peshkov

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Tax-Managed World Diversified Fairness Earnings Fund (NYSE:EXG) invests in a reasonably diversified portfolio, together with offering world publicity. The fund is sort of much like its sister fund, Eaton Vance Tax-Managed World Purchase-Write Alternatives Fund (ETW). If the title alone does not let you know what the distinction between these closed-end funds, or CEFs, is, you then’re most likely not alone.

Each funds incorporate world publicity, however the benchmark for EXG is, extra particularly, the MSCI World Index. For ETW, they incorporate each the S&P 500 and MSCI Europe Indexes as its benchmark. Each of those funds then additionally incorporate a call-writing overlay technique, writing towards indexes. That is additionally the place they barely diverge by way of their method. ETW overwrites as much as almost 100% of its worth, and EXG is at round 50%.

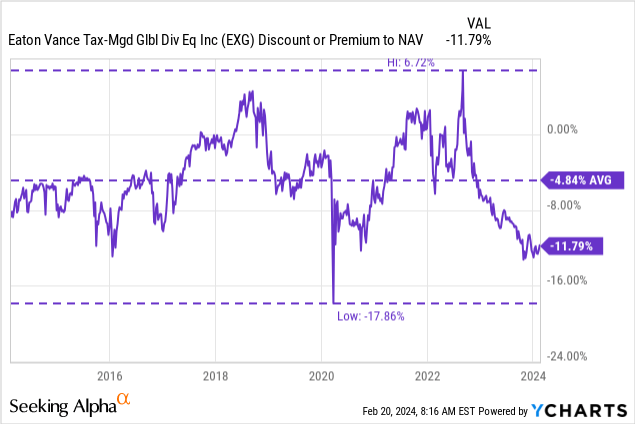

What makes EXG (and ETW) engaging at the moment is the big reductions these funds are carrying. A big low cost by itself does not inform us the entire story, however this fund is not simply buying and selling at a large low cost on an absolute foundation but additionally on a relative foundation.

EXG Fundamentals

- 1-12 months Z-score: -0.92

- Low cost: -11.79%

- Distribution Yield: 8.37%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Property: $2.754 billion

- Construction: Perpetual.

EXG will:

“invest in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend-paying stocks and writes call options on one or more U.S. and foreign indices with respect to a portion of the value of its common stock portfolio to generate current cash flow from the options premium received.”

They last reported being overwritten by 48%, which recurrently is the case, because it was the very same in our prior replace.

They’ve a “tax-managed” focus, because the title would counsel. They do that by:

“evaluating returns on an after-tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the fund.”

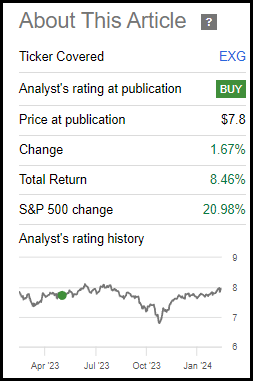

Efficiency – Low cost Trying Interesting

Since our last update, the fund has offered constructive complete returns and barely constructive value returns. Nonetheless, it was exceeded simply by the S&P 500. A few of this was as a result of low cost widening, resulting in considerably diminished outcomes.

EXG Efficiency Since Prior Replace (Searching for Alpha)

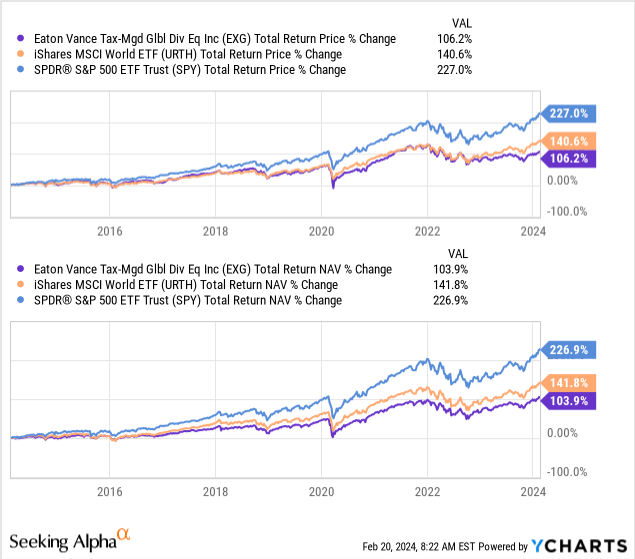

Nonetheless, a bigger issue right here is world publicity and a call-writing technique. World investments have been comparatively weaker performers for many of the final decade. Nonetheless, that is not all the time the case, as traditionally, there have been durations the place worldwide investments did outperform. That mentioned, for many of EXG’s life, it has been comparatively weaker.

