The USD moved higher on risk-on sentiment which saw stocks in the US move solidly higher to start the holiday-shortened week.

The final numbers are showing:

- Dow industrial average rose 740.58 points or 1.78% at 42343.65. At session lows the index was up 245.97 points.

- S&P index rose 118.72 points or 2.05% at 5921.54. At session lows the index rose was up 51.25 points

- NASDAQ index rose 461.96 points or 2.47% at 19199.16. At session lows the index was up 224.48 points

The S&P index is now positive on the year by 0.68%. The NASDAQ index is still modestly lower by -0.58%. The Dow industrial average is down -0.47% for 2025.

In the US debt market yields moved lower with the long end outperforming:

- 2-year yield 3.980%, -0.6 basis points

- 5-year yield 4.035%, -4.1 basis points

- 10-year yield 4.443%, -6.7 basis points

- 30 year yield 4.950%, -8.7 basis points.

Yields moved lower on the day, despite a strong rebound in consumer sentiment, with the Conference Board Consumer Confidence Index rising to 98, well above both the 87 estimate and last month’s 85.7 reading. However, other economic data painted a more mixed picture.

The Case-Shiller Home Price Index showed a modest decline of -0.1%, falling short of the +0.3% forecast. Meanwhile, durable goods orders (advance) dropped -6.3%, which was better than expectations of a -7.8% decline. Excluding transportation, orders rose 0.2%, reflecting the outsized impact of large-ticket transportation items.

Notably, non-defense capital goods orders excluding aircraft—a key proxy for business investment—fell -1.3%, sharply below the -0.1% estimate. This decline underscores growing caution among businesses, likely driven by uncertainty around tariffs and trade policy.

Fed’s Barkin spoke today and described the U.S. economy as remaining on a similar path as the past couple of years, with low unemployment and inflation gradually easing toward target. He noted that businesses are cautious, citing hiring freezes and delayed investment, though he doesn’t see evidence of outright cancellations. Barkin emphasized business sentiment as a key forward-looking indicator.

On the consumer side, he pointed out that although inflation expectations are weighing on sentiment, real-time data does not yet show a drop in spending. He also mentioned that government spending cuts are starting to impact employment, particularly in the D.C. area.

Regarding Trump’s tariff policies, Barkin said the effects on inflation and employment appear balanced so far. Businesses are responding in two ways—stockpiling inventories or cutting imports—but it’s too early to assess the full economic impact.

Overall tone: Cautiously neutral, with a wait-and-see approach to how businesses and consumers react to evolving inflation and policy changes.

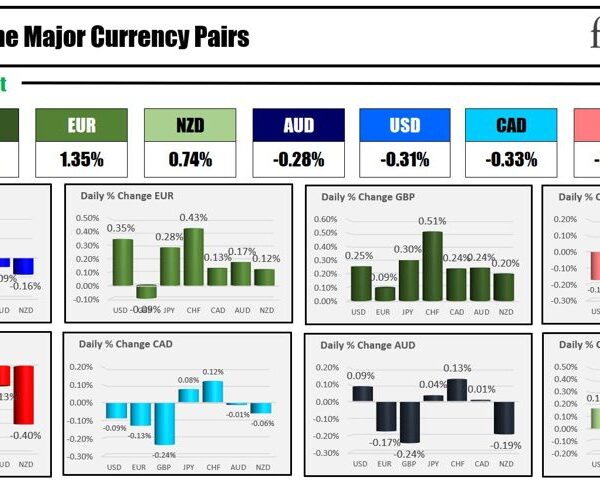

Looking at the US dollar, the greenback was higher vs the major currencies today, led by a 1% gain vs the JPY. The USDJPY is closing above the 200-hour MA at 144.077 (at 144.346).

The EURUSD is closing below its 100 hour MA at 1.1344 but short of the 50% midpoint of the range since the April high. That level comes in at 1.1318. Teh current price comes in at 1.1326.

The GBPUSD is lower and is testing its 100 hour MA at 1.3497 going into the new trading day. That will be a key barometer in the new trading day. Staying above is more bullish. Moving below, increases the sellers bias.

The RBNZ is expected to cut rates by 25 basis points in the new trading day. The 100/200 bar MA on the 4-hour chart and the 200 hour MA are all converged near 0.5935. The current price is at 0.5942. That cluster will be the key barometer for buyers and sellers in the new trading day.

Good fortune with your trading.

ForexLive.com

is evolving into

investingLive.com, a new destination for intelligent market updates and smarter

decision-making for investors and traders alike.