deberarr

Fairness Residential (NYSE:EQR) has misplaced over 8% over the previous yr, considerably lagging the broader inventory market. This has been extra in line with declines seen throughout a lot of the REIT universe as greater charges and slowing hire progress have weighed on investor sentiment. Shares have returned -3.5% since I advisable shopping for final October. This has been extra pushed by a compressed a number of than poor efficiency, and I see shares as enticing as we speak for earnings growth-oriented buyers.

In search of Alpha

Within the firm’s third quarter, EQR generated $0.96 in funds from operations (FFO), which did miss consensus by $0.01, as Ceremony Assist’s chapter weighed on outcomes. Whereas EQR is primarily a multifamily proprietor, the bottom flooring of its buildings usually has retail house. Alongside this, there was a sluggish restoration in unhealthy debt expense as onerous foreclosures processes in California have allowed delinquent tenants to stay in models for longer.

Given these quarterly outcomes, administration revised steering. For the complete yr, it now expects normalized FFO of $3.77-$3.79, decreasing the top-end of the vary by $0.04. On the midpoint, that is up 7% from final yr, which is according to the ~6% progress I forecast in final yr’s purchase advice. The truncated top-end of the FFO vary is as a result of internet working earnings steering was revised from 6.3-7% to six.2%. This was half as a result of chapter of Ceremony Assist and slower enchancment in unhealthy debt and half as a result of weakening in San Francisco and Seattle, a extra persistent issue to be involved about.

