Douglas Rissing

On January 31, the Treasury Department announced a dramatic rise within the variety of Treasuries it plans to public sale over the primary quarter of 2024. This implies a internet enhance of $300-$350 billion in privately-held provide, in response to the US Division of the Treasury.

This motion will doubtless put upward stress on rates of interest even because the monetary markets predict charge cuts. However the Fed has little alternative. The federal government’s finances has soared to file highs and extra tax cuts are on the horizon. There may be little will on both aspect of the Congressional aisle to gore political sacred cows to get our nation’s fiscal home so as.

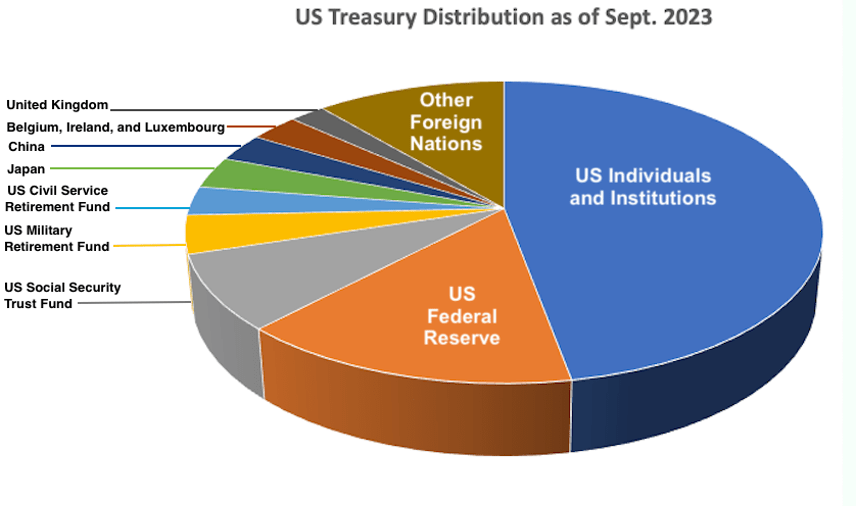

The place Treasury Demand Is Coming From

The Treasury Division is relying on US banks, institutional buyers, the US authorities itself, and different home consumers to vacuum up this extra provide, a necessity if rates of interest are to remain degree. There may be little likelihood our largest overseas clients shall be rising their Treasury purchases over the approaching yr. We must always anticipate the other.

Fig. 1

US Treasury Division

Japan’s Financial Outlook

The Financial institution of Japan recently announced it plans to reverse 1 / 4 century of Quantitative Easing over the approaching yr. That is doubtless in response to inflation, which jumped to 7.3% final yr in January 2023. Since then, headline inflation in Japan has dropped to three.3% as of October, however inflation within the meals and beverage sector continues to be operating sizzling at 8.6%. Lowered native spending energy may put downward stress on Japan’s economic system.

Even small incremental charge will increase may trigger turmoil within the Japanese economic system as it’s the most indebted country on the planet, with a 252% debt-to-GDP.

Moreover, these charge will increase may spell bother for Japanese banks that are holding large quantities of bonds with zero, and even unfavorable rates of interest. These will shortly lose worth if charges enhance even barely, which may translate into billions of {dollars} of paper losses. Briefly, Japan’s purchases of US Treasuries are prone to proceed a two-year-long downward slide.

China’s Financial Outlook

Our second largest buyer, China, is in even worse form. China’s share of US Treasuries has already dropped from a high of 14% in 2011 to a mere 3% as of 2024. Contemplating they’re now within the throes of an enormous implosion of their actual property sector, their skill to purchase Treasuries is prone to additional dwindle over the approaching yr.

Why Fed Price Cuts Might Wind Up On The Chopping Block

This previous December, Fed Chair Jerome Powell indicated there can be three quarter-point rate cuts over the approaching yr when he claimed, “The appropriate level [of the federal funds rate] will be 4.6% at the end of 2024”

Whereas this assertion was ballyhooed on Wall Road, the Fed additionally made a cryptic prediction that the majority buyers missed. Based on the Federal Open Market Committee, inflation will doubtless attain its target of 2 percent inflation in 2026, two years from now.

Then, on January 31, the Fed introduced there shall be no rate cuts till they see progress on inflation returning to its 2% goal. Once you put these two statements collectively, the Fed appears to be warning Wall Road that the three charge cuts promised for this yr may simply be swept off the desk.

