Editor’s notice: In search of Alpha is proud to welcome Mapache Investing as a brand new contributor. It is easy to change into a In search of Alpha contributor and earn cash on your finest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click here to find out more »

EPR wants individuals to flock to the amusement parks SanneBerg/iStock through Getty Photos

The Thesis

Surviving the COVID disaster has not allowed EPR Properties (NYSE:EPR) a possibility to bloom in 2023; slowed progress and never sufficient money for enlargement go away EPR going through uncertainty forward as rising inflation and unpredictable modifications in rates of interest change into the primary risks for this yr; it is higher to be cautious and Maintain on the present costs.

What’s The Enterprise Behind The Enjoyable?

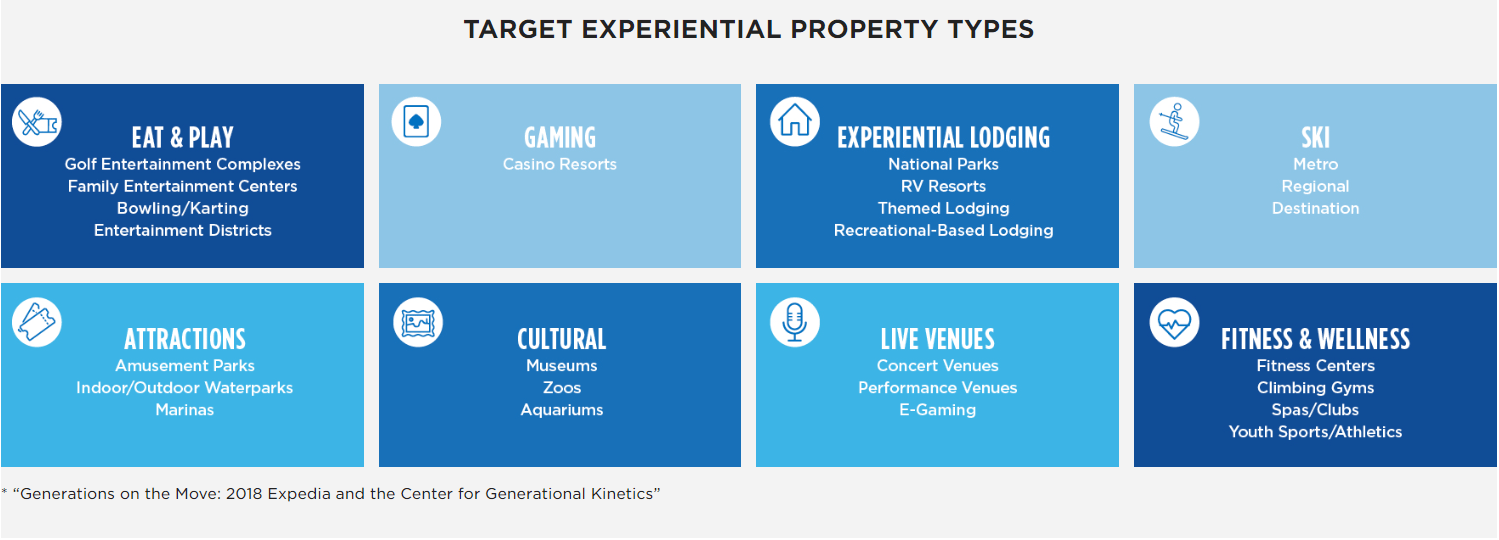

EPR is a diversified experiential REIT. Its holdings are service companies that present expertise within the type of completely different experiential properties, starting from golf complexes and amusement parks to yoga spas, snowboarding resorts, casinos, zoos, museums, and plenty of extra.

EPR classifies them by kind and at the moment holds $6.8B+ in Investments, unfold throughout 359 places in 44 states and Canada. With such an intensive and well-diversified portfolio of investments, having them grouped by kind turns into crucial.

