grandriver

I began coverage of Exxon Mobil Corp (NYSE:XOM) in October 2023, highlighting it as my favourite play within the worldwide oil patch given its superior execution and administration together with a good geographic footprint vs. friends. Following the corporate’s announcement to take over Permian E&P Pioneer Sources (PXD) in late November, I printed an extra be aware, commenting and offering my ideas on what I deem to be an ideal strategic match to XOM’s mid-term technique of shifting its portfolio in the direction of increased safety and shorter cycle home US-produced barrels. On this be aware, I’ll present an replace on key themes introduced in these preliminary notes and replace my valuation to include Pioneer’s contribution with the acquisition anticipated to shut in Q2 2024.

[Note: Peers refer to Chevron (CVX), Shell (SHEL), BP (BP) and TotalEnergies (TTE)]

2023 Evaluation

Issued on February 2, Exxon’s This autumn and FY23 earnings release revealed continued sturdy execution whilst crude traded considerably beneath latest heights for almost all of the yr. Complete annual earnings amounted to $36bn, representing >40% annual development vs. a 2019 baseline, with working money at $55bn for a >15% CAGR vs. 2019.

Capital Effectivity

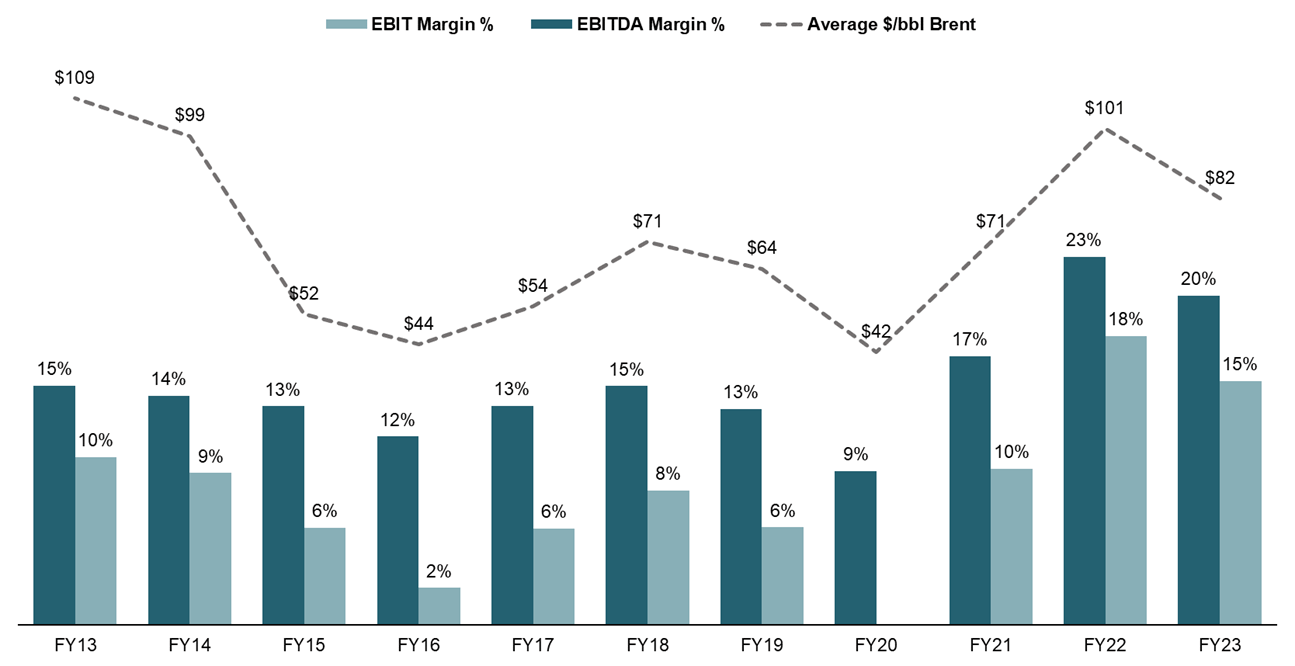

EBITDA and EBIT margins for 2023 stood at 20% and 15% which, whereas down from FY22, considerably exceeded realized margins in prior durations with comparable oil value environments (FY23 common $/bbl Brent of $82).

As mentioned in prior notes, nearly all of this margin growth may be attributed to administration’s important effectivity packages which as of FY23 achieved complete structural value financial savings of ~$10bn, primarily within the type of strategic headcount reductions and portfolio rationalization throughout up- and downstream.

