SOPA Photos/LightRocket through Getty Photos![]()

Introduction and Background

As a high-quality-seeking dividend progress investor, the pickings just lately have been fairly slim. The market has been on a job, which from a net-worth perspective, makes me really feel good, however as an lively investor trying to put cash to work in compounding dividend progress, there have been fewer alternatives. For this reason I commonly monitor an inventory of round 100 of the highest-quality dividend progress shares, in order that as valuations come into honest vary, I can take benefit. I don’t at all times time purchases completely, however over the long run, I’ve been very proud of the outcomes. After greater than 20 years of investing ups and downs, the one factor I do know is that you just actually can’t go mistaken with high quality.

If you happen to’ve been following alongside, you already know that one in all my favourite methods to search for worth on this high-quality dividend progress area is to display for these shares buying and selling close to 52-week lows. I made a decision to filter my watchlist by corporations which are buying and selling at lower than 30% of their 52-week vary (52-week low being 0% and 52-week excessive being 100%).

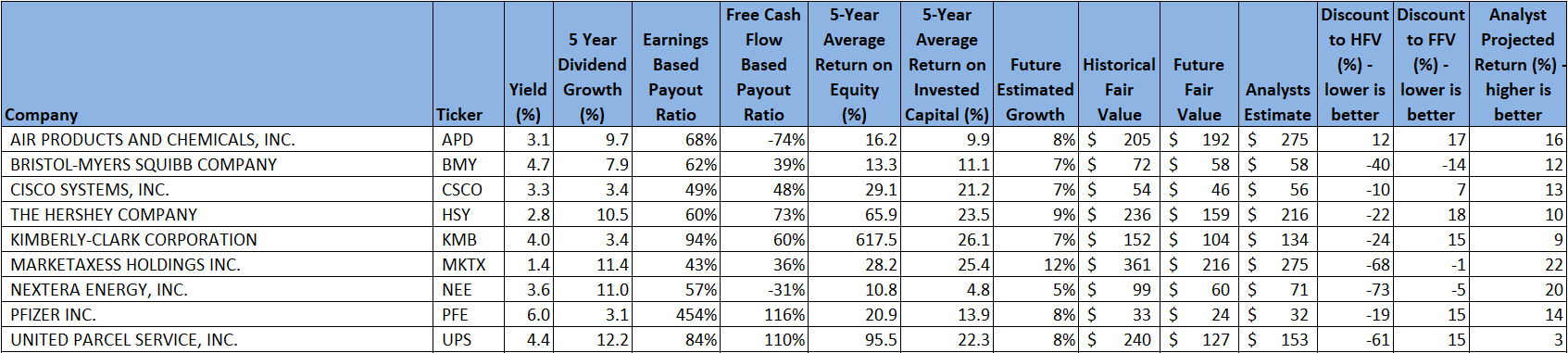

Utilizing this primary move standards, we will likely be wanting on the following checklist of corporations:

Finbox, Looking for Alpha, Writer’s Evaluation

Truthful Worth Estimation

As I’ve described in earlier articles, I wish to calculate a good worth in two methods, utilizing a Historic honest worth estimation, and a Future honest worth estimation. The Historic Truthful Worth is solely primarily based on historic valuations. I evaluate 5-year common: dividend yield, P/E ratio, Schiller P/E ratio, P/Ebook, and P/FCF to the present values and calculate a composite worth primarily based on the historic averages. This provides an estimate of the worth assuming the inventory continues to carry out because it has traditionally. I additionally need to perceive how the inventory is more likely to carry out sooner or later, so make the most of the Finbox honest worth calculated from their modeling, a Cap10 valuation mannequin, FCF Payback Time valuation mannequin, and 10-year earnings price of return valuation mannequin to find out a composite Future Truthful Worth estimate.

I additionally collect a composite goal worth from a number of analysts, together with Reuters, Morningstar, Worth Line, Finbox, Morgan Stanley, and Argus. I wish to see how the present worth compares to analyst estimates as one other knowledge level, and as a sanity verify to my very own estimates.