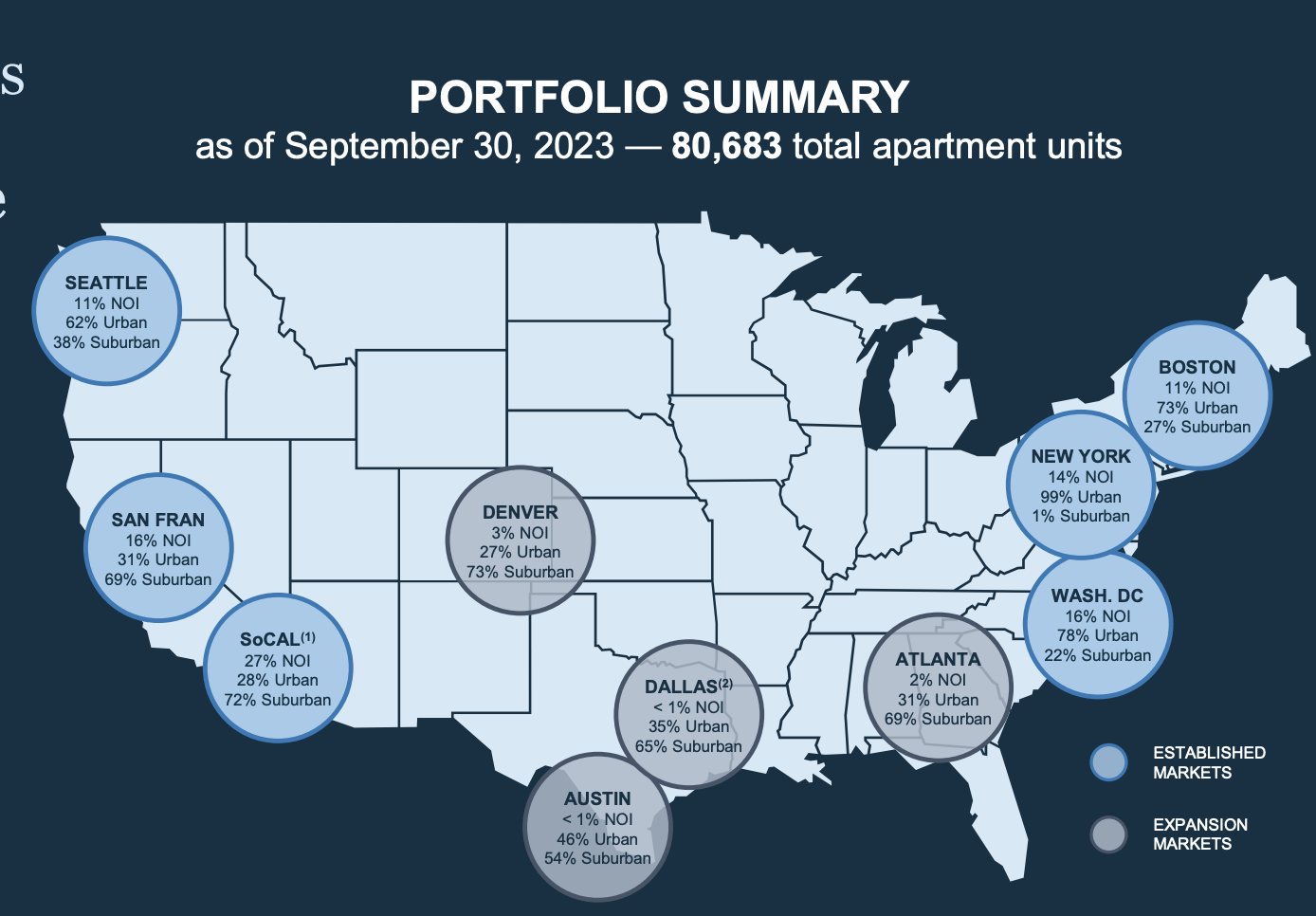

EQR owns over 80,000 models throughout 305 communities. It primarily operates out of legacy metropolitan areas, as you possibly can see beneath, like New York, Boston, DC, and San Francisco. It’s slowly increasing into the Solar Belt, ultimately concentrating on 20% of earnings in these growth markets. EQR operates upscale condo buildings; its common tenant has $170k family earnings, 60% above the nationwide common and is simply 32 years outdated. Given their greater earnings, the common hire to earnings ratio is simply 20.2% (~28% is a wholesome stage).

EQR

Its publicity to legacy markets has usually been seen as a headwind as a result of inhabitants is mostly rising quicker within the Southeast, aided by migratory patterns. Nonetheless, not all legacy markets are created equal. The truth is, in keeping with ApartmentList, Boston and New York have seen the 5th and 6th quickest rental progress over the previous three years whereas San Francisco has seen the slowest. NY has confirmed extra resilient than many anticipated, however San Francisco is clearly weak. Fortuitously, most of EQR’s publicity right here is suburban, which ought to mitigate the draw back.