The decision-writing technique additionally performs a job in some underperformance when the market is broadly performing nicely. That is why, during the last decade, it additionally is not too shocking to see the fund outperformed by one thing just like the iShares MSCI World ETF (URTH).

Ycharts

Writing calls can typically cap upside potential, and by writing index calls, the fund can expertise losses when the index it writes towards retains rising.

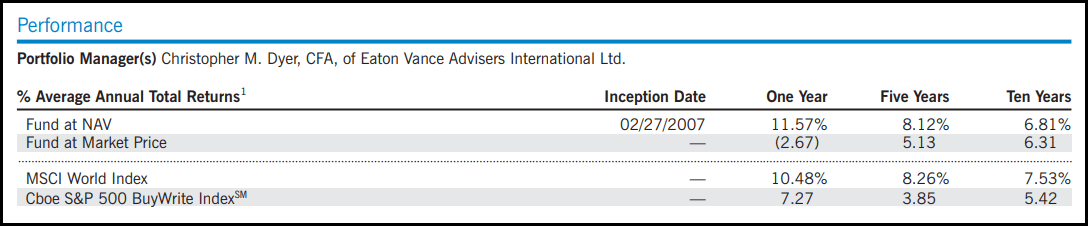

That is why when the fund lays out its efficiency, it additionally consists of the CBOE S&P 500 BuyWrite Index for comparability to assist present some context of the efficiency relative to the choices technique it employs. On that foundation, EXG’s outcomes are far more comparable and even exceed the index’s outcomes fairly considerably. Although it needs to be famous that these outcomes are from the fund’s final annual report, that’s, for the interval ending October 31, 2023.

EXG Annualized Efficiency In comparison with Benchmarks (Eaton Vance)

One factor that investing in an index cannot present – moreover not being instantly investible within the first place with out a proxy ETF that tracks an index – is a reduction to its internet asset worth per share.

The low cost for EXG, much like the opposite Eaton Vance equity-based funds, got here primarily as the results of distribution cuts the sponsor took in late 2022. A distribution reduce is commonly one of many essential catalysts for a reduction to open up on closed-end funds as a result of, in contrast to their exchange-traded fund (“ETF”) counterparts that always pay variable dividends primarily based on money flows acquired, CEFs aren’t allowed to chop their distributions primarily based on situations. They have to pay a managed or degree distribution for his or her complete life. Properly, not likely by any actual legislation or something, however by the unwritten legal guidelines of most CEF traders.

Personally, I discover distribution cuts typically current a few of the greatest investing alternatives. After all, I would not say I prefer it when it is finished in a fund I already personal, but when it is one I am trying so as to add, it typically gives a chance.

With that being mentioned, earlier than that, the fund was buying and selling at a premium. So clearly, this was one of many essential catalysts to push the low cost wider.