XOM Margins (Firm Filings)

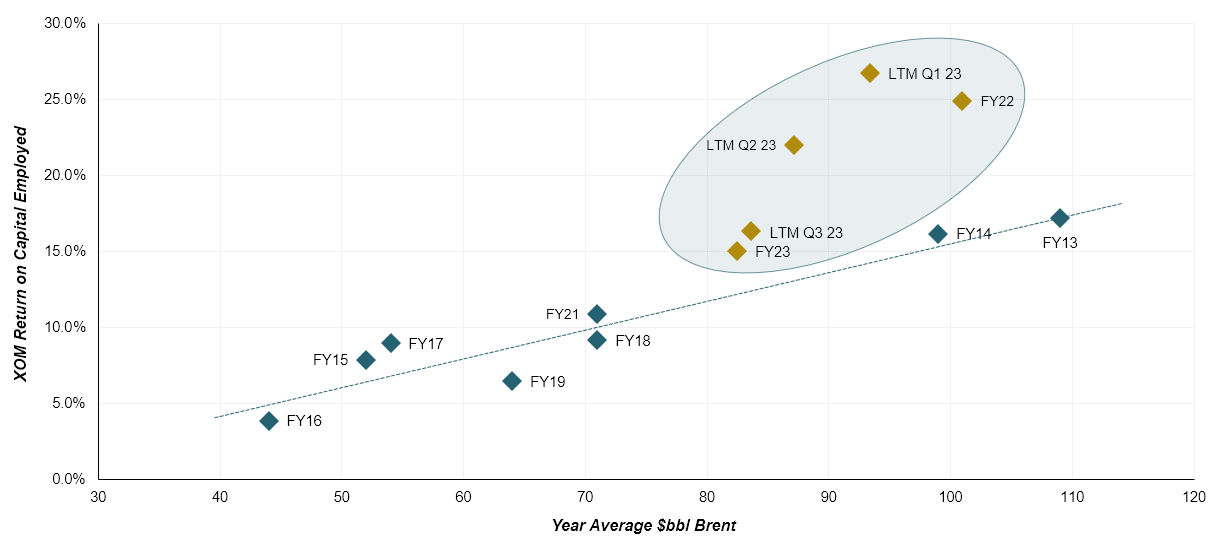

On the again of upper margins and steady ranges of employed capital (outlined by the corporate as Complete Belongings much less Complete Liabilities ex Debt), XOM additionally continued its trajectory of delivering considerably increased returns on capital in comparison with earlier durations. Whereas complete FY23 ROCE (Return on Capital Employed) of 15% was beneath earlier LTM durations (LTM Q3 23 / Q2 23 ROCE of ~16%/~22%), it continues to attain greater than 25% above previous-period implied ROCEs as measured by a regression method.

I do be aware that these premia (for a better description of the idea I employed, please see my initiation note) have come down from FY22 and the LTM interval as of Q1 23 the place precise ROCEs have been 86% and 67% increased than predicted. Nonetheless, as these durations had terribly excessive $/bbl environments on the backdrop of the Ukraine struggle, I consider present outcomes are extra reflective of normalized midcycle oil value environments whereas nonetheless highlighting the numerous growth in capital effectivity versus the pre-2019 interval.

XOM Returns on Capital Employed (Firm Filings)

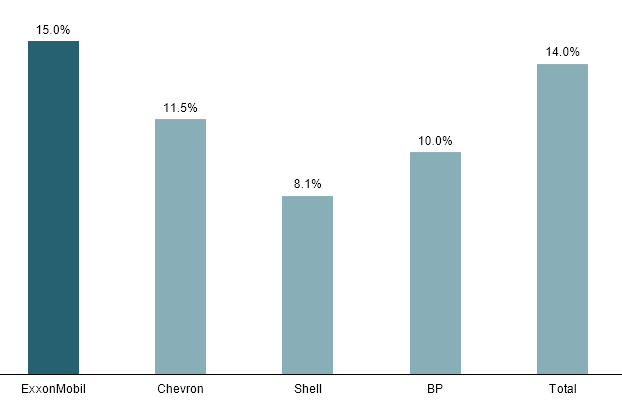

ROCE additionally continues to exceed friends, producing on common ~11%, giving XOM virtually a 40% premium in capital effectivity towards friends.

