Hiroshi Watanabe

In the middle of stamping out each flickering brush fireplace on Wall Road over the previous couple of years, the Fed has engineered not less than two backdoor QEs—one within the type of giant financial institution bailouts and one other in the type of beneficiant In a single day Repo Facility subsidies. As well as, the Fed has pumped up investor confidence on Wall Road by repeatedly promising (although not but delivering) someplace between 3 to five charge cuts this 12 months.

Whereas among the Fed’s strikes had been telegraphed far upfront—like quantitative tightening and elevating rates of interest—different maneuvers that had simply as a lot, if no more, affect on the inventory market had been performed both subtly, or in close to secrecy.

The Biden administration has additionally gotten into the sport by promoting off almost half of the US oil reserves. This coverage didn’t simply inject additional synthetic liquidity into the financial system, it distorted your complete vitality panorama.

The Fed’s Trillion Greenback Subsidies for the In a single day Repo Market

One of many very important organs within the physique of our nation’s financial system is the in a single day reverse buy facility, which offers a form of buying and selling publish for short-term repurchase agreements. Massive monetary establishments, often banks, borrow cash within the type of Treasuries in a single day and pay the mortgage again very first thing within the morning along with prorated curiosity, often on the Federal Funds charge.

Many of the debtors and lenders are monetary establishments. Normally, the Fed performs a minor function on this facility.

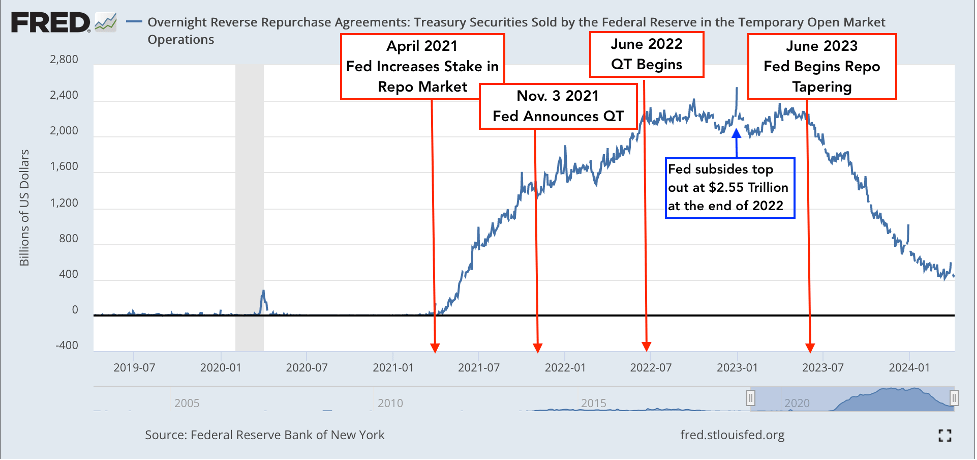

Fig. 1

In a single day Repurchase Agreements: Treasury Securities Bought by the Federal Reserve (St. Louis Fed)

On March 3, 2021, the Fed had simply $500 million of Treasuries within the in a single day reverse buy market earlier than it flooded the operation with liquidity. The next month, the Fed started generously subsidizing this monetary equipment. As you’ll be able to see from the chart above, this infusion of liquidity crescendoed till it reached $2.55 trillion by December of 2022.

It’s seemingly the Fed supposed to buffer no matter shock quantitative tightening would possibly induce within the inventory market. Nonetheless, this unannounced back-door QE seemingly distorted the market by inducing the surge in inventory costs that started within the fall of 2022, simply because the Fed’s infusion of liquidity was reaching its zenith.

The Charge Lower Mirage

The Fed’s oft repeated guarantees of charge cuts in 2024, whereas clearly supposed to stabilize the inventory market and general financial system, may seemingly change into a mirage.