EPR web site

Diversified Leisure, A Portfolio Of Experiences

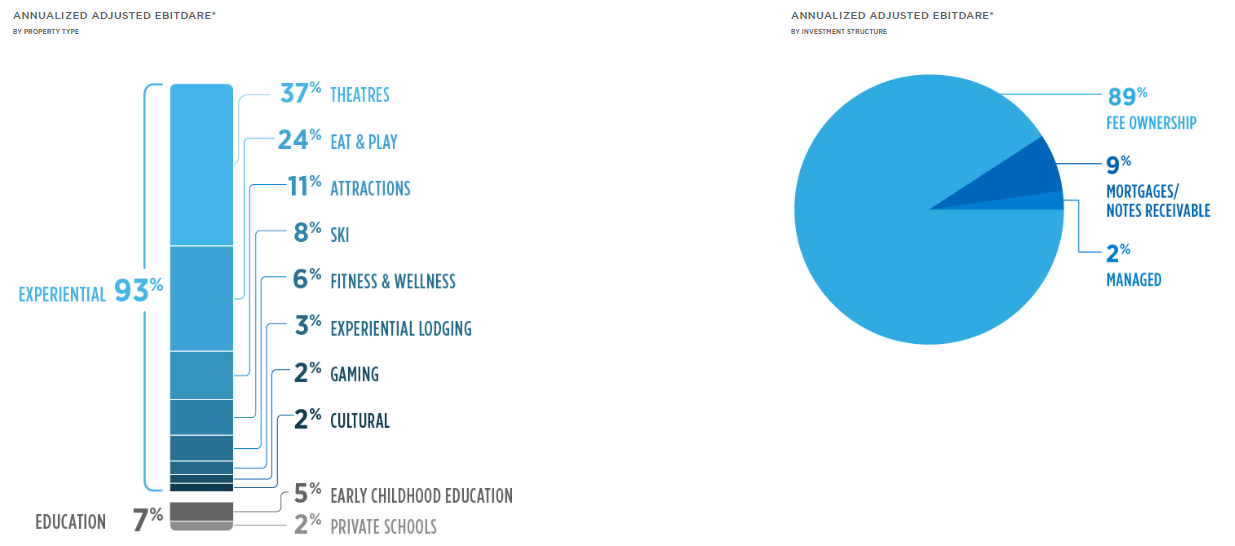

EPR holds $6.8B+ in 44 States and Canada, with over 200+ tenants; their central holdings are in cinema theaters as it’s the unique focus of the REIT, with Eat & Play facilities being an fascinating angle, as they provide a extra various expertise, offering an thrilling different to common eating locations and will doubtlessly be on the trail to change into as clients new most well-liked night time out.

The 7% in training is taken into account a legacy funding by the corporate. Nonetheless, they supply extra diversification and properly spherical up a portfolio primarily centered on enjoyable and discretionary spending.

EPR has diversified its enjoyable issue (EPR web site)

There’s a generational divide between child boomers and millennials (Who would have guessed!). The older era had an ownership-of-things mentality, while millennials look for experiences instead of things. Additionally they have elevated model loyalty if you may make the impression of the expertise worthwhile; this shift might be a reasonably good long-term driver of progress for EPR, primarily as the corporate focuses on high-quality experiences with a really diversified catalog and a few distinctive choices like Artmaint facilities the model has each an enormous and strong base and a few greater danger extra modern avenues.

On the detrimental aspect and from their 10-K page 3:

As of December 31, 2023, our owned theatre properties had been leased to 17 completely different main theater operators. A good portion of our complete income was from AMC and Regal. For the yr ended December 31, 2023, roughly $94.7 million, or 13.4%, and $103.7 million, or 14.7%, of the Firm’s complete income was from AMC and Regal, respectively.

Although it is by no means good to thoroughly depend upon one main buyer, the 14.7% will not be that prime however presents their distinctive dangers, as AMC and Regal’s main trade is cinemas.

As ticket gross sales proceed to say no yr after yr, as more people decide to stream their movies instead of a night out in the cinema, EPR might be left holding a dropping bag of cinema theaters and a hazard that may be compounded with elevated inflation, with cinema ticket prices average $10.78 vs. Netflix subscription of $8.99 a month cinemas appear poised to be struck by inflation, as soon as once more compounding the already dangerous place of the main portfolio.

Considerably, 2024 is projected to be a yr of 5% lower ticket sales for cinemas.

The 37% of theater holdings remains to be an important a part of the REIT, however administration is taking steps towards decreasing the share of earnings that will depend on theaters, increasing on different areas.