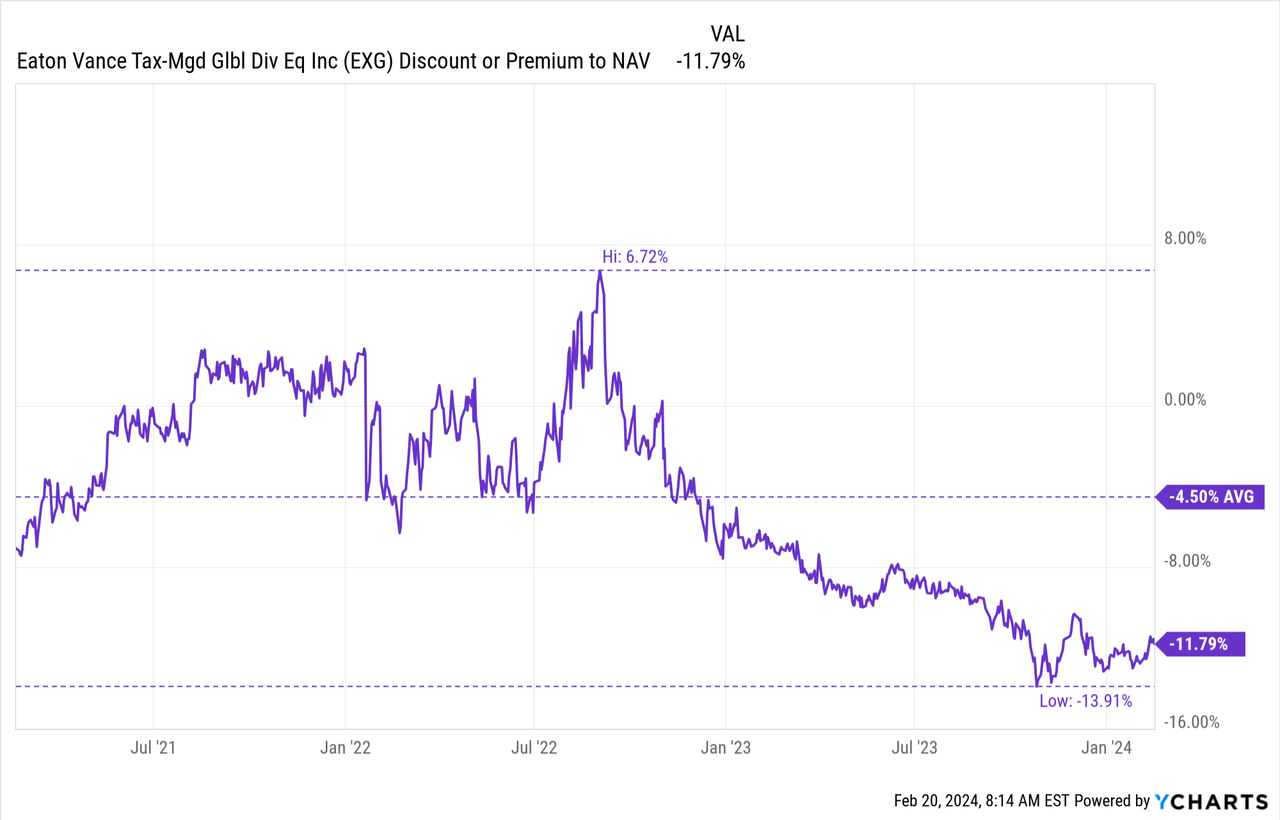

Additional, CEFs have been buying and selling at a few of the widest discounts historically. This has narrowed considerably extra lately. Nonetheless, since we got here from 2021 when reductions had been traditionally slender, the drop has actually felt far more dramatic during the last couple of years.

EXG was just about an ideal instance to focus on what was taking place extra broadly and what a distribution reduce can do to a CEF’s valuation as nicely. Going from a premium of almost 7% after which dropping all the best way to a low low cost level of almost -14% is one thing shareholders are going to really feel.

Ycharts

We have come off the lows, however on a relative foundation, we will see that the low cost is sort of interesting at the moment. Although the above is for the final three years, if we have a look at the final 5 years, the fund’s common low cost was considerably comparable at round -5.2%. Trying again even longer, during the last decade, we additionally see an analogous image.

Ycharts

The fund might go to a good wider low cost, however at the least if historical past is any indication, additional low cost widening might be restricted from right here.

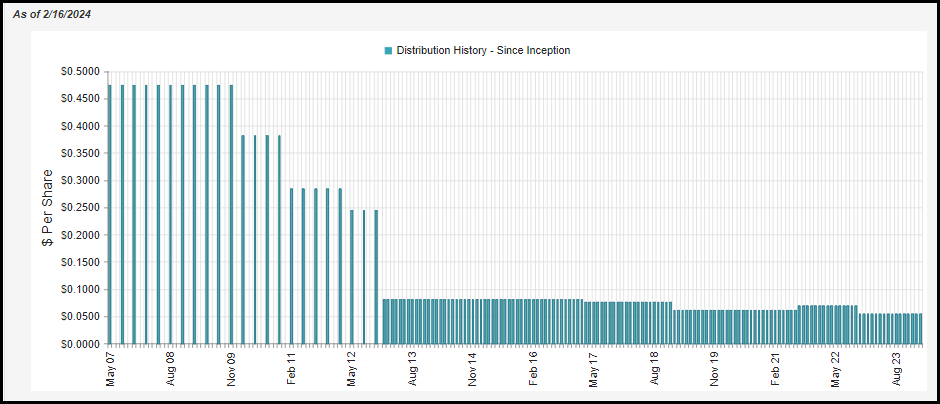

EXG’s Distribution

The fund’s distribution involves a comparatively engaging 8.37% distribution yield, and that works out to an NAV charge of seven.38%. The distinction right here is that due to the fund’s substantial low cost, traders can obtain greater than the underlying fund has to earn.

