Andrii Yalanskyi

Eaton Vance Threat-Managed Diversified Fairness Earnings Fund (NYSE:ETJ) is an fairness closed-end fund that invests in a diversified portfolio of widespread shares and hedges its publicity by:

- Shopping for out-of-the-money short-dated S&P 500 index put choices.

- Promoting out-of-the-money S&P 500 index name choices of the identical time period because the put choices.

- The choice roll dates are staggered throughout the choices portfolio

The Fund pays month-to-month distributions utilizing a managed distribution plan. The fund managers attempt to maximize after-tax complete return by looking for to attenuate and defer federal revenue taxes.

(Information beneath is sourced from the Eaton Vance web site until in any other case acknowledged.)

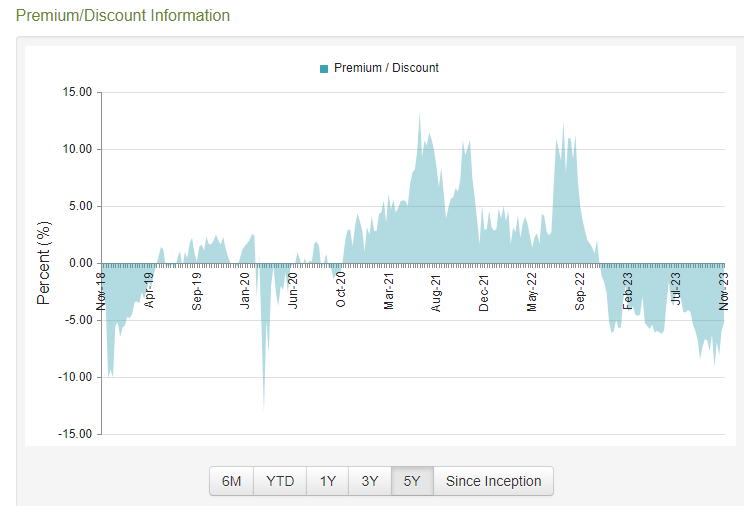

The fund is at the moment promoting at a 4.89% low cost to NAV, which is about common for the final 12 months.

Here’s a five-year historical past of the ETJ premium/low cost from CEFConnect:

ETJ Low cost Historical past (CEFConnect)

The Fund invests primarily in giant cap shares with a small allocation to mid caps. The highest holdings are extremely correlated with the S&P 500, which makes the S&P 500 choice hedging simpler. Listed here are the highest ten holdings as of October 31, 2023:

ETJ- High 10 holdings (ETJ Website)

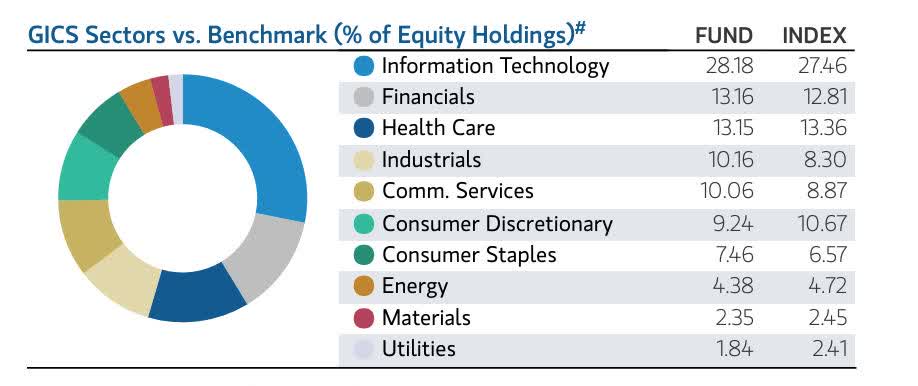

Sector Breakdown

ETJ Sector Breakdown (ETJ Website)

Supply: ETJ Reality Sheet, September 2023

Throughout the fairness lined name CEF sector, I choose funds that use index choices over those who use choices on particular person shares. Except for the tax benefit, the choices on inventory indexes typically commerce with a decrease bid-asked unfold and are way more liquid. This implies diminished “slippage” prices, leading to much less drag on efficiency. ETJ solely makes use of choices on the S&P 500 which might be extremely liquid.