The Fed Can not Afford One other Spherical of Quantitative Easing

There is just one manner the Fed can engineer a charge lower and that’s by shopping for up a big quantity of Treasuries to create synthetic demand in a maneuver often known as Quantitative Easing. Based on the legal guidelines of provide and demand, when demand will increase and the availability stays regular, the worth goes up. Within the case of Treasuries, a better value means a decrease rate of interest.

Wall Road has come to imagine that Quantitative Easing is an “easy button” the Fed can hit anytime there’s a lot as an uncomfortable pinch within the inventory market. However the sheer measurement of the debt held by the Federal Reserve financial institution tells one other story.

Fig. 2 Federal Debt Held by Federal Reserve Banks

US Division of the Treasury

Discover within the chart above that from the primary quarter of 2009, when the Fed first launched its Quantitative Easing program, till the primary quarter of 2022, the Fed has elevated the quantity of its Treasury holdings by a whopping 1,171%. Because the introduction of Quantitative Tightening, which started in June of 2022, the Fed has introduced its holdings down a mere 14%, hardly sufficient to say victory over the matter.

To imagine the Fed can proceed to load up on US Treasuries when they’re already gorged with an enormous quantity of Federal debt, an quantity which has no precedent in historical past, is kind of presumably naïve on the a part of each the Fed and Wall Road. To place it in pedestrian phrases, Uncle Sam’s bank cards are nearly maxed out.

Within the desk of US Treasury Auctions beneath, discover the upward pattern within the quantity of Treasuries auctioned month-over-month as proven in the fitting column. These climbing numbers point out the Treasury Division’s obligation to maintain up with the US authorities finances.

Fig. 3

US Division of the Treasury

Curiosity Charges Nonetheless Trending Up

One other indication that Treasury charges are in an total upward pattern may be seen within the historic chart for the 10-12 months Treasury Be aware beneath. Ever for the reason that Fed introduced its plan to reverse Quantitative Easing on the finish of 2021, the charges have been marching steadily upward with the occasional sharp pullback, as now we have simply skilled over the previous few months. However despite the fact that the 10-year T-bill made a pointy downturn after touching 5% in October, the speed continues to be hovering above its 50-day shifting common, and nonetheless hovering above the 200-day shifting common.

Fig. 4

Finance.Yahoo Chart

Contemplating the monetary panorama, it’s puzzling as to why the Fed would promise charge cuts in 2024 when all of the financial indicators are pointing towards an involuntary charge enhance that the Fed could also be powerless to cease.

However when one places themselves within the Fed’s sneakers, it does make sense. There’s little question the Fed would very very like to chop charges within the close to future, albeit their guarantees are primarily based extra on wishful pondering than market fundamentals. Nevertheless, in the event that they have been to persuade bond buyers that charges have been extra prone to enhance than lower over 2024, that would spell catastrophe for the bond market. Such a revelation would solely encourage would-be buyers to carry off and await larger charges within the months to come back and this might ship charges hovering in a suggestions loop state of affairs.

Conversely, if Wall Road is satisfied that charges will quickly go down, bond buyers shall be motivated to reap the benefits of these present larger charges earlier than the promised decrease charges come to cross.

Treasury Secretary Janet Yellen appears to be effectively conscious of those circumstances. On January 26, she instructed there was a chance that rates of interest may settle again to the place they have been earlier than the pandemic. She then shortly adopted up with this comment. “But the strength of the economy also suggests that perhaps productivity growth and potential output growth have increased and the level would be higher.”

It seems Yellen is suggesting that, within the close to future, rates of interest may go larger. The monetary information and financial pattern strains counsel she may very well be proper.

In a previous article I instructed {that a} good hedge in opposition to this oncoming monetary uncertainty was to put money into short-term Treasuries and CDs, something between 3 months and 1 yr. I’ve not modified my stand on this regard. As a consequence of a steep yield curve inversion, charges on short-term bonds are larger than some long-term bonds.

The chance on this wealth preservation technique is that an investor may lose out on additional will increase within the inventory market. Or, if charges have been to come back down within the coming months and years, one may miss out on locking in larger charges for these curious about long-term bonds.

Abstract

A hovering US authorities finances has compelled the Treasury Division to place a historic quantity of Treasuries up for public sale over the approaching yr. This may doubtless put upward stress on rates of interest. Whereas the Fed and Treasury Secretary have been sending blended alerts relating to the place charges are heading, it’s in the very best curiosity of the Treasury Division and the Fed that the upcoming Treasury public sale is enticing to buyers.