SW Images/DigitalVision through Getty Photos

In the case of First Photo voltaic (NASDAQ:FSLR), a lot is definitely presently recognized in regards to the main North American photo voltaic panel producer’s potential progress and earnings trajectory.

With an enormous backlog of ~80 Gigawatts, an enormous deal pipeline in varied phases of growth, and ASP’s which are trending greater, not decrease, and there is not any query that the corporate is presently set as much as ship robust outcomes by way of the tip of 2030.

The query, at this level, is about whether or not or not FSLR can execute, making good on its bold manufacturing targets and supply timeline. There’s additionally a query about whether or not or not the corporate’s earnings previous the tip of this decade will likely be impacted by Chinese language oversupply and dumping dangers.

In our thoughts, with a robust observe document of innovation, a wonderful liquidity place, and with a robust model for high quality inside the trade, we anticipate that FSLR is well-prepared to climate the storm and ship market-beating outcomes for the foreseeable future.

As we speak, we’ll check out FSLR’s financials and the inventory’s worth proposition as a way to present why we expect this main clear power play seems massively undervalued versus its potential.

Sound good?

Let’s dive in.

First Photo voltaic’s Financials

As at all times, let’s start by looking at FSLR’s financials.

In brief, FSLR has had a secure, if considerably anemic, previous few years of operations.

TTM Gross sales have been constant, ranging between $2.4 and $3.6 billion between 2017 and the current:

TradingView

Earnings have been much less secure, however largely optimistic, with web earnings ranging between -$200 million and $600 million over that very same interval.

Clearly, this isn’t preferrred, particularly for a corporation inside a ‘progress trade’ like clear power. Nonetheless, it is largely as a result of the truth that photo voltaic has seen a variety of boom-and-bust funding cycles, and so gamers like FSLR, SunPower (SPWR), and others have needed to tinker, over time, with their enterprise fashions. Within the case of SPWR, it seems to have been for the more serious.

Nonetheless, with FSLR, we see the corporate’s current jettisoning of its techniques enterprise as a optimistic, and, with a clearer, extra streamlined enterprise mannequin centered on designing, manufacturing, and delivering panels, we’re anticipating to see higher leads to the years forward.

That is already displaying up within the outcomes.

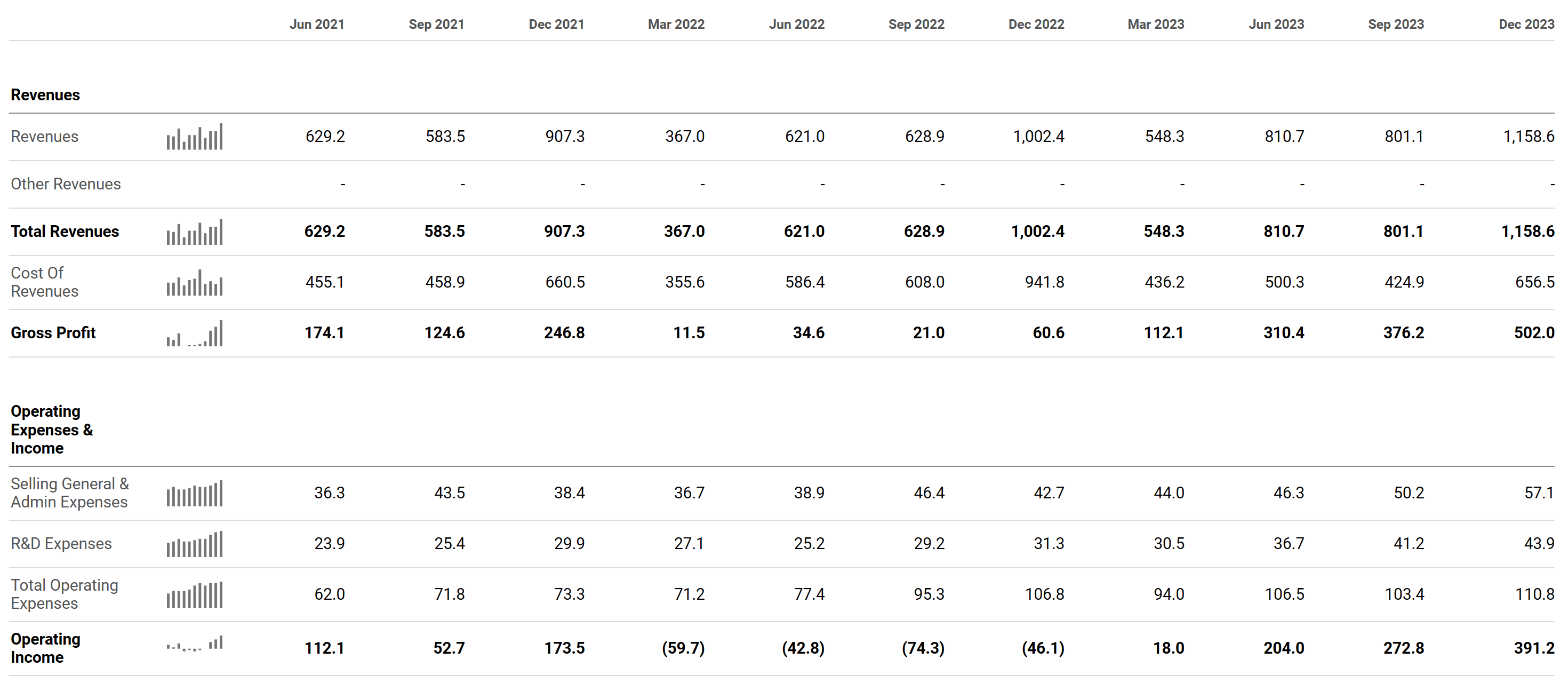

Over the previous couple of quarters, you may see that Income, Gross Revenue, and Working Revenue have all grown considerably:

Searching for Alpha

In our eyes, the vast majority of this enchancment comes right down to elevated deal with FSLR’s core enterprise and worth proposition.

