Nuthawut Somsuk

And there have been huge upward revisions of the already sizzling readings for January.

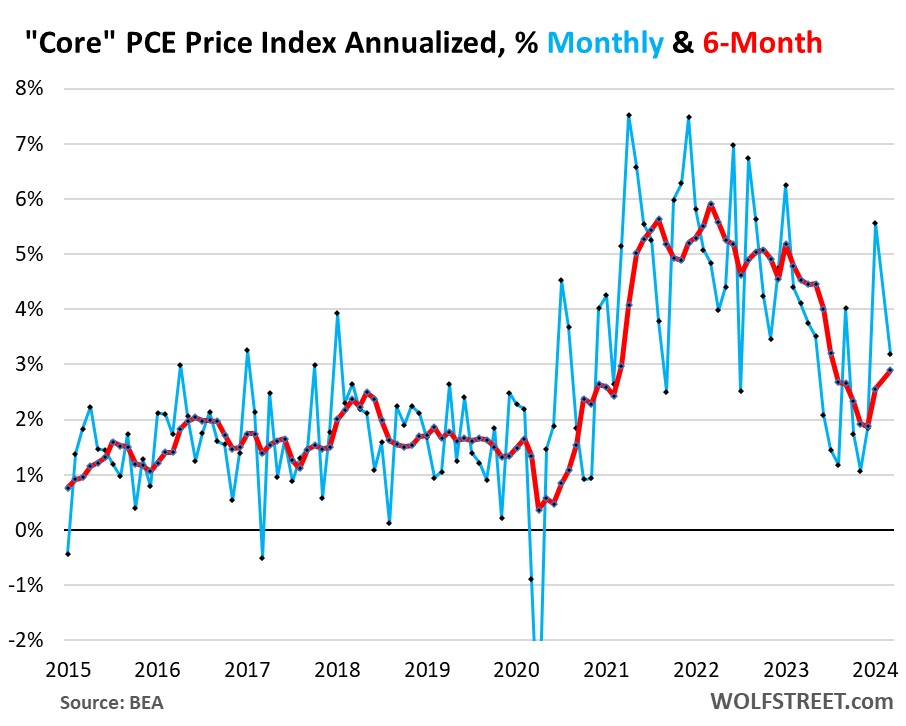

The core PCE value index, the inflation index that the Fed is targeted on and refers to on a regular basis, was revised up on Friday for January to an annualized month-to-month progress charge of 5.6% (up from the unique 5.1%) on an enormous up-revision of the index for core providers to an annualized charge of seven.9% (up from the unique 7.1%). In core providers is the place inflation is now solidly entrenched.

So in February, on high of these upwardly revised figures for January, the core PCE value index rose by 3.2% annualized from January (+0.28% not annualized), in accordance with the Bureau of Financial Evaluation on Friday. This pushed the six-month annualized core PCE value index to 2.9%, the very best since July.

Powell cites this 6-month measure (purple within the chart under) on a regular basis as a result of it reveals the current pattern higher than the month-to-month readings (blue), that are tremendous risky, and the year-over-year readings, that are too sluggish in reacting to altering tendencies. The Fed’s goal is 2%.