EXG Distribution Historical past (CEFConnect)

At this charge, we might nearly be ready for the fund to boost its payout to traders, assuming the market continues to stay comparatively calm and carry out nicely. The market performing nicely is an actual concern for the distribution as a result of, like many fairness CEFs, it’s going to rely considerably on capital beneficial properties to fund its payout to traders.

EXG Annual Report (Eaton Vance)

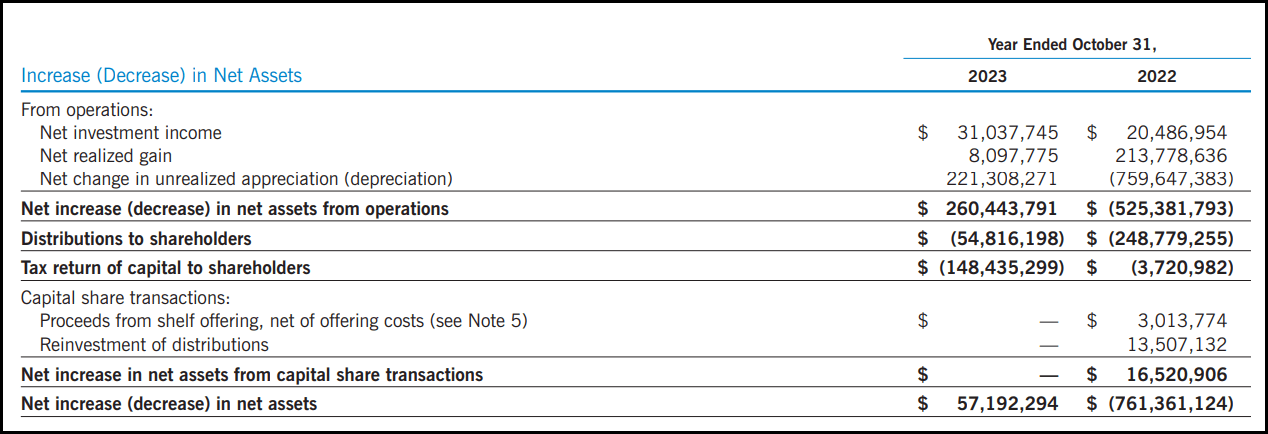

A few of these capital beneficial properties can come from the choices writing technique. Nonetheless, it typically is not as simple as that. It’s because the technique also can produce losses; as we talked about above, if the index continues to rise, they’re going to have to shut out the contracts at a loss.

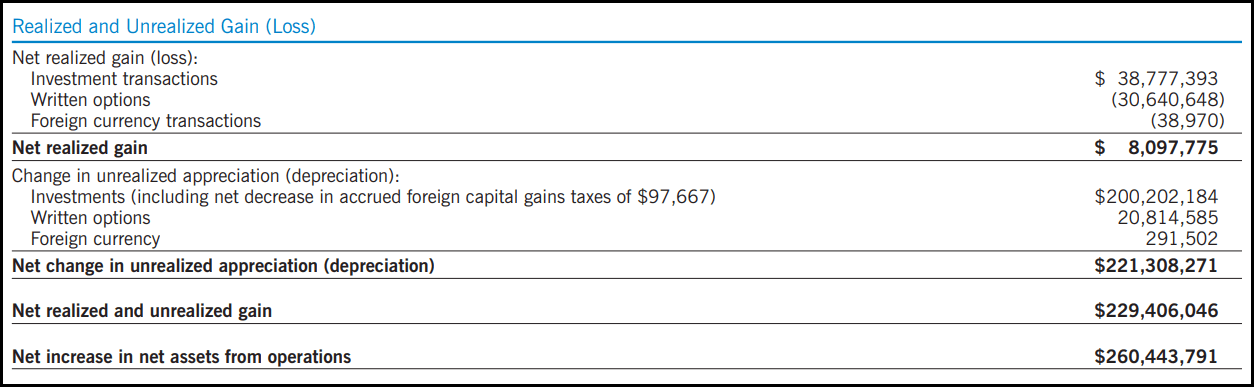

That is what ended up taking place within the final fiscal 12 months, because the choices technique generated unrealized losses of over $30.5 million – partially offset by the unrealized beneficial properties of almost $21 million from the technique. These losses had been additionally greater than offset by realized appreciation from the fund’s underlying portfolio.