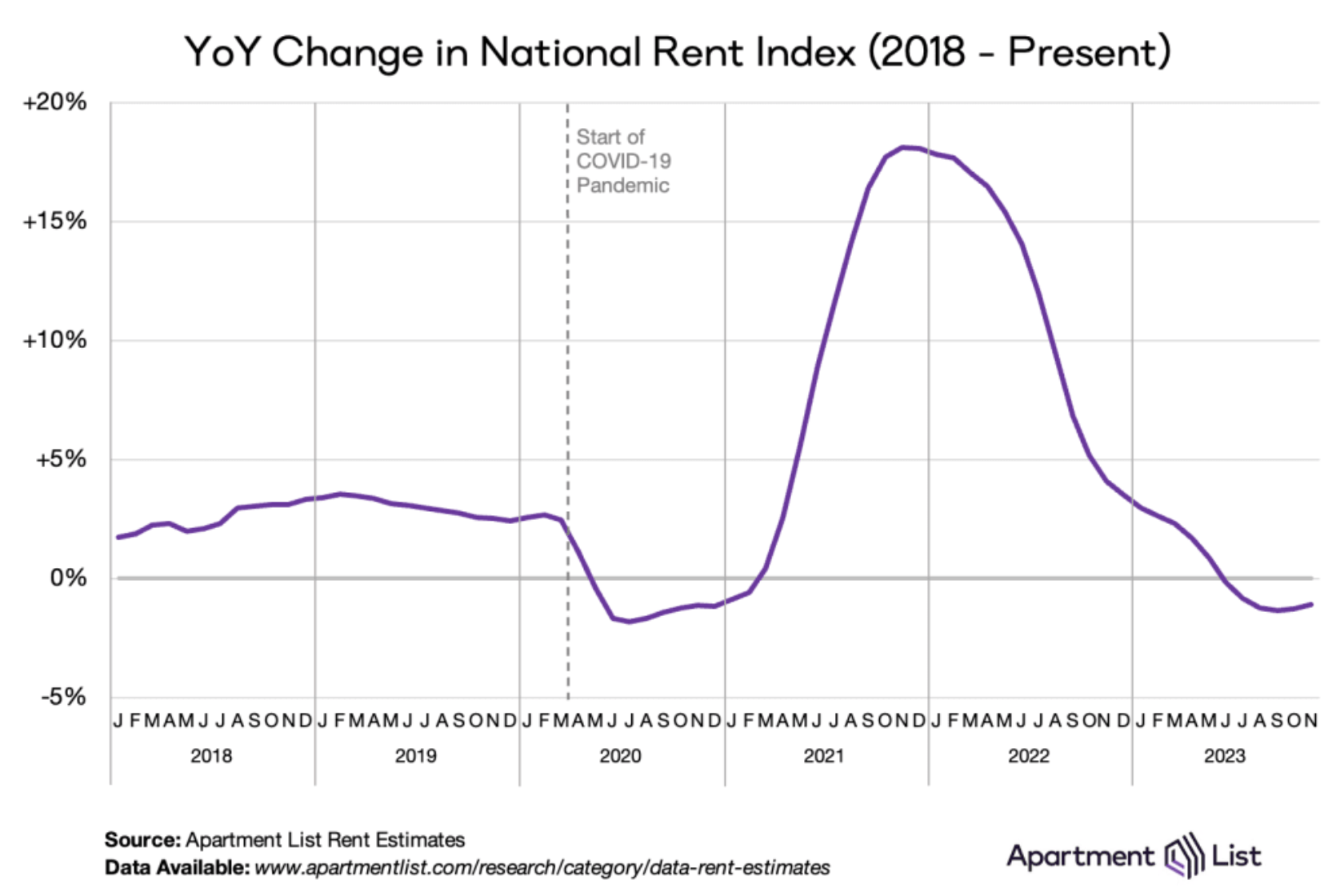

The problem for all multifamily REITs has been that rental inflation has slowed. As you possibly can see beneath, after surging dramatically after the pandemic, hire inflation is now operating adverse over the previous yr. EQR has outperformed this pattern. In Q3, blended charges rose 3.1% with new leases up 0.5% and renewals up 5.5%. I’d observe this pattern weakened in October to 1.6% as new leases declined 3.1%. Nonetheless, EQR is seeing hire progress vs the nationwide decline.