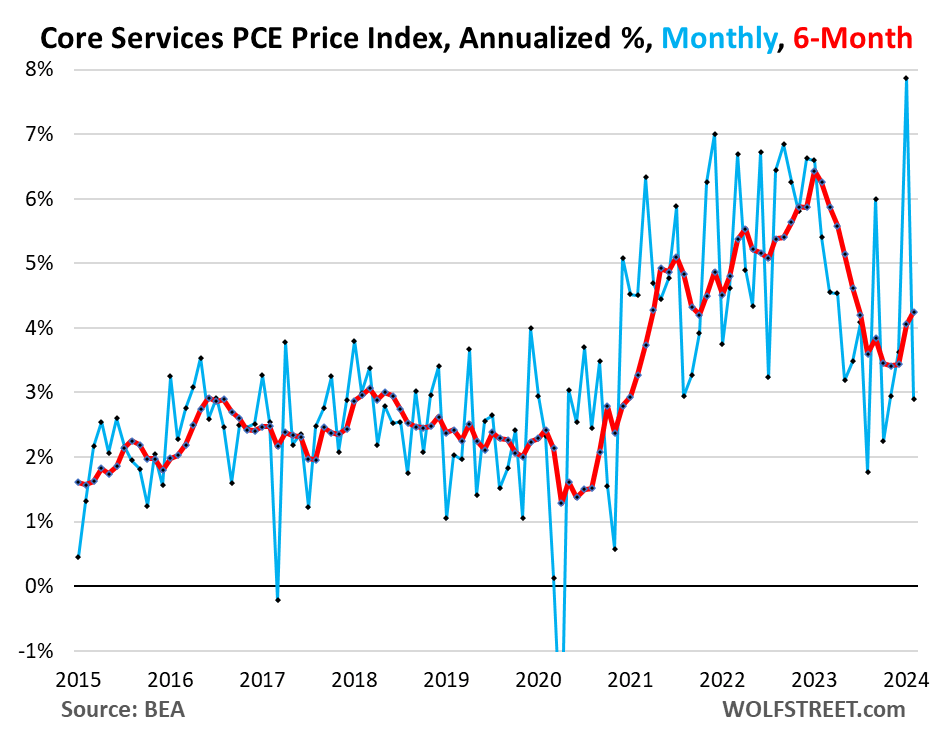

Core Providers PCE value index is the place the motion is. Power costs plunged since mid-2022, although they’ve come up once more just lately, and sturdy items costs dropped, and people have produced the cooling inflation charges we noticed final 12 months.

However core providers inflation – providers with out power providers – has remained at excessive ranges and has began to re-accelerate. Core providers is the place nearly all of customers spending goes. And Fed audio system have mentioned this subject endlessly.

The horror present got here with the January studying of “core services.” Within the studying launched a month in the past, the PCE value index for core providers spiked to 7.1% annualized in January from December, the worst month-to-month leap in 22 years. On Friday, this was upwardly revised to 7.9%.

In February, the studying of core providers rose by 2.9% annualized (blue line within the chart under). And the 6-month studying rose by 4.25% annualized, the very best since June 2023.

For 5 months within the second half final 12 months, the core providers index had gotten caught round 3.5%, which had triggered the dialogue about sticky providers inflation. However core providers inflation then received unstuck and has ratcheted larger.

Within the month-to-month readings (blue) since August 2023, we see larger highs and the upper lows. That is when the pattern modified, however it was exhausting to see initially as a result of enormous volatility. Now it turns into clearer:

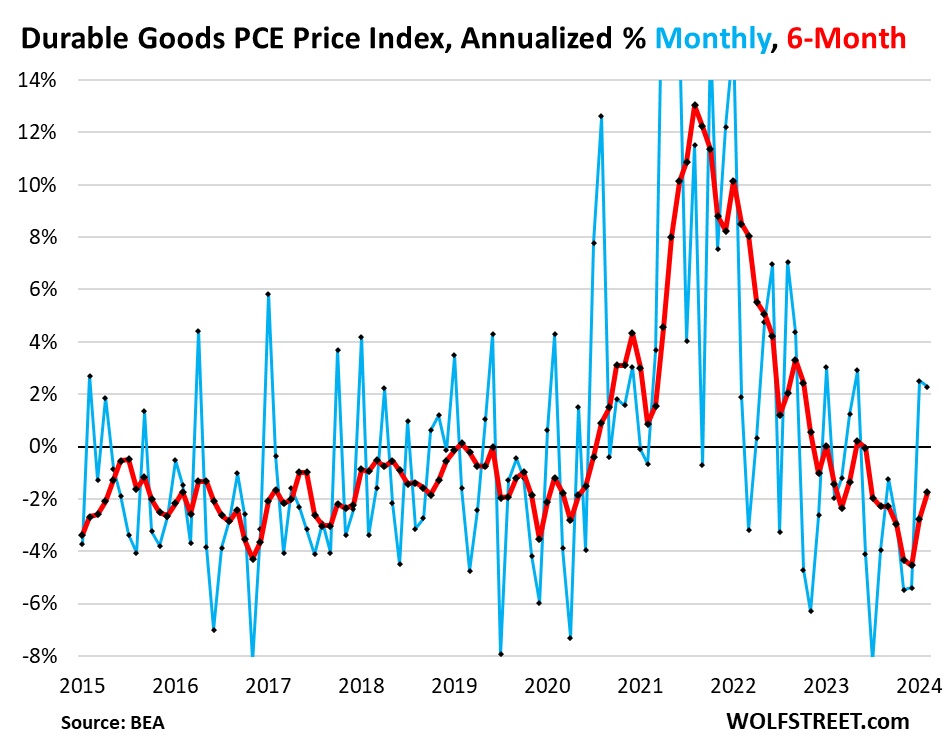

Sturdy items PCE value index rose in February by 2.8% annualized from January, the second month in a row of optimistic readings, after an enormous dive into the adverse (blue within the chart under). This raised the 6-month index to -1.7% (purple).