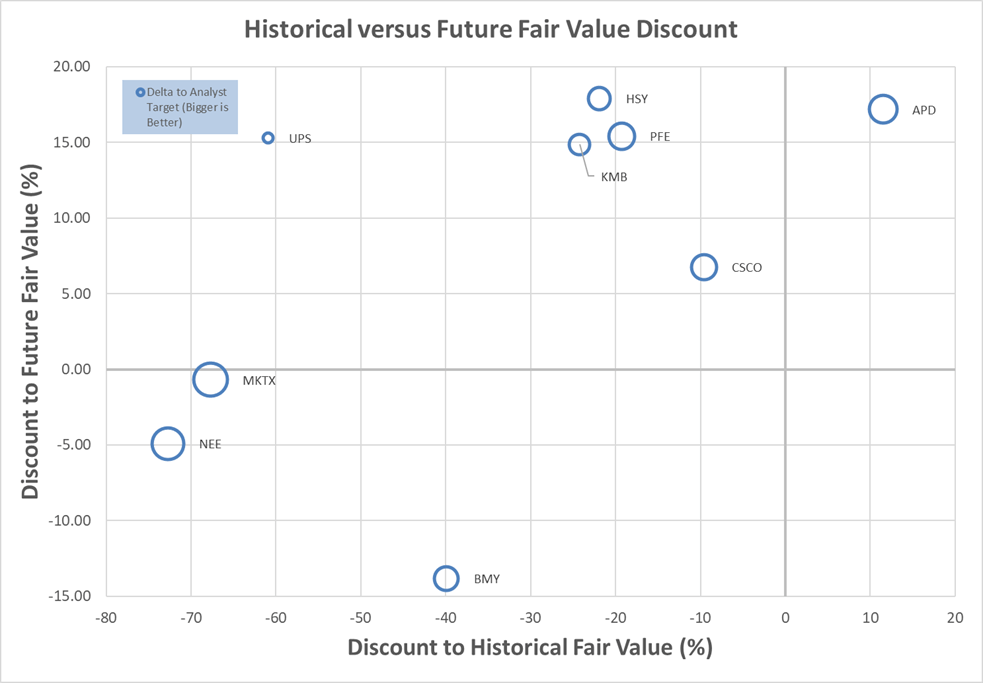

Plotting three variables on one plot is difficult, however utilizing a bubble plot permits us to visualise three variables by plotting the Historic honest worth versus the Future Truthful Worth on a normal x-y chart, after which use bubbles to characterize the scale of low cost relative to analyst estimates.

Writer calculation of Historic and Future Truthful Worth, analyst estimates

This chart is insightful when you perceive how you can interpret it. What we’re in search of are shares which are buying and selling at a reduction to each the Historic Truthful Worth and the Future Truthful Worth. So, these shares which are farther to the left, and farther to the underside, are probably the shares buying and selling on the largest low cost to honest worth. This could be the underside left quadrant of the graph. Moreover, these shares with the largest bubbles are the shares which are buying and selling on the largest low cost to analyst estimates, so in idea, shares within the decrease left quadrant that even have giant bubbles, must be respectable candidates for funding.

The chart means that MarketAxess (NASDAQ:MKTX), NextEra Power (NEE), and Bristol Myers Squibb (BMY) are all buying and selling at reductions to their Historic and Future Truthful Values, in addition to favorably in comparison with analyst estimates.

I personal the entire shares within the checklist / chart aside from Kimberly-Clark (KMB). I’ve just lately initiated a place in Air Merchandise and Chemical substances (APD) at $226 and added to my positions in MarketAxess at $217 and in NextEra Power at $56. I have already got a full place in Bristol-Myers, however nonetheless consider it to have good potential as a long-term funding. If there’s a theme to my investing, exterior of high-quality dividend progress, it’s the out-of-favor, beat down, however high-quality shares that I consider have unappreciated potential. That works extra occasions than it doesn’t.

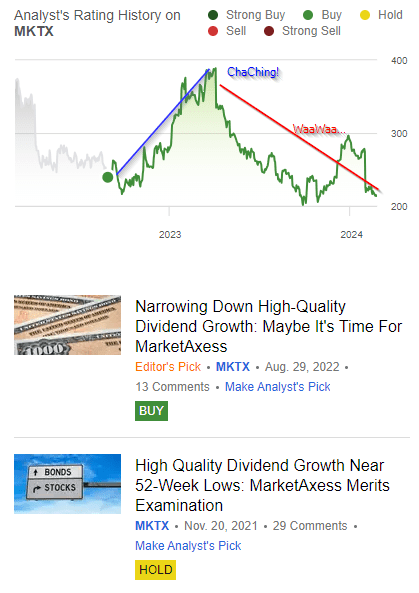

MarketAxess and I are nonetheless figuring one another out. I’ve written a pair articles prior to now about it and am nonetheless excited for the long run prospects, however up to now, the outcomes haven’t been good. I need to take one other look, because it has been some time, to see the rationale for my current buy.

MarketAxess Evaluation

Since I’m not attempting to promote something on Looking for Alpha (belief me, I don’t do it for the cash) however extra to encourage me to dig deeper and be a greater investor, I wish to be as clear as doable. I wrote my first article on MKTX on the finish of 2021. Total, I rated it as an fascinating maintain at that time, but in addition famous that I used to be in search of a goal worth round $330. I in the end initiated a place a number of months later at $307. I wrote one other article in August of 2022 the place I up to date my score to Purchase. I’ve bought MKTX a number of occasions since that preliminary buy at $307 – $244, $246, $225, and $217. I’ve a protracted, time horizon, and I like greenback value averaging when valuations look honest.

