The USD is ending the session decrease to finish the buying and selling week with a lot of the declines coming vs the AUD and the NZD. In a single day, ANZ reported that’s now predicts that the Reserve Financial institution of New Zealand (RBNZ) will enhance the Official Money Fee (OCR) by 25 foundation factors in each February and April, bringing it to a complete of 6%, which deviates from the consensus view. This forecast is predicated on a sequence of small, however unwelcome surprises in financial information, main ANZ to imagine that the RBNZ is not going to really feel assured that it has sufficiently met its inflation targets. The OCR is at present at 5.5%, and whereas the market is essentially anticipating the RBNZ to take care of charges within the upcoming February assembly, with a 90% anticipation of a maintain choice, ANZ stands out by anticipating price hikes in each the February 28 and April 10 conferences.

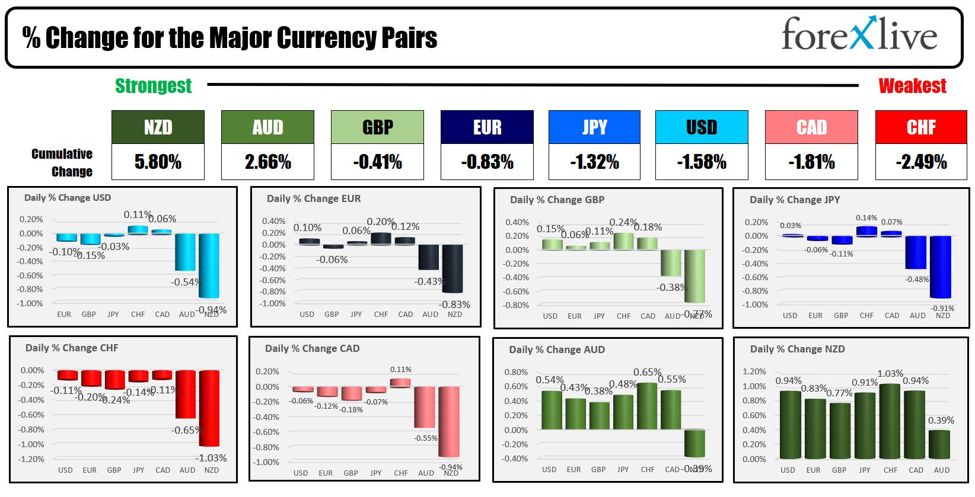

That information helped to propel the NZDUSD to a close to 1% achieve on the day. The AUDUSD moved up 0.54%. The USD was combined vs the opposite currencies in a subdued up and down buying and selling session within the US. Total, for the day, the NZD was the strongest of the foremost currencies whereas the CHF was the weakest.

The strongest to the weakest of the foremost currencies

Within the session as we speak, the Canada employment information confirmed a achieve of 37.6K however all of the achieve was partly time jobs. Full time jobs fell by -11.6K. The unemployment price did fall to five.7% from 5.8% final month. The USDCAD ended the day little modified in up and down buying and selling.

There have been no US financial information as we speak. Nevertheless, there was some extra Fed speak from Fed’s Logan and Bostic.

Fed’s Logan emphasised that the labor market stays very tight, though there are indicators of loosening, signaling a nuanced view of present financial circumstances. She acknowledged important progress made on inflation however famous that additional efforts are essential to totally tackle it. Logan advocated for a cautious and data-driven method, suggesting there isn’t a quick urgency to regulate rates of interest presently. Her feedback replicate a precedence on constructing confidence within the long-term stability of inflation charges. Whereas she famous that offer chains have largely normalized, Logan additionally acknowledged ongoing provide chain points in sure industries, indicating these may have extra time to resolve absolutely. She expressed a powerful give attention to monitoring potential dangers that might undermine progress on inflation, highlighting the Fed’s vigilance in sustaining financial stability.

Fed’s Bostic, in a dialogue with NPR, expressed concern that inflation has been excessively excessive for an prolonged interval. He conveyed optimism about the USA being on monitor to regain its pre-pandemic financial vitality, emphasizing the significance of stopping a brand new surge in inflation. Bostic highlighted that present information point out the potential for continued actual wage good points over the subsequent a number of months. He identified that companies are primarily challenged by difficulties to find workers and inexpensive housing. Moreover, Bostic reassured that banks are conscious of the dangers current of their portfolios and are outfitted to handle them successfully, suggesting a degree of preparedness throughout the banking sector to navigate potential financial fluctuations.

For the buying and selling week, the US greenback index rose 0.10% (DXY) however was combined vs the foremost currencies. Wanting on the main currencies, the USD was just about unchanged vs the EUR and GBP, it was the strongest vs the CHF and the weakest vs the NZD:

- EUR, unchanged

- JPY, +0.65%

- GBP, unchanged

- CHF, +0.90%

- CAD, -0.02%

- AUD, -0.20%

- NZD, -1.49%

At this time, yields have been combined with the shorter finish greater, and the longer finish decrease.

- 2-year 4.484%, +2.8 foundation factors

- 5-year, 4.140%, +1.6 foundation factors

- 10-year, 4.177%, +0.7 foundation factors

- 30 yr, 4.374%, -0.6 foundation factors

For the buying and selling week, yields moved greater because the market began to dial again the variety of tightening.

- 2 yr, +11.4 foundation factors

- 5 yr, +15.4 foundation factors

- 10 yr, +15.3 foundation factors

- 30 yr, +15.1 foundation factors

US shares as we speak continued it transfer to the upside with strong good points for the broader indices. The S&P index closed above the 5000 degree for the primary time ever. The Nasdaq index traded above 16K for the primary time since November 2021. The S&P closed at a file degree and though the Dow as decrease as we speak, it traded to file ranges this week.

The ultimate numbers are exhibiting:

- Dow industrial common fell -54.64 factors or -0.14% at 38671.70

- S&P rose 28.70 factors or 0.57% at 5026.62

- Nasdaq rose 196.94 factors or 1.25% at 15990.65

For the week, the foremost indices closed greater for the fifth week in a row after beginning 2024 with a pointy decline within the 1st buying and selling week of the yr.

- Dow industrial common, rose 0.04%

- S&P rose 1.37%

- Nasdaq rose 2.31%

In different markets this week,

- Crude oil rose $4.26 or 5.89% to $76.54

- Gold fell -$15.02 or -0.74% to $2024.42

- Silver fell $0.08 or -0.34%

- Bitcoin surged by $4975 or 11.6% as threat on flows pushed the digital forex greater.

Subsequent week US CPI will spotlight the financial releases

Monday:

Tuesday:

- NZ inflation expectations

- UK Employment

- US CPI

Wednesday:

- UK CPI

- UK Gov. Bailey speaks

Thursday:

- AUD employment

- UK GDP

- US Retail Gross sales

- US unemployment claims

Friday:

- UK Retail gross sales

- US PPI

- US Michigan Client Sentiment.

On the earnings calendar subsequent week, Shopify, Coca Cola, AIG, Cisco and Coinbase are corporations of curiosity. The Huge Daddy of maybe the whole earnings season might be launched on February 21, when Nvidia is scheduled to report. The destiny of AI and Ai shares rests with the chip provider:

Tuesday:

- Shopify

- Coca Cola

- Marriott

- Lyft

- AIG

Wednesday:

- Kraft Heinz

- Albemarle

- Twillio

- Cisco

Thursday:

Thanks on your help. Wishing you all a terrific weekend.