DarioGaona

We’re nearing the end of the Q1 Earnings Season for the Silver Miners Index (SIL), and while quite a few silver producers started the year off generating positive free cash flow, First Majestic Silver Corp. (NYSE:AG) was not one of them despite its much larger production profile. In fact, free cash outflows continued in Q1 despite turning off its highest cost asset (Jerritt Canyon) last year. While the outlook for Q2 is better, the stock continues to trade at an unappetizing free cash flow multiple at over 70x FY2024 free cash flow estimates. In this update, we’ll dig into the Q1 results, its valuation vs. other mid-sized producers, and why the stock continues to be an inferior buy-the-dip candidate.

Santa Elena Mine – Company Website

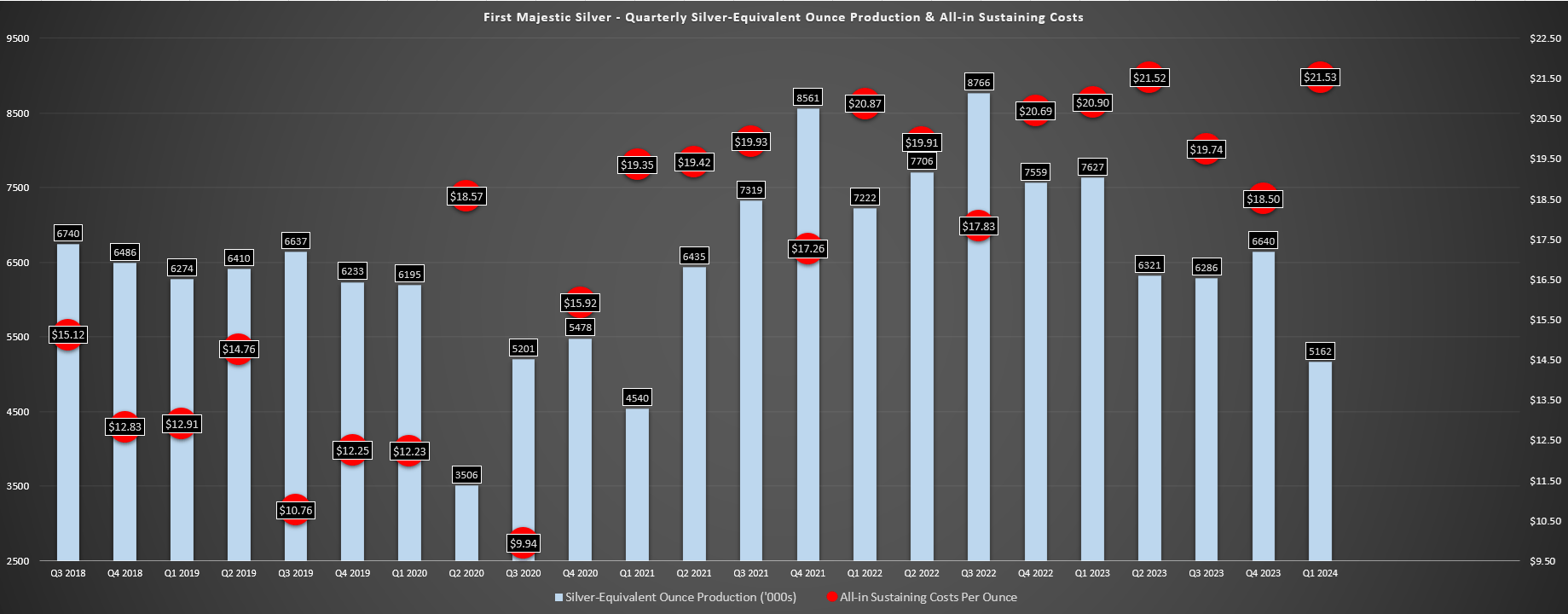

First Majestic Silver Q1 Production & Sales

First Majestic released its Q1 results earlier this month, reporting quarterly production of ~5.2 million silver-equivalent ounces [SEOs] or ~1.98 million ounces of silver and ~35,900 ounces of gold. This translated to a 22% decline in silver production and a 41% decline in gold production. Gold output was significantly affected by having to lap Jerritt Canyon’s production, with the asset heading offline in Q2 of last year. Meanwhile, silver production slid because of lower production at La Encantada (limited water supply to the plant) and lower grades at San Dimas (mining in low-grade areas) plus a labor disruption.

