PhonlamaiPhoto

Thesis

Fluence Power, Inc. (NASDAQ:FLNC) is a pure-play, Power Storage world chief. Particularly, the corporate supplies battery electrical storage techniques (BESS), software program options, and repair packages. I offered Fluence in a previous article and set a robust purchase score. Whereas nonetheless holding 75% of my long-term place, offering having been a purchaser at ~$6.75, I made a decision to promote ~25% of my place at ~$31 for a greater than profitable revenue (one of many few occasions I virtually completely timed a backside and a prime). This was momentum-and-valuation-related motion, and a possibility to lock in some income on the time. Nevertheless, I plan to carry the remainder of my place for the long term, because the BESS market progress remains to be within the early phases and Fluence is a number one participant. Thus, the earlier article’s details stand agency, and contemplating the latest worth drop, I reiterate my long-term robust purchase score.

Enterprise Replace

Fluence retains firing on all cylinders and just lately introduced 2 main mission wins in Australia (AGL and Origin), a big joint mission in Germany (the third in partnership with MW Storage), and one other giant mission within the UK.

- AGL Energy Limited 500 MW/1000 MWh vitality storage system for the Liddell Battery Challenge Power Restricted

- Origin Energy Limited 300 MW/650 MWh battery on the Mortlake Energy Station

- MW Storage 100 MW/200 MWh vitality storage system in Germany

- SSE Renewables 150 MW/300 MWh vitality storage system at Fiddler’s Ferry former coal energy station, Warrington (UK)

The corporate has developed Ultrastack and Gridstack Professional, so as to add to its Gridstack, Sunstack, and Edgestack vitality storage techniques whereas additional optimising Nispera, and Mosaic on the software program entrance which brings in recurring and better revenue margin income. Its operational service packages full Fluence’s built-in vitality storage options.

Fluence has labored its provide chain diversification into a bonus and has already secured battery provide for the subsequent two years. Moreover, the Utah facility (eligible for IRA manufacturing tax credit score) is anticipated to start out manufacturing this summer time. Fluence will even profit from an asset-lite regional manufacturing strategy (presently 2 contract producers, within the US and Vietnam).

Lastly, it is value mentioning that the corporate was just lately included within the Forbes annual listing of America’s Most Successful Mid-Cap Companies (#37).

Regardless of these information, Fluence confronted two unlucky occasions just lately.

- Litigation between Fluence and Diablo Power Storage, an LS Energy affiliate regarding the mission in Pittsburg, California. Fluence filed a grievance searching for ~$37M from the defendants whereas Diablo later filed a cross-complaint searching for a minimal of ~$25M (as much as ~$230M). Fluence dismissed the allegations and urged it to take the actions wanted to guard its pursuits.

- A short report revealed by Blue Orca Capital. Fluence issued a response addressing its most vital allegations.