Even averaging down, I’m underwater on this funding. If I used to be a dealer, my preliminary “hold” score in 2021 ought to have been a “sell”. It’s also fascinating to see that had I offered earlier than mid-2023, I’d have had a very nice capital acquire. Possibly I must be a dealer…

Looking for Alpha

Since I’m not a dealer, let’s begin with the fundamentals. MKTX has a 5-year common Return on Fairness of 28.2%. Nonetheless, its most up-to-date ROE is 21.7%. The 5-year common Return on Invested Capital is 25.2% however its most up-to-date ROIC is nineteen.4%. In each instances, I like that ROE is so near ROIC, since this implies administration isn’t enjoying video games with debt to extend the ROE, nevertheless, regardless that the numbers are nonetheless superb, there’s some deterioration towards the typical that may be a minor warning flag. A fast take a look at ROIC versus the Weighted Common Value of Capital (round 10%) reveals wholesome margin, which must be progress indicator. With the preliminary yield being low, we’d like progress to be sturdy to assist sturdy future dividend progress.

The earnings-based dividend payout ratio of 43% and free-cash-flow-based dividend payout ratio of 36% are each wonderful. They’ve paid a rising dividend for over 14 years now. The newest increase of two.8% is disappointing towards the backdrop of the low preliminary yield. Morningstar charges MKTX as large moat, with exemplary capital administration, and presently has a 4-star valuation score.

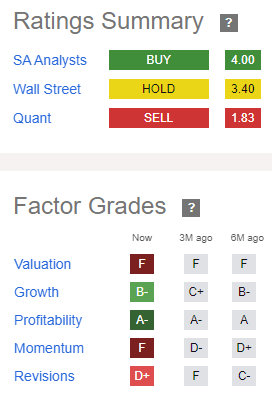

Looking for Alpha makes out there a abstract of rankings, in addition to issue grades. These make for one more good, first move filter for funding timing.

Looking for Alpha

Beginning with the highest stop-light chart – you possibly can take your decide between Purchase, Maintain, and Promote. My solely argument right here is that Quant and Wall Road are typically short-term centered, and I wish to assume the analysts on Looking for Alpha are extra refined, and due to this fact longer-term centered – apologies to these merchants on the market, I’m a really long-term investor, therefore in fact I’m refined (chuckle).

The Issue Grades are relative, and due to this fact very depending on the peer comparisons. MKTX doesn’t have loads of direct competitors, so these relative comparisons have to be taken in context. Two issues which are necessary to the funding thesis in MKTX are progress and profitability although, and it scores effectively right here. These are necessary to the sustainability and excessive progress expectations we now have for the dividend. In any other case, the momentum and revisions recommend it is perhaps out of favor, which conveniently, falls proper into my wheelhouse.

MarketAxess Technique

I need to be actually easy about how I take into consideration MKTX.

- Disruption of the normal phone-based, guide system for bond buying and selling by means of automation and market creation.

- Market creation creates extra alternatives for buying and selling and hedging by means of improved liquidity and lowered transaction prices.

- Huge and rising alternative – market share is necessary and the difficulty with MarketAxess has been shedding market share, however the market is giant, and the chance is rising.

- Decrease rates of interest could assist buying and selling volumes, however since MKTX is fee pushed, absolutely the rate of interest could also be much less necessary than the motion in charges, and the period of the bond.

- Strategic acquisitions have been necessary to the outcomes and have carried out effectively – that is an space to observe, since valuation / Good Will, and integration dangers are larger with a method that features acquisition.

On the one hand, income continues to extend properly, amidst elevated adoption and volumes. Then again, market share has been coming down amidst sturdy competitors from key opponents which are additionally rising, like Tradeweb and Trumid. That is the basic supply of investor frustration with the inventory – is the expansion story intact, and can MKTX proceed to develop even within the face of sturdy competitors?