ApartmentList

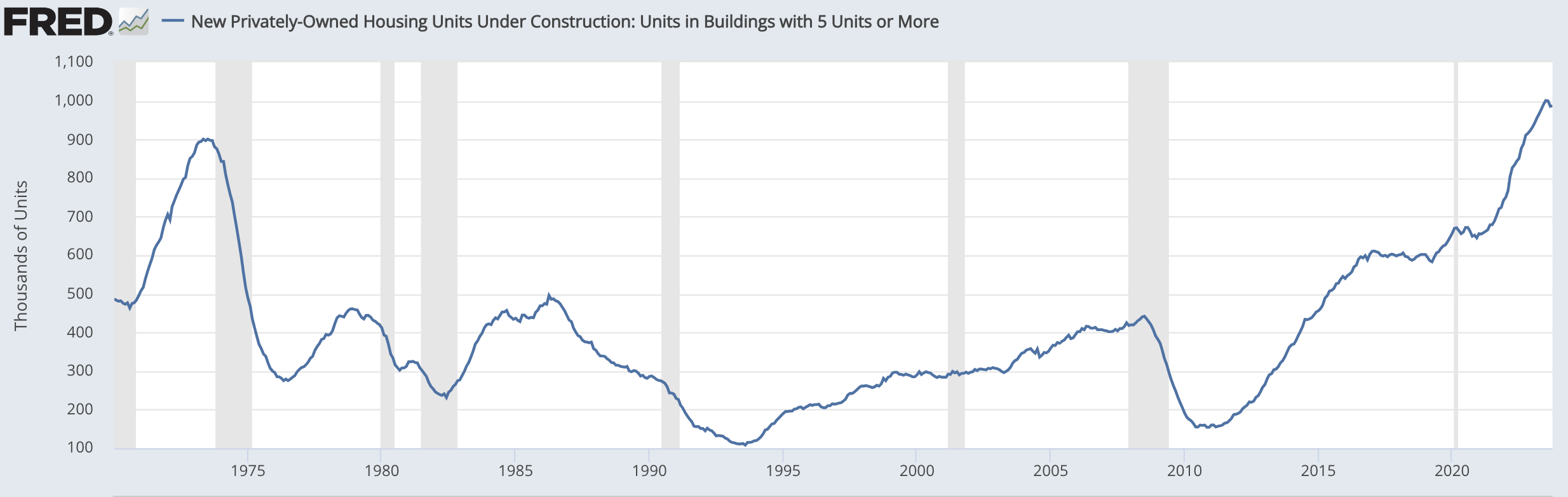

Slowing nominal earnings progress and normalizing family formation patterns have performed a job on this deceleration in hire. Nonetheless, one other main issue has been provide. Elevated rental charges made new building tasks extra enticing as builders sought to earn these rents. As such, multifamily building has soared to file ranges, although it has begun to tick down with new begins down meaningfully from their highs.

St. Louis Federal Reserve

Now, as I famous above, the Solar Belt usually talking has a extra optimistic medium-term image given the quicker inhabitants progress. Builders have seen this too, and far of this surge in building has been in these excessive progress markets. There was comparatively little building within the legacy markets EQR operates. This lack of provide has assist to insulate EQR from provide pressures. As such, whereas rental progress has remained sluggish, it has stayed optimistic general.

EQR

Whereas progress has slowed, I’d additionally emphasize that occupancy completed the quarter at 95.9% and ticked as much as 96% in October. These are excessive ranges, talking to the robust demand for its flats. EQR has additionally loved stable working leverage because it has pushed up rents over the previous two years. Final quarter, same-store income rose by 4.1% in opposition to 3.1% expense progress, rising internet working earnings by 4.6%. Comparatively modest expense progress has been aided by only a 2.5% improve in tax and insurance coverage. Offsetting this, property administration prices rose a extra substantial 9.3%.

