Erik Isakson

Fabrinet’s (NYSE:FN) stock surged by more than 157% last year, beating the tech-heavy Invesco QQQ Trust ETF (QQQ) by more than 100% as shown in the chart below. This is mostly because of the market pricing in AI-related prospects, but things seem to have changed from March this year, illustrated by its orange chart underperforming NVIDIA Corporation (NVDA) in purple.

Comparing the price performances (seekingalpha.com)

This volatility was most likely induced by an announcement about copper interconnects replacing optical fiber in data centers during the launch of the semiconductor giant’s latest Blackwell architecture as detailed later. However, the stock has already recouped some of its losses, and this thesis aims to show that the upside has legs.

First, I provide insights about how Nvidia’s accelerator GPUs making their way into data centers has benefited the demand for Fabrinet’s products.

Exploding Demand for Interconnects Have Boosted Optics Sales

Today, most data centers are filled with servers containing CPUs (compute processing units) produced mostly by Intel Corporation (INTC) that have to be connected to network switches linked to other servers or storage devices, thereby requiring the use of interconnects. Things started to change rapidly since the emergence of ChatGPT in November 2022 which is powered by Generative AI and, for this new flavor of artificial intelligence to function optimally, there is a need for Nvidia accelerator GPUs such as the H100.

Now, as these superfast chips make their way into data centers, operators have to adapt, not only to cater to higher power and cooling requirements but also to elevated network bandwidth or capacity. The reason is that with their ability to perform parallel processing or several tasks simultaneously, GPUs can ingest data faster than CPUs. In this scenario, fiber optics interconnects such as Active Optical Cables (AOC) manufactured by Fabrinet are key to transmitting data at a rate fast enough to satisfy AI demands without causing latency (delay).

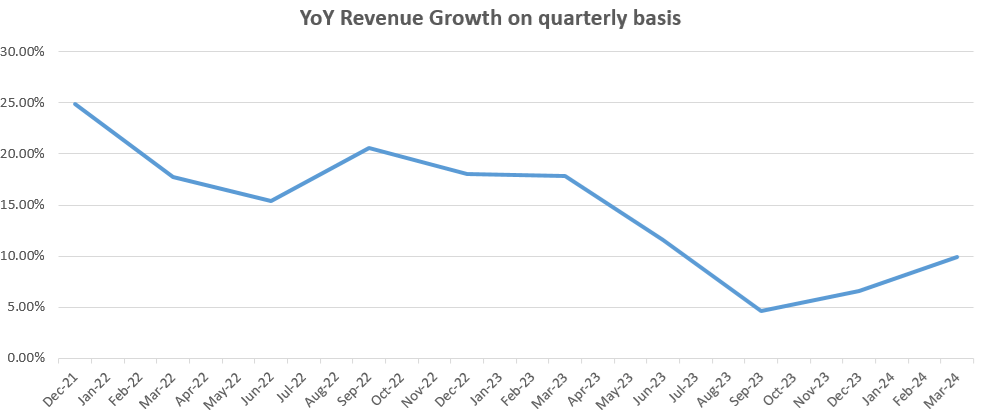

Thus, as more GPUs go online, the fiber counts per server are increasing requiring more AOCs resulting in Fabrinet’s Datacom segment’s revenue skyrocketing by 150% YoY in the third quarter of fiscal 2024 (Q3) thanks mostly to demand for its 400 gigs (Gigabytes) products together with the newer 800 gigs technology.

Looking at the trend, revenues have continued to grow after the double-digit digital transformation-led growth of 2021-2022 as charted below, but at a lower pace than for Super Micro Computer, Inc. (SMCI) which has benefited from a much higher degree of derived demand as an OEM manufacturer packing Nvidia’s GPUs into servers.

Chart prepared using data from (seekingalpha.com)

The reason is that Fabrinet also has a non-optical communications business that has not fared well partially offsetting the strength seen in optics. Thus, only $140.1 million was obtained from non-optics in Q3 representing both a YoY and sequential decline as pictured in the yellow chart below.

