da-kuk

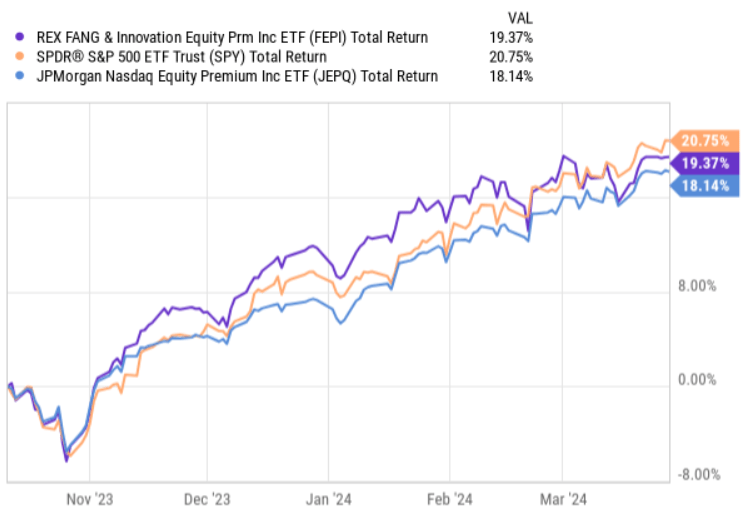

REX FANG & Innovation Fairness Premium Earnings ETF (NASDAQ:NASDAQ:FEPI) is a comparatively contemporary lined name ETF that was established again in November, 2023.

For the reason that inception, it has managed to maintain up with the well-performing S&P 500 delivering engaging distribution earnings from the written choices.

Ycharts

Throughout this time interval, FEPI has even barely outperformed the extra fashionable JPMorgan Nasdaq Fairness Premium Earnings ETF (NASDAQ:JEPQ), which carries some options that correlate with these of FEPI.

Regardless that we would not have a lot to evaluate from the FEPI’s historic knowledge given its current inception date, we will nonetheless check out the underlying mechanics of FEPI and see how the ETF might match into investor portfolios.

The construction

At its core, FEPI is a standard lined name ETF, which tracks a particular universe of shares, whereas promoting out of the cash calls to seize earnings.

The expense ratio is at 0.65%, which is kind of consistent with what we will discover within the total lined name ETF area. It isn’t low-cost neither is it costly.

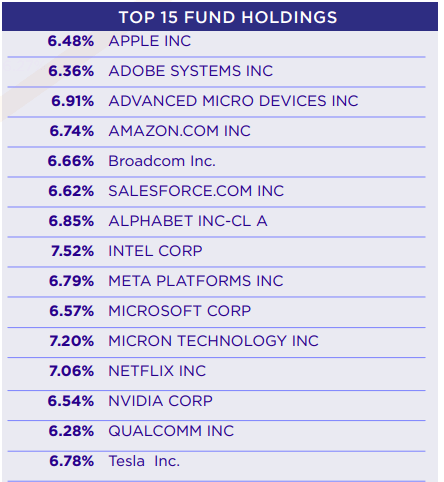

What’s somewhat FEPI particular is the pattern of shares it tracks or holds because the underlying investments towards which the calls are bought. The publicity right here is generally within the main tech corporations that represent notable share of the S&P 500 and the Nasdaq 100.

FEPI truth sheet

As we will see within the chart above, the High 15 (which is comprised of large-cap tech firms) clarify all the holdings base of FEPI.

Furthermore, it’s price underscoring the distribution amongst these High 15 names. Reverse to most different lined name ETFs like JEPQ or fashionable indices such because the S&P 500 and the Nasdaq 100, FEPI’s portfolio is structured on an equal-weight foundation, thereby avoiding extreme focus in couple of firms which have exhibited robust momentum of their market cap ranges.

By way of the lined name programme, there may be nothing that deviates from the normal strategy inside different related ETF automobiles:

- Length of written calls is normally certain by 30 days.

- FEPI doesn’t promote within the cash or on the cash calls.

- The decision strikes are normally comparatively removed from the underlying inventory value (albeit, the Administration has the luxurious to maneuver right here by assuming tactical bets relying available on the market situations and the general alternative).

Thesis

Now, as soon as we’ve established a foundation (i.e., how FEPI is structured and the way the chance and return drivers appear to be), I’ll elaborate on two distinct benefits of FEPI that would encourage traders going lengthy the ETF.

The first one is the improved yield potential, which stems from the comparatively concentrated positions in solely 15 firms.