Under is a abstract of the put and name choices utilized by the Fund. On common, the lengthy put choices are solely barely out of the cash. The decision choices written are typically about 5% out of the cash. Be aware that 96% of the portfolio is hedged, which implies that ETJ has diminished draw back danger. However in return for this, you hand over a number of the upside returns.

ETJ Choice Traits (ETJ Website)

Supply: ETJ Reality Sheet, September 2023

Let’s do a deep dive and check out a number of the choice hedge trades from the final semi-annual report. The Fund does choice buying and selling practically day by day, however I’ve chosen choices that expire on three days – July 5, 6 and seven.

The choice holdings within the S&P 500 Index contract had been:

|

Expiration Date |

# of contracts |

Train Worth |

|

|

07/05/23 |

105 |

$4,140 |

Lengthy Put |

|

07/05/23 |

105 |

$4,375 |

Quick Name |

|

07/06/23 |

105 |

$4,150 |

Lengthy Put |

|

07/06/23 |

105 |

$4,375 |

Quick Name |

|

07/07/23 |

104 |

$4,190 |

Lengthy Put |

|

07/07/23 |

104 |

$4,400 |

Quick Name |

Supply: ETJ Semi-Annual Shareholder Report

Be aware that the fund managers weren’t making an attempt to time the market. They execute balanced choice publicity trades every day with lengthy places barely out of the cash and quick calls about 5% out of the cash.

Distributions

As with many lined name funds, the fund makes use of a managed distribution plan the place they at the moment pay $0.0579 per 30 days. The month-to-month distribution has remained unchanged since October 2022, when it was diminished from $0.076.

Typically, a lot of the distributions are capital positive aspects or return of capital, which is intentional for the reason that fund tries to maximise after-tax complete return. For instance, this was the tax breakdown in 2022:

Capital Good points Distributions: $0.55

Return of Capital: $0.29

Certified Strange Div: $0.03

Complete Distributions= $0.87

Risk-Managed Diversified Equity Income Fund

Given the excessive annual distribution charge, you may count on the NAV of ETJ to steadily fall over time. However by re-investing the distributions (both again into ETJ or into different investments), you’ll be able to nonetheless get an honest after-tax complete return.

That stated, I believe ETJ generally is a good short-term swing buying and selling inventory to be owned once you wish to get extra defensive. I do not see it as a long run purchase and maintain fund that you just put away and overlook about.

Right here is the whole return NAV and value efficiency file of ETJ since 2013 in comparison with Morningstar’s Reasonable Threat class. Be aware how ETJ typically outperforms the S&P 500 in bear market years, however underperforms in bull market years due to its choice hedging actions.

|

ETJ NAV Efficiency |

ETJ Worth Efficiency |

Morningstar Reasonable Threat |

S&P 500 |

|

|

2013 |

+16.50% |

+19.54% |

+ 8.83% |

+32.21% |

|

2014 |

+3.67% |

+4.24% |

+ 4.30% |

+13.53% |

|

2015 |

+1.66% |

+5.90% |

– 1.03% |

+ 1.34% |

|

2016 |

-0.25% |

– 0.76% |

+ 6.66% |

+11.80% |

|

2017 |

+11.02% |

+18.92% |

+10.86% |

+21.69% |

|

2018 |

– 2.51% |

– 7.04% |

– 2.86% |

– 4.45% |

|

2019 |

+15.10% |

+26.89% |

+15.25% |

+31.29% |

|

2020 |

+18.73% |

+22.56% |

+11.86% |

+18.40% |

|

2021 |

+ 4.14% |

+ 4.25% |

+ 6.36% |

+28.59% |

|

2022 |

-14.89% |

-22.49% |

-13.85% |

-18.14% |

|

YTD |

+13.23% |

+15.19% |

+ 6.21% |

+20.68% |

Supply: Morningstar EV Risk-Mgd Divers Equity Inc ETJ

ETJ Fund Administration

1) Charles Gaffney, Managing Director, Portfolio Supervisor

Charlie is a managing director of Morgan Stanley and a portfolio supervisor on the Eaton Vance Core/Development crew. He’s accountable for purchase and promote selections, portfolio building and danger administration for a lot of Eaton Vance U.S. core fairness methods. He’s a member of the Eaton Vance Fairness Technique Committee. He’s additionally a vp and portfolio supervisor for Calvert Analysis and Administration. He joined Eaton Vance in 2003. Morgan Stanley acquired Eaton Vance in March 2021.