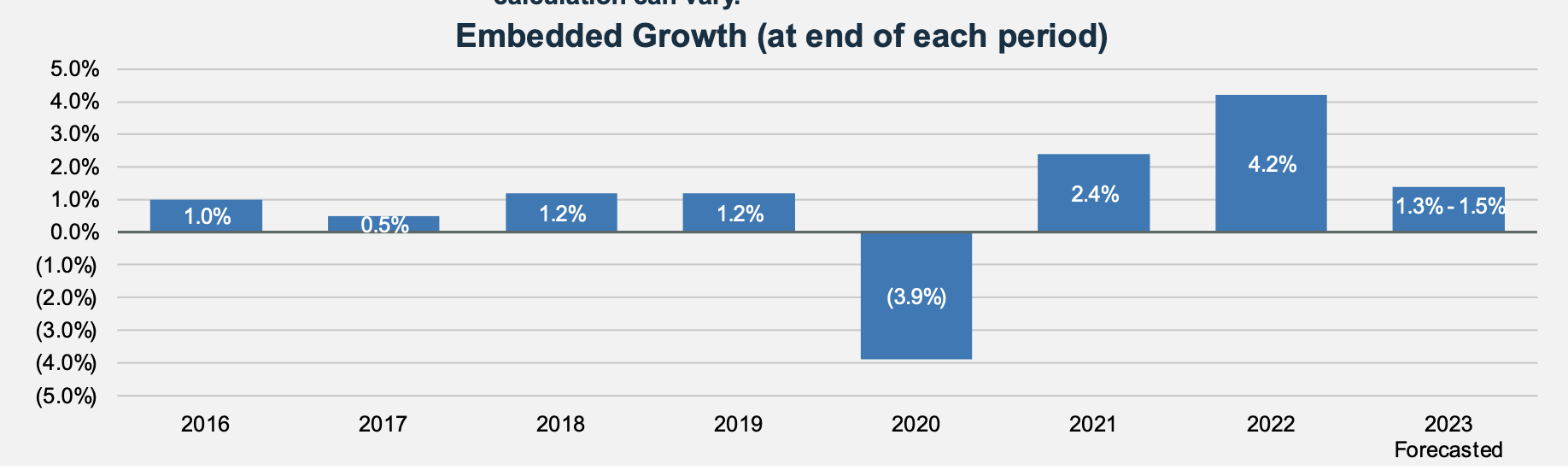

As we take into consideration subsequent yr, there needs to be a tailwind from re-leasing to the 54% of tenants who renew. In mixture, its leases are 0.8% beneath the market price. That is considerably lower than the 5.1% final yr, which is why renewal lease charges have been robust this yr. Nonetheless, this could help additional progress in 2024. Certainly, simply primarily based on the place the corporate is exiting the yr, if it does nothing else, progress needs to be 1.3-1.5% in 2024. That is according to slowing, however nonetheless optimistic progress.

EQR

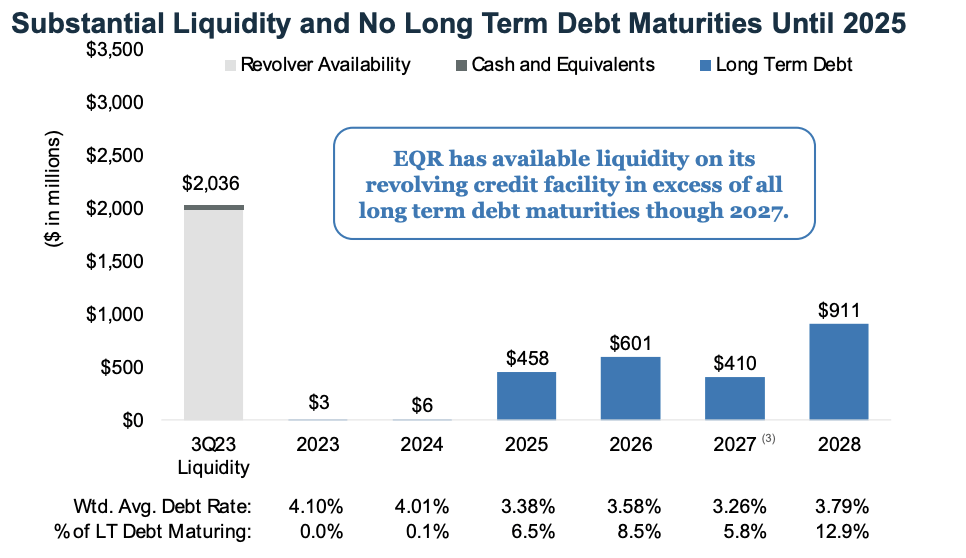

Lastly, EQR has a rock stable steadiness sheet. Even with greater charges, internet curiosity expense fell 5% to $68.9 million final quarter as mortgage notes have fallen by $300 million this yr. It has simply 4.2x internet debt to EBITDA. Its debt additionally carries an 8.3 yr common maturity, and there are not any materials maturities till 2025, largely insulating money movement from greater rates of interest.