First Majestic Silver Quarterly Production & Costs – Company Filings, Author’s Chart

On a positive note, First Majestic has now lapped these difficult comps as it heads into Q2 2024, with Jerritt Canyon contributing ~16,300 ounces of gold and ~$24.1 million in revenue in Q1 2023 which hurt its year-over-year results (limited production this year). Meanwhile, the company expects a better H2 out of its smallest La Encantada Mine, with an additional water source identified that is expected to push processing rates back to 3,000 tonnes per day by Q3. Finally, San Dimas is expected to benefit from better grades and higher throughput in H2, and hopefully union negotiations go well, with First Majestic noting that negotiations at San Dimas on headcount, base pay and bonuses continued into Q2.

The other positive worth noting was that Santa Elena has performed well thanks to Ermitano, with ~2.28 million silver-equivalent ounces produced at all-in sustaining costs of $14.70/oz. This was actually an improvement year-over-year despite the stronger Mexican Peso (Q1 2023: $15.18/oz), with higher throughput (~224,400 tonnes processed), higher silver grades, and higher gold/silver recovery rates. The mine also benefited from no ounces produced on royalty ground attributable to its silver stream, with the only impact being royalties held on Ermitano. That said, the better quarter out of Santa Elena wasn’t enough to offset lower sales from San Dimas, Jerritt Canyon, and La Encantada.