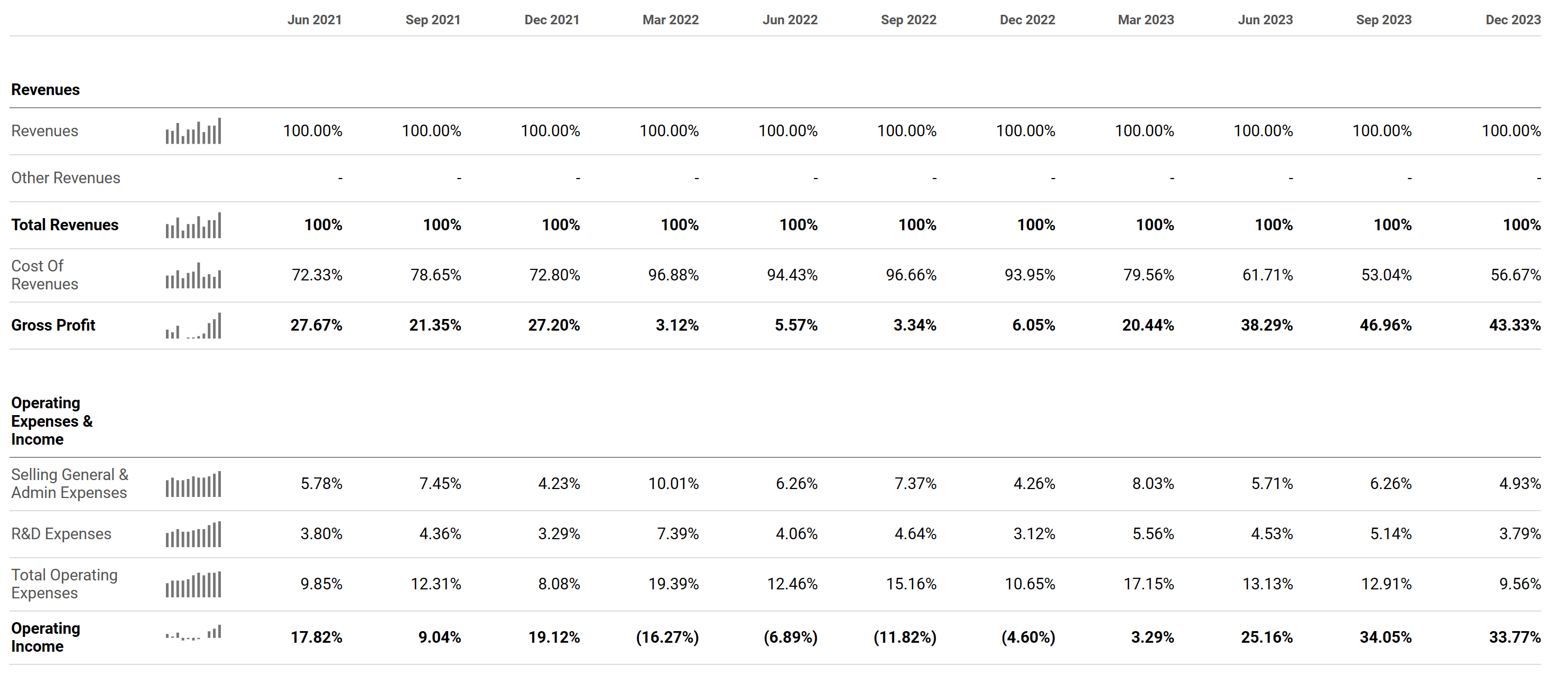

This has additionally led to a giant enhance in FSLR’s margin profile, significantly on the gross margin entrance, between 2021 and This autumn 2023, rising from the mid 20’s to the mid 40’s:

Searching for Alpha

This gross margin enchancment is absolutely distinctive inside the trade, and it may be defined by the model that FSLR has constructed up over time with prospects.

Whereas many have turn into involved with Chinese language oversupply within the panel market, FSLR administration would not seem like too involved.

Why?

Due to FSLR’s model.

When requested why FSLR can cost ASP’s per watt which are considerably greater than opponents and overseas firms like JA or Tongwei, CEO Mark Widmar had the following to say:

I used to be having a dialog with certainly one of our largest companions simply final week. They usually could not be happier to be partnering with First Photo voltaic.

And the attributes we’re speaking about, the power of the expertise, the understanding of First Photo voltaic, but it surely additionally will get into the accountable photo voltaic points as nicely and our carbon footprint and our water utilization and our power payback and our round financial system. And whenever you — that is inherent to their worth proposition that they are promoting to their contracted off-take prospects, like information facilities, who worth that as nicely.

…

And our accomplice stated, mainly, look, I do know I’ll need to pay just a little bit extra for First Photo voltaic, however after I take a look at the model and the understanding and the worth proposition that they are creating, more than pleased to try this. And this can be a counterparty that’s nearly 80 plus %, 100% sole supply into First Photo voltaic, and we have a deep relationship and multi-gigawatts of alternative nonetheless in entrance of us. And I do not see this as a singular one-off.