Discussing Product-Mix and Nvidia-Related Risks for Fiber Versus Copper

Therefore, it is important to analyze the revenue mix to ascertain whether optics can continue to drive overall sales.

seekingalpha.com

Thus, looking deeper into non-optics, the sequential revenue decline was due to automotive customers digesting their inventories. However, since the problem was not due to unfavorable macros but to certain products having already been over-supplied, the management is optimistic that related sales will make a comeback in the fourth quarter (Q4).

Moreover, the company has a degree of dependence on the telecom sector where revenues picked up mostly driven by data center interconnect products, after several quarters of decline. However, this pickup is viewed as temporary due to weakness in the sector exacerbated by elevated inventory levels. Thus, the management anticipates “continued choppiness” as its telecom customers digest their inventories.

Therefore, it appears to be more of a mixed picture, but one that could benefit from continued strength in optics, but, first, it is important to discuss the related risks.

In this respect, there is uncertainty emanating from Nvidia itself when during its GTC2024 conference on March 18 marking the launch of Blackwell, the latest generation of AI chip architecture. At that time, it was mentioned that the first Blackwell chip, or the GB200 would use a copper cable interconnect, instead of fiber because of the advantages in terms of high-speed data transmission thereby allowing for faster processing while consuming less energy to transmit the same terabyte of data. Copper’s energy argument is a strong one given GPUs consume more power than conventional CPUs, and, in contrast, Fabrinet capitalizes on optics.

In these circumstances, it is not surprising that Nvidia’s update somewhat coincided with volatility for the stock causing it to lose more than 50% of its value because of doubts emerging as to whether it can sustain the same sales momentum for optical interconnects in AI data centers.

Sustained Demand From AI and AMD ships GPUs

However, in response to this threat, Fabrinet’s CEO downplayed the risks during Q3’s earning call, mentioning that these pertain to specific use cases and should not result in copper interconnects cannibalizing his company’s market share.

I believe this position is justified based on an article in Semiconductor Engineering on how AI is driving the need for optical interconnects in data centers. Thus, the industry is transitioning to higher data-speed products with 100 gigs being gradually phased out in favor of higher speeds like 200 gigs followed by 400 gigs and now 800 gigs for AI workloads, but, at the same time, the distances between appliances are increasing. This development does not favor copper which tends to perform well for short reaches only. Therefore, while some hyperscalers may adopt copper for inter-rack connectivity, it is debatable whether they will alter their data center setups just to be aligned with Nvidia’s position, and for the Blackwell chip that has not yet been launched.

Moreover, the fact that the stock has recovered gives credence to the idea that there is a limited risk of copper dethroning fiber in data centers. Along the same lines, Nvidia’s GPUs have only accelerated the demand for more network bandwidth to support data-intensive AI applications. In this context of change, in addition to Nvidia, there is Advanced Micro Devices, Inc. (AMD) with its MI300 GPUs, expected to start mass-shipping in the first half of this year. To keep pace, both data center operators and network equipment suppliers have to continue providing higher-speed interconnects, explaining why demand for Fabrinet’s 800 gigs interconnects is expected to remain “very robust” while it is preparing to support the faster 1,600 gigs products.

This idea of robust demand is supported by research by the Dell’Oro Group which expects most of the switch ports in AI back-end networks to be upgraded to 800 Gbps by 2025 and 1600 gigs by 2027. Moreover, since bandwidth demand is expected to grow by 30%-40% yearly, the revenue estimates for FY’25 (ending in June this year) which currently stands at $3.17 billion and constitutes a 10.8% YoY growth could be revised upwards.

Assuming a 30% increase, sales would increase to $3.72 billion instead of the $3.17 billion estimated by analysts as illustrated in the table below, in turn reducing the forward price to sales to 2.38x ((2.86/3.72)x 2.79). This is below the median for the IT sector of 3.05x by around 22%.