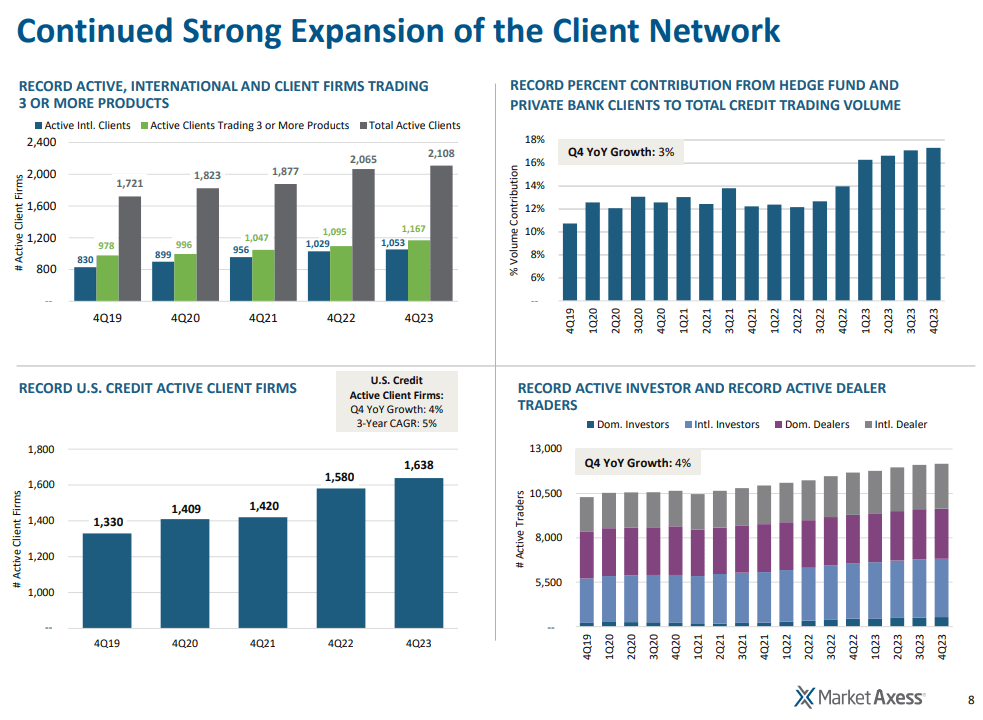

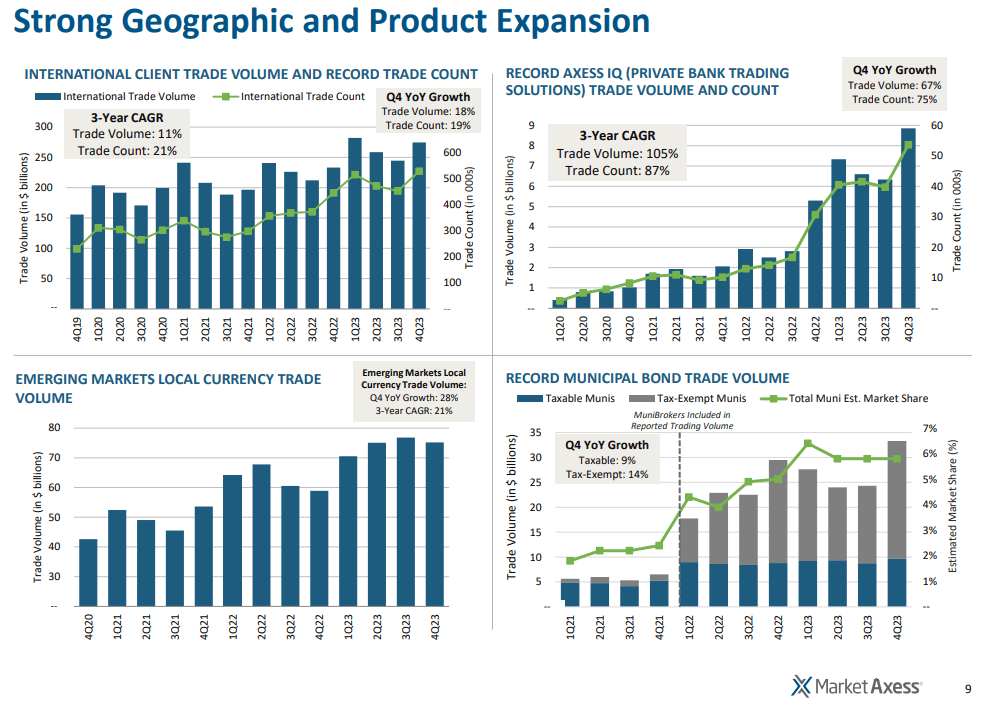

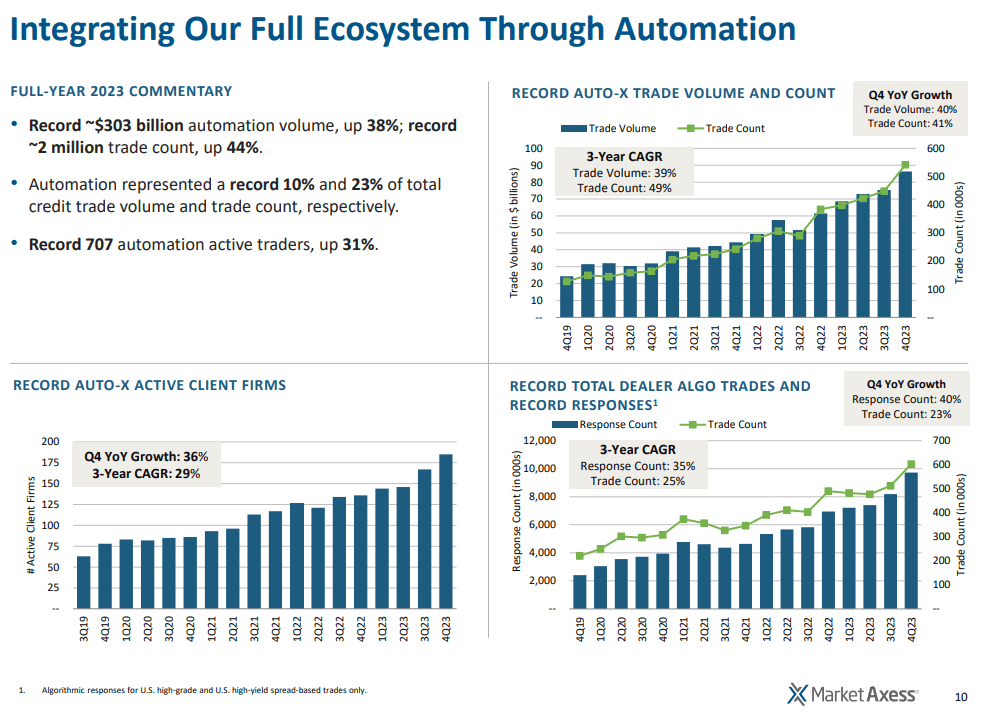

Just some graphs of outcomes from the current MarketAxess FY 2024 Earnings Results present that there’s a lot to be enthusiastic about.