…

They worth the understanding of First Photo voltaic, and [are] trying to de-risk their tasks as far out as they will go. The opposite factor that is nonetheless driving some uncertainty within the market is, as you have seen not too long ago with on an IP standpoint, particularly because the market has transitioned to TopCon. Gencos has indicated that they are going to have a robust IP place for TopCon and they are going to implement that IP. You’ve got seen Maxeon make statements as nicely that they have an IP place round TopCon that they are additionally going to implement. So, our prospects additionally need to assume by way of freedom to function with their counterparties round mental properties.

The best way we see it, FSLR’s pricing power comes from 3 key issues:

- Differentiated Tech

- Secure accomplice

- ‘Accountable Photo voltaic’

While you’re shopping for FSLR as a buyer, you are spending up on higher panels, certainty in pricing and IP, and a dedication that the panels have been made in accordance with greatest environmental practices.

Zooming in for a second, on the panel entrance, FSLR’s distinctive Cad-Tel panels are higher at changing the solar’s power into electrical energy than conventional silicon, which provides a greater payback interval to scaled traders:

Investor Presentation

Moreover, as FSLR has a variety of hedging agreements in place that present visibility into pricing and margins, FSLR can supply worth certainty to prospects means out into the longer term, whereas locking in gross margins at present second in time:

As of December 31, 2023, roughly 95% of the megawatts in our backlog had some type of freight safety, and roughly 85% had some type of metal and/or aluminum commodity value safety.

Add all of it up, and FSLR seems poised to win enterprise now, and nicely into the longer term, regardless of not being as aggressive on value as different panel producers in China and southeast Asia.

It is also why the corporate’s ASP has truly elevated in current quarters, regardless of the oversupply of panels, on the whole, available in the market.