What we’re beginning to see is that the massive deflation in sturdy items has seemingly ended, and sturdy items value developments are actually normalizing, which removes a few of the counterbalance to sizzling inflation in providers.

Sturdy items pricing is what we’re going to look at very fastidiously. It’s sturdy items and power that induced the massive and really welcome cooling of inflation final 12 months. However power prices have been rising for months, and now sturdy items are beginning to grow to be a priority once more.

The 7 Core Providers Classes

Core providers are grouped into seven PCE value indices. The month-to-month knowledge in these classes of core providers could be super-volatile (blue within the charts under), so we’ll concentrate on the six-month annualized readings, which iron out this volatility and present the current tendencies (purple within the charts under).

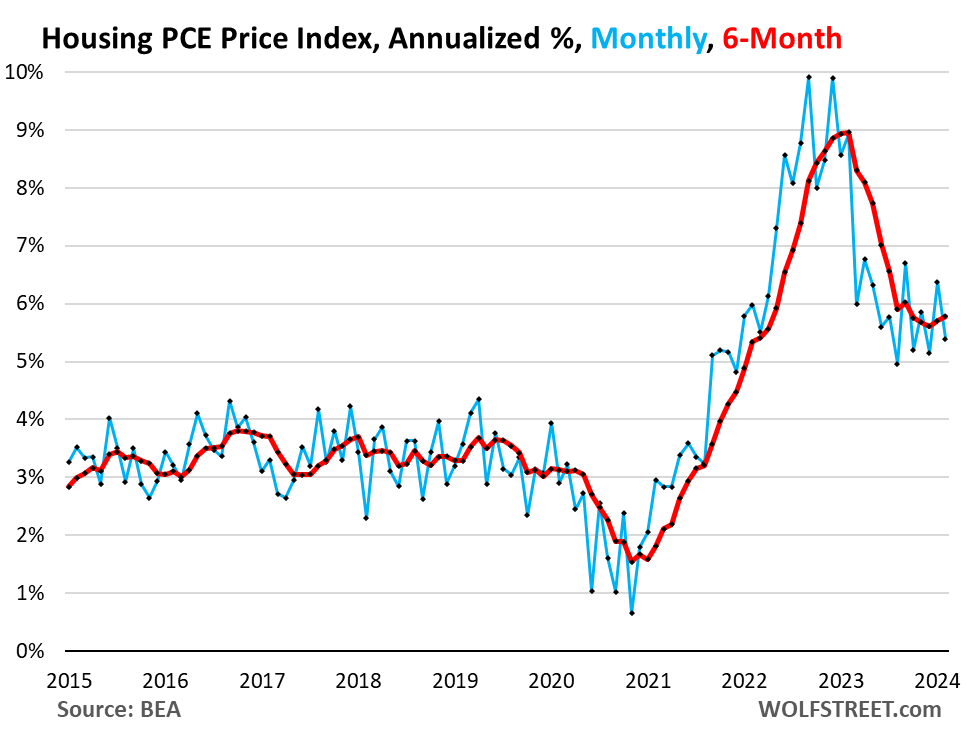

Housing, 6-month annualized: +5.8% in February, having hovered just below 6% since August 2023. The stickiness of housing inflation has stunned numerous individuals.

The housing index is broad-based and contains elements for hire in tenant-occupied dwellings; imputed hire for owner-occupied housing, group housing, and rental worth of farm dwellings.

