes-rock, logistics, LOE, and technology when it comes to the top tier of liquids-weighted shale producers. It’s been on our buy list for a long time and just hasn’t reached a hope-inspired level to allow an entry point. The current sell-off in everything related to oil may present such an opportunity.

EOG Shale Footprint (EOG Resources)

Analysts have been increasing their projections for Q-2 EPS ($2.73-$3.03) and stock price improvement for EOG, based in part on the company has been beating EPS estimates and increasing production. Both are music to the ear. Currently, the stock is rated as Overweight, but that was before the current sell-off from the $130’s to the current $120 level. Price forecasts range from $125 to $169, with a median of $144.50.

At $120, EOG is trading at 5.1X EV/EBITDA and $65K per flowing barrel. Neither are bargain-basement metrics, but this is the EOG we are talking about. EOG is sitting on its 200-day SMA and at the midpoint of support and resistance.

With that preamble, we will take a more in-depth look at our overall thesis for current conditions and the thesis for entering EOG at or near current levels.

Macro outlook for oil

There is no question the macro for oil has weakened since late May, after bobbing around in the low $80’s for most of the month. Doubts about the economy and persistent focus on the Fed cutting rates have dogged the demand picture for crude. Competing forecasts from the IEA and OPEC+ muddied the water still further. The stake through the heart has been the odd 35 mm bbls we’ve added to storage since the first of the year, combined with a lackluster start to the driving season. OPEC’s decision to “try” to unwind cuts is meaningless against that backdrop, and current panic is overdone in my book. Price action today suggests the market may be drinking a second cup of coffee at the price of WTI.

Conversely, there have been a couple of rays of sunshine that should soon start to exhibit themselves in the market. There has been no rebound in drilling despite the ~50% move in gas since the middle of April. The rise in gas appears resilient for many of the reasons we have discussed, and we should soon see an uptick in gas drilling. Most of the oil-weighted drillers are talking about flat or slightly shrinking rig counts for 2024, so that may steepen the production peak we are now seeing in shale liquids output. Production has been essentially flat since the start of the year, with only the Permian and the Bakken registering any growth at all. We just haven’t seen a reason for this dynamic to change as yet.

Note-while we were working on this article, WTI has had an inventory led rally and moved back above $80. Oil stocks have responded in kind.

With that, let’s dig into EOG.

The case for EOG

With its liquids-weighted production, EOG is right in the zone of recent Permian M&A. I think EOG will remain a standalone company at $66 bn. It would be an enormous bite, but it could be done. The Super Majors have made big moves recently, and any further concentration of acreage by them would undoubtedly draw antitrust scrutiny. On the other hand, for example, there is Shell plc (SHEL) sitting there with ~$40 bn in cash on its balance sheet. You can’t rule it out.

On the flip side, we haven’t seen EOG reaching into the bargain bin in the current M&A frenzy, nor are we likely to. Ezra Yakob, CEO, commented in a recent investing conference on this topic-

When we roll up kind of the acquisition opportunities, mergers and acquisitions, and we look at them, dominantly, they come with a lot of production, so it’s a low rate of return. And dominantly, they’re in known plays, which is going to come with a high dollar cost as opposed to the organic exploration effort. As long as we can continue to explore and discover opportunities that are additive to the corporate portfolio, for us, that makes more sense on a full cycle returns approach.