Inflation And Water Parks, One Is Enjoyable, The Different Not So A lot

The corporate acknowledges that the 2 most vital components outdoors its management are inflation and rates of interest. They’ve essentially the most vital influence on the highest line (Inflation driving clients away) and the underside line (rising rates of interest making their CAPEX prohibitively costly).

Whereas a lot of the economic system is instantly affected by the FED, it certain can hit more durable an organization depending on discretionary buyer spending for his or her earnings and whose construction is capital intensive.

As service inflation has been the main motor behind inflation to this point, EPR may use 2024 with decrease inflation and decrease rates of interest, with the REALLY worst-case state of affairs being, after all, excessive inflation inflicting clients to shrink back from discretionary spending, answered by the FED with an rate of interest hike inflicting mortgage prices to skyrocket and bringing a chapter cascade on the EPR’s holdings and taking the entire REIT down beneath.

Competitors In The Enterprise Of Leisure

Their greatest rival is VICI (VICI), an enormous experiential REIT with prized places within the Vegas Strip and a market cap of practically ten occasions extra, VICI 30.842B vs. EPR 3.146B. Fortunately for EPR, the primary focus of VICI is within the on line casino trade. The places of each REITs do not have such a substantial overlap that the smaller EPR might be threatened and even pushed out of the market by outbidding or comparable.

VICI map of places (VICI web site) EPR map of places (EPR web site)

The extra spread-out EPR places additionally present extra geographical diversification and entry to extra native US markets, so it is a web constructive for the corporate.

But experiential REITs are comparatively new, and historical past has proven many times that the businesses which are the trailblazers many occasions find yourself being swallowed by the opponents that may enhance the brand new enterprise mannequin and exploit all of the weaknesses of the older corporations, so we will not solely discard that somebody may cross the moat and assault the EPR citadel.

Dividends From Enjoyable Actions Are Doubly Enjoyable

However you continue to want to make sure you can preserve paying them with out heading in direction of chapter 11 (which is decidedly not enjoyable in any respect).

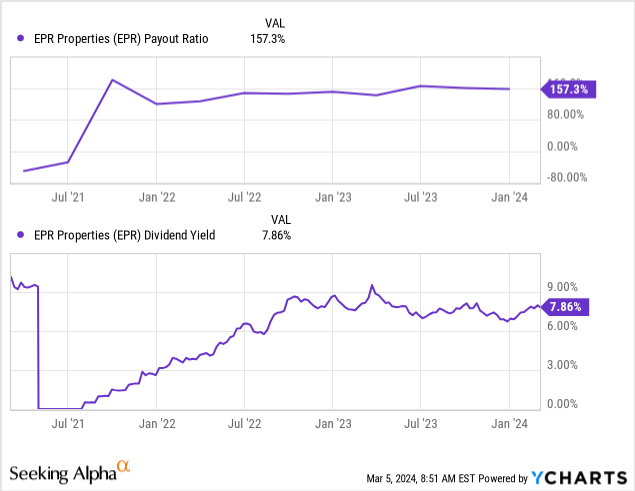

The payout ratio has been saved regular, whereas the dividend yield is in a transparent secular pattern; I contemplate this a great signal, as a steady payout ratio is each good for the wanted monetary planning the corporate has forward and reveals the precise effort in paying a better dividend yield has not elevated that a lot.

It is important to maintain payout ratios in thoughts, as they’re top-of-the-line metrics to measure the sustainability of dividends.

The opposite nice metric compares the FFO per share to the dividend per share, this can be a take a look at of the capability of the inventory to proceed paying the dividend with the cash generated by it.

EPR 10-Ok FY 2023

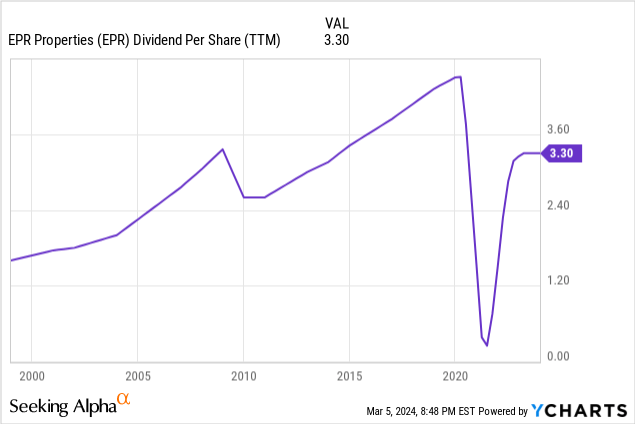

As we are able to see from their final 10-Ok, the FFO per widespread share and the FFOAA per widespread share, each diluted, are 5.15 and 5.18, respectively. To be conservative, we are able to use the bottom of them: 5.15

With a DPS of three.30 and an FFO per share of 5.15, the dividend is roofed, though the margin of only one.85 per share for future investments may use a bump up.