Fluence 03/2024 Investor Presentation

Q1 2024 ER / FY 2024 Steerage

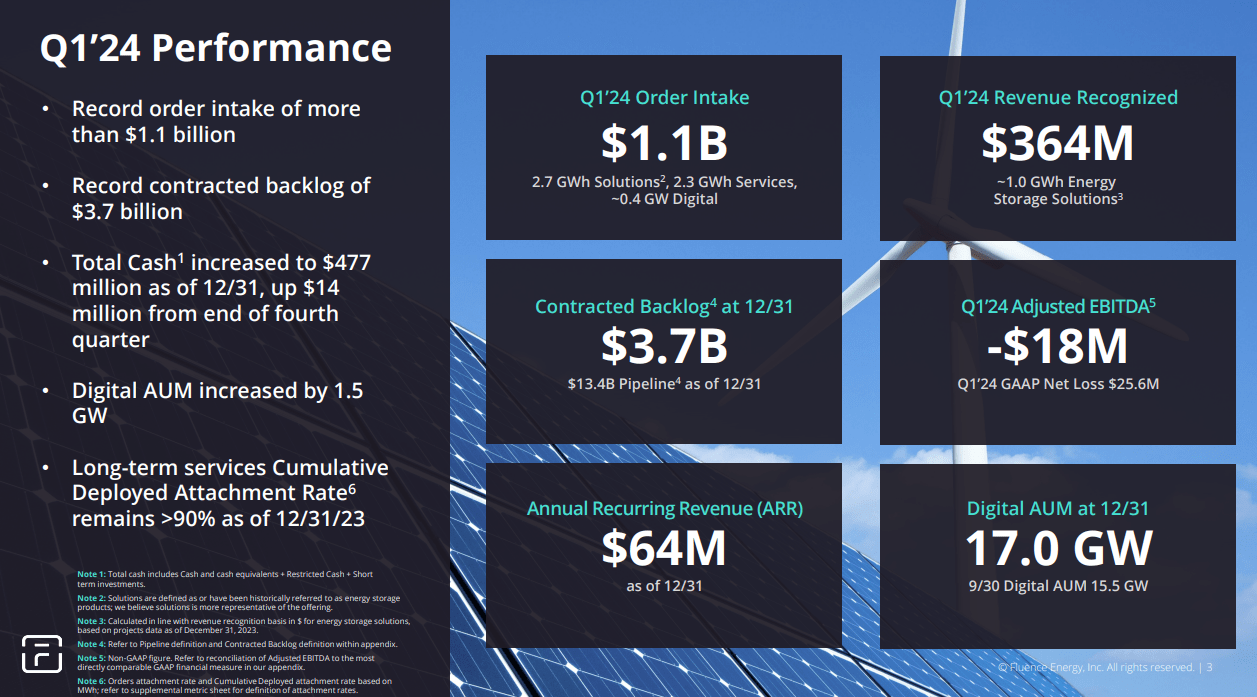

On 02/07/2024 the corporate announced one other strong ER for its Q1 2024 (ending 12/31/2024).

- Income of $364M, elevated 17% q-o-q.

- GAAP gross revenue margin of 10%, vs ~3.9% for Q1 2023.

- Internet lack of ~$25.6M, vs ~$37.2M for Q1 2023.

- Adjusted EBITDA of ~-$18.3M, vs ~-$26.1M for Q1 2023.

- Contracted backlog stood at ~$3.7B as of 12/31/2023, elevated by $0.8B in comparison with 09/30/2023.

- Complete Money of roughly $477 million, elevated by ~$16M in comparison with 09/30/2023.

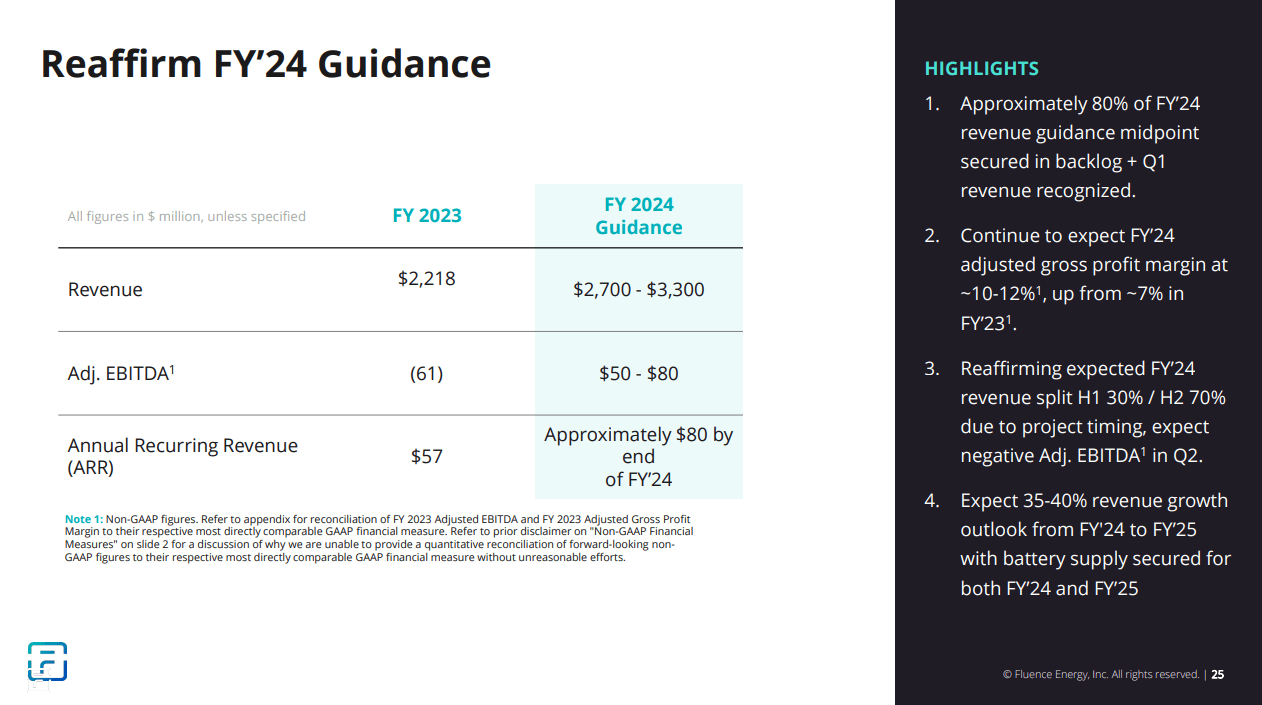

The corporate is dedicated to reaching and sustaining worthwhile progress from 2024 onwards. Fluence expects $2.7B to $3.3B complete income, $50M to $80M adjusted EBITDA, and ~$80M annual recurring income for FY 2024.