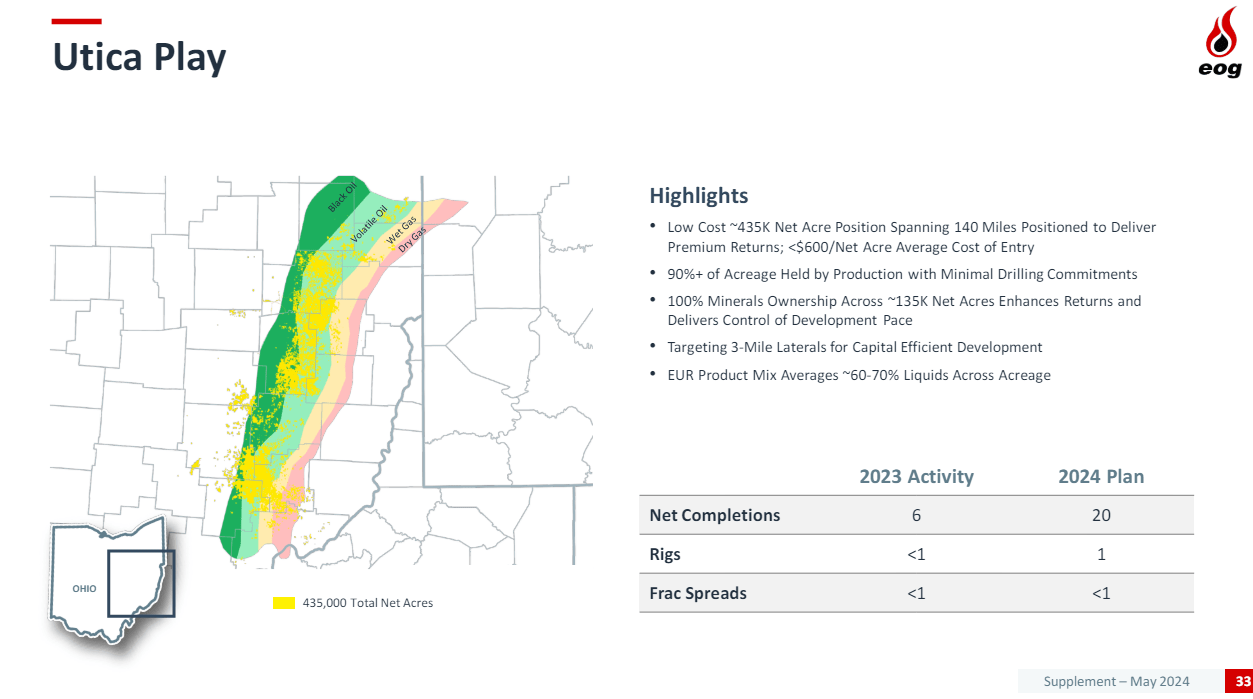

EOG’s most recent major merger was with Yates Petroleum in 2017. In recent times, EOG has made a move into the western Utica/Marcellus “Combo” play, targeting the oily and NGL-rich Utica shale with some potential landing zones in the Marcellus if gas prices justify. We can’t really call this move a near-term catalyst for EOG, as it’s not where they will be spending big sums of capex in 2024. Where they are spending money is in their two core areas: the Permian and the Eagle Ford. We could see this ramp-up in a success case. EOG has a huge footprint here

EOG Utica shale position (EOG Resources)

