CuorerouC/iStock Editorial through Getty Photographs

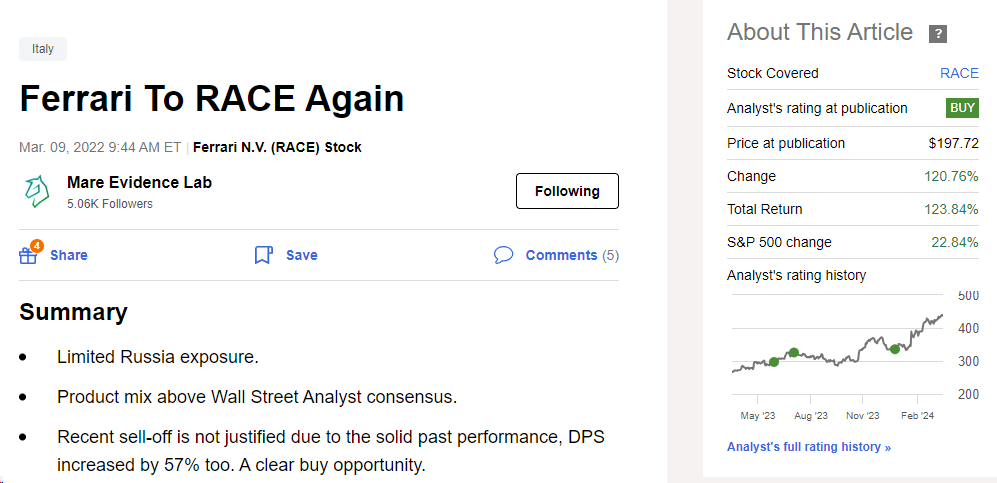

Since early March 2022, our staff has had a long-standing purchase ranking on Ferrari (NYSE:NYSE:RACE). With a publication referred to as Ferrari To RACE Again, we recorded a triple-digit inventory worth appreciation (Fig 1). In 2024, we have been additionally anticipating an Outperformance, however we imagine the corporate’s valuation is not engaging. Whereas we like Ferrari’s high quality and long-term progress prospects, we decrease our suggestion from purchase to impartial. Nevertheless, we raised the goal worth from €350 to €380 to replicate larger earnings estimates and decrease bills in the long run. We see the inventory market specializing in high quality corporations; nevertheless, after a plus 30% since our final replace (early January 2024), the inventory trades at virtually 12x gross sales and a P/E >50x on its 2024 steerage.

Mare Ranking Evolution

Fig 1

Ferrari Numbers into Perspective

Right here on the Lab, we like auto corporations, and we have now luxurious automobiles in our protection. We intently observe Porsche AG, Aston Martin, and Lamborghini, which Volkswagen controls. Due to this fact, earlier than offering our replace and to assist our readers, it’s vital to report our following takeaways:

To repay Ferrari’s present market capitalization of €73 billion, on the document of a median promoting worth of €397k per automobile with a web revenue margin of 21%, Ferrari ought to promote greater than 800k automobiles. On the present manufacturing charge, it could take greater than 60 years to take action.

One other consideration to assist buyers put the corporate’s shortage into perspective:

Dr. Ing. h.c. F. Porsche AG (or P911) (OTCPK:DRPRF) (OTCPK:DRPRY) makes in a single 12 months what Ferrari has made in its whole historical past. The Italian firm was based in 1939;

Ferrari delivered roughly 13,663 items, equal to Toyota’s ten manufacturing hours.

Our Unfavorable Takes

Our earlier evaluation anticipated 2024 gross sales and EBITDA margin at €6.55 billion and 29.0%, respectively. This was backed by larger pricing (2%) and a greater product MIX evolution (+6.5%). On a optimistic be aware, we thought of larger automobile personalization, however we additionally took into consideration the decrease common promoting worth of the upcoming Roma Spider (the brand new automobile has a beginning worth of €249,650 in comparison with a median promoting worth of roughly 397k per automobile recorded in This autumn 2023).