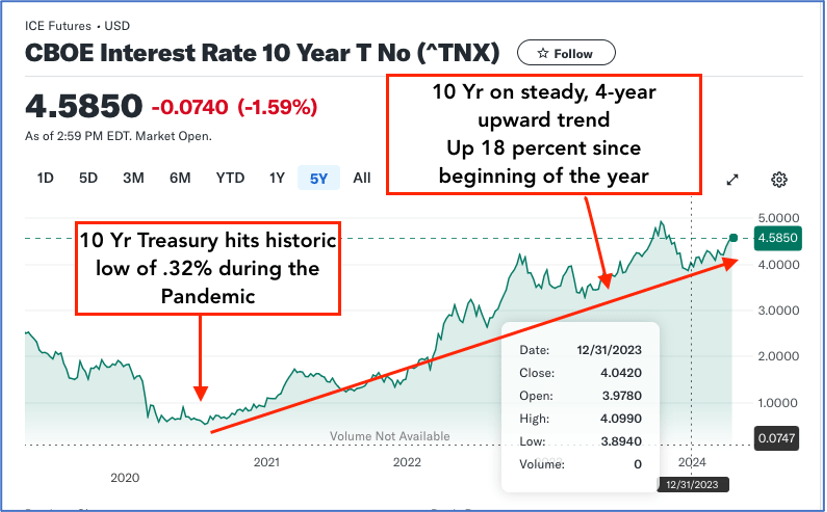

The mere proven fact that the US authorities is promoting a file quantity of Treasuries to finance a record-high finances for 2024 has already pushed the 10-12 months Treasury 18 p.c increased (3.9%-4.6%) for the reason that starting of the 12 months. This could come as no shock, as the ten 12 months is solely following by means of on a 4-year pattern line that started through the pandemic.

Fig. 2

Finance.Yahoo

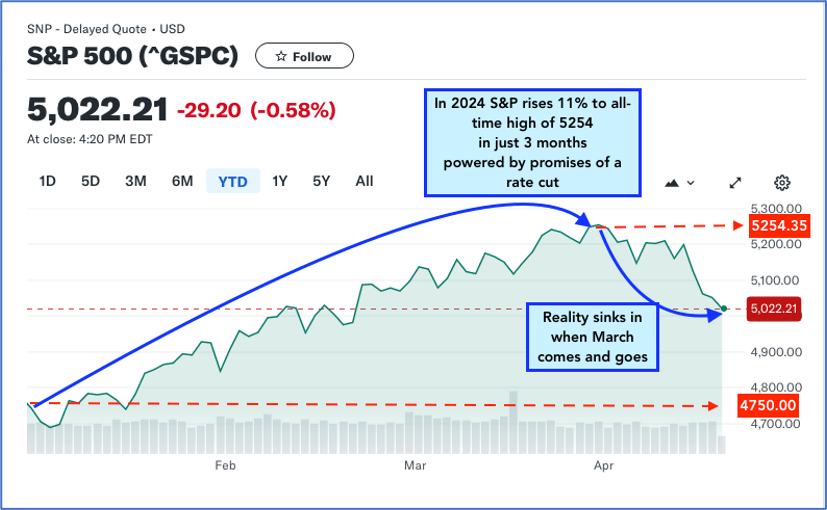

In the meantime, the inventory market soared 11% in simply 3 months from January 2024, seemingly in anticipation of additional liquidity. However when March got here and went with not one of the promised charge cuts, it seems actuality sank in because the S&P slid 232 factors as proven within the chart beneath.

Fig. 3

Finance.Yahoo.com

Financial institution Bailouts of April 2023

When Silicon Valley Financial institution, Signature Financial institution, and several other different giant banks geared towards enterprise capitalists veered off into uncharted territory to discover a brand new enterprise mannequin, one can solely marvel in the event that they assumed the Fed would rescue them if their high-risk gambit instantly unraveled.