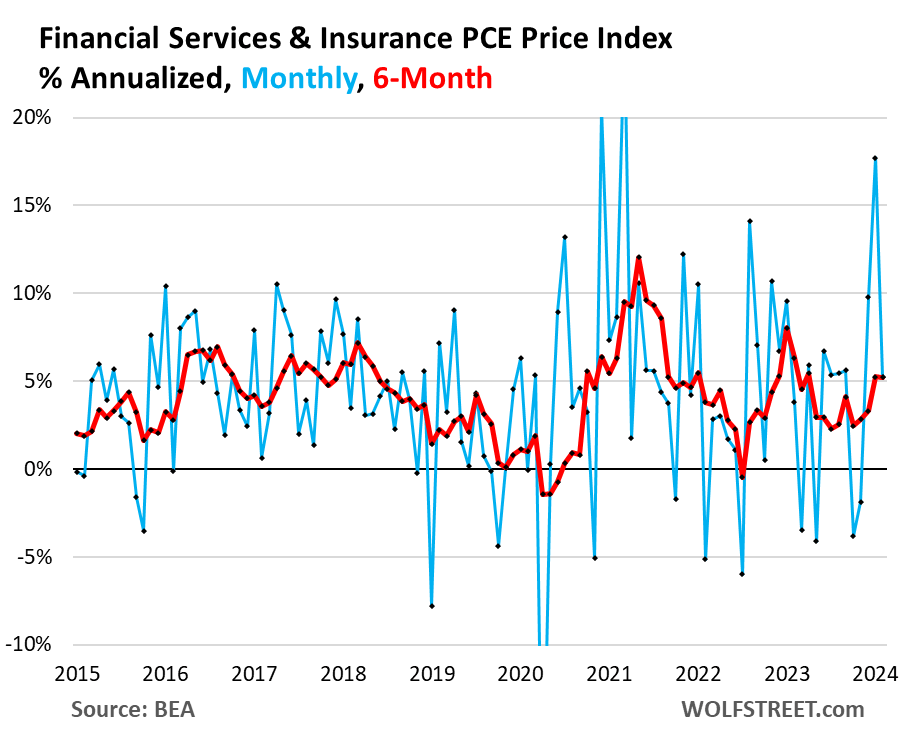

Monetary Providers and Insurance coverage, 6-month annualized: +5.2%.