Table prepared using data from (www.seekingalpha.com)

To identify a target price, I consider that with a momentum score of A+, the stock could benefit from further upside when Q4’s financial results are announced in August as was the case on May 6 when it jumped by 15% when Q3’s results were announced. Thus, incrementing the current share price of $235.47 by 15%, I obtained a target of around $271. This buy position is justified by the company beating topline estimates eight times in the last eight quarters, which tends to indicate conservatism when the management provides guidance.

However, do expect volatility.

How To Play the Stock Given Nvidia’s Earnings Next Week

Given the latest vertiginous upside of 45% in only about three weeks which has also to some extent been driven by the possibility of the Federal Reserve cutting rates sooner rather than later after core consumer prices cooled in April, volatility could follow. This is also justified by the RSI score of 80.44, or the stock lying in overbought territory. Factors that could trigger volatility include competitors bagging major contracts for optics, any major announcements about a hyperscaler opting for copper interconnects for part of its AI workload, or Nvidia’s earnings call on May 22.

In this case, its CEO Jensen Huang is likely to be questioned by analysts about copper interconnects, and depending, on his response, the stock may be volatile, especially if he emphasizes a move away from fiber. Therefore, for those who missed the upside, the ensuing volatility could provide a better margin of safety.

This would constitute an opportunity to buy.

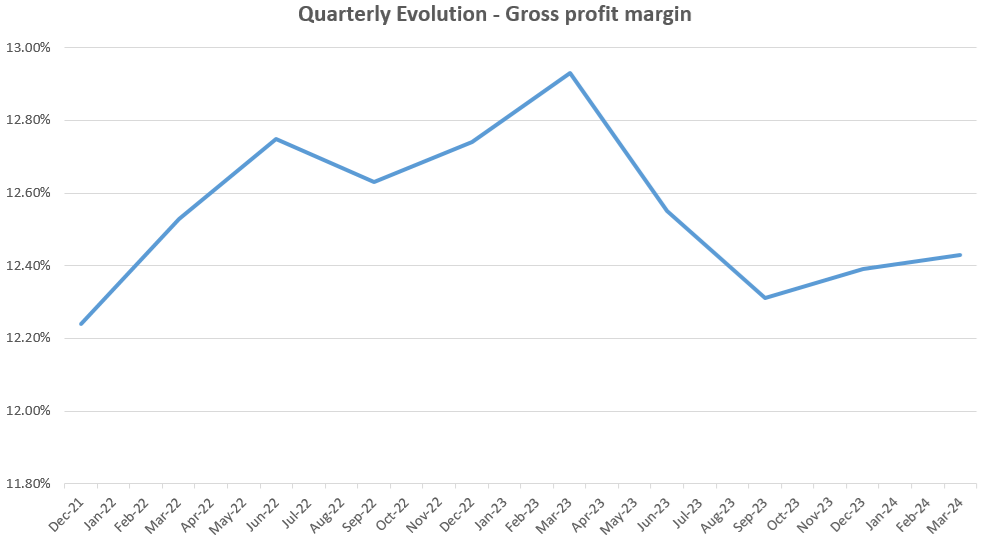

Another reason is with robust demand comes pricing power and better margins. Hence, gross profit margins remained in the 12% to 15% range during the last ten quarters despite weakness in non-optics as per the chart below. This signifies that Fabrinet could attain or even beat the EPS estimate of $8.7 for FY’24, which would constitute a 13.47% YoY increase, triggering an upside.

Chart prepared using data from (www.seekingalpha.com)

Finally, given the high demand for networking bandwidth that ChatGPT-style applications put on GPUs when they access different sources of information in real-time, Fabrinet should continue to see traction for its products, but, the company also needs to rapidly boost production capacity for the 800 gigs program in the Pinehurst facility. For this purpose, its balance sheet is equipped with $794 million of cash versus only $6 million of debt.