Total, EPR can preserve the dividends going, however I am curious if the wanted funding in progress won’t be left behind in 2024; I charge this as constructive however not too good.

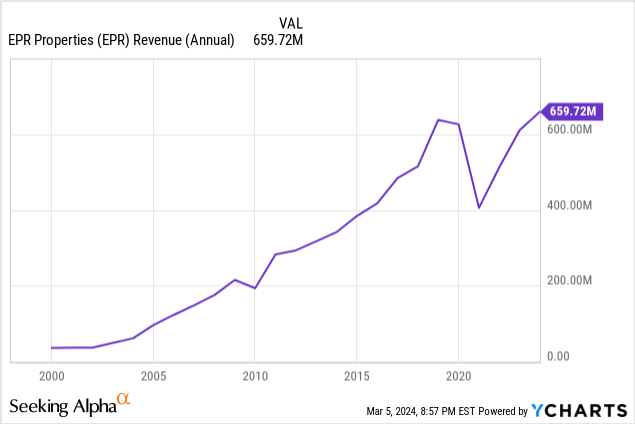

The Cash To Preserve The Amusement Park Music Going

Revenues had been hit exhausting by the worldwide pandemic, as anticipated from companies the place massive numbers of persons are gathered, with a secular pattern of 5 years damaged. Nonetheless, with a gradual restoration, 2023 closed with revenues above pre-pandemic ranges.

The rates of interest proper now are too excessive for the corporate to speculate closely and improve its capability to earn the corporate.

As REITs are capital intensive, they’re exceptionally wise to modifications in the price of capital, the company says on their last 10-K

Subsequent to 2021, REITS have typically skilled heightened dangers and volatility because of the influence of inflation, together with rising rates of interest. Because of this, detrimental stress in monetary and capital markets has elevated the price of capital. Till capital prices enhance, we count on that our ranges of funding spending shall be restricted within the near-term and that these investments shall be funded primarily from money available, extra money stream, disposition proceeds and borrowing availability beneath our unsecured revolving credit score facility, topic to sustaining our leverage ranges in step with previous observe. Because of this, we intend to proceed to be extra selective in our funding spending till such time as financial circumstances and our price of capital enhance.

However the firm additionally has a dividend payout of 167.80%, which means it pays far more dividends than its annual web earnings would enable. Whereas REITs are required to pay greater than 90% of their web earnings in dividends, they have to additionally strike a steadiness of getting sufficient Web Earnings left for investments. With rates of interest not being cut yet, we may doubtlessly enter a state of affairs the place EPR couldn’t make new investments within the foreseeable future.

That is the largest hurdle to investing in EPR proper now. With the mixture of slowed progress and the hazards of the present or rising rates of interest, we may have 2024 with none investments, inflicting a scarcity of compounding for years to come back. That is one thing apart from what traders need.