On this distinctive enterprise mannequin, these banks inspired their purchasers to deposit billions of {dollars} into their accounts to create a big pool of cash that different financial institution purchasers may draw upon to both develop their companies or fund new ones. There was one obtrusive flaw on this banking mannequin. All deposits over $250,000 usually are not backed by the FDIC, which implies these monetary establishments had been weak to the proverbial run on the financial institution, one thing we haven’t seen for the reason that Nice Melancholy, largely due to the FDIC.

To provide some perspective, the very motive US Treasuries are in style world wide is as a result of they’re a safe solution to park billions of {dollars} with little or no danger, not like piling it into an unsecured checking account.

When the Fed lastly started quantitative tightening in March 2023, despite the fact that the disruption to the usual banks—whereby almost all deposits had been backed by the FDIC—was minimal, the disruption to the brand new banking mannequin that Signature and Silicon Valley Financial institution had embraced was extreme. A surge in demand for giant loans brought on some high-value depositors to get chilly toes and withdraw their unsecured funds from the financial institution. The sudden increased demand for giant loans, shortly adopted by even bigger withdrawals, brought on an old school run on these enterprise capitalist-style banks. As a result of the quantities concerned had been so big, the Fed feared that in the event that they didn’t intervene, the contagion may spill out into your complete banking sector, and from there, to the nationwide and even international financial system.

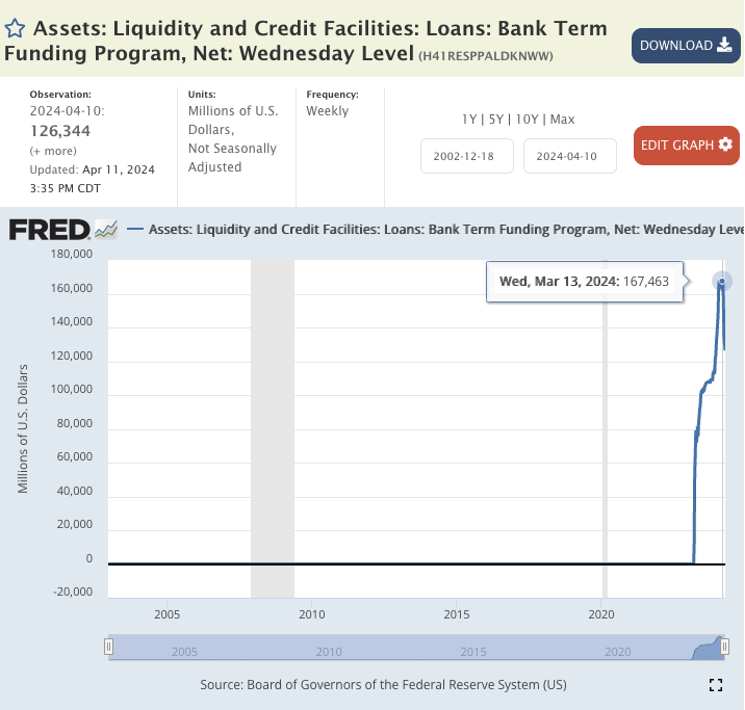

So, with little to no concern that they had been as soon as once more rewarding malfeasance within the banking sector, the Fed rushed to the rescue with a program referred to as the Bank Term Funding Program (BTFP) which lasted from March 15, 2023 to March 11, 2024.

In March 2024, simply earlier than the Fed ended this system, the excellent steadiness of the BTFP was $167 billion. To date, the entire banks that tapped into the BTFP have had no hassle repaying their loans. However since these loans have one-year phrases, most of them are nonetheless excellent. Whether or not the entire banks that tapped into this pool of cash at the moment are solvent stays to be seen.

Fig. 4

Financial institution Time period Funding Program (St. Louis Fed)

Many of those banks will merely roll over their loans, and that is the very motive the Fed has been promising charge cuts. Nonetheless, the present financial local weather—cussed inflation within the housing, meals, and gas sectors; matched with excessive employment charges, a hovering inventory market, and a file quantity of federal debt that should be financed with ever-increasing volumes of Treasury gross sales—makes charge cuts extremely unlikely.