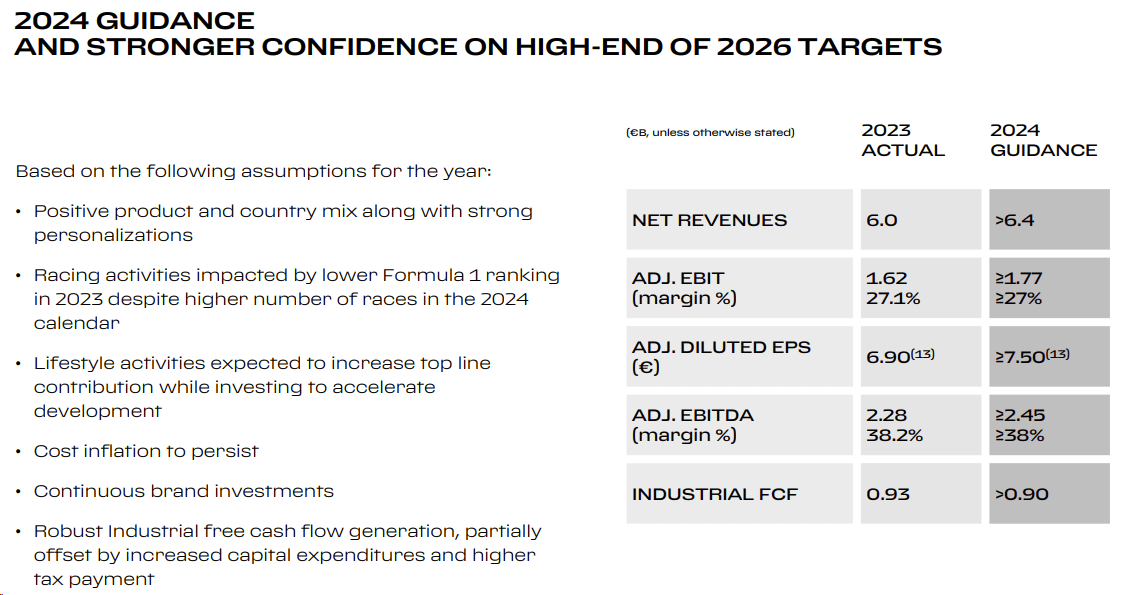

Right here on the Lab, we count on the same old beat-and-raise dynamic for Ferrari, and because of this, we’re above the corporate’s 2024 earnings per share outlook. Due to this fact, we persist with our earlier numbers and ensure our 2024 EPS forecast at €8.4. We must also report that Ferrari’s preliminary 2024 steerage signifies progress of income and EPS between 8% and 10% (Fig 3). Certainly, Ferrari tasks progress; nevertheless, that is slower than its historic common. Wanting on the previous 12 months, income and EPS elevated by 17% and 36%, respectively. Due to this fact, sell-side analysts may determine to decrease the corporate’s goal worth.

There are additionally 4 destructive information to be priced in:

- Ferrari will face a category motion in the US. The corporate is accused of failing to restore a brake defect in some fashions, together with the Ferrari 458 Italia. The category motion recognized a brake fluid leak, and regardless of automobile remembers, the corporate may face new complaints;

- We imagine Ferrari will decelerate with the buyback. At effectively over 50x P/E, we’re positive that Ferrari has higher methods to deploy its capital. This may present stress on the corporate’s inventory worth;

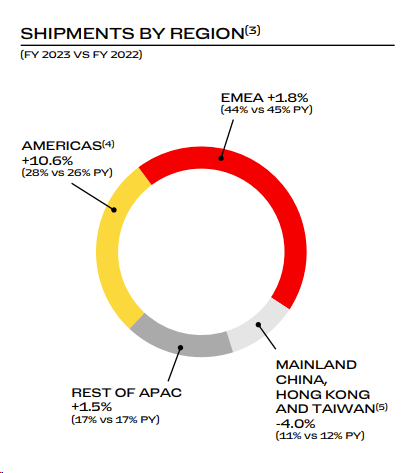

- The corporate is just not resistant to decrease unit gross sales in China. Intimately, gross sales decline in China in This autumn 2023 (Fig 2);

- Businesswise, there must be extra certainty about electric-only know-how. Within the very long run, right here on the lab, our staff sees Ferrari as one of many few surviving automobile gamers that may produce inner combustion engine automobiles. Nevertheless, this poses a danger, and we can not forecast a quantity progress story just for automobile collectors.

Ferrari’s decrease APAC gross sales

Supply: Ferrari Q4 results presentation – Fig 2

Ferrari 2024 Steering

Fig 3

Valuation

Right here on the Lab, the time has come to query Ferrari’s valuation. The corporate’s enterprise is extra difficult than Hermès’, and this could recommend a reduction on the inventory market. Each corporations presently commerce at a P/E of greater than 50x, near all-time highs and considerably above the multiples of different luxurious corporations. Nevertheless, if we indicate slower earnings per share progress charge (15% and 20%), Ferrari’s P/E goal must be valued at round 35/40 occasions. In the present day, Ferrari trades at parity with Hermes, and we’re not going into the frequent saying, ‘Ferrari’s all the time been costly and all the time might be.” Our 2025 EBITDA margin is at 39.5%, while Hermès reached a record year EBITDA margin of 47%. Therefore, we believe a 10% discount is justified. The French luxury giant trades at a 50x P/E, and continuing to apply a 10% discount, we derived a price target of €380 per share ($405 in ADR). Ferrari’s fundamentals are similar to those of automotive companies, such as lower sales in China and auto parts issues (North American class action is just an example). Therefore, we moved our rating to an equal weight two years later.

Risks

Here at the Lab, we consider different risks, such as Ferrari’s lower volume growth, rapid change in consumer tastes and technology, failure in Formula 1, and, we believe, a lower valuation methodology from sell-side analysts. Ferrari is an automotive company that is affected by common business risks such as currency evolution, raw material pricing pressure, defective auto parts, and wage inflation. The company is also subject to a high corporate tax. Ferrari is moving on with new lifestyle activities such as the Fashion industry. From now on, the company will launch a fashion collection every year for both men and women. This is a new business, and it might fail to meet expectations and the necessary product development.

Conclusion

Ferrari has a solid order book, and the company’s production is covered until 2025. Investors and sell-side analysts positively viewed Ferrari’s backlog; however, the company’s EPS might be slower than consensus expectations. Again, Ferrari’s exclusivity is also perceived due to limited auto production. Last time, we were the first to believe that there was Luxury Upside Still To Price In, but today, considering a high valuation, we decided to lower Ferrari’s rating to a neutral status.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.