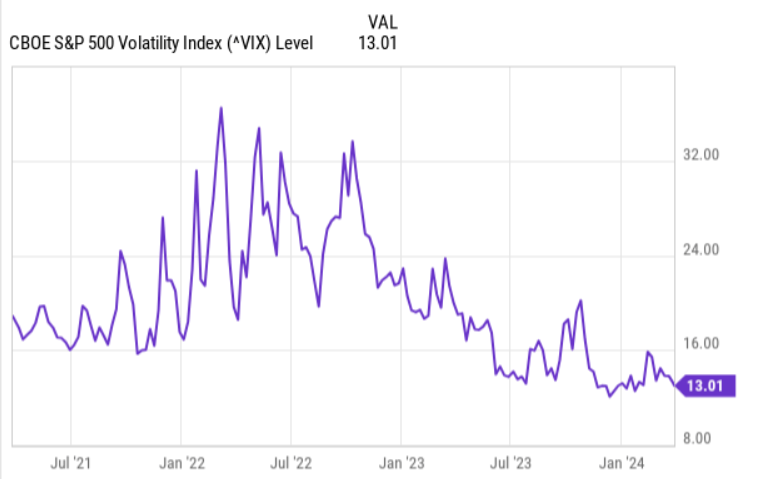

The best way how lined name ETFs can distribute engaging earnings, whereas not divesting the underlying NAV base is thru option-writing. The upper the worth of possibility, the upper the acquired earnings that may be then paid out to unit holders. One of many elementary drivers of possibility value is the implied volatility degree. Particularly, the extra risky the inventory is towards which the decision is bought, the upper premium could be pocketed by the ETF.

At present, the general volatility ranges are depressed, rendering lined name methods much less engaging throughout the board.

Ycharts

Nevertheless, if we take a look at FEPI’s distribution yield, it’s nonetheless within the double digit territory at ~ 10.6%.

So, in FEPI’s case there are two particular drivers that present a direct assist for the yield-generation:

- FEPI doesn’t promote calls towards a broad index, which per definition is much less risky than particular person shares or an index that’s constituted of a small pattern of shares. Therefore, by having fewer positions based mostly on which the calls are written, the implied volatility ranges are oftentimes larger than in ordinary conditions / lined name ETFs.

- The shares themselves which are tracked by FEPI are fairly risky and given the tech-focus are additionally strongly correlated that, once more, is supportive of capturing larger volatility.

For instance, if we evaluate JEPQ with FEPI, we are going to discover that the latter is ready to supply optimistic unfold in yield of ~ 170 foundation factors.

With that being stated, carrying a extra concentrated publicity comes with some extra dangers as effectively. Whereas the yield is perhaps larger, the sensitivity to main value corrections within the FEPI’s holding firms (or perhaps a single firm) could cause the ETF to lower accordingly.

The second one is expounded to the skew in the direction of Magnificent 7 firms which have actually pushed the inventory marketplace for fairly some whereas. As we all know, if one adjusted for the Magnificent 7, the general inventory market can be in a totally totally different zone (i.e., nowhere close to the all time highs).

Right here it boils right down to traders’ subjective views as as to whether these identical particular person shares will handle to take care of the assumed momentum, thereby pushing the inventory market to incremental highs. If that is so, and, much more, if the positive aspects happen in a continuing and gradual vogue, FEPI would be the clear beneficiary.

Conversely, if the small-cap issue out of the blue comes again into vogue, whereas the big cap names stagnate or drop as a consequence of optically stretched multiples, FEPI will endure accordingly. Granted, there may be some embedded safety within the type of name premiums, however within the state of affairs of actually giant drawdowns this is not going to transfer the needle.

The underside line

For my part, FEPI presents an attention-grabbing alternative, the place traders can isolate booming tech publicity, whereas extracting a lot of the positive aspects within the type of engaging present earnings. On the identical time, by going lengthy FEPI, traders can get hold of some layer of draw back safety as a result of inherent lined name programme, the place the pocketed premiums can partially compensate the loss from value depreciation within the underlying portfolio.

Having stated that, there are additionally some clear dangers. Essentially the most notable, in my view, is the chance value of not absolutely collaborating within the continued positive aspects of the Magnificent 7 names. Whereas there is a long way between the underlying value and possibility strike value, it isn’t that significant since FEPI has to focus on yield technology.

The state of affairs by which FEPI would thrive must be related to an gradual uptick in large-cap and tech-related firms as on this case, no main alternative value is incurred and the traders can safely seize the above common yield as a consequence of larger vol choices.

For me FEPI is a maintain.