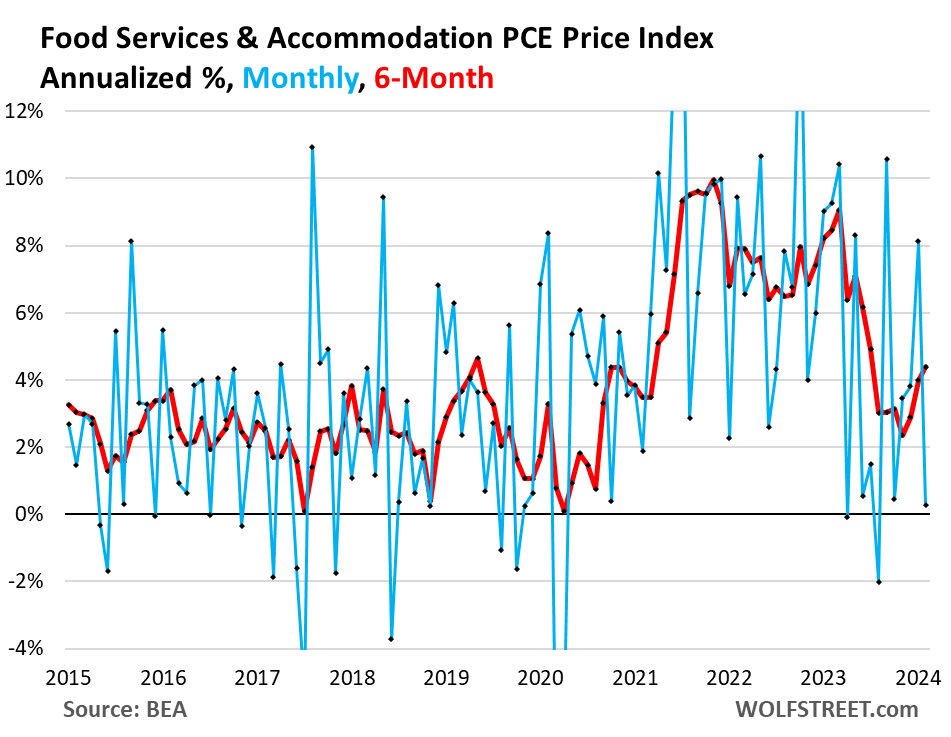

Meals providers and lodging, 6-month annualized: +4.4%

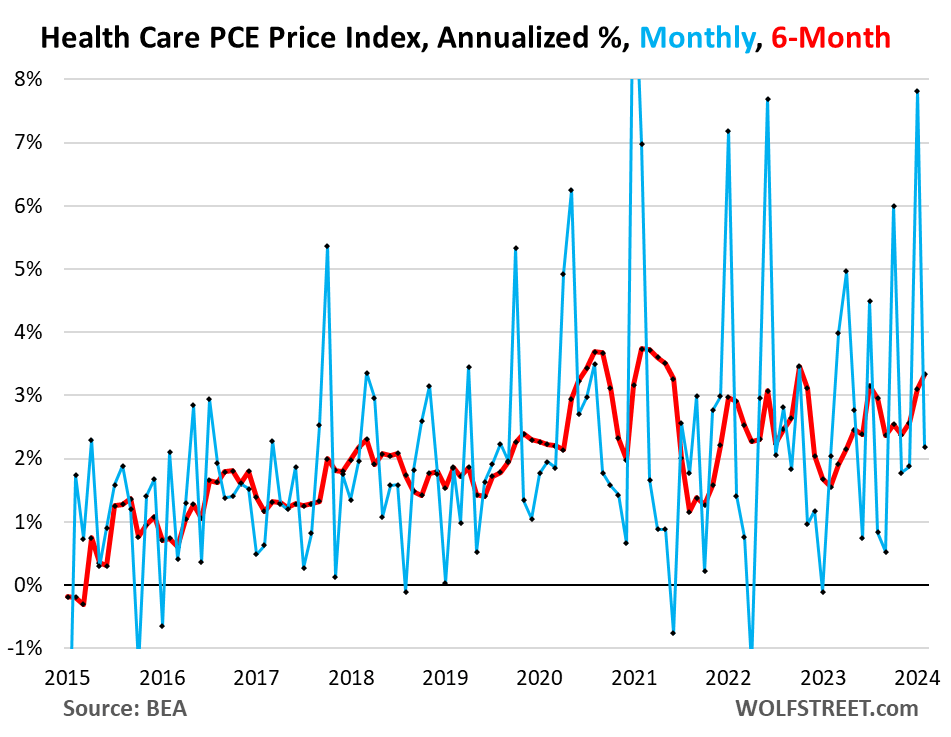

Well being Care, 6-month annualized: +3.3%.

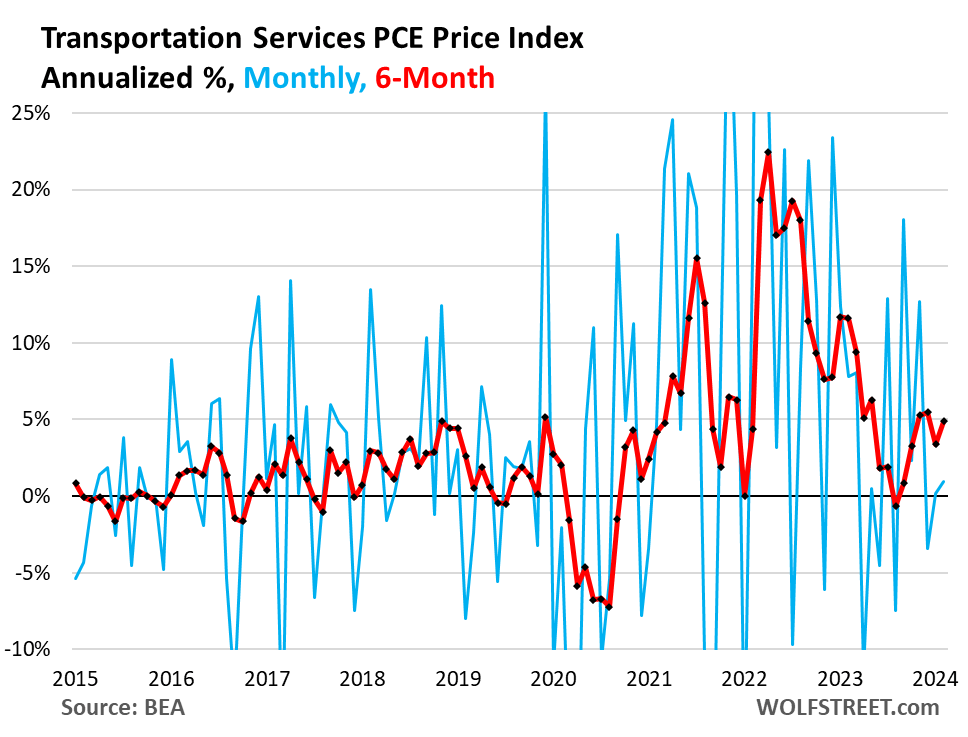

Transportation providers, 6-month annualized: +4.9%.