Catalysts for EOG

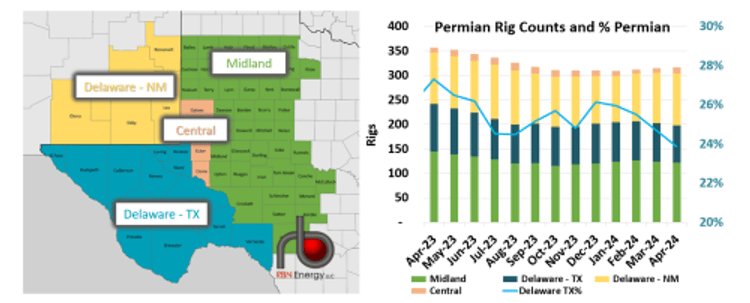

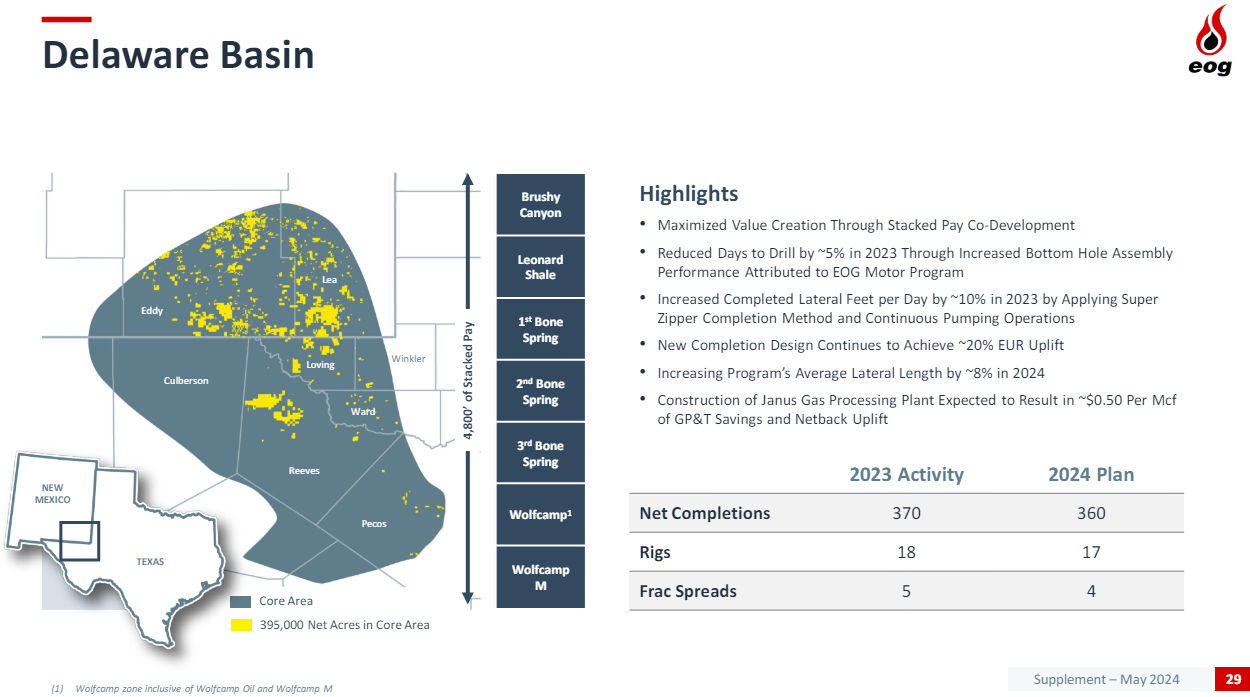

Much of EOG’s acreage in the Delaware is in the choicest parts of the Northern part of the basin that yield lower GORs. A report put out recently by RBN Energy confirms this, with a graph showing rig counts in New Mexico actually increasing incrementally, while other parts of the Permian Basin took a hit.

Rig count focus in Permian (RBN Energy-used with permission)

As we’ve noted, much of the M&A activity is being driven by the desire/need to acquire Tier I drilling inventory, and an anticipated future demand for liquid fuels, and heavy gas liquids used in plastics production.

EOG is known for driving field margins through cost control. Not necessarily low-bidding vendors, but pushing for greater efficiencies from established vendors. One of the ways this shows up is by pushing the technology envelope. Super Zipper fracs are an example of fracking two wells simultaneously while wire lining on two others. Not for new hires or the meek. The law of large numbers kicks in and wells get cheaper. Ezra Yakob comments on their contracting strategy:

The way we structure our agreements, typically, we like to partner with high quality equipment, high -quality crews, because ultimately, what we focus on lowering well cost are really the operational efficiencies. We like to increase operational efficiencies. And that takes good equipment, and it takes stakeholder alignment between us and our partner vendors. And we’re seeing great progress on that this year. Drilling times, drilling efficiencies have increased year-over-year in our core place.

EOG Delaware basin footprint (EOG Resources)

It is also worth noting that the crude coming out of the New Mexico side of northern Delaware is particularly advantaged by its relatively low API gravity-sub 40 API. This makes it more useful for blending in U.S. refineries than the higher grades coming out of southern parts of the basin.