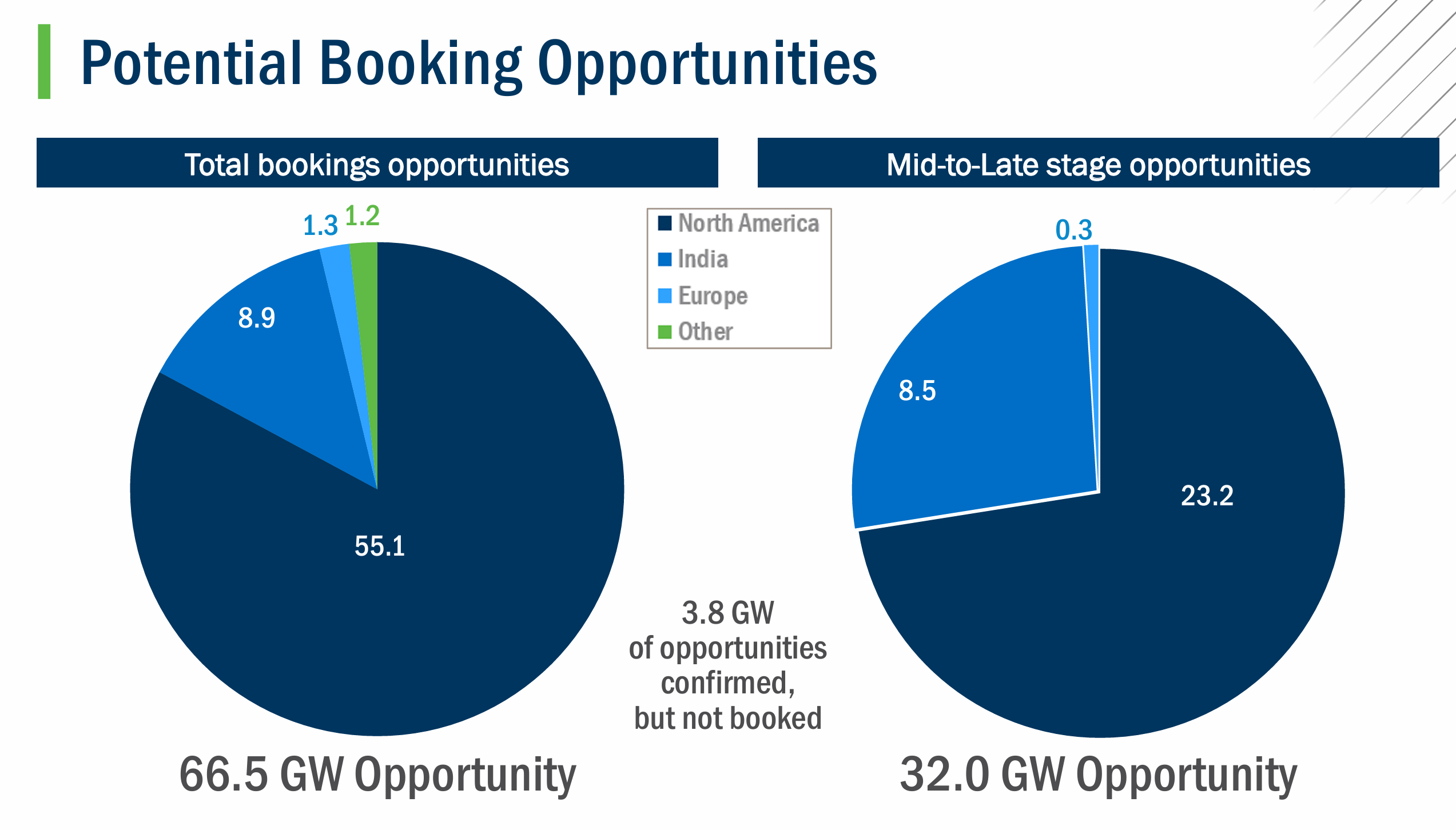

First Photo voltaic’s Backlog

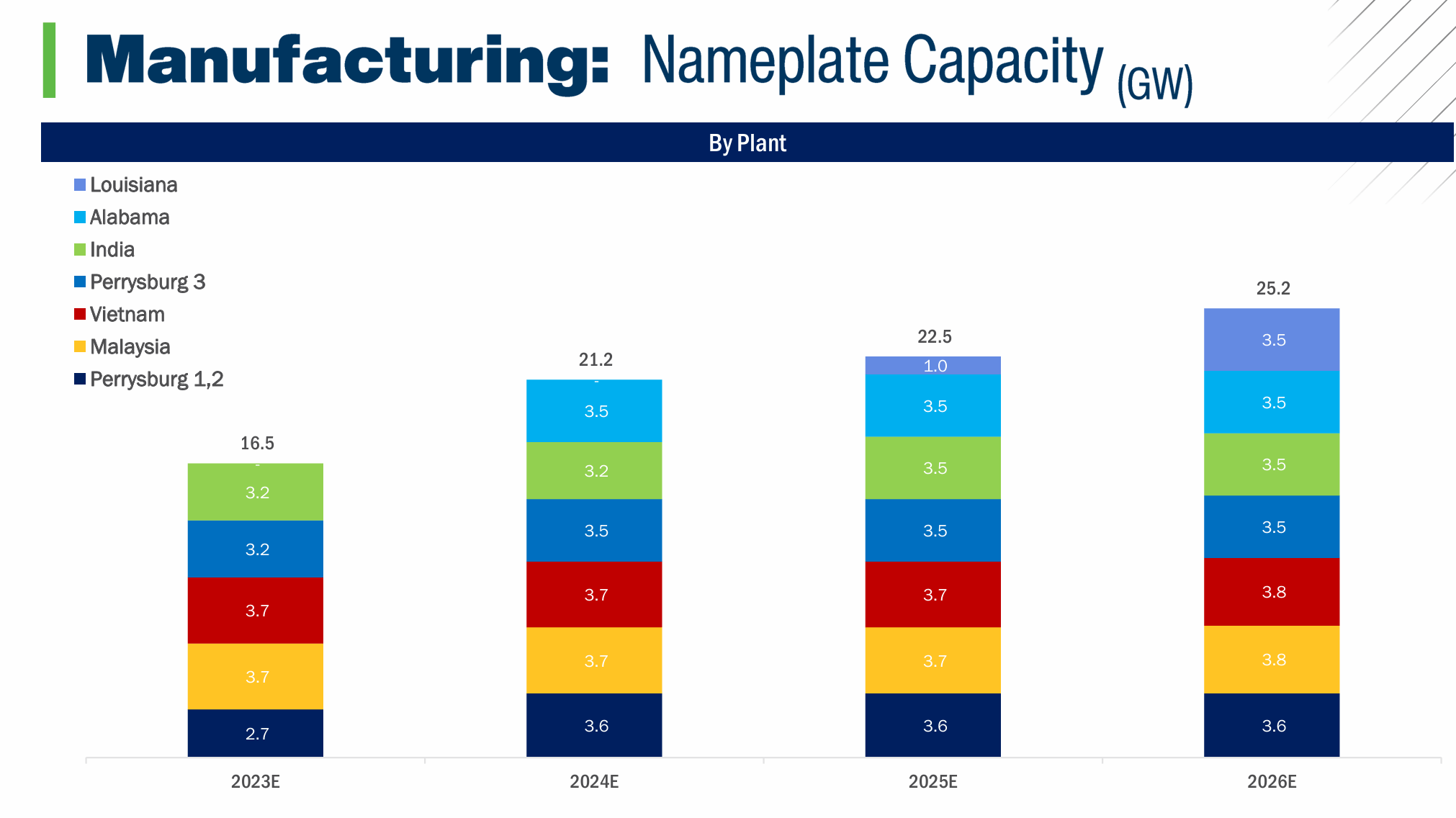

Mix these benefits, and tack on the elevated deal with the core enterprise, and it is no marvel that FSLR’s backlog is big, and increasing.