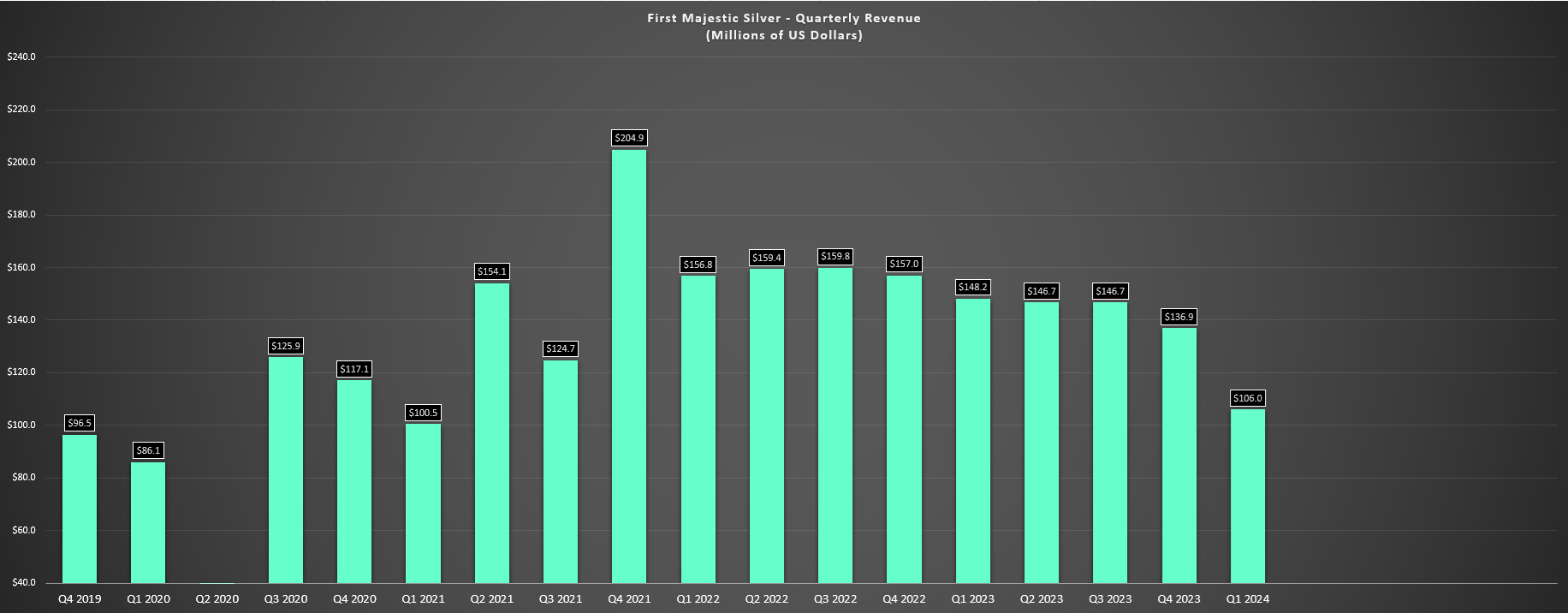

First Majestic Silver Quarterly Revenue – Company Filings, Author’s Chart

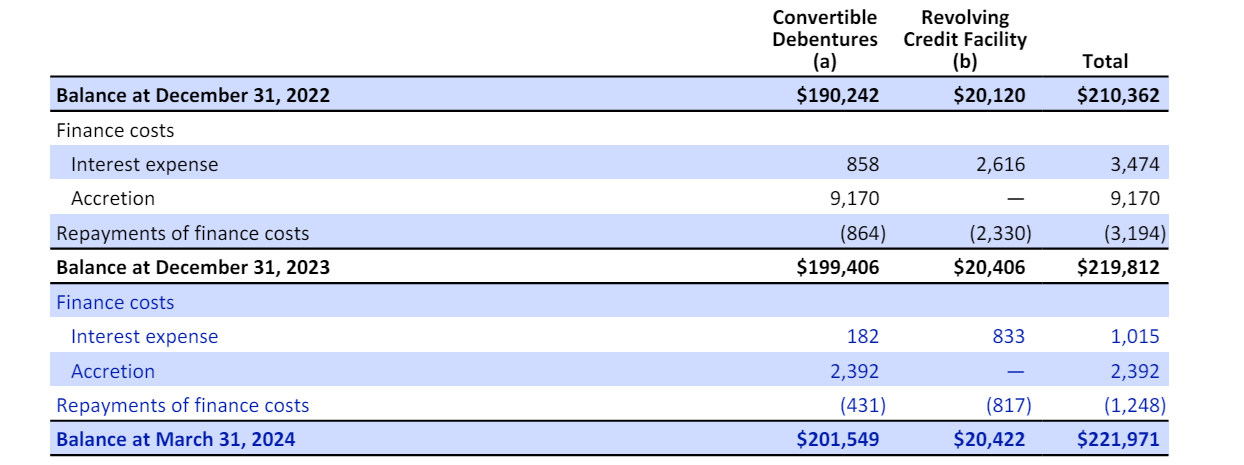

As for its financial results, there was little to write home about, with First Majestic reporting a 32% decline in revenue year-over-year despite the benefit of higher metals prices. This was related to no revenue from Jerritt Canyon, as discussed previously, and significantly lower throughput from La Encantada and San Dimas and much higher costs (*). The result was that First Majestic saw continued free cash outflows, with operating cash flow of just ~$12.4 million in the period vs. capex of $28.2 million, resulting in a free cash outflow of $15.8 million in Q1 2024. Given the decline in cash to $102 million, the company continues to have a net debt position with its convertible notes and outstanding balance on its revolving credit facility.

First Majestic Silver Debt Facilities – Company Filings

(*) San Dimas’ AISC in Q1 2024 came in at $20.49/oz while production costs per tonne rose to ~$200.7 vs. $14.67/oz and ~$157.4/tonne in the year-ago period. (*)