EXG Realized/Unrealized Features/Losses (Eaton Vance)

That is actually the place the technique facilities round: an index cannot be owned instantly, however they’ll personal underlying positions that make up the indexes. In order that takes the chance off the desk of theoretically limitless losses that would occur from bare index writing. If the choices writing technique is producing losses, it is as a result of equities are appreciating. This could work in reverse, too; if the underlying portfolio is falling and producing losses, the choices premium acquired can offset a few of these declines.

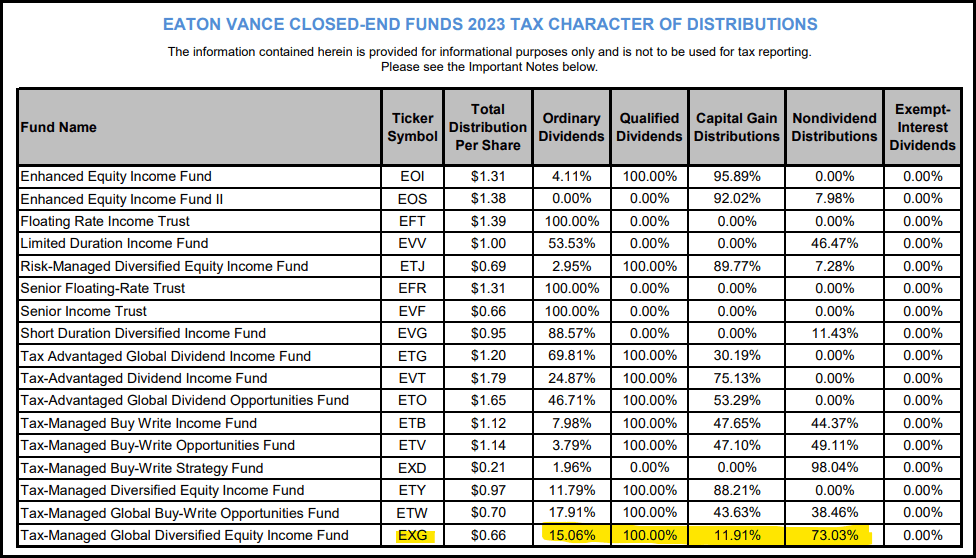

Lastly, the choices writing technique also can play a job within the fund’s distribution tax classifications. Should you understand losses from one facet of the technique which can be offsetting realized beneficial properties from the opposite facet, you then will find yourself producing a return of capital distributions. On this case, Eaton Vance labels them “non-dividend distributions.”

These breakdowns can fluctuate from 12 months to 12 months, however seeing ROC distributions from Eaton Vance funds is not something too shocking. That’s, in truth, the place they get the “tax-managed” a part of their names.

For EXG, 2023 listed {that a} majority of the distribution was ROC. What portion that wasn’t ROC was both certified dividends or long-term capital beneficial properties – that are additional tax-friendly classifications for distributions.

Eaton Vance Distribution Tax Character (Eaton Vance (highlights from writer))

EXG’s Portfolio

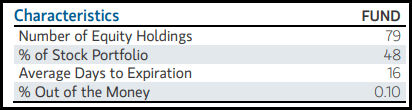

Turning towards the fund’s portfolio, they had been slightly bit quiet within the newest fiscal 2023. Their portfolio turnover charge got here to 19%, which was down from 27% and 44% in every of the prior fiscal years. That is not essentially a foul factor, both, because it as soon as once more can return to its portfolio technique of avoiding an excessive amount of in taxable distributions. If investments are performing nicely throughout the board, an excessive amount of turnover might result in realizing too many beneficial properties.

The fund’s newest truth sheet confirmed they had been holding simply 79 holdings complete. We additionally see that the overwriting of the portfolio got here in simply shy of fifty%, which is according to their goal degree.