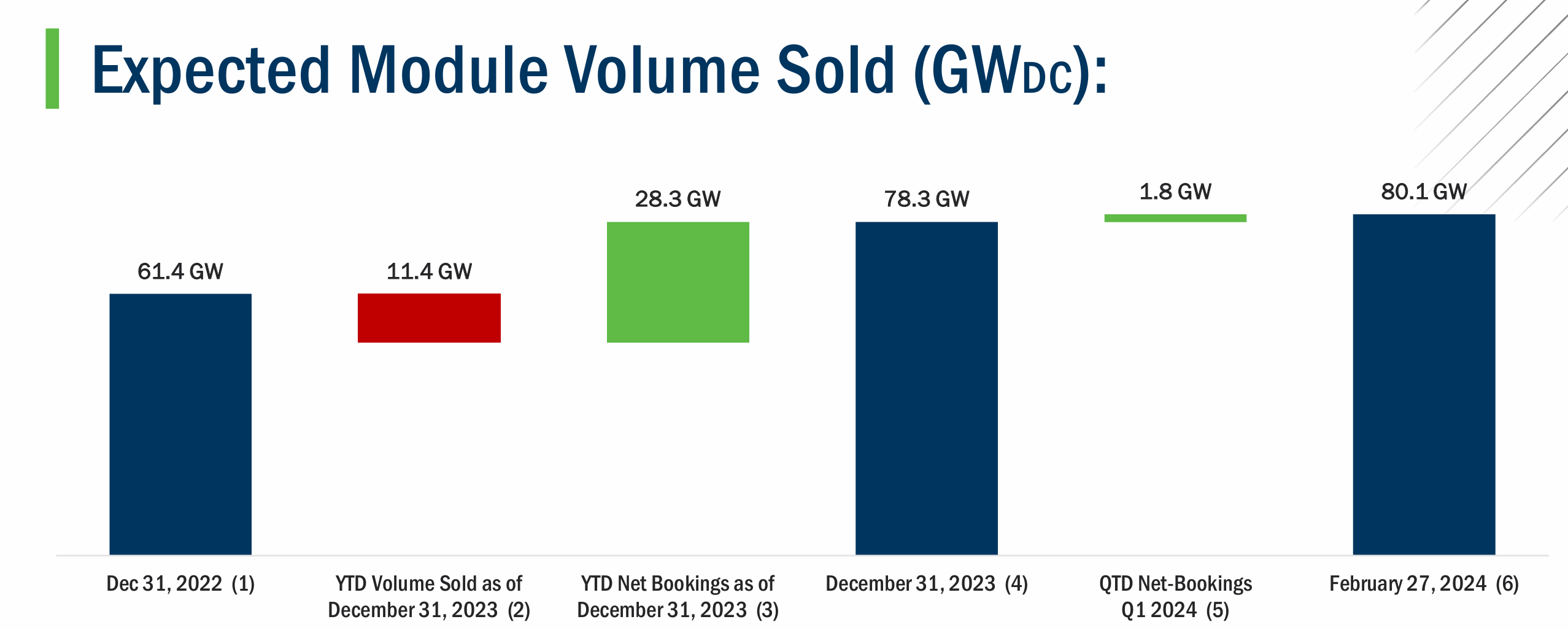

With 80 GW booked, incremental provides to this backlog over current quarters, and one other 100 GW within the potential pipeline, FSLR’s monetary place seems safe nicely into the longer term:

Investor Presentation Investor Presentation

Because of this the corporate is targeted on rising manufacturing, so it could possibly meet the calls for of the market over time:

Investor Presentation

Even at this degree of manufacturing, it can take years and years to chunk by way of the present backlog.