The Fed has been put within the uncomfortable place of selecting between extra financial institution bailouts that would set off hovering inflation, or maintaining inflation in examine whereas risking extra financial institution failures.

As for banks that also want a serving to hand with monetary liquidity, their lender of alternative is Federal Residence Mortgage banks (FHLBs). Nonetheless, anticipating a rush to their lending window, the FHLBs put out this sharp warning.

“…the role of FHLBanks in providing secured advances must be distinguished from the Federal Reserve’s financing facilities, which are set up to provide emergency financing for troubled financial institutions confronted with immediate liquidity challenges.

The FHLBank System does not have the functional capacity to serve as the lender of last resort for troubled members that could have significant borrowing needs over a short period of time.”

This implies if banks are in hassle and wish a lender of final resort, they have to go to the dreaded Fed Low cost Lending window. Banks try to avoid this situation for quite a few causes, the main one being that the transfer seems determined to their banking colleagues and purchasers which may trigger additional harm to their establishment. The banks worry that the stigma of tipping their hand by going to the Fed’s Low cost Lending Window may ship their institutions right into a monetary tailspin. To date this has not occurred, however there are eleven months forward for such situations to play out.

The upshot is that this sugar rush of a back-door QE program offered extra synthetic stimulus to the inventory markets and sure performed a giant function within the run-up from the summer time of 2023 thus far. However there isn’t any means of figuring out what the ultimate results of this program can be till subsequent 12 months.

Promoting Off The US Strategic Oil Reserves

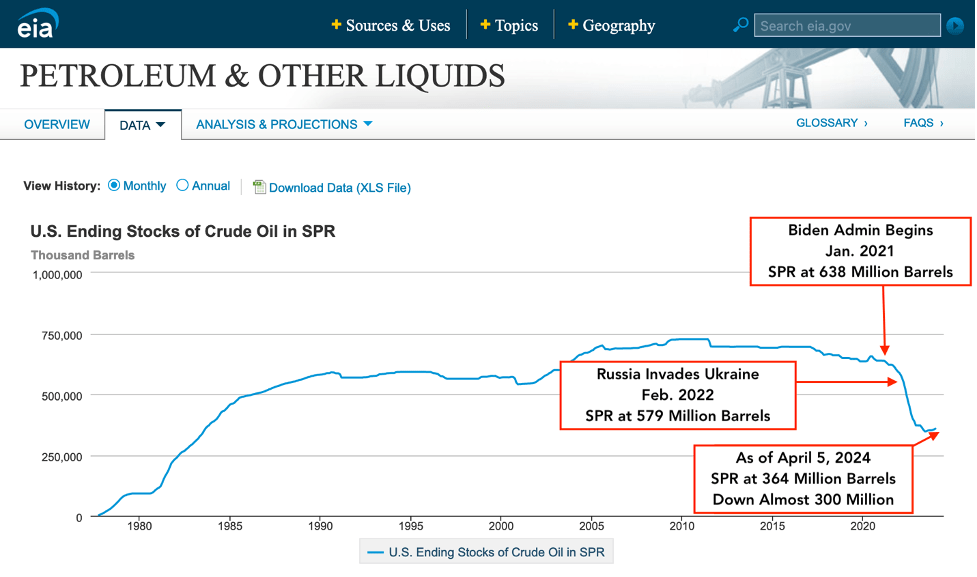

When Russia invaded Ukraine, the US Strategic Oil Reserves had already dropped by 59 million barrels. Over the subsequent few years, because the Biden administration slapped sanctions on Russia, it bought off greater than 40 p.c of US oil reserves to make up for the Russian oil that was presumably to be taken off the worldwide market.