Charlie started his profession within the funding administration trade in 1996. Earlier than becoming a member of Eaton Vance, he was a sector portfolio supervisor with Brown Brothers Harriman and a senior fairness analyst with Morgan Stanley Dean Witter.

Charlie earned a B.A. from Bowdoin Faculty and an MBA from Fordham College.

2) Douglas R. Rogers, CFA, CMT, Govt Director, Portfolio Supervisor

Doug is an government director of Morgan Stanley and a portfolio supervisor on the Eaton Vance Core/Development crew. He’s accountable for purchase and promote selections, portfolio building and danger administration for Eaton Vance progress fairness methods. As well as, he covers the knowledge know-how and communication companies sectors. He joined Eaton Vance in 2001. Morgan Stanley acquired Eaton Vance in March 2021.

Doug served as a nuclear submarine officer in america Navy previous to starting his profession within the funding administration trade in 1999. Earlier than becoming a member of Eaton Vance, he was a analysis analyst with Endeca Applied sciences Inc.

Doug earned a B.S. from america Naval Academy and an MBA from Harvard Enterprise Faculty. He holds the Chartered Market Technician (CMT®) designation and is a CFA charterholder.

Supply: ETJ Net Website

Low cost Historical past

The low cost to NAV as of November 30 is -4.89%. The one-year low cost Z-score is +0.09 and the one-year common low cost is -5.04%, which implies that the present low cost to NAV roughly according to the common low cost over the past 12 months.

Supply: CEFConnect

Alpha is Generated by Low cost + Excessive Distributions

The excessive distribution charge of 8.72% together with the 4.89% low cost permits buyers to seize just a little little bit of alpha by recovering a portion of the low cost each time a month-to-month distribution is paid out.

Everytime you get well NAV from a fund promoting at a 4.89% low cost, the proportion return is 1.00/0.9511 or about 5.14%. So the alpha generated by the 8.72% distribution is computed as:

(0.0872)*(0.0514)=0.0045 or about 0.45% a 12 months in low cost seize alpha.

Be aware that this nearly half of the 1.12% baseline expense ratio.

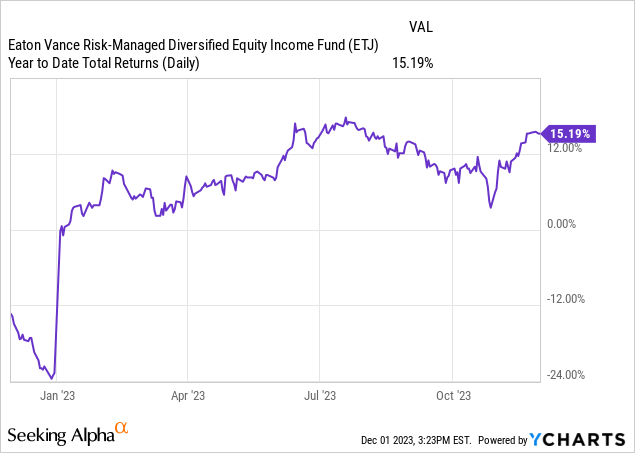

Here’s a chart exhibiting year-to-date return for ETJ. Be aware the reset firstly of 2023.

[object HTMLElement]

Ticker: ETJ Eaton Vance Threat Managed Diversified Fairness Fund pays month-to-month

- Complete Belongings= $564 Million

- Annual Distribution (Market) Charge= 8.72%

- Fund Expense ratio= 1.12%

- Low cost to NAV= -4.89%

- Portfolio Turnover charge= 55%

- Common Day by day Quantity= 158,000

- Common Greenback Quantity= $1.25 million

- Name Choices (written) as a % of complete property= 96%

- Put Choices (owned) as a % of complete property=96%

- No leverage used

Due to the current run-up within the inventory market, this can be time to think about including some ETJ in your portfolio as a partial hedge. It’s pretty liquid and simple to buy. Due to its tax administration coverage, it may be holding in both a taxable account or an IRA. I’d attempt to purchase ETJ at a reduction of seven% or greater, and would take into account trimming some shares if it trades at a premium once more, prefer it did in 2021 and 2022.

Full Disclosure: Lengthy ETJ.