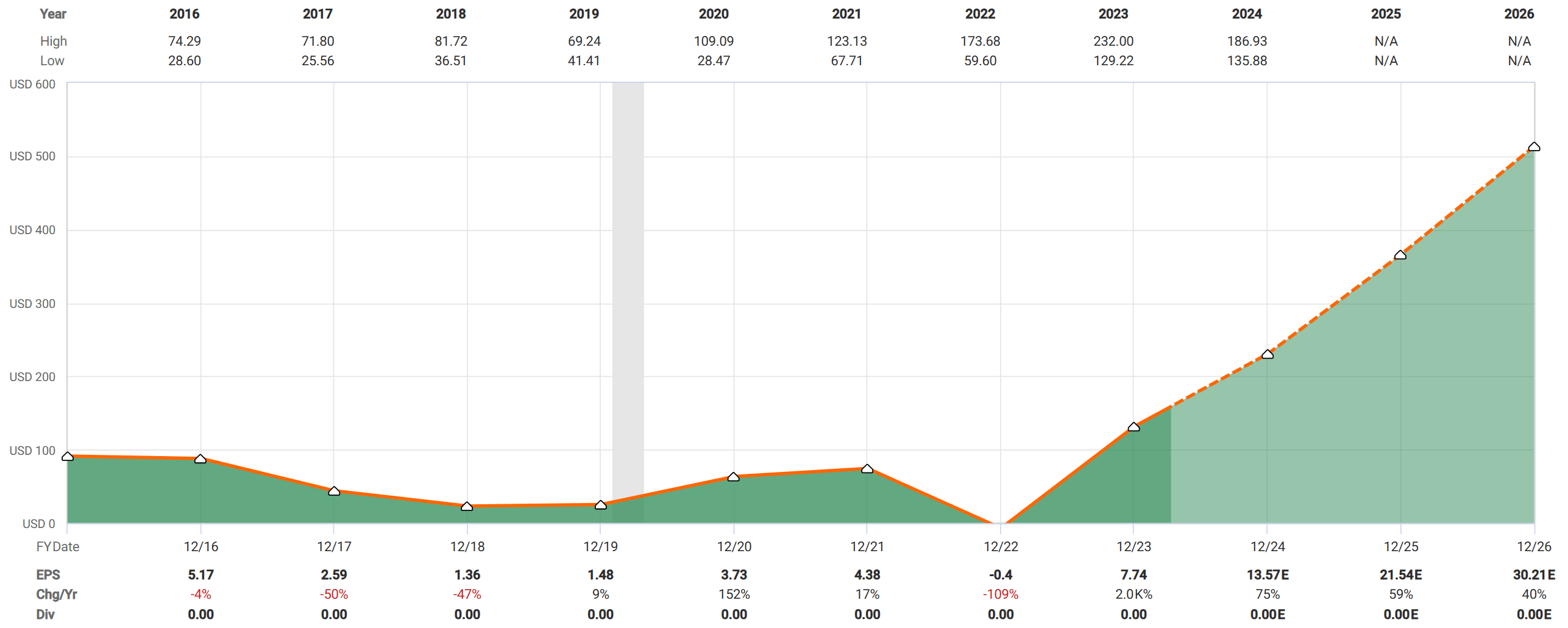

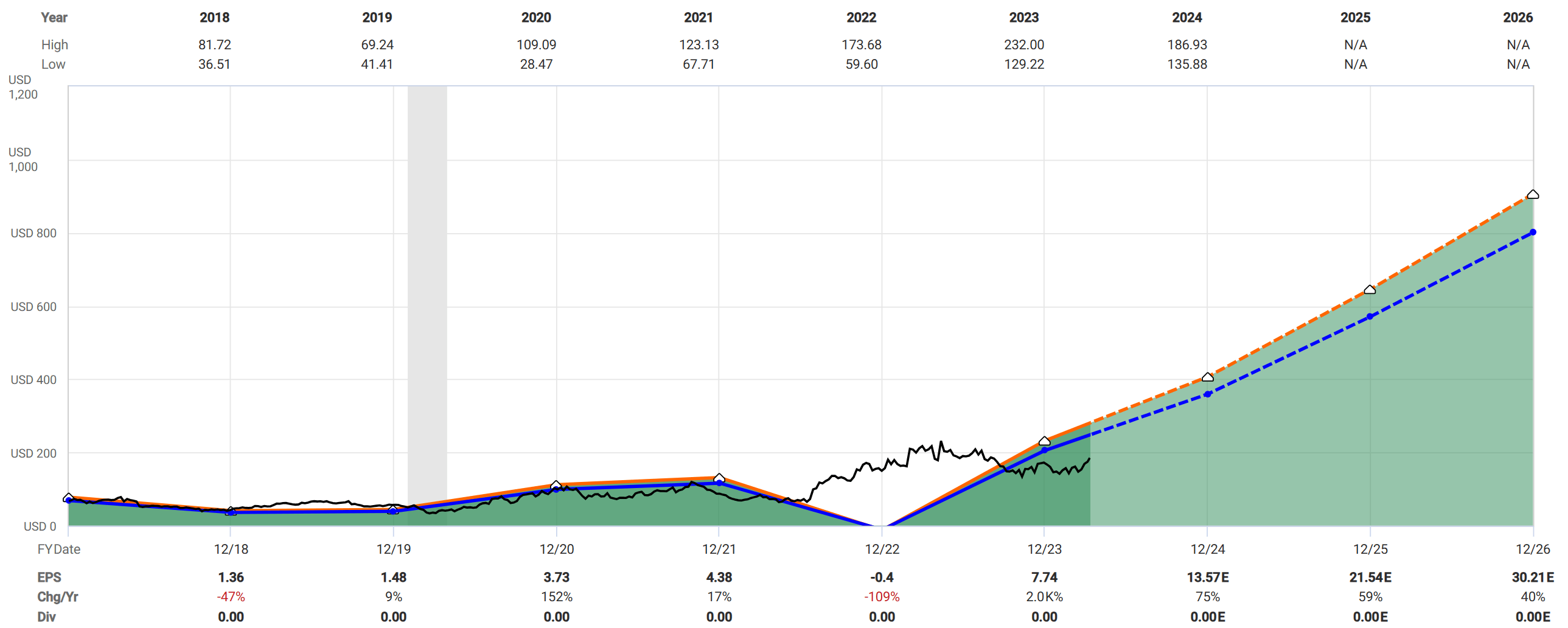

Wanting ahead to earnings, analysts presently imagine that Adjusted Working Earnings are poised to broaden significantly, to ~$13, $21, and $30 per share over the following 3 years:

FAST Graphs

This appears affordable to us on condition that increasing realized income ought to come about on the again of manufacturing progress and backlog execution, and the corporate ought to see secure / enhancing margins given administration’s lengthy historical past of value management. Plus, with a comparatively fastened value base, we anticipate that new incremental gross income ought to drop straight to the underside line.

If FSLR is ready to execute on this backlog on the quoted ASPs, which, once more, appears affordable as a result of FSLR’s traditionally conservative strategy to managing contracts, liquidity, and commitments, it seems as if the corporate’s EPS ought to broaden dramatically within the coming years, from the ~$7 per share it reported in 2023.

What Is First Photo voltaic Price?

So, if First Photo voltaic has a variety of long-term strengths that ought to permit it to proceed profitable enterprise previous the backlog, the corporate is increasing manufacturing capabilities to satisfy demand, and earnings on the present backlog are anticipated to spice up EPS considerably, what may the inventory be value?

Proper now, FSLR trades at a ~$19 billion market cap.

For 2024, administration is forecasting $1.5 billion midpoint for working earnings.

This offers FSLR a 13x 2024 Working a number of, which seems very affordable given the potential future progress in retailer right here.

On this case, working a number of looks like a great place to start out, as a result of it reveals the precise ‘outcomes’ of the enterprise, with out trying on the current tax credit score sale and different issues that would muddy the waters. We’re making an attempt to see what the market’s a number of positioned on enterprise exercise is, and in our view, 13x seems enticing.