MarketAxess Full 12 months 2023 Outcomes Presentation MarketAxess Full 12 months 2023 Outcomes Presentation MarketAxess Full 12 months 2023 Outcomes Presentation

MarketAxess Historic Evaluation

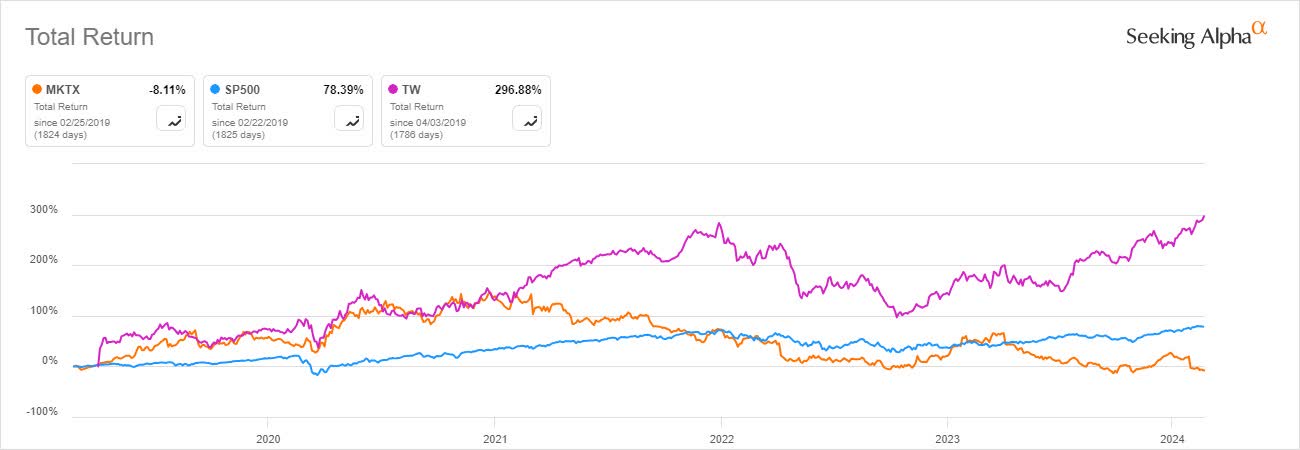

Earlier than we dig deeper into the expansion, I do wish to look the place issues have been prior to now. I feel we notice that previous efficiency could be considerably indicative of the standard of the corporate. Clearly, it’s necessary to know the important thing drivers for that previous efficiency, to see if you happen to consider something has modified that would affect that. So, let’s begin with how MKTX has carried out for shareholders prior to now:

Looking for Alpha

First, MKTX has drastically outperformed the S&P 500 prior to now, together with a short interval final yr. Lately, nevertheless, MKTX has given up all of its out-performance and is now under-performing. Of curiosity, Tradeweb is without doubt one of the key opponents we talked about above. It has considerably outperformed the market in addition to MKTX. I can’t assist however discover that a few of MKTX’s under-performance appears correlated to a few of Tradeweb’s outperformance, and this is without doubt one of the key foundations for the bear case – Tradeweb is taking loads of that new and addressable market that MKTX is meant to be getting. MKTX isn’t rising as a lot as a result of Tradeweb is taking market share. Taking the counterpoint, if the entire addressable market is rising, MarketAxess has been capable of proceed to develop, even with a complete market share decline, and Tradeweb is performing very effectively, may MarketAxess be undervalued relative to the efficiency potential of the entire addressable market?

Let’s now see if valuations have improved relative to historical past with the decline in worth, or if we’re seeing total degradation. Let’s reference P/E and yield for this.

Finbox Finbox

Possibly a optimistic word is forming with this view – the P/E continues to be comparatively excessive, however in comparison with its historic valuation, is at a low in comparison with the 5-year common of 55.8. This means that the enterprise has not degraded to the extent that the value has. Moreover, the yield can be at a 5-year excessive in comparison with the 5-year common of 0.8%. From this historical-based view, MKTX could also be attractively valued.

MKTX continues to do a pleasant job of sustaining shares excellent, not letting shareholders get diluted. Nonetheless, it doesn’t seem like share buy-backs must be counted on so as to add to future earnings per share progress. This might nonetheless recommend that they consider they’ve higher methods to develop earnings for shareholders by means of strategic funding than simply counting on share buybacks or may recommend they’re preserving capital attributable to issues about progress.