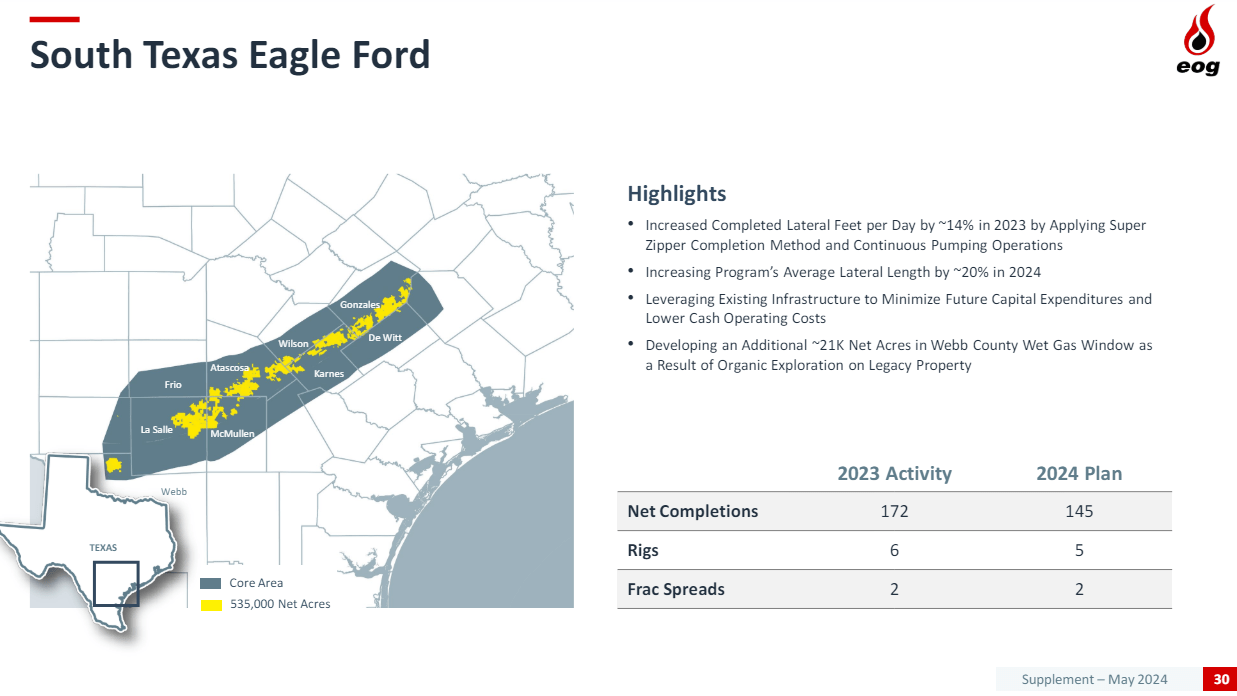

The Eagle Ford (EF) is the next busiest area where EOG will be allocating capital. The EF has just been ripping with M&A activity over the last couple of years. RBN noted the frenzied pace and the key players in a recent blog post:

- Devon Energy’s $1.8 billion purchase of Validus Energy, a privately held Eagle Ford producer, which closed in September 2022.

- Marathon Oil’s December 2022 acquisition of Ensign Natural Resources’ Eagle Ford assets for $3 billion

- Spanish energy giant Repsol’s February 2023 purchase of the South Texas acreage and production of Japan’s INPEX Corp. for an undisclosed amount.

- U.K.-based INEOS’s purchase of some of Chesapeake Energy’s South Texas assets for $1.1 billion – a deal that was finalized in May 2023.

- Canadian producer Baytex Energy’s June 2023 acquisition of Eagle Ford pure-play Ranger Oil in a cash-and-stock deal valued at $2.2 billion.

- The $551 million purchase by privately held Ridgemar Energy of Callon Petroleum’s Eagle Ford assets, which closed in July 2023.