XOM FY23 ROCE vs Friends (Firm Filings)

Downstream Section

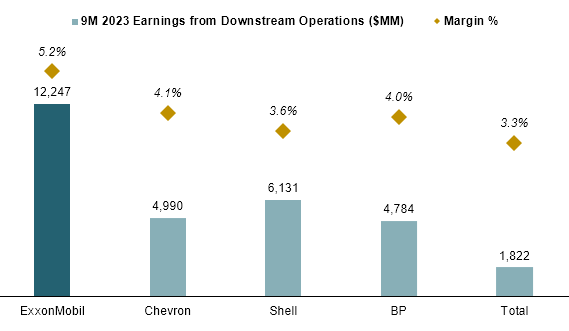

Exxon’s downstream phase, which I beforehand highlighted as a key aggressive benefit to friends because of its means to (no less than partially) offset the whole earnings impression of oil value declines as earnings features from decrease feedstock costs steadiness out decrease upstream income. As of 9M 2023, income from downstream (Vitality Merchandise, Chemical Merchandise, Specialty Merchandise) contributed ~42% of XOM’s complete earnings, giving it a considerably increased weight in comparison with friends with on common ~26% of earnings from downstream.

General 9M 2023 earnings from downstream operations have been down by ~23% to $12.3bn on the again of comparatively steady volumes and normalizing refining margins which had terribly benefitted the phase in 2022. Vitality Merchandise (petroleum refining) throughput was up by 2.1% to ~5.5 mboed amid document excessive working reliability and a 250kboed capability growth in its Baytown, Texas refinery offsetting additional underperforming complicated divestments. Chemical Merchandise (commodity petrochemicals) volumes have been additionally up by 1.1% whereas volumes within the Specialty Chemical compounds enterprise decreased by 2.7% pushed by decrease financial exercise, particularly in manufacturing.

Regardless of the decline in earnings and margins falling by ~60bps to five.2%, Exxon’s downstream operations proceed to steer friends in each scale and profitability whereas administration’s efforts to streamline the refinery and petchem plant footprint precipitated margins to contract considerably lower than friends (common adverse ~82bps).

Downstream Efficiency XOM vs Friends (Firm Filings)

Steadiness Sheet and Shareholder Returns

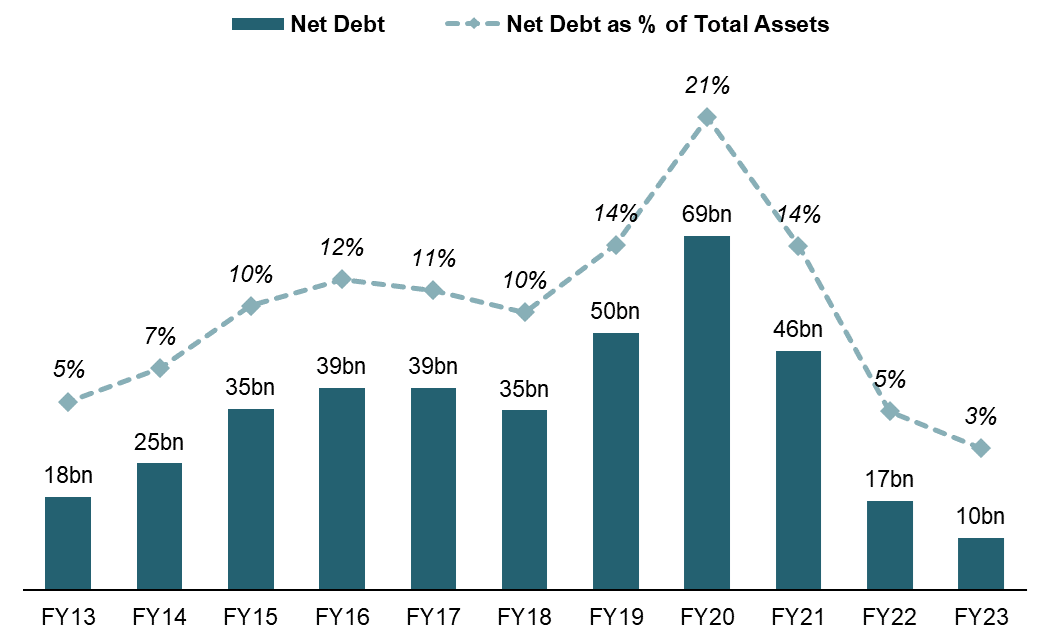

Throughout FY23, Exxon additional strengthened its steadiness sheet, decreasing its web debt place to ~$10bn on increased money and continued Covid-era debt paydown.