Finbox

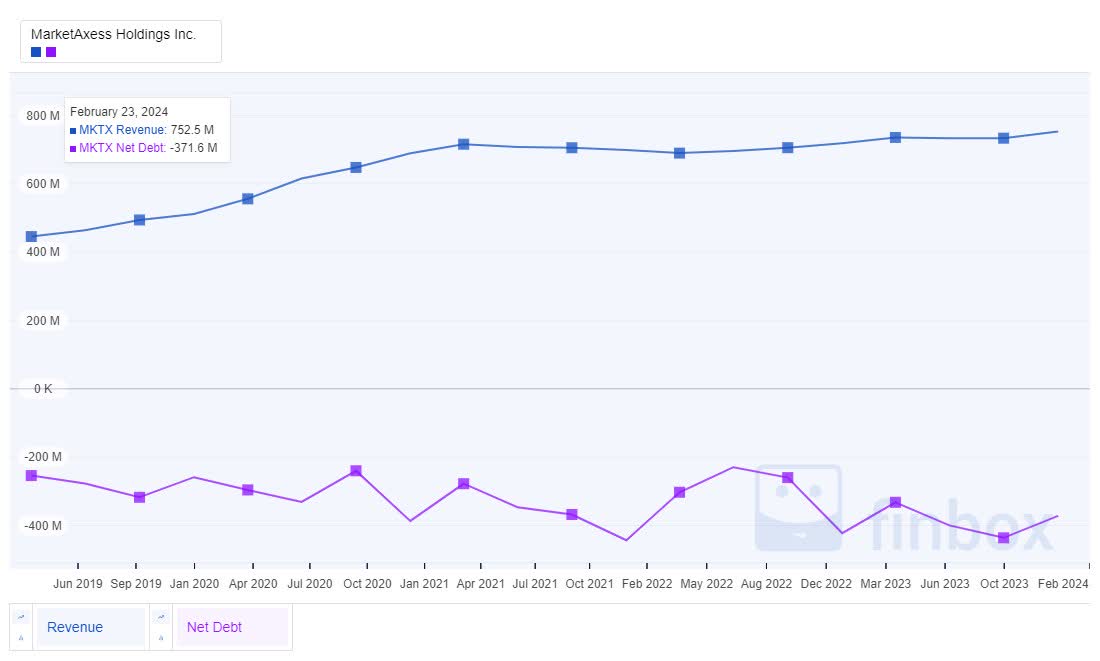

I nonetheless actually love the income versus web debt story. MKTX is debt free and has a powerful web money place. This isn’t quite common in immediately’s day and age, and one thing I like seeing as a long-term investor relying on that compounding dividend progress far into the long run. Even with the historic acquisitions which have added to enterprise outcomes, sustaining this debt free standing is spectacular.

Finbox

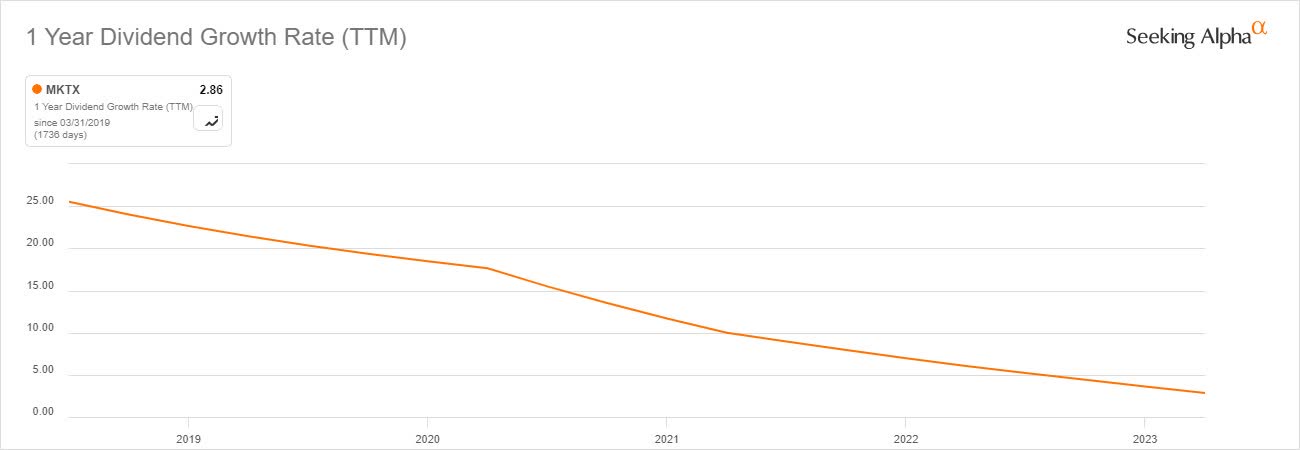

MKTX has paid a rising dividend for over 14 years and has traditionally demonstrated very sturdy dividend progress. The expansion is tapering considerably just lately, with the newest increase being beneath 3%. I take a look at this as an oblique indicator of administration’s confidence in future progress, so after I see dividend progress pulling again, it may point out administration shouldn’t be satisfied of their progress prospects. Likewise, it may additionally point out that they produce other plans in thoughts, resembling strategic M&A or inside R&D, or it may simply point out that the excessive price of progress within the early years was to get the dividend to a goal stage, and now that concentrate on stage has been achieved, the expansion will likely be extra throttled by fundamentals (nonetheless tied to progress).