Consists of motorized vehicle providers, corresponding to upkeep and restore, automobile and truck rental and leasing, parking charges, tolls, and public transportation from airline fares to bus fares.

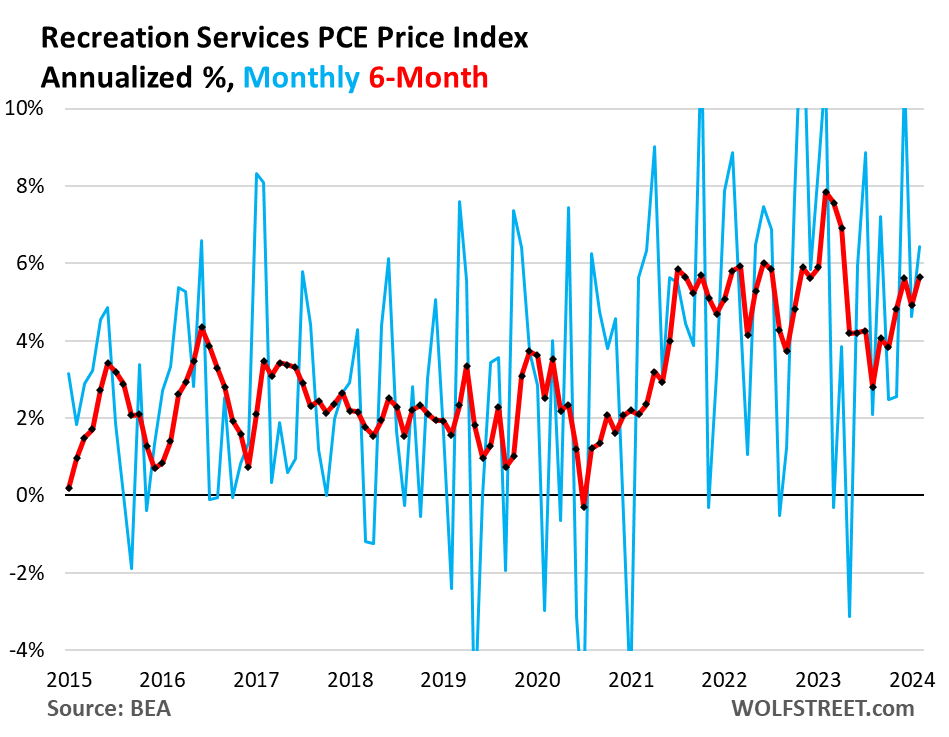

Recreation providers 6-month annualized: +5.7%.

Consists of cable, satellite tv for pc TV and radio, streaming, live shows, sports activities, films, playing, vet providers, package deal excursions, restore and rental of audiovisual and different gear, upkeep and restore of leisure autos, and so on.