- The recently announced, $22.5 billion plan by ConocoPhillips to acquire Marathon Oil-both companies have a significant presence in the Eagle Ford.

- And most recently, Crescent Energy’s pickup of Silverbow Resources.

EOG EF Footprint (EOG Resources)

This naturally leads to the question: what’s up in the EF? Part of the driver for EF acreage deals is the opportunity to go back into older wells with new technology. Horizontals have doubled or tripled in length in the last 15 years, and AI-enhanced reservoir studies have made oil companies smarter about lining up subsurface targets and well spacing. New completion technology stages and frac intensity have tied a bow around this shale “elder statesman.”

Another attractive feature of the EF is its proximity to the export hub of Corpus Christie. All the concerns about “field bottlenecks” go away in the EF. By virtue of its “elder” status, the EF is rich in takeoff infrastructure as compared with the Permian.

Without doing a lot of LOE, field expense, and capex per barrel comparisons, we can see that a Return on Capital Employed-ROCE comparison shows that EOG is performing at a top-tier level in the shale cohort.

ROCE of EOG and shale cohort (EOG)

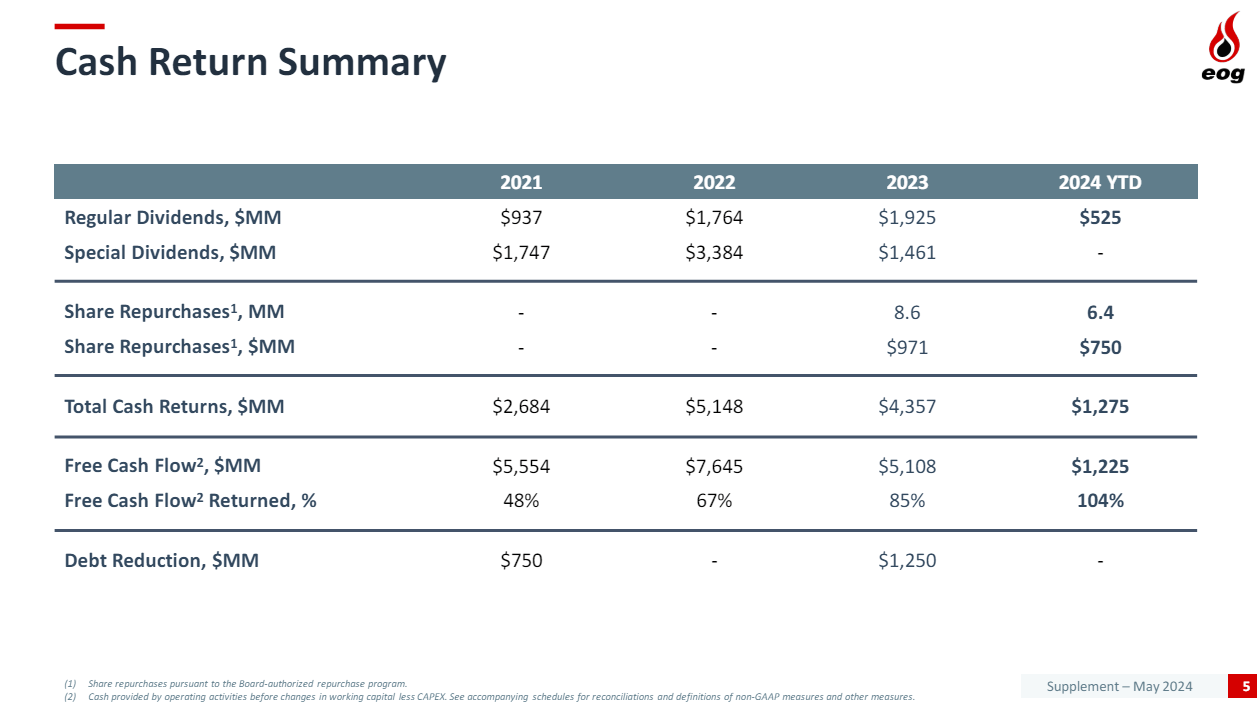

EOG is committed to returning capital to shareholders via its 3% yielding base dividend with an occasional boost from a variable feature. EOG has returned an average of about $4.5 bn over the last couple of years and is certainly on a pace to maintain that rate this year. It has a bias toward special dividends as opposed to buybacks, but the CEO noted that in 2024 that might reverse, while maintaining an overall 70% capital return policy.