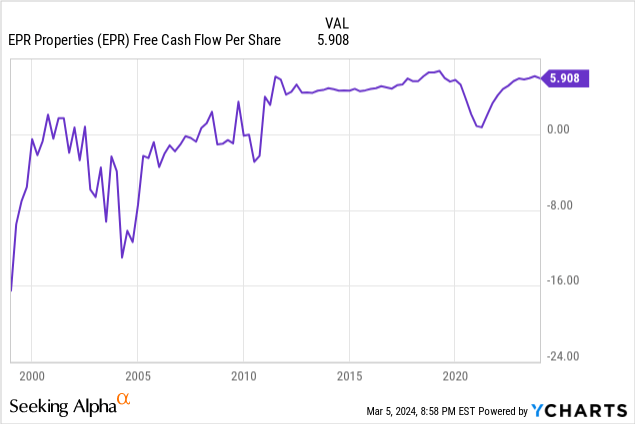

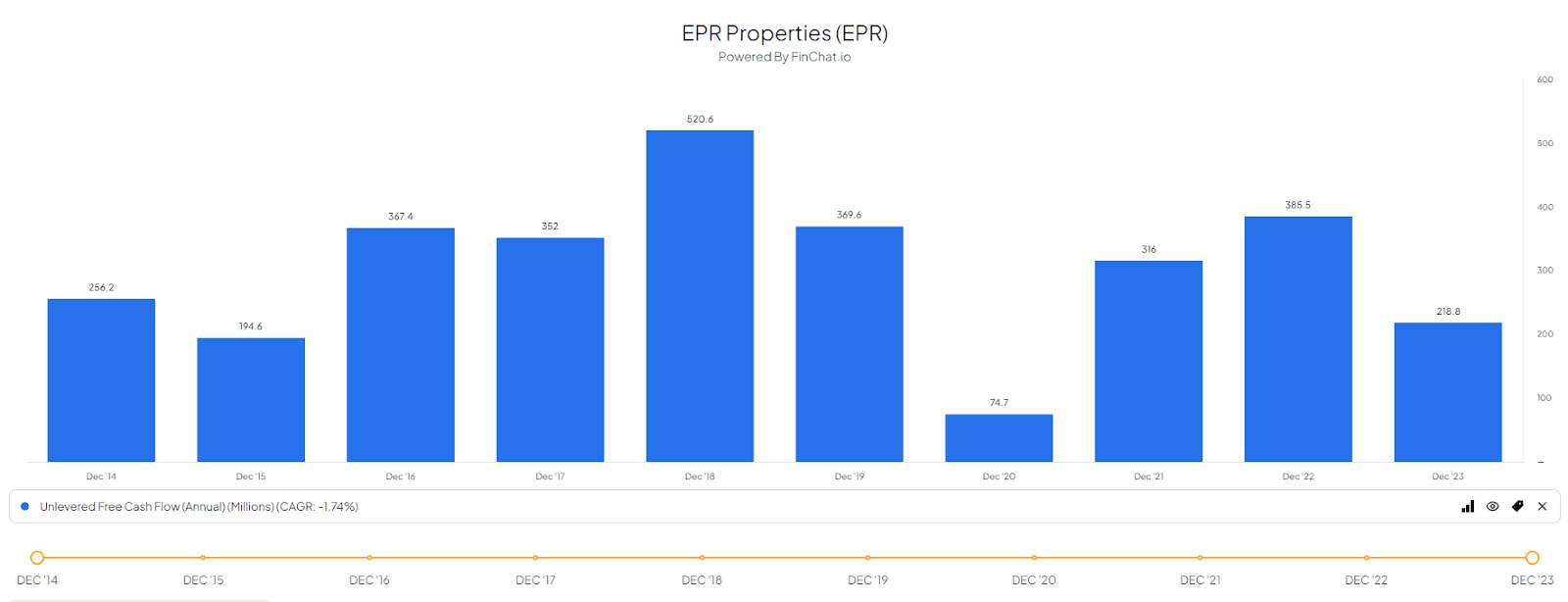

Chilly exhausting cash is the KING of issues a enterprise wants; as Charlie Munger as soon as mentioned, “EBITDA are Bullshit earnings“

Money remains to be king (Finchat.io)

And as soon as once more, restoration has been gradual; we’re nonetheless under 2019 in Unlevered Free Money Move, in large half due to the big dividend payout of +166.70%, a quantity comparatively excessive if we contemplate that the dividend yield is 7.90%, practically twice the trade’s charge of 4.64% however inflicting EPR to maintain burning treasured cash have to fund the enlargement that would put the corporate on the monitor to a full restoration of the COVID pandemic.

However Can You Actually Worth Enjoyable?