Looking for Alpha

The earnings and free money flow-based payout ratios are wholesome and comparatively steady. Primarily based on free-cash-flow, which is how dividends are paid, it seems to be like the next stage of progress might be sustained. This leads us again to our above query wanting on the progress – does administration lack confidence, or is that this an indication of conserving money for different strategic investments?

Finbox

MarketAxess Future Evaluation

Transferring on to our future wanting evaluation, it looks like the story hasn’t modified rather a lot since we final checked out MKTX. The query nonetheless boils all the way down to that future progress. Let’s check out a few of the future indicators to see if something important has modified in that story.

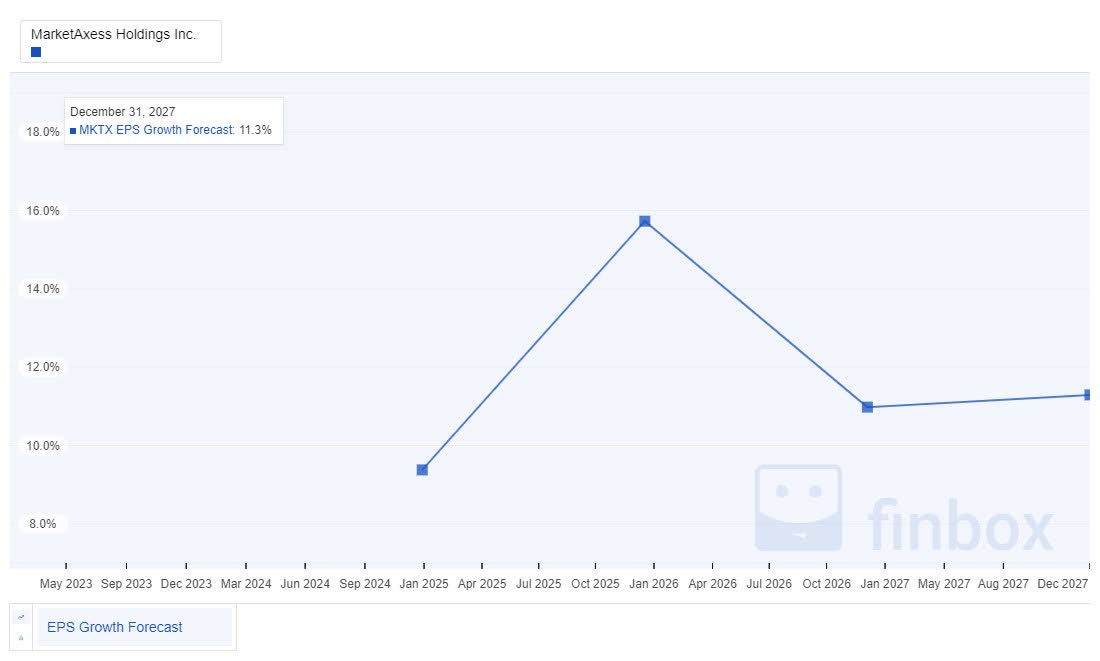

Let’s begin with projected earnings progress. Frankly, I like what I see. Removed from being a no-growth / low-growth story, not less than from an EPS perspective, the expansion projections are strong.

Finbox

The longer term progress projections align effectively with the previous estimates for long-term progress. Typically, with corporations which are out of favor, there’s a massive discontinuity between the anticipated future progress and previous estimates for long-term progress. That doesn’t look like the case right here.

Finbox

My very own estimate for MKTX’s ahead progress is round 12%. I derive this from a mix of varied progress projections and progress fashions. I personally really feel like a mean, low double-digit progress expectation is affordable for MKTX, and count on the expansion to proceed on a reasonably steady trajectory, as we’ve seen with the historic progress outcomes. These ranges of sustainable progress do good issues for compounding over time.