EOG Capital Allocation Plan (EOG Resources)

Risks

U.S. producers are price takers, not price setters. That honor goes to OPEC+ due to their productive capacity and ongoing restraint-withholding millions of barrels per day to bolster prices. All indications are they intend to exercise restraint, but history tells us they can change that outlook for various reasons. Any shift in OPEC+ strategy would adversely affect EOG.

Your takeaway

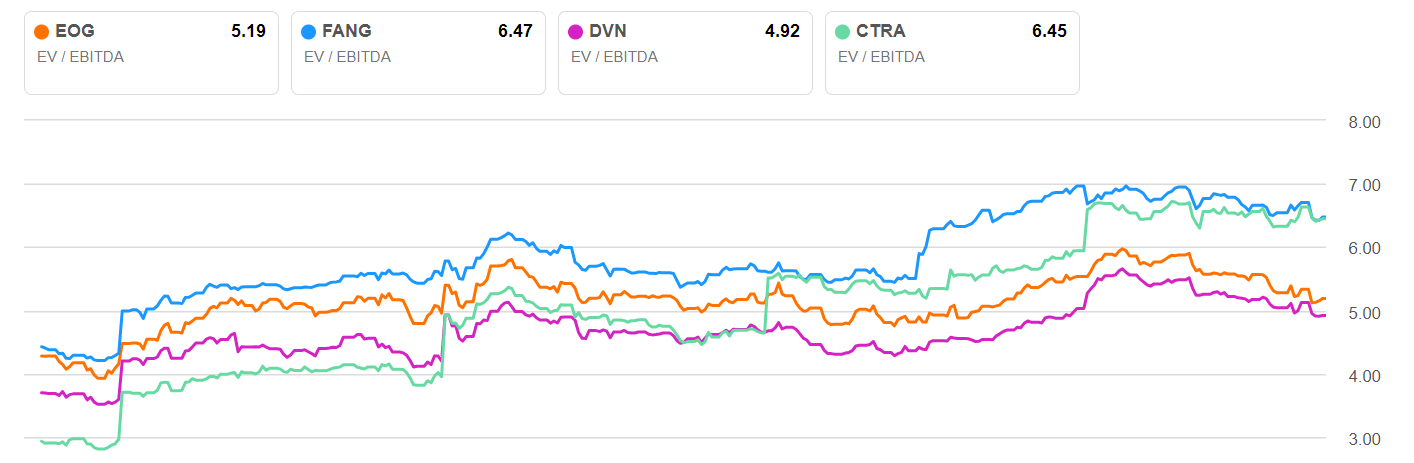

EOG is down from a recent high of $137. It trails only Diamondback Energy, Inc., (FANG) and Coterra Energy Inc. (CTRA) on a TTM EV/EBITDA basis. If we were to give EOG FANG’s multiple, shares would re-rate back toward the $137 level. Not anything to make you do backflips. Growth in EBITDA this year to the tune of about

EV/EBITDA of shale players (Seeking Alpha)

+6% in BOEPD should bump EBITDA to ~$14 bn and potentially deliver that increased multiple handily.

Two things might impact the share price for EOG meaningfully. The first is a buyout – not something we expect, but I would expect a 25% premium to prevailing share prices, putting an offer in the $150-$160 per share range.

Finally, a sustained rally in WTI could do the same thing, or perhaps compound it. EOG Resources, Inc. is an outstanding company in a horrible market. I think investors looking for near-term growth and increasing shareholder returns should carefully consider whether EOG meets their investing profile.