- Record closes for the NASDAQ and S&P index

- The private crude oil weekly inventory data will be released at 4:30 PM ET

- Crude futures settle at $79.26

- Bank of England’s Bailey: Thinks the next on rates will be a cut

- How will the catastrophe in Iran shake markets?

- Fed Gov. Waller on CNBC: The data looks like we don’t need to raise rates

- European major indices close lower on the day

- ECBs Nagel: June rate cut doesn’t mean ECB will cut in subsequent meetings

- Fed Gov. Barr: Overall, the US economy is quite strong

- Ethereum ETF Approval Boosts Ether’s Value; SEC Signals Positive Stance

- Treasury Secretary Yellen: Concerns about China strategy are shared among G-7 finance

- New Zealand global dairy trade prices rise 3.3%

- The RBNZ rate decision is ahead. What is the technical roadmap for traders?

- More from a Fed Gov. Waller: I just do not see rate hikes happening

- More from Fed Gov. Waller: Probability of a recession seems to have disappeared

- Amazon halts orders of Nvidia “superchip” to await updated model

- Fed Gov. Waller: Wants to see several more months of good inflation data

- Fed Atlanta Fed Pres. Bostic: Fed’s high priority is to get inflation back to 2%

- Kickstart the FX trading day for May21 w/a technical look at the EURUSD, USDJPY and GBPUSD

- Canada April CPI 2.7% versus 2.7% expected

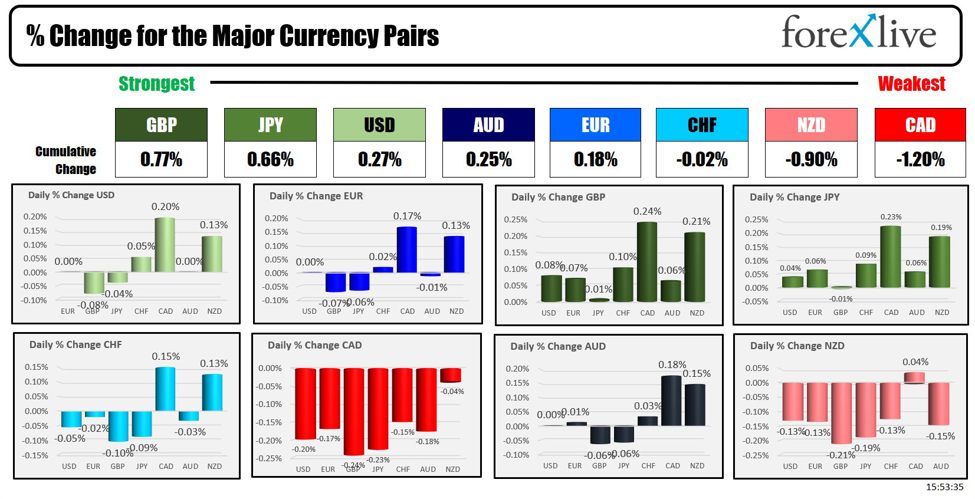

- The CHF is the strongest and the NZD is the weakest as the NA session begins

- ForexLive European FX news wrap: Currencies little changed, Ether surges

For the second consecutive day, there were no economic releases in the US. Instead, Fedspeak was the only fundamental influence and even so, what was said, was not all that different from prior Fed officials

At the end of the day five of the seven major currency pairs – the EURUSD, GBPUSD, USDCHF, AUDUSD and NZDUSD all had trading ranges of only 40 pips or less indicative of a quiet market. Moreover price action was more up-and-down versus trending.

Even the USDCAD which did benefit from a volatility standpoint due to the softer CPI data and the expectations that it may be good enough for the Bank of Canada to cut rates in June (it certainly didn’t hurt those chances). Nevertheless gave up a good portion of the gains (lower CAD). Nevertheless the CAD is ending the day is the weakest of the major currencies, while the GBP and JPY are vying for the strongest.

As far as the Fedspeak:

- Fed’s Bostic emphasized caution in cutting rates, stating he is “not in a hurry” and wants policy easing to be “unambiguous.” He prefers to wait longer to avoid inflation fluctuations and stoking excessive investment. Despite businesses’ confidence in the economy, they have less pricing power than six months ago. Bostic noted improvements in supply chains and hopes for continued goods deflation, expecting inflation to decline slowly without a rate cut before the fourth quarter. The Fed’s top priority is reducing inflation to 2%, and while monetary policy’s efficacy may be weaker, it is still impacting rate-sensitive sectors and delaying investment. He remains optimistic about the economy’s solid performance in the next year or two.

- Meanwhile Fed Governor Waller was busy speaking at an event and later on CNBC. His comments were perceived to be less hawkish than his recent comments due to slower growth and signs of slowing inflation. He reiterated comments from Fed;s Powell, that he does not see a hike in rates but said that needs several more months of positive inflation data before supporting policy easing. He highlighted that credit card and auto loan delinquency rates indicate some consumer stress. He said that you will closely monitor private domestic final purchases in Q2. While wage growth is slightly higher than desired, it’s not excessively high. Spending and labor market data suggest current monetary policy is suitable to reduce inflation, which isn’t accelerating. April data shows modest progress towards the 2% inflation target. Waller noted the probability of a recession has diminished, with the 10-year Treasury rate reflecting tightening effects. He emphasized ensuring inflation trends downward, potential policy pressure on demand, and concerns over deficit spending impacting rates.

- Finally, Fed Governor Barr stated that the overall US economy is quite strong, but the Fed still needs to address inflation and must maintain tight policy for longer than previously anticipated. He highlighted the need to manage interest-rate risk. Barr reiterated that Q1 inflation was disappointing and did not provide the confidence needed to ease monetary policy. The Fed believes that maintaining the current tight policy is necessary and is in a good position to monitor the economy. He acknowledged that the Fed remains vigilant to the risks associated with both inflation and employment mandates, considering their current approach prudent for managing these risks.

Looking at other markets:

- US stock indices rose modestly, but the gains were good enough for record closes in the S&P and NASDAQ index. Tomorrow the Nvidia earnings will dominate when they are released after the close. Today in anticipation, Nvidia continued its move to the upside with a gain of $6.06 or 0.64% to a new record closing level at $953.86. Microsoft also close higher with a gain of 0.87%. The Dow industrial average ended the day with a gain of 0.17%. The S&P index rose by 0.25%, and the NASDAQ index rose by 0.22%.

- In the US debt market, yields are ending the day lower the 2-year down -0.6 basis points, the 10 year yield down -2.5 basis points, and the 30-year down -0.24 basis points. Tomorrow the U.S. Treasury walked off 20 year bonds at 1 PM ET

- The price of bitcoin is closing back below the $70,000 level after trading as high as $71,958. It is trading at $69,156. Ethereum, however, continued its run to the upside with a gain of 6.95% which comes off a gain of 13.3% in trading yesterday. Traders are responding to expectations that the SEC will approve of a Ethereum ETF.

Gold is trading down $3.65 or -0.15% at $2421.25. Silver is trading up $0.18 at $31.99. That is the highest level since December 2012.

This article was written by Greg Michalowski at www.forexlive.com.