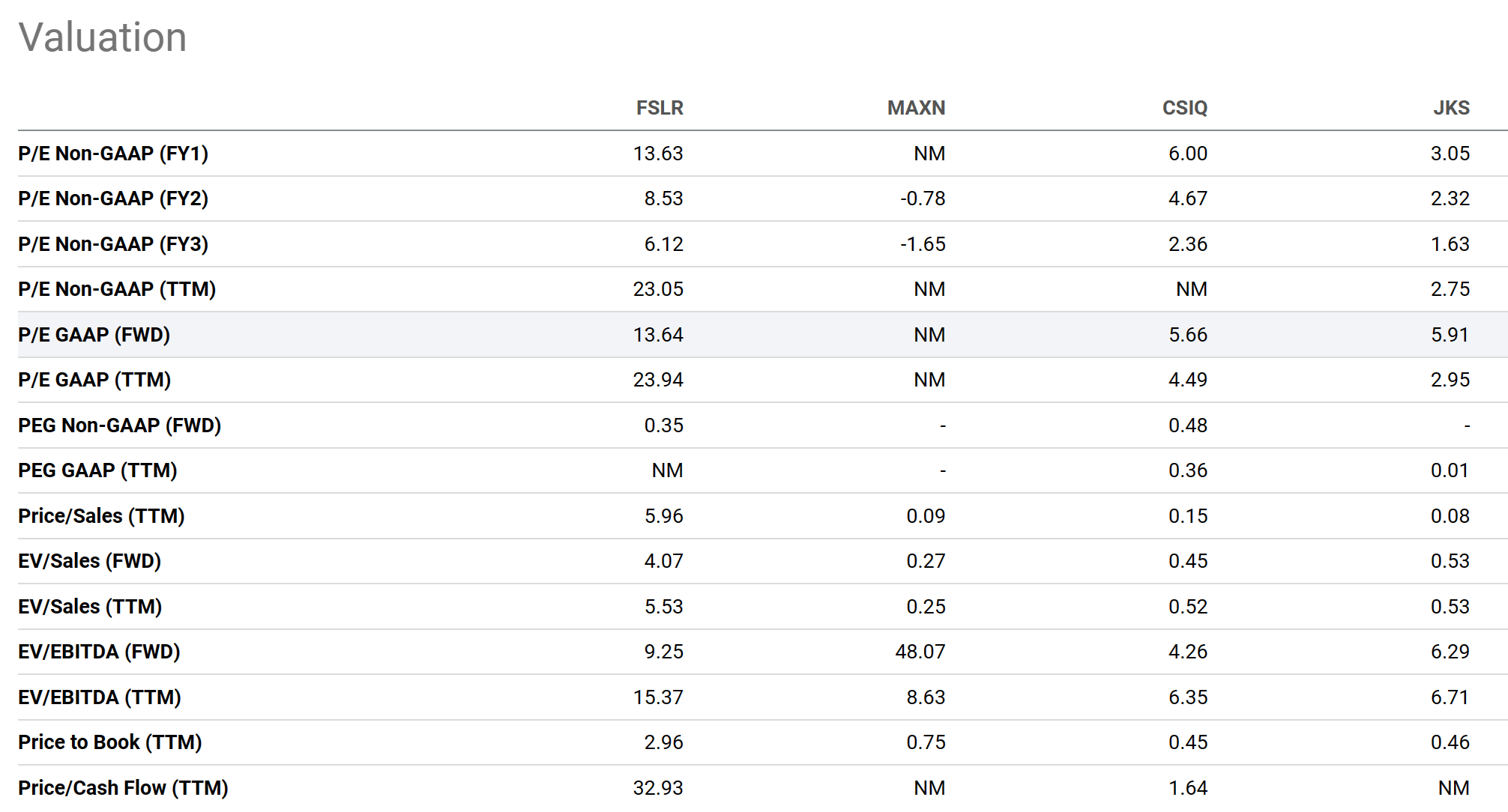

On one hand, 13x FWD earnings would not examine favorably with different shares available in the market, like Maxeon (MAXN) and Canadian Photo voltaic (CSIQ):

Searching for Alpha

Nonetheless, FSLR is many occasions bigger than these domestically listed opponents, which provides it dimension, scale, and completive benefits.

Moreover, when put next with the S&P 500’s nominal long run a number of of 18x, FSLR seems enticing, particularly as a result of it is anticipated to develop at a a lot faster charge over the interim.