Fig. 5

US Vitality Data Administration (EIA)

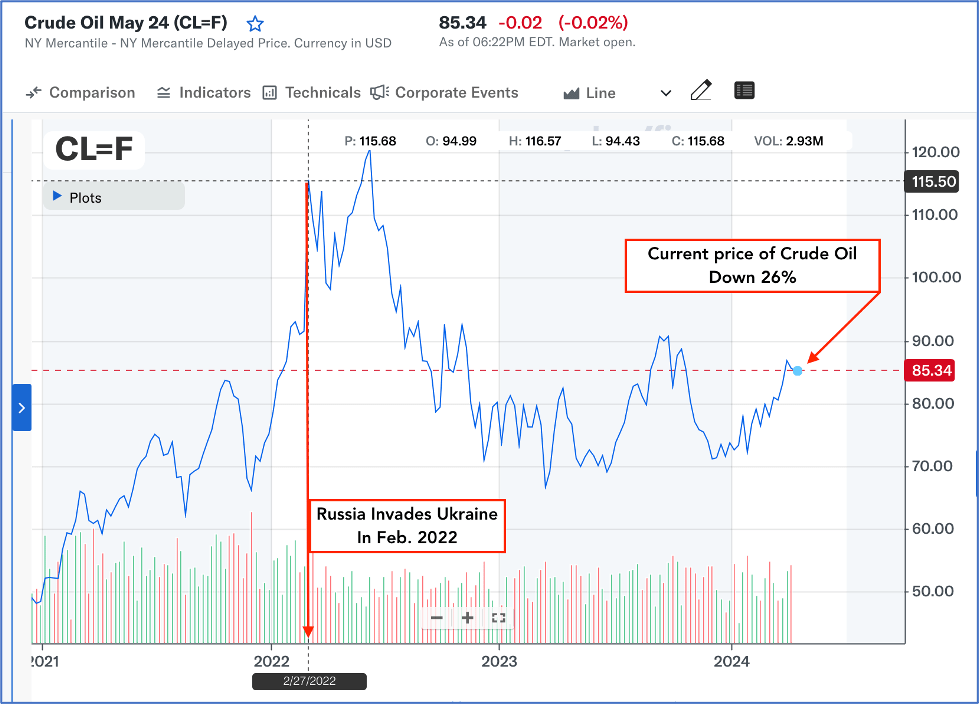

This maneuver whipsawed the value of oil. Crude Oil bought at $120 a barrel in June 2022, however over the subsequent three quarters, it dropped 45% to a low of $66 per barrel in March 2023. The federal government started changing the oil the next month. Since then, the value has ticked as much as $85 per barrel.

Fig. 6

Crude Oil NY Mercantile (Finance.Yahoo.com)

This interference within the international gas markets has seemingly performed a job in depressing the sale of EVs, which had been significantly decrease than anticipated in 2023 and 2024.

This coverage created reduction for shoppers on the gasoline pump whereas many People proceed to complain about rising costs. Nonetheless, the value drop was synthetic. Now that the coverage is in reverse, it’s seemingly contributing to these cussed inflation experiences.

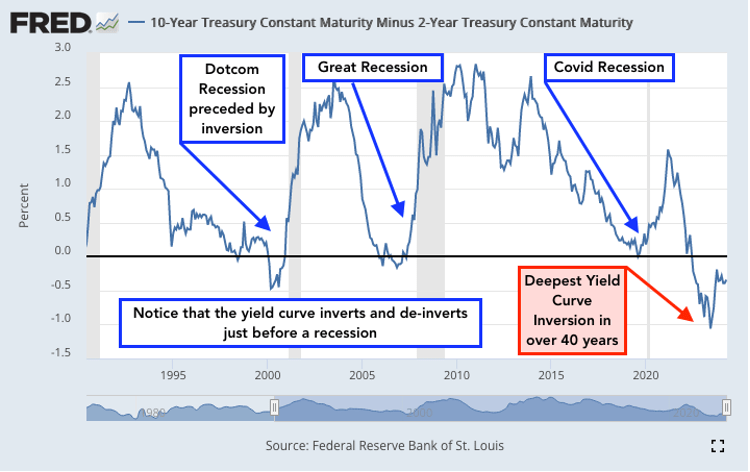

The Yield Curve Inversion Chart Is Flashing Crimson

Whereas many monetary analysts are respiration a sigh of reduction and declaring a gentle touchdown for the financial system, the Yield Curve Inversion charts are telling a unique story. Probably the most dependable recession indicators obtainable, a yield curve inversion is what occurs when short-term Treasuries pay a better charge of curiosity than long-term Treasuries as institutional traders pile into the long-term bonds, particularly the 10-year, to protect their clientele’s wealth earlier than an anticipated recession. This sturdy demand for long-term bonds drives up the value, which drives down the rates of interest.