Costs & Margins

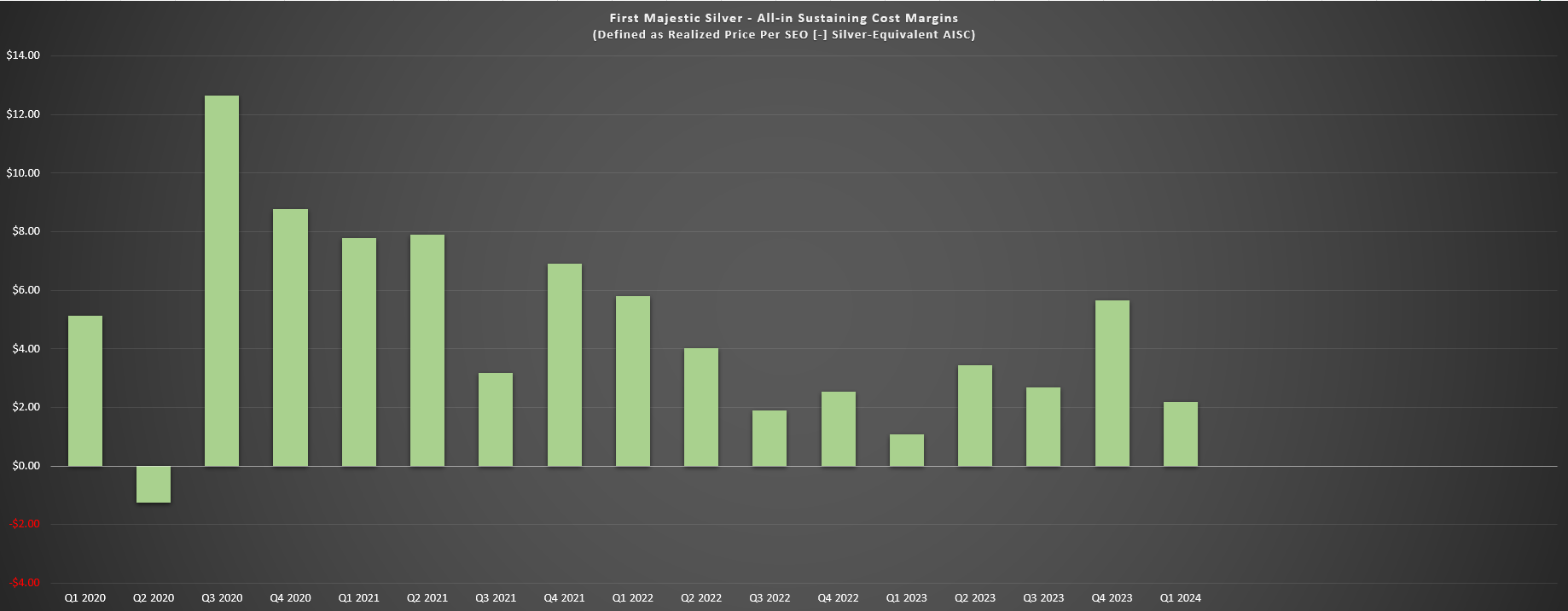

Moving to costs and margins, First Majestic’s all-in sustaining costs per silver-equivalent ounce came in at $21.53/oz in Q1 2024, a 3% increase from the year-ago period. The higher costs were despite taking its highest-cost operation offline (Jerritt Canyon), with First Majestic affected by lower grades at San Dimas, a much lower scale at La Encantada (limited water availability) and a significant headwind from the strength of the Mexican Peso (*). And while the silver price has certainly woken up since Q1, the company won’t see the full benefit of this in its Q2 results. This is because it will be another moderate production quarter (La Encantada still ramping up) and the fact that the silver price spent most of Q2 below $28.00/oz, even with its recent charge higher.

First Majestic Silver AISC Margins – Company Filings, Author’s Chart

(*) The USD/MXN has averaged ~16.9 year-to-date vs. the US Dollar, a significant decline from ~18.4 in the same period last year and cost guidance of $20.00/oz (guidance midpoint) is based on a USD/MXN rate of 18.0 to 1.0. (*)

Fortunately, the gold price (XAUUSD:CUR) strength contributed to a stronger silver-equivalent price of $23.72/oz in Q1 even while silver underperformed gold, with First Majestic’s all-in sustaining cost margins improving to $2.19/oz (9.2%) vs. $1.08/oz (4.9%) in the year-ago period. However, these are still razor-thin margins relative to the producer peer group. The good news is that it looks like we may have seen trough margins and a better setup is finally on deck, with silver-equivalent AISC likely to drop below $20.00/oz in H2 with La Encantada ramping back up, and what could be an average realized silver price of $27.00/oz or better or ~$7.00/oz AISC margins.

Quarterly Gold Price – StockCharts

As for the upcoming Q2 results to be reported in August, we will likely see elevated AISC with a minor drag from La Encantada processing at lower rates. However, we should still see silver-equivalent AISC margins improve to $4.00/oz or better. If achieved, this would represent a near 90% increase sequentially vs. the $2.19/oz reported in Q1 2024, and we’ll also see a significant lift to revenue now that the company has lapped the difficult comps from Q1 while Jerritt Canyon was still online.

Valuation

Based on ~293 million fully diluted shares and a share price of US$8.00, First Majestic trades at a market cap of ~$2.34 billion and an enterprise value of ~$2.50 billion. This continues to make it one of the highest market cap names in the 300,000 ounce producer peer groups and is trading at an enterprise value similar to that of Torex Gold (OTCPK:TORXF) and K92 Mining (OTCQX:KNTNF) combined. To put this in perspective, First Majestic will be lucky to generate $100 million in free cash flow in 2026 and has relatively short mine lives, while these two companies will generate nearly $600 million in combined free cash flow. And while some premium is warranted for being a highly liquid silver producer, First Majestic continues to be one of the most expensive producers sector-wide relative to its scale, margins and NAV estimates.