XOM Web Debt (Firm Filings)

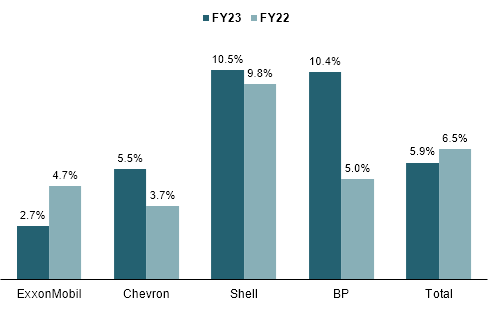

As of YE23 web debt stood at ~2.7% of complete belongings, down from ~4.7% at YE22, giving XOM the bottom leverage within the peer group with CVX, SHEL and BP really growing leverages, primarily pushed by decrease money balances.

Web Debt as % of Steadiness Sheet (Firm Filings)

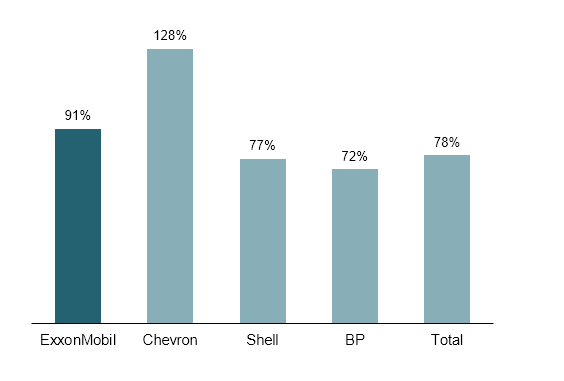

Paying a complete of $15bn in widespread inventory dividends and repurchasing $17.5bn value of shares (~4.3% of present cap) throughout FY23, Exxon allotted 91% of complete FCF ($36.1bn) in the direction of shareholders, behind CVX at 128% however considerably forward of European friends at ~75%. Whereas XOM notably trails its key US rival in shareholder distributions, I do like administration’s barely extra conservative method within the matter, as an alternative aiming to additional enhance its steadiness sheet versus funding extra payouts with new debt/present money.

Shareholder Returns as % of FCF (Firm Filings)

XOM Buyback Potential (Firm Filings)

Manufacturing Replace

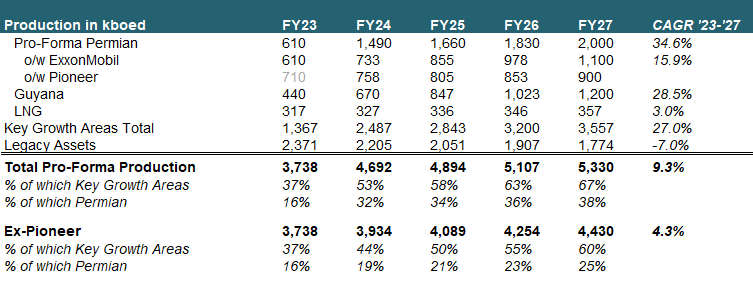

Common every day oil-equivalent manufacturing as measured in kboed for FY23 stood at 3,738 which was flat vs. FY22 as a powerful This autumn (3,824kboed) was offset by upkeep initiatives in H1. Notably, oil manufacturing within the Permian and Guyana (together with LNG and Brazil, designated as administration’s key development areas) rose by 18% YoY with Guyana reaching a document quarterly gross manufacturing of ~440 kboed because the Payara growth within the Stabroek block got here on-line forward of schedule.

Incorporating Pioneer into my manufacturing forecast, I estimate Professional-Forma oil & fuel manufacturing in oil-equivalent models to rise to ~5.3mboed by FY27 at a 9.3% annual development fee with Pioneer anticipated to contribute a complete of 900kboed, rising from 710kboed as of FY23. As mentioned throughout my be aware on the proposed acquisition, I estimate this to extend Professional-Forma Permian manufacturing to ~2mboed, representing a ~38% share of complete versus ~25% on an Exxon standalone foundation. The manufacturing share of key development areas may even rise to 67% over the interval, in comparison with 37% as of FY23, as Guyana manufacturing is projected to extend to ~1.2mboed by FY27.