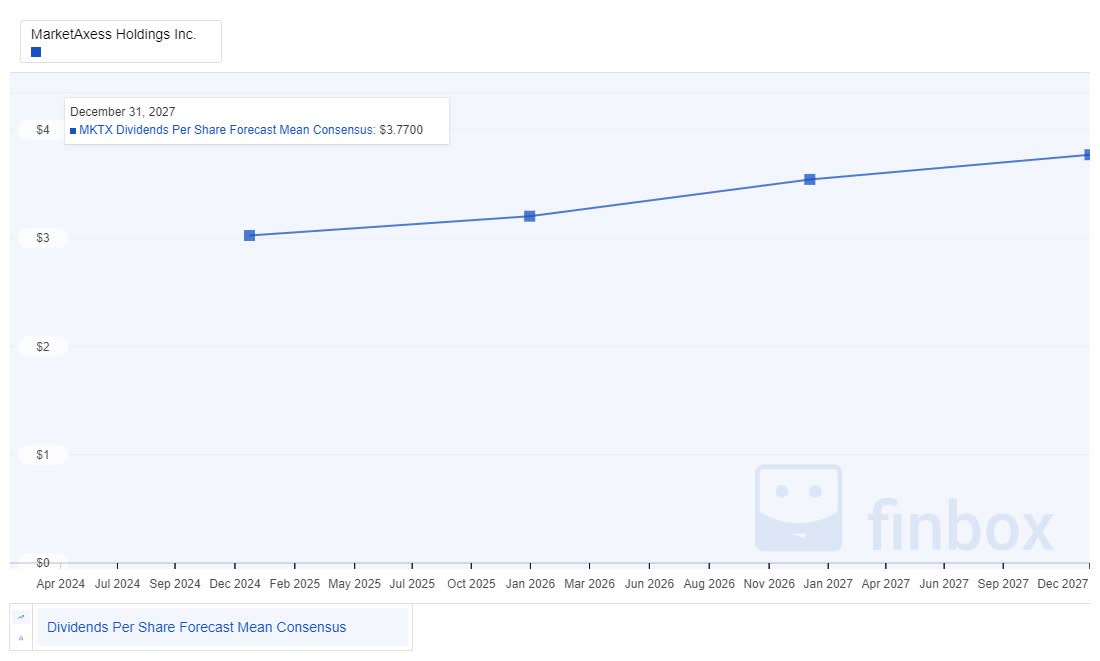

For a dividend progress investor, understanding future dividend progress potential can be necessary, particularly in as a lot as it’s sustainable. Listed here are the long-term dividend progress projections for MKTX. The forecast progress seems to be constant. I do surprise if the current deceleration in dividend progress is short-term, or extra of the brand new customary. I don’t like 3% dividend progress from such a low yielder. My hope is that short-term sacrifices in dividend progress will enable for strategic funding, which MKTX has confirmed to be adept at, permitting longer-term progress sooner or later. As a extra growth-oriented inventory basically, that progress ought to probably additionally end in engaging capital appreciation.

Finbox

The longer term projections for payout ratio present the chance to develop the dividend in-line with different progress projections, with out rising danger. Even when the low progress of late calls into query future progress, it seems the capability will likely be there.

Finbox

Since EPS shouldn’t be a full indicator of progress, the opposite factor to tie out is income. Income is predicted to proceed on a wholesome progress projection, in a steady manner.

Finbox

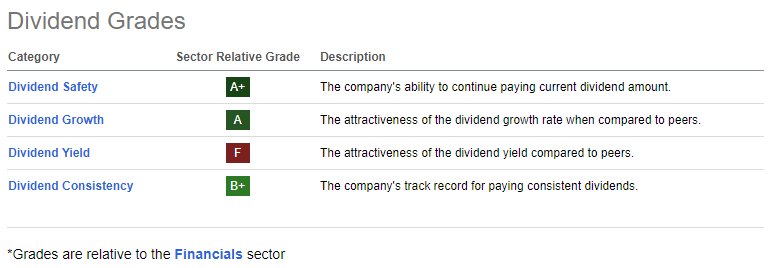

The Looking for Alpha Dividend Grades present the potential on this funding, with sturdy relative scores for security, progress, and consistency – all issues we wish to see. We all know the yield is low, and relative to the monetary sector, this low grade isn’t a shock.

Looking for Alpha

Threat

Let’s finish our journey with a short dialogue on danger. On the finish of the day, the story with MKTX is a progress story. If the chance for progress is lower than anticipated, or if MKTX is unsuccessful in capturing its share of the expansion, which I consider is the largest concern the market has, then the inventory is probably going overvalued.

From a monetary and high quality perspective, there doesn’t look like a lot danger right here. Resulting from its debt-free standing, MKTX doesn’t even have credit score rankings from the most important businesses, nevertheless, the Worth Line Monetary Energy score is A. As we mentioned beforehand, Morningstar charges it as Huge Moat with Exemplary Capital Administration. The Altman-Z rating is presently a really wholesome 11.39. The largest danger is probably going valuation, and as we’ve mentioned, the valuation seems to be engaging presently.

Abstract

MKTX and I’ve had a coloured historical past. Had I offered shares at sure factors, I’d probably be a lot wealthier, not less than on paper, nevertheless, I do consider within the high quality of this firm, like the expansion historical past and prospects, and assume the addressable market they serve is engaging. To an extent, it is a picks and shovels sort of firm for the bond market, and they’re doing one thing that, although not completely with out competitors, is disruptive. The strategic work they’re doing to create a extra liquid market, which itself generates stickiness, in addition to driving buyer worth by means of the liquidity, and decrease prices, appears to me like a fairly sound technique. They’ve additionally proven skill to execute strategic acquisitions in an accretive manner, whereas nonetheless sustaining a really strong steadiness sheet.

I don’t know what is going to occur brief time period, however I’m a strong-buy for the long-term investor, even given my storied historical past with this inventory. I feel the inventory is attractively valued on the present worth, and as I famous earlier, just lately put my cash the place my mouth is and added to my place at $217.

The preliminary evaluation for this text additionally recognized different good candidates for additional consideration. NextEra and Bristol Myers Squibb look to be attractively valued primarily based on Historic and Future valuations, and have respectable upside to analyst estimates.