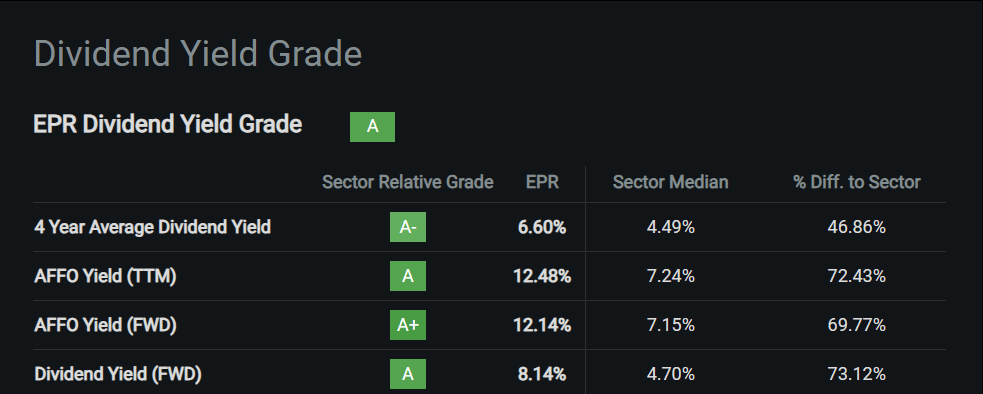

Sure, you possibly can; as of proper now, one of many greatest drivers of curiosity in EPR is the excessive dividend yield, with a 4-Yr Common Dividend Yield a hefty 46.86% above the sector and the Dividend Yield (FWD) a staggering 73.12% above different REITs, EPR has change into an enormous dividend choice in the event that they preserve the dividends rolling.

In search of Alpha Premium

I discover essentially the most logical approach is to worth this inventory utilizing the Dividend Low cost Mannequin for 2 major causes: The primary is, after all, the excessive dividend yield in comparison with its friends; the second is I imagine progress is likely to be impaired if rates of interest and inflation don’t go down. And though rising rates of interest, may need a constructive long-term impact for REITs both approach, EPR has a good distance forward both approach, with both having to attend for sufficient cash to roll in and for his or her funding or ready for the modifications in rates of interest that will assist additional develop.

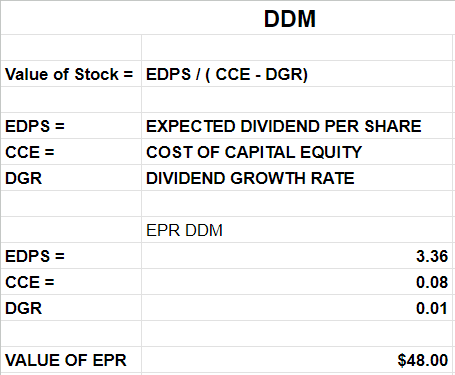

The system for the Dividend Low cost Mannequin I shall be utilizing is a straightforward DDM.

Google Sheets (Personal creator calculations)