Professional-Forma Manufacturing Forecast (Firm Filings and Writer’s Estimates)

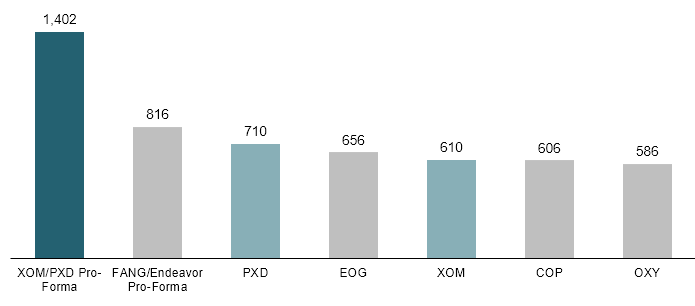

The deal may even make the consolidated entity the undisputed chief within the Permian at ~1.4mboed present manufacturing. Notably, since my final be aware Diamondback Vitality (FANG) introduced its intention to amass non-public driller Endeavor Sources, making it the second-largest producer behind Exxon/Pioneer and forward of EOG (EOG), ConocoPhillips (COP) and Occidental (OXY).

FY23 Permian High Producers (Firm Filings, Enverus)

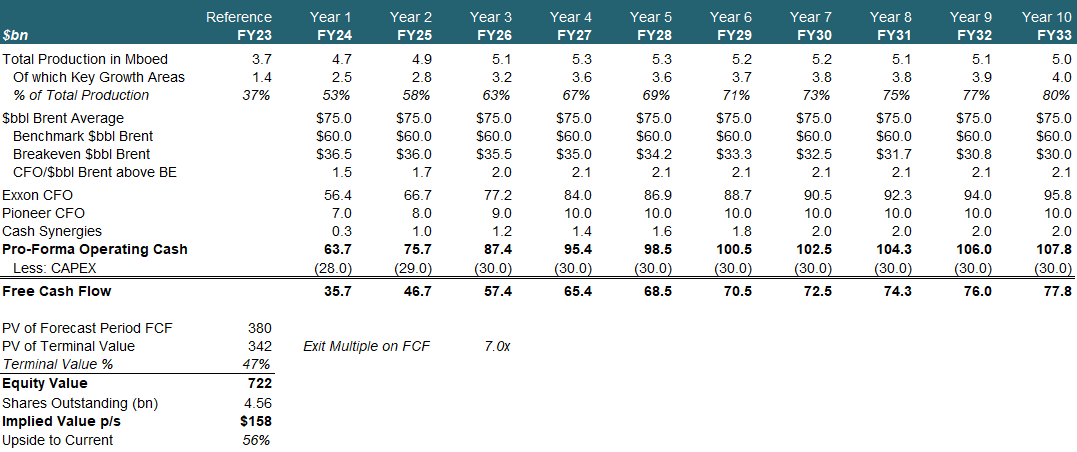

Valuation Replace

I initially valued XOM primarily based on a 5Y-DCF with an infinite development assumption of -2% to replicate the (slower than beforehand anticipated however sure) secular decline of the trade. Nonetheless, right here I wish to introduce an up to date framework, extending the projection interval to 10 years and as an alternative utilizing an exit a number of on FY33 estimated FCF to higher replicate the corporate’s terminal worth.

Holding my assumptions for oil costs at an inexpensive $75/bbl Brent stage, I regulate breakeven value projections in step with Exxon’s newest company plan as of December 2023, now calling for $35/bbl to be reached by FY27 versus the beforehand focused $30/bbl. I additionally incorporate Pioneer’s anticipated money flows, which I estimate at $10bn p.a. by FY27 (according to a regression of CFO to Brent $/bbl for earlier 12-month durations over the previous 2 years) and anticipated merger synergies as lined out in my be aware on the deal. Capex can also be adjusted upwards to replicate ~$4bn of annual Capex from Pioneer and a slight enhance in Exxon’s projected Capex ranges.

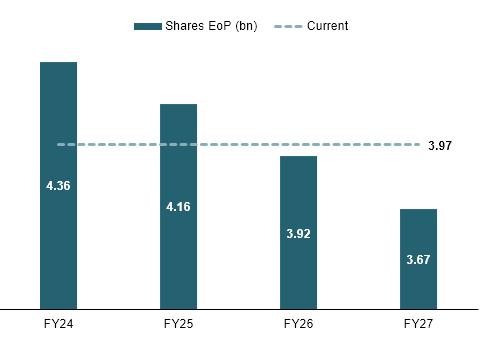

Utilizing an unchanged value of fairness of 10% and an exit a number of of seven.0x Value/FCF (barely beneath XOM L5Y common of ~8.4x), I calculate a complete Fairness Worth of $722bn. Assuming a post-close share rely of 4.56bn (3.97bn present and 0.59bn in extra shares to be issued) I derive a good worth per share of $158 for the consolidated entity, up 15% vs. my earlier value goal and implying 56% upside to present buying and selling ranges.

XOM DCF Evaluation (Firm Filings and Writer’s Estimates)