EXG Portfolio Traits (Eaton Vance)

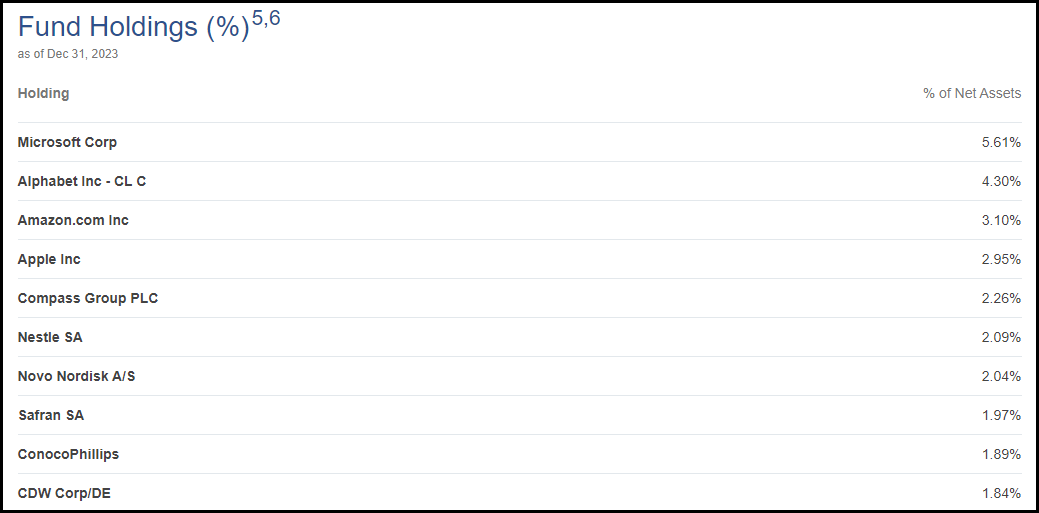

When trying on the prime ten holdings, we see fairly just a few Magazine 7 names. In complete, these mega-cap tech names signify simply shy of 16% between Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN) and Apple (AAPL). These had been additionally holdings listed as prime ten names within the final replace we had for this fund.

EXG High Ten Holdings (Eaton Vance)

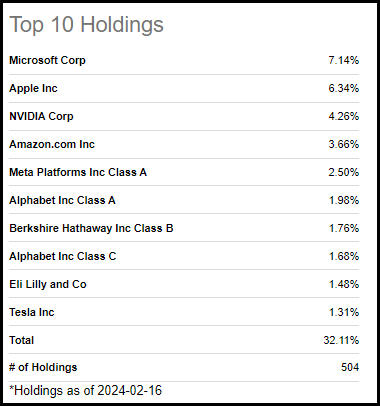

That weighting within the Magazine 7 names is definitely considerably lower than the S&P 500 itself proper now, as represented by the SPDR S&P 500 ETF (SPY), which listed its Magazine 7 publicity as simply over 27.5%. When you think about that SPY lists 504 holdings, that is an enormous relative obese to those few chosen names. In some methods, it might be argued that EXG is definitely extra diversified regardless of solely carrying lower than 80 complete holdings.

SPY High Ten (Searching for Alpha)

Once more, SPY or the S&P 500 aren’t truly benchmarks for the fund, however the dialogue is useful for offering some relative context and why efficiency goes the best way it’s. If the fund had simply overweighted the Magazine 7 names traditionally, it might have truly carried out higher. That is all the time straightforward to see in hindsight, although.

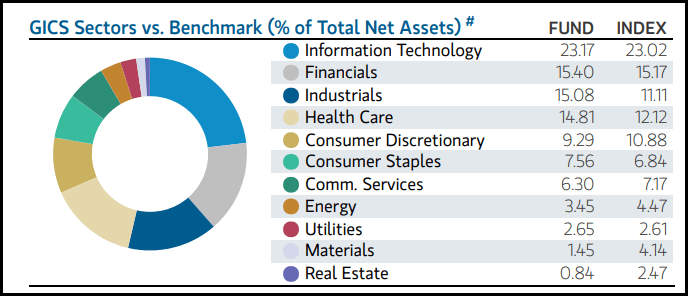

When trying on the fund’s precise benchmark, the MSCI World Index, we will see that the sector weightings are far more in line.

EXG Sector Allocation (Eaton Vance)

Conclusion

Eaton Vance Tax-Managed World Diversified Fairness Earnings Fund is buying and selling at a significant low cost on an absolute and relative foundation. The distribution reduce from nicely over a 12 months in the past was at the least partially accountable for getting the fund to commerce at a considerable low cost. Nonetheless, the widening of CEF reductions during the last couple of years extra broadly clearly performed a job as nicely. Whether or not the low cost will slender sooner or later is but to be decided; although, if historical past is any information, we might at the least be seeing a degree the place the low cost widening even additional might be restricted. That makes it a reasonably engaging time to think about investing in Eaton Vance Tax-Managed World Diversified Fairness Earnings Fund.