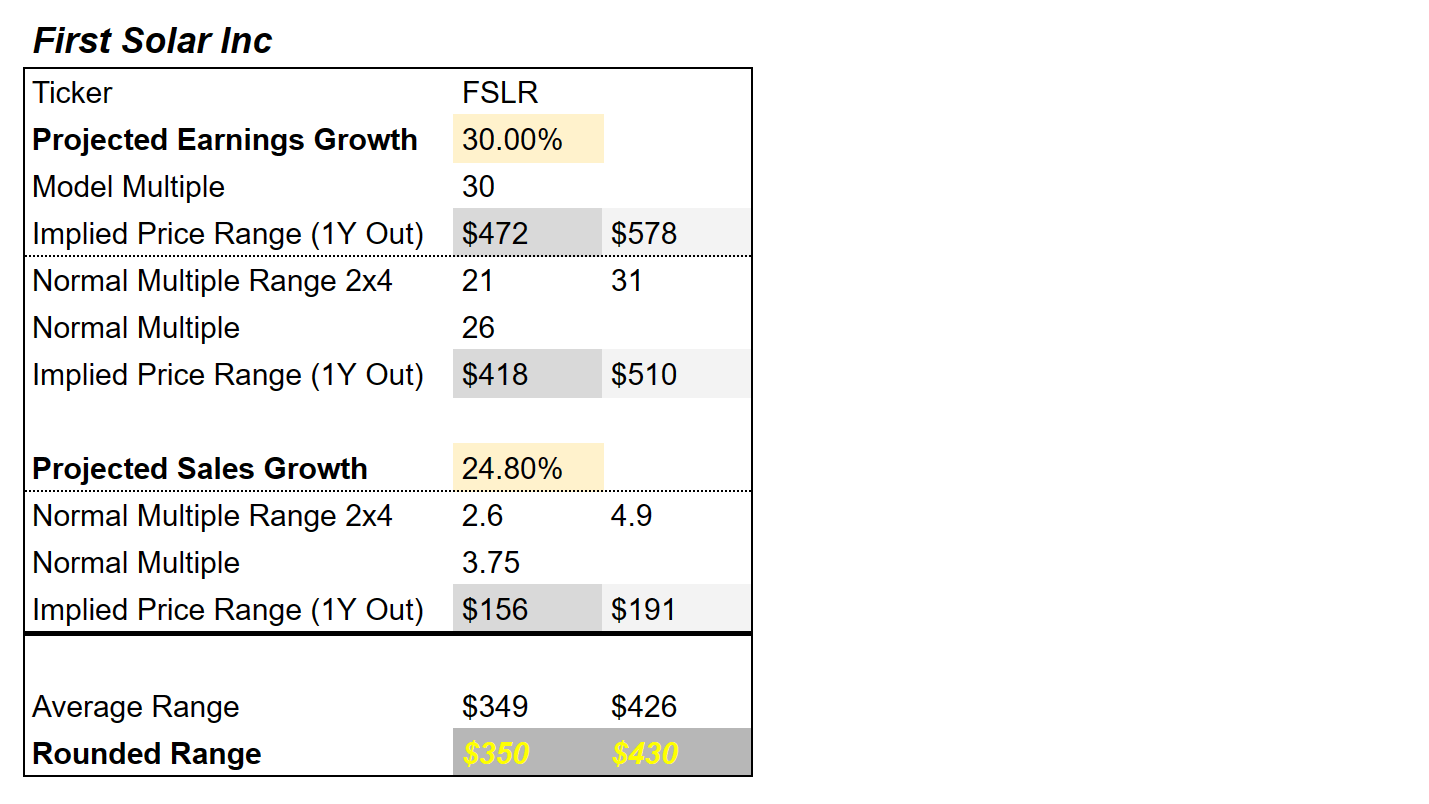

Looking extra, we see potential EPS progress of 30% averaged over the approaching years, which ends with a ensuing 1-year-out Honest Worth of $350 – $430 in our view:

PropNotes

The inventory presently trades for $185, which is considerably beneath this.

Thus, growth to what’s, in our view, a reasonably sure degree of progress and earnings, then, with a median / mannequin historic a number of on high of that, we do not assume our Honest Worth mannequin seems unreasonable going ahead:

FAST Graphs

It is true that the corporate’s historic gross sales a number of offers much less upside when seen in a vacuum, however as FSLR’s web earnings expands previous the $1 billion mark for the primary time, we expect the market will start to focus extra on the bottom-line outcomes, which may dramatically enhance the inventory as earnings multiples broaden to the expansion charge.

Dangers

The important thing danger right here to investing in FSLR is primarily political.

Chinese language photo voltaic producers are largely backed by the CCP, which implies that they will produce merchandise for a lot lower than different corporations in different international locations. This has led to a slew of solar dumping headlines as of late, which is primarily why we imagine that FSLR’s backlog and earnings potential is so discounted – destructive sentiment.

We predict that anti-dumping commerce protections will possible enhance FSLR’s aggressive place, however as we mentioned, even with out efficient blockers proper now, we expect FSLR’s model is robust sufficient to climate this pricing storm, particularly as a result of Cad-Tel’s power effectivity benefit, which permits utilities to provide the identical quantity power in a smaller bodily footprint.

The IRA subsidy of 0.7c per watt additionally ameliorates this danger considerably.

That stated, pricing, on the finish of the day, is the important thing danger in relation to the market, and if FSLR cannot compete, or proceed to construct its backlog, then it could run the chance of over-investing into unprofitable manufacturing capability, which may damage earnings, and the inventory, trying ahead.

One other danger is the chance that FSLR will not be capable to clear its backlog shortly or effectively, or in any other case fumbles in relation to execution, which may result in misplaced orders and decreased progress, revenues, and profitability.

The operational complexity wanted to scale up a PV panel manufacturing enterprise isn’t inconsequential, and FSLR wants to finish 2 extra factories this yr and subsequent to satisfy its manufacturing objectives.

In our thoughts, this danger is materials, which possible explains a number of the present low cost as nicely. Nonetheless, FSLR is not increasing into manufacturing facility quantity 2, it is increasing into factories 6 and seven. It is completed this earlier than. At this level, it stands to cause that administration is expert within the artwork of constructing and deploying manufacturing capabilities, which lowered this danger in our thoughts.

Thus, whereas there is a severe execution job in entrance of administration, we expect they’re as much as the problem, and can be prepared to entrust them with our capital as traders.

Abstract

All in all, although, we see FSLR’s EPS rising significantly over the approaching years as manufacturing improves and margins stay constant, which we expect ought to ship the inventory a lot greater, in direction of our Honest Worth estimate above $350 per share.

There are some dangers with Chinese language photo voltaic overcapacity, that are materials, however given FSLR’s distinctive worth proposition, robust model, and elevated deal with the core enterprise, we expect that the corporate ought to climate the storm nicely till simpler commerce protections are adopted.

Even when this does not occur, we expect FSLR continues to be a robust guess on the general clear tech progress and margin alternative.

Thus, our ‘Sturdy Purchase’ ranking.

Cheers!