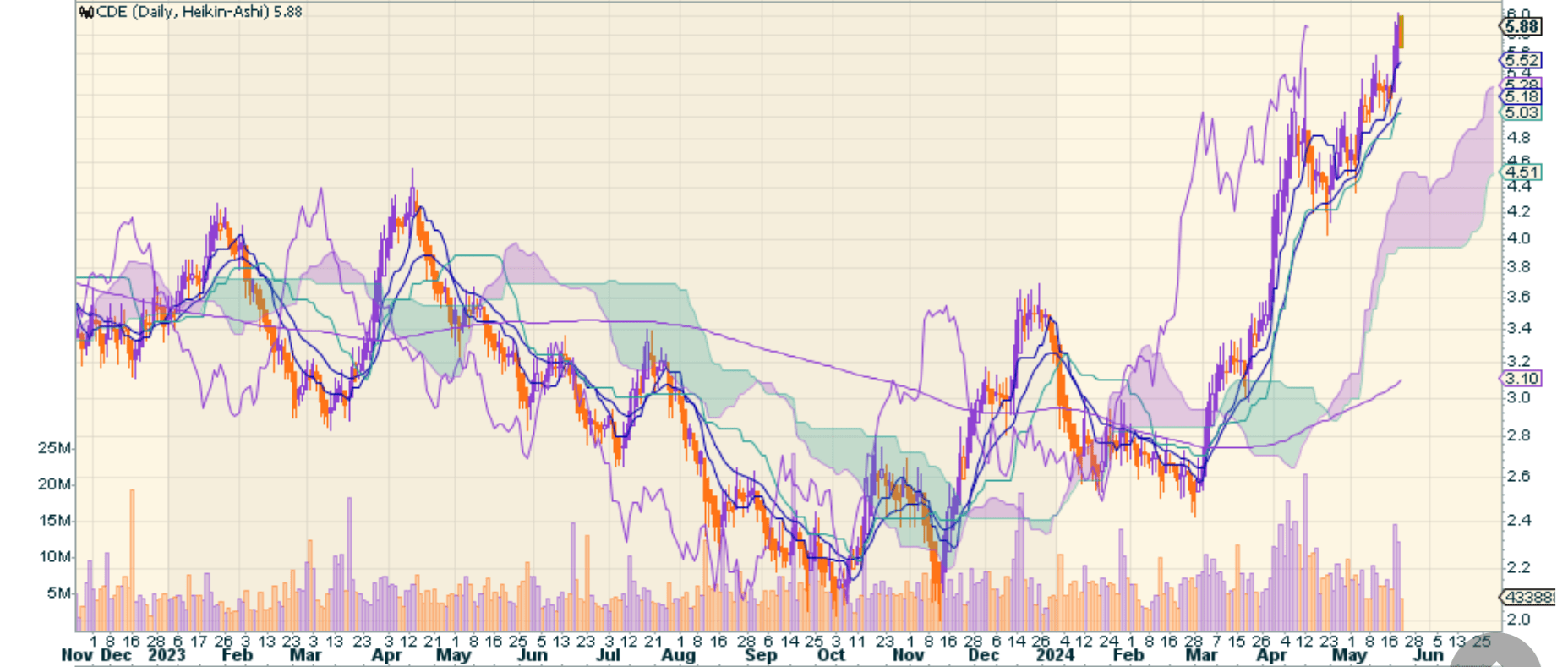

CDE Daily Chart – StockCharts.com

As we’ve seen with several other lower-quality producers that have been serial diluters over the years, like Endeavour Silver (EXK) and Coeur Mining (CDE), a rising tide (silver price) will lift all boats. Still, I continue to see names like AG as the least attractive ways to invest in the sector and while they could trade higher, there is no investing without valuation. And at today’s prices, an investor needs to believe that gold and silver prices will average $2,800/oz and $32.00/oz, respectively, and that First Majestic will restart Jerritt Canyon to even begin to justify its current valuation. Hence, I see the stock as fully valued here at US$8.00, and I see no reason to chase this rally, with the stock now vulnerable to a sharp correction.

Summary

While a few high-quality precious metals names continue to trade at very reasonable multiples, First Majestic trades at a P/NAV multiple that’s higher than that of Wheaton Precious Metals (WPM) and Franco-Nevada (FNV). This is despite First Majestic being a low-margin silver producer with three shorter life assets and the bulk of its NAV tied to a Tier-2 ranked jurisdiction (Mexico), and is the antithesis of what one should look for in an investment (lower relative quality, and expensive on relative value).

A rising silver price will lift all boats, and technically AG is nowhere as overbought as it got in 2021, which suggests there’s likely further upside here medium-term even if it is overdue for a correction short-term. Still, for those looking for value in the sector, I think there are far more attractive bets elsewhere than chasing First Majestic Silver Corp. after a ~90% rally above US$7.90 per share.