EQR

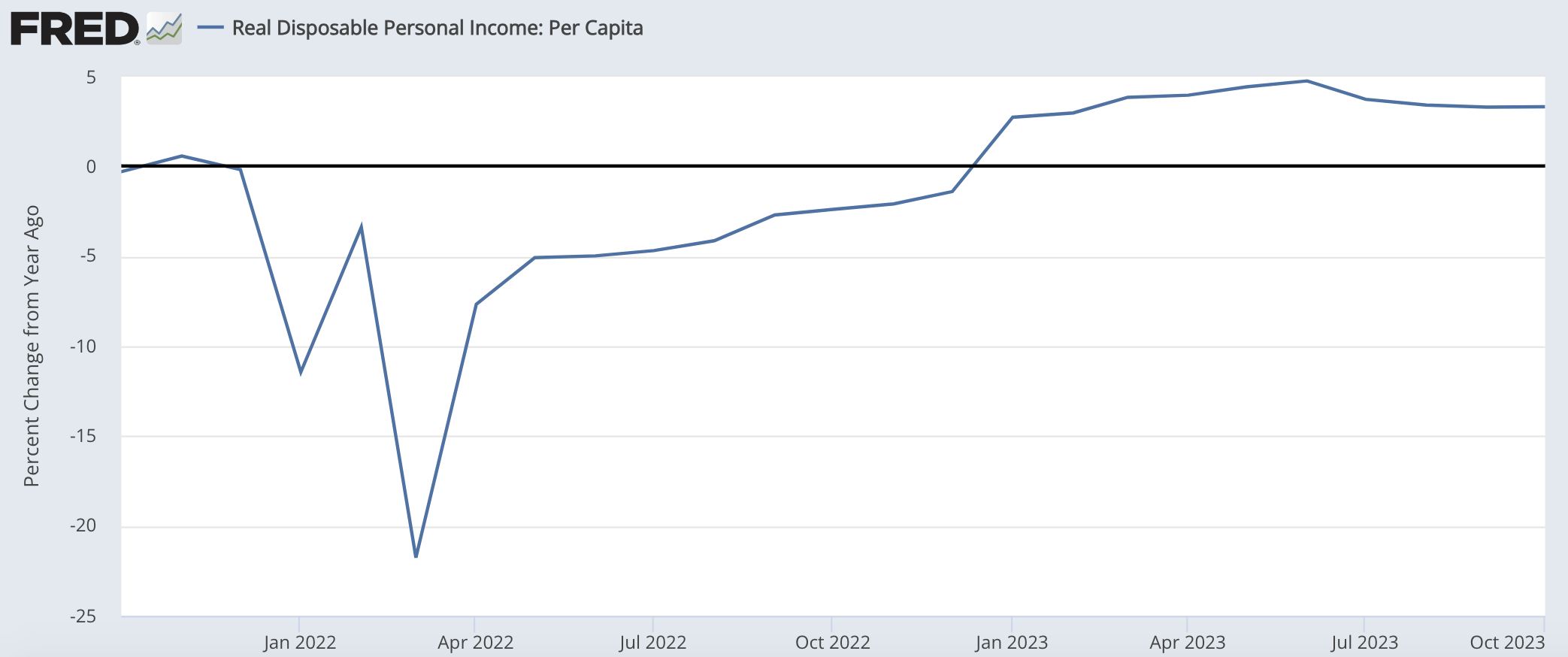

EQR affords a 4.5% yield, and it supplied 6% dividend progress this yr with a $2.50 payout. As we glance out to subsequent yr, you will need to do not forget that actual disposable earnings continues to be rising, which ought to help rental progress. Whereas the San Francisco market could stay weak, we’re seeing stronger ends in different key EQR markets, and provide in these markets ought to keep pretty muted.

St. Louis Federal Reserve

I do anticipate progress to sluggish as there’s much less hire catch-up. One optimistic tailwind is that internet unhealthy debt expense is operating at 1.27% from 0.5% pre-COVID, partially as a result of prolonged foreclosures processes. As these work by in 2025, EQR ought to be capable of cut back unhealthy debt expense and start incomes income on these models once more. Even closing simply half the hole may improve FFO by 0.4%. Given a 1.3% exit progress price, 0.4% from unhealthy debt expense, 1-2 unit progress, and assuming 1-2% hire progress, lower than the three% seen earlier than the pandemic. EQR ought to develop FFO by 4-5%, given modest working leverage.

Contemplating its robust steadiness sheet, I anticipate dividend progress to fulfill or barely exceed FFO progress, or are available at 5-6%. With a beginning 4.5% yield, that’s a pretty mixture according to a ~10% complete return. Given the structural tightness within the housing market given the shortage of building final decade, I do anticipate rents to rise quicker than inflation over time, enabling ongoing 5-7% dividend progress. At this worth, earnings progress buyers should buy a robust, safe firm with double-digit medium-term return prospects. I proceed to love EQR. Absent a renewed rise in long-term charges, which might weigh on actual property shares, I see upside in shares over the subsequent yr and can be a purchaser as much as $65.