Fig. 7

10 yr T and a pair of yr T Yield Curve Inversion Chart (St. Louis Fed)

Quick-term Treasury Payments Nonetheless the Most secure Guess

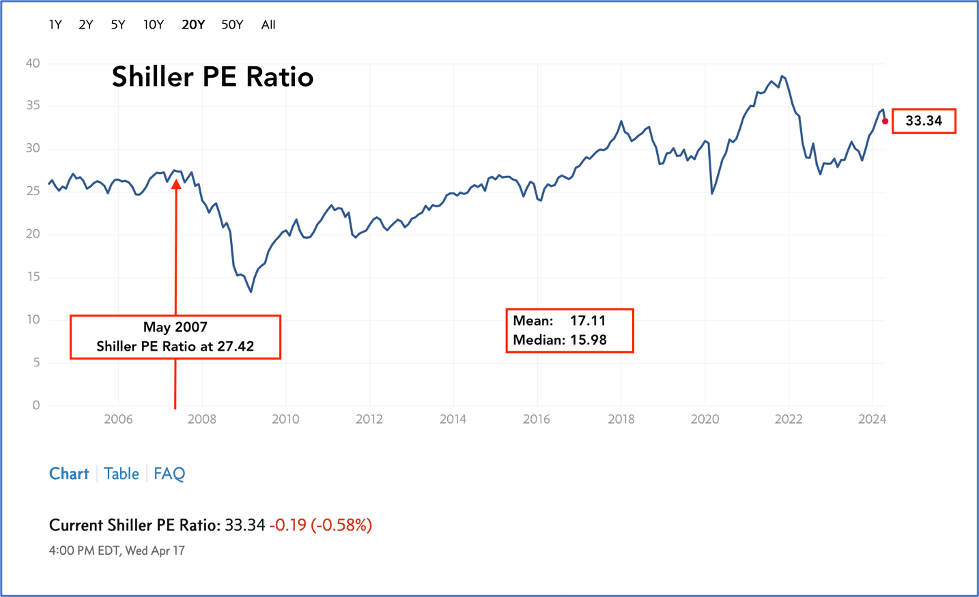

In February, I predicted that the Fed would likely back-pedal on rate cuts this 12 months for quite a few causes, together with a file variety of US Treasuries bought at public sale to finance a hovering authorities finances. Whereas the inventory market remains to be offering spectacular returns, it’s over-heated in line with the Shiller PE Ratio. At 33.34 it’s roughly double each the imply and the median of the index, which stand at 17.11 and 15.98 respectively. It is usually significantly increased than the 27.42 that it was in Could of 2007, simply earlier than the onset of the Nice Recession.

Fig. 8

Multpl Monetary and Financial Knowledge

Contemplating the danger components, getting a assured 5% or so from short-term Treasury payments is much safer than playing with one’s life financial savings on the inventory market, which is taking up the texture of a on line casino.

The danger think about short-term charges is missed alternatives on the inventory market if it resumes its meteoric rise. Or lacking out on locking in these present charges in a longer-term Treasury bond ought to the Fed lastly make good on its promise to chop rates of interest.

Abstract

The Fed’s repeated interference within the inventory market has not simply made the monetary panorama tough to foretell, it has probably distorted the markets to the purpose of destabilization. For that reason, one of many few protected investments is short-term Treasuries which at present pay a good 5% or so, and can enable traders to shortly unencumber their cash ought to the inventory market drop and current shopping for alternatives.