Jonathan Kitchen/DigitalVision by way of Getty Photographs

Thesis

With the entrance finish of the yield curve larger prior to now 12 months, brief period devices have develop into interesting throughout asset courses. To that finish, it’s price revisiting the Eaton Vance Quick Length Diversified Earnings Fund (NYSE:EVG), a hard and fast earnings CEF lined greater than two years in the past. On the time of the initial article on the title, we highlighted for readers why the fund didn’t make sense on the time, having a really excessive, unsupported yield, with a excessive ROC (‘return of capital’) distribution.

Increased yields have translated into larger money flows for the EVG parts, and whereas different multi-asset funds have rocketed at premiums to NAV, this fastened earnings CEF remains to be buying and selling at a reduction, regardless of a considerable enchancment in its analytics and money flows. On this article, we’re going to re-visit the title and spotlight for traders why immediately’s surroundings is a smart one to take a protracted place on this CEF.

Low period collateral composition

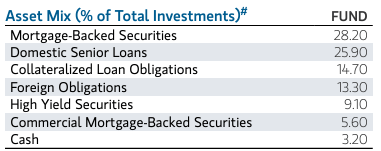

The fund has a really low 2.5 years period achieved by way of holding floating-rate leveraged loans and low period MBS bonds:

Asset Combine (Fund Reality Sheet)

Mortgage Backed Securities compose 28.2% of the portfolio, adopted by leveraged loans at 25.9% and CLOs at 14.7%. To notice EVG is a multi-asset fund by way of its composition, holding small sleeves of worldwide bonds, U.S. excessive yield, and CMBS securities.

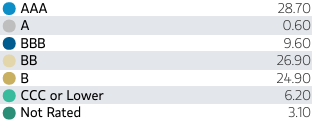

Nearly all of the MBS securities are AAA-rated, thus being primarily pushed by charges:

Rankings (Fund Reality Sheet)

The fund manages to steadiness out its credit-risky names which fall within the double-BB and single-B buckets with AAA MBS bonds. Given the excessive present Fed Funds and enchancment in yields on the entrance finish of the curve, the automobile runs little or no leverage presently, leverage which stands at solely 14%.

To notice that the market is implying three Fed cuts this 12 months, and we’ll lastly have a steadiness between decrease charges and better credit score spreads. We totally count on risk-off environments within the later half of the 12 months to be marked by decrease risk-free charges when credit score spreads transfer larger, which can see the fund steadiness out by way of its composition.

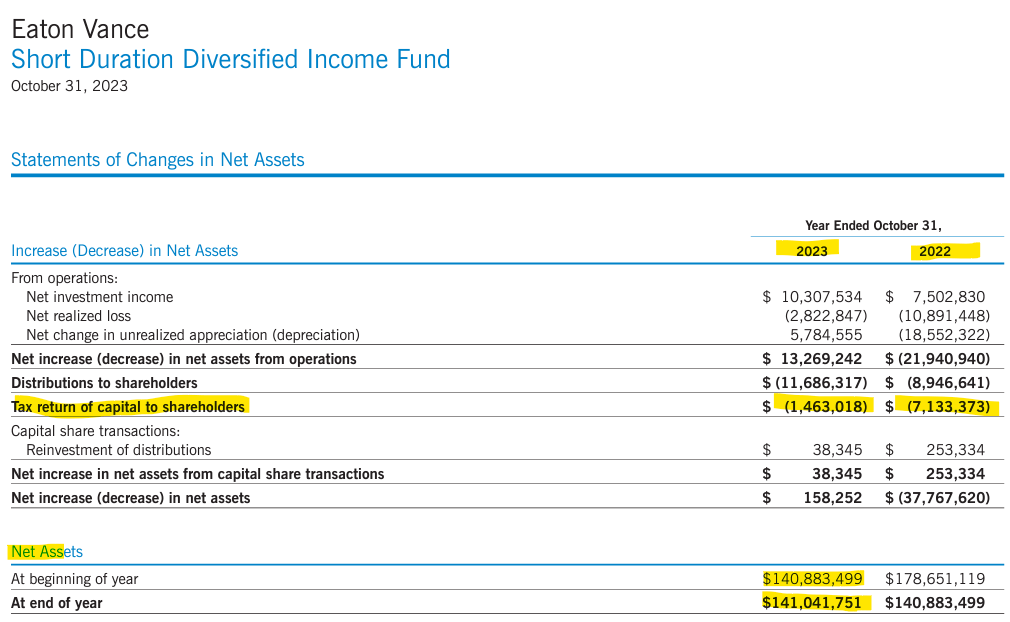

Overdistribution was a problem prior to now

In a low charges surroundings this fund was overdistributing, however issues have improved tremendously:

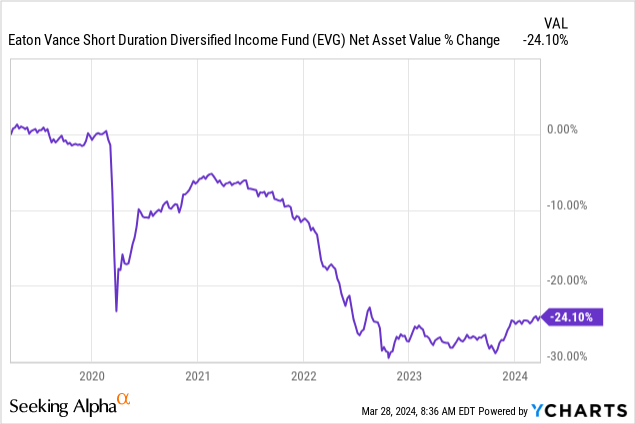

As exemplified by its NAV efficiency, the fund has lastly discovered its footing prior to now 12 months. From a pure money circulate perspective, this is sensible since leveraged loans yield 8% to 9%, whereas MBS bonds with 14% leverage ought to present for cash-flows in extra of, 6%.

Whereas the fund doesn’t present for a Part 19a discover publicly, we will have a look at its Annual Report to get the identical info:

ROC (Annual Report)

We are able to see the CEF having decreased by 6x its ROC utilization in 2023 versus the prior 12 months, with the respective line transferring from $7.1 mm to $1.4 mm. Extra importantly, the low ROC utilization plus the right asset administration of the fund resulted in an accreting NAV for 2023. If we have a look at Web Belongings firstly and finish of 2023 we will see they’re virtually the identical (with a slight constructive accretion truly). That is the signal of a wholesome CEF that distributes the money it makes however retains a gradual NAV.

These are precisely the kinds of metrics you need to see as an investor. You need a steady NAV and a excessive yield with a low volatility metric.

No higher time for EVG

Traditionally there is no such thing as a higher time to purchase EVG. The fund is lastly distributing what it’s making because of the excessive rate of interest surroundings, and by way of its composition, it is going to blunt a number of the impression of decrease Fed Funds later within the 12 months. The CEF was affected by overdistribution prior to now however has moved to a steady NAV. We count on this state of affairs to persist for the subsequent two years till Fed Funds transfer under 3% once more.

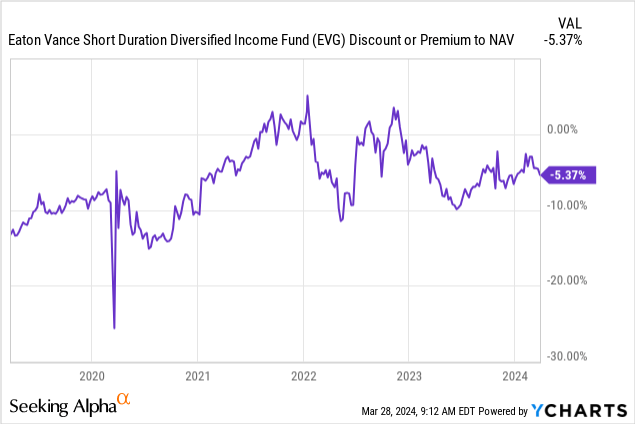

Whereas the market has bid up different CEFs, EVG remains to be buying and selling at a excessive low cost because of its historic overdistribution:

We count on the title to maneuver flat to NAV within the subsequent twelve months, thus count on an extra +5% return from the low cost narrowing. Shopping for this title on the present ranges and utilizing the Drip characteristic for CEFs can also be a sensible option to benefit from the present fund analytics.

The above graph exhibits us how the fund traditionally traded at roughly -10% low cost to NAV, with intervals of premiums pushed by intrinsic market technicals.

In immediately’s overbid market with stretched excessive yield, a retail investor must deal with relative worth and the names that are nonetheless ‘low cost’. EVG falls in that class and traditionally has delivered within the 12 months after Fed charge cuts, with a +16% whole return in 2019 after the Fed minimize charges.

Its low leverage can also be an asset within the present surroundings, with many different names being dragged again by the excessive value of funds for his or her floating charge leverage.

Danger components

The principle danger issue for this fund is a sudden and violent collapse in Fed Funds. If the economic system goes south and the Fed cuts by 250 bps or extra this 12 months, the CEF will begin seeing strain on its money flows in the direction of the tip of the 12 months, with 2025 being probably one other 12 months of ROC utilization. A clean path of charge cuts in 2024/2025, in keeping with the Fed ‘dot-plot’ and our base case state of affairs wouldn’t represent a sudden lack of yield for the CEF.

The CEF’s low period of solely 2.5 years insulates it from extra charge hikes, though we don’t assume there’s any potential for such a transfer in a presidential election 12 months.

Conclusion

EVG is a hard and fast earnings CEF. The fund has a low period of solely 2.5 years and a big AAA MBS bucket. The title used to overdistribute in a low rate of interest surroundings, however is now using little or no ROC to maintain its 9% yield. The fund had a steady NAV in 2023 and can profit from the Fed reducing charges as per the bottom case, because it did in 2019. In contrast to a few of its friends, the fund remains to be buying and selling with a -5% low cost to internet asset worth, which makes it an interesting selection in an in any other case stretched market.