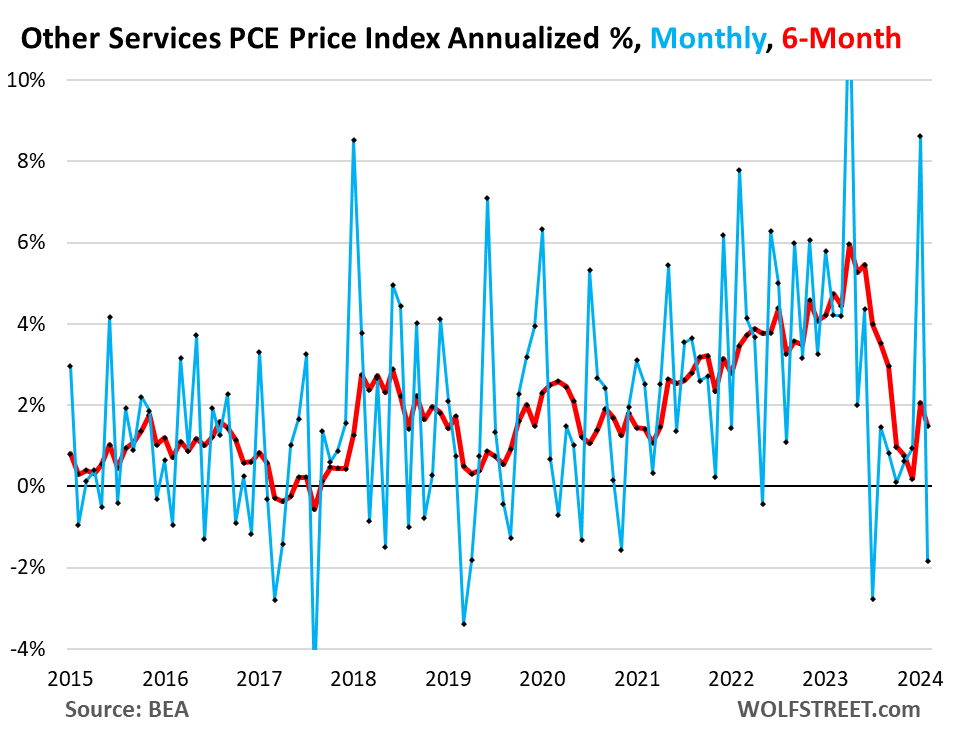

Different providers, 6-month annualized: +1.5%.

An enormous assortment of different providers, together with broadband, cellphone, and different communications; supply; family upkeep and restore; transferring and storage; schooling and coaching throughout the board; skilled providers, corresponding to authorized, accounting, and tax providers; union dues, skilled associations dues; funeral and burial providers; private care and clothes providers; social providers corresponding to houses for the aged and rehab providers, and so on.

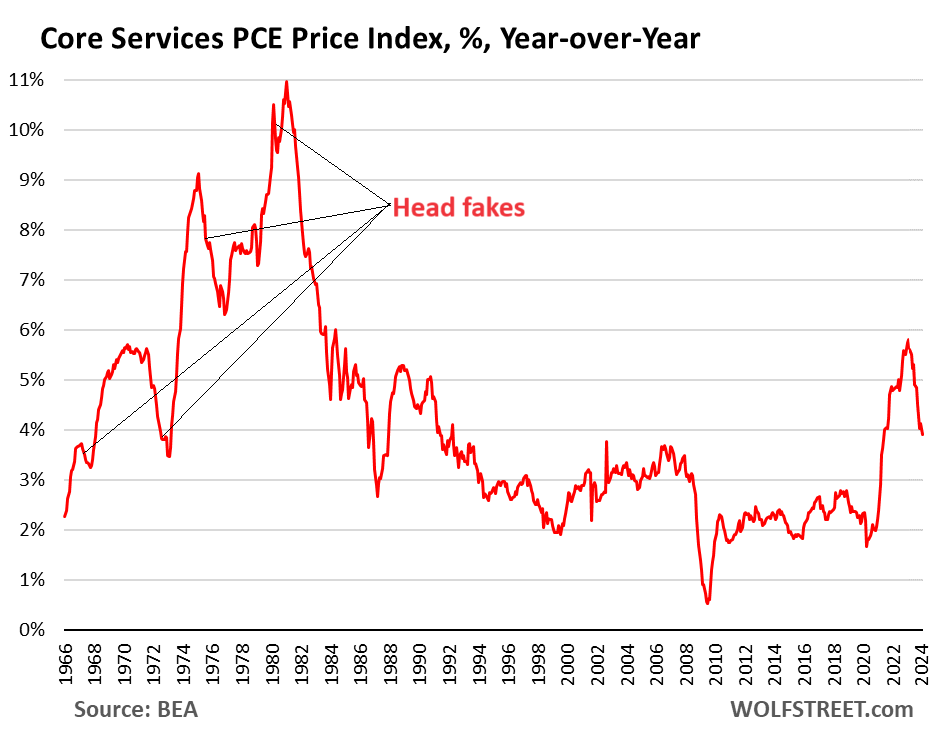

The core providers inflation head fakes final time

Final time core providers inflation of this magnitude and better occurred – within the Nineteen Seventies and Nineteen Eighties – there have been clear indicators that inflation was cooling sharply, that the excessive rates of interest had pushed inflation again down, which induced the Fed to ease, then the core providers inflation resurged, and the Fed jacked up charges even additional.

So that is the year-over-year “core services” PCE value index which excludes power and the direct results of the 2 oil value shocks on the time. Powell has talked about the chance of being misled by head fakes a couple of instances to assist the Fed’s wait-and-see mode.

Editor’s Observe: The abstract bullets for this text had been chosen by Searching for Alpha editors.