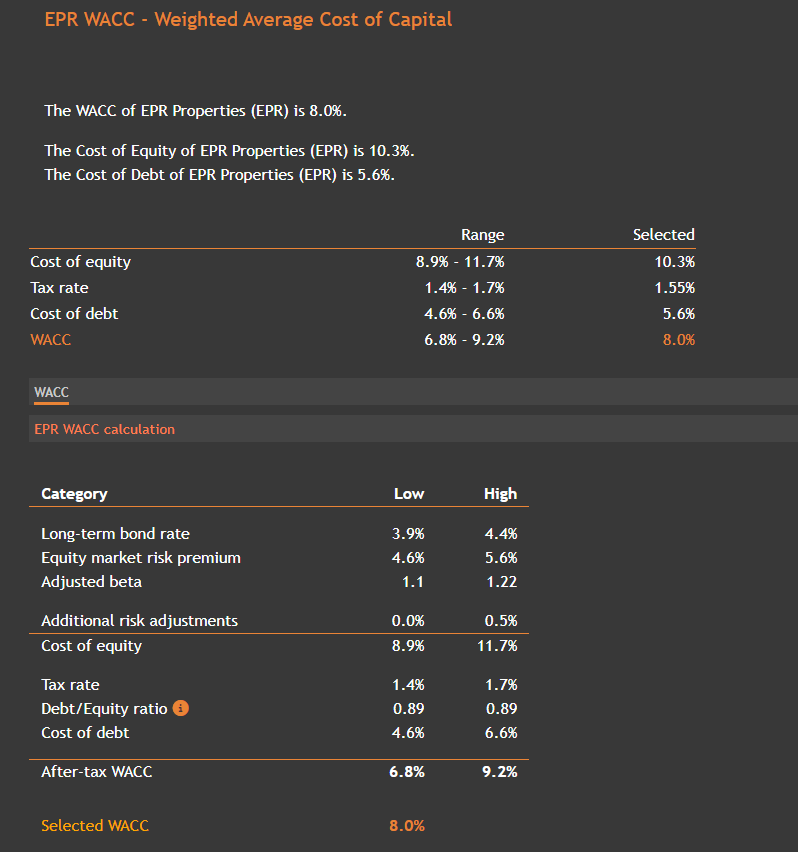

The price of capital fairness is a WACC from Valueinvesting.io.

Valueinvesting.io

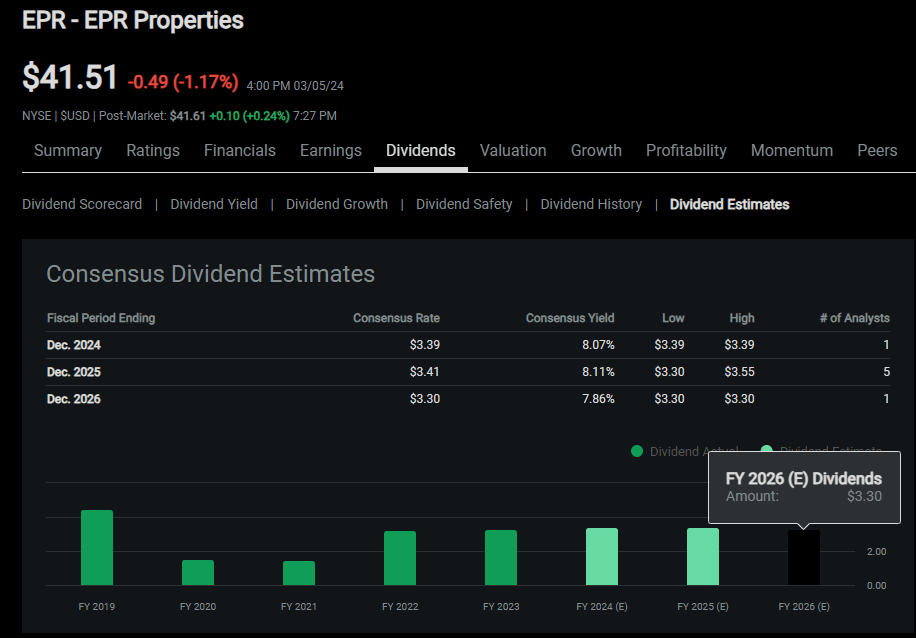

And the dividend estimates I obtained from In search of Alpha Premium.

In search of Alpha Premium

The 1% progress in dividend is a determine I imagine is one of the best conservative wager with the knowledge we’ve got proper now and the earlier issues for EPR to investing in its personal progress. Thus, my principal assumption is that EPR is aiming to change into established as a excessive dividend earnings inventory and never as a progress inventory, which means simply that, low progress in trade for a excessive earnings for traders.

Conclusion

Right here, we discovered the large query: is administration making an attempt to attend for decrease rates of interest and decrease inflation to start out engaged on the initiatives wanted to develop YoY? Then, if the reply is a powerful sure, one ought to look ahead to that couple with a value drop precipitated primarily by market hypothesis.

The corporate has its deserves; it has loads of well-diversified holdings and an thrilling and relatively modern worth proposition, however on the present value and with stagnation brought on by lack of assets, coupled with an unsure future, the enjoyable will not start till we are able to have a transparent sight of investments that may carry progress and more money.

Increasing into different areas turns into much more pressing, because the central holdings of EPR are in an trade with a secular decline, and nobody needs to be left with a dropping bag and no cash to pivot into greener pastures.

With a $48 honest worth vs the $41 it at the moment trades, there may be not sufficient margin of security to warrant an funding proper now. Too many variables may negatively hit the value in 2024, like inflation, rates of interest, and the persevering with decline of cinemas, which nonetheless account for a big a part of the revenues.

Personally, I’ll look ahead to a value drop, brought on by an exterior FUD, whereas monitoring the intrinsic worth and the margin of security.

My ultimate verdict is a cautious HOLD and protecting each eyes open.