Fluence 03/2024 Investor Presentation

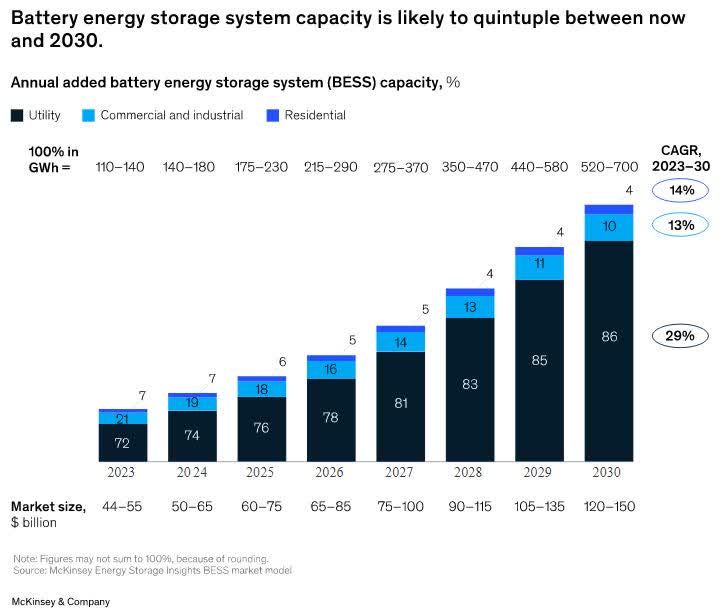

The BESS market alternative

The BESS improvement remains to be in its early phases. Fluence, a worldwide BESS chief, will profit from that pattern for the years to come back. Particularly relating to utility-scale initiatives, a Fluence power, the demand will skyrocket and the CAGR is anticipated to the touch 30% by 2030. Fluence expects at the least ~35% CAGR for 2024 and 2025.

McKinsey Power Storage Insights BESS Market Mannequin

Valuation

Offering Fluence is within the progress stage, Value/Gross sales ratio is suitable to worth the corporate. Based on Seeking Alpha Metrics, the P/S (TTM) ratio is ~0.87 whereas the Industrials sector median is ~1.54, exhibiting that Fluence is considerably undervalued. Particularly, Fluence is presently buying and selling at ~$16.61 per share whereas the sector median exhibits that the inventory might have been buying and selling at ~$29.40 which might be thought-about a good valuation. The quick report and a worst-case situation regarding the Diablo case appear to have affected the inventory worth and may very well be thought-about priced in. Moreover, the corporate’s progress prospects, wholesome financials, and main BESS market place might assist an excellent greater than the sector median valuation.

From a long-term perspective, on the way in which to 2030, my beforehand set goal worth of ~$53.82 nonetheless stands and will even be thought-about conservative.

- Assuming a ten% CAGR Fluence would produce a $5.31B income in 2030, and making use of the present sector median P/S (TTM) ratio of 1.54, might assist a $8.18B valuation (~$45.29 worth per share).

- Assuming a 20% CAGR Fluence would produce a $8.96B income in 2030, and making use of the present sector median P/S (TTM) ratio of 1.54, might assist a $13.8B valuation (~$76.41 worth per share).

- Assuming a 30% CAGR Fluence would produce a $14.48B income in 2030, and making use of the present sector median P/S (TTM) ratio of 1.54, might assist a $22.3B valuation (~$123.47 worth per share)

As talked about, Fluence expects at the least a 35% CAGR for 2024 and 2025.

Dangers

Sure dangers might seem alongside the way in which and ought to be in buyers’ minds.

- Sure provide chain bottlenecks might seem, reminiscent of a Center East disaster or the Purple Sea route disruption presently.

- Uncooked supplies prices might enhance.

- Inexperienced transition politics/laws might change.

- Opponents might acquire a larger-than-expected market share.

- A better-for-longer price atmosphere might hassle potential purchasers.

- The Diablo case might have an effect on the corporate’s financials and fame.

Conclusion

Briefly, Fluence expects ~$3B in income and constructive EBITDA for 2024 whereas presently buying and selling at a ~$3B market cap; a poor valuation for an Power Storage chief, net-debt adverse, rising in a booming trade. The quick report could have triggered short-term volatility however I do not consider it may possibly hurt the corporate so long as it retains up the tempo. As well as, relating to the authorized matter of the Diablo mission, the market punished the inventory assuming a worst-case situation. Siemens (OTCPK:SIEGY), AES (AES), and the QIA will probably shield their funding/partnership as a result of they anticipate benefiting from this standing, in any other case, they might be taking pictures their very own toes. Present buying and selling ranges or, even higher, decrease ought to be seen as a shopping for alternative. Buyers ought to exploit any weak point within the share worth to provoke or enhance their positions with a long-term goal at all-time highs.