The economic data today was focusing Canada where retail sales rose by a higher-than-expected 0.9% but you should prices were lower than expectations.

In the US, two-days after the FOMC rate decision to cut rates by 50 basis points, Feds Waller – normally a more hawkish member – spoke on CNBC. His comments were thought to be more dovish as the Fed recalibrates policy with inflation lower and potential for unemployment to move higher.

Fed Governor Chris Waller stated that the economy remains strong, and inflation is coming down. He expressed openness to front-loading rate cuts based on inflation data, especially during a recent blackout period. Waller noted that the core PCE inflation has been running at 1.8% over the past four months but would be closer to 1% if housing services are excluded. He outlined multiple potential scenarios for rate cuts, which could be gradual, faster, or even paused, depending on the incoming data. While inflation is softer than he initially expected, Waller indicated that he might be more aggressive in cutting rates if the data supports it. He also cautioned that inflation could reverse, though he believes it is currently on the right path.

A quotable from the Fed Governor:

“The committee sees a lot of room to move down over the next 6-12 months. That’s really what we should be focusing on.”

Philadelphia Fed Pres. Harker also gave a speech and commented that the Federal Reserve has done a good job navigating the economy. He compared monetary policy to driving a bus, where it’s important to balance speed. Harker emphasized that maximum employment involves job quality, not just quantity, and highlighted the importance of both “hard” and “soft” data in the Fed’s decision-making. He also noted the Fed’s role in bank supervision, financial stability, and its exploration of emerging technologies like AI and quantum computing in finance. Later, Harker warned that there is a risk that the decline in inflation could stall and that the labor market could soften. His comments were ho-hom.

Finally, Fed Governor Michelle Bowman commented after being the first dissenter on the Fed Board since 2005, when she preferred a 25 basis point cut to a 50 basis point cut. Bowman expressed her support for recalibrating the Fed funds rate but preferred a smaller initial move. She sees a risk that the FOMC’s larger policy action could be interpreted as prematurely declaring victory over inflation, noting that the inflation target has not yet been met. Bowman advocates for a measured pace toward a neutral policy stance to continue progress in bringing inflation back to the 2% goal without unnecessarily increasing demand. She emphasized that the economy remains strong, with the labor market near full employment, and expressed her respect for colleagues who supported a larger rate reduction, remaining committed to working with them to achieve the Fed’s dual mandate goals.

I’m sure next week we will get a slew of commentary from various Fed officials. The Fed does not meet again until November 7-8 immediately after the US election.

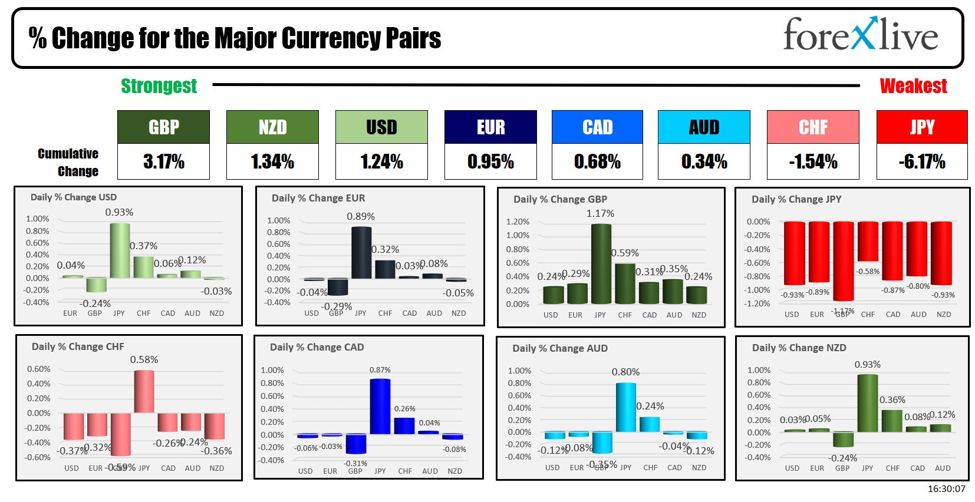

Looking at the forex market today, the GBP is ending the day as the strongest of the major currencies, while the JPY is the weakest. THe USD ends the week with gains versus the JPY, CHF, and AUD. The greenback was near unchanged versus the EUR, CAD and NZD and was mostly lower verse the GBP.

The BOE kept rates unchanged on Thursday and had higher retail sales released today.

The BOJ also kept rates unchanged when they announced their decision today, but it was more of a dovish policy view. The JPY fell by -0.93% vs the USD and the NZD, and by -1.17% vs the GBP. The JPY fell by -0.58% to- 0.89% vs the other currencies.

Below is a view of the strongest to the weakest of the major currencies today.

US stocks closed the session mixed:

- Dow industrial average rose 38.17 points or 0.09% at 42063.36

- S&P index fell -11.09 points or -0.19% at 5702.55

- NASDAQ index fell -65.66 points or -0.36% at 17948.32

The small-cap Russell 2000 fell -24.81 points or -1.10% at 2227.88

For the week:

- Dow industrial average rose 1.62%

- S&P index rose 1.36%

- Nasdaq index rose 1.49%

- Russell 2000 rose 2.08% despite the 1% decline today

In the Europe, the closes were lower:

- German DAX -1.4%

- France’s CAC -1.5%

- UK’s FTSE 100 -1.2%

- Spain’s IBEX -0.1%

- Italy’s FTSE MIB -0.8%