The North American session was initially highlighted by the weekly initial jobless claims. They came in higher than expectations at 231K vs 215K estimate. That was thehighest level since November 2023. It is just one week, and the spikes tend to be some funky seasonal. Easter was early this year and that may have been an influence. It will take a few more weeks to figure out whether it was a fluky number or the start of a new trend for jobs/employment. With the US NFP jobs showing weakness last Friday, today’s report did catch the markets attention.

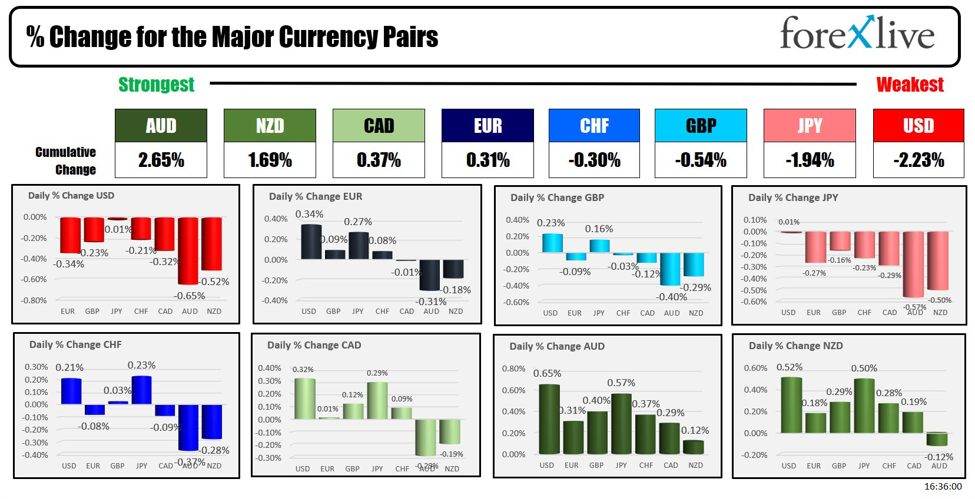

At the end of the day, the USD is ending the day as the weakest of the major currencies reversing declines and more from yesterday’s gains (the USD was the strongest of the major currencies yesterday).

The AUD is ending the day as the strongest of the major currencies.

The USD was the weakest of the major currencies today.

The other key event was the Bank of England rate decision. The BOE kept rates unchanged as expected, but by a of vote of 7-2. The 2 dissenters were in favor of easing policy by 25 basis points.

In his press conference, Governor Bailey highlighted various insights. He noted increased skepticism among businesses about their ability to pass on higher wage costs (good for inflation), reflecting broader economic uncertainties. Bailey emphasized that recent market movements in interest rate expectations were largely influenced by U.S. actions, with UK inflation dynamics differing significantly. He also pointed out issues with labor force participation data, making it difficult to assess real-time economic changes.

Bailey expressed that while the BoE is not yet at a point to cut rates, it is likely that rate cuts will be necessary in the coming quarters and could be more substantial than the market currently anticipates (that was a surprise). He did caution that the rate decisions will be data-dependent. Bailey affirmed that the monetary policy is effectively steering inflation towards the target, but he anticipates a potential uptick in inflation in the latter half of the year. Despite the higher than expected wage and service inflation since February, he cautioned against overinterpreting these signals, underscoring the expectation that the secondary effects on domestic wages and prices will diminish quicker than previously thought.

Overall, the comments were more dovish. And although the GBP had a tilt to the downside, the pound still rose vs the USD (by 0.23%) and the JPY (by 0.16%) at the end of the day.

Later in the day, BOE’s policymaker Pill indicated that while there is increased confidence in beginning to ease policy restrictions, the time to act has not yet arrived. The decision to reduce rates is pending further data and is contingent on the absence of significant economic disruptions. Pill emphasized that the consideration for rate cuts could occur over the coming months, underlining the importance of being data-dependent in their approach. Additionally, he noted that the process of reducing inflation is still ongoing, necessitating the maintenance of some level of economic restriction for the time being.

ECBs deGuindos was also chirping today and suggested that the future landscape of inflation is likely to be shaped by the slowdown in globalization and the regionalization of markets, leading to potentially higher inflation rates than previously experienced. This is particularly relevant in the context of Europe post-Russia’s invasion of Ukraine, where there is an expected shift in economic priorities from civilian needs (‘butter’) to military expenditure (‘cannons’), which could result in higher inflation and modestly slower growth. Additionally, while the European Central Bank (ECB) operates independently of the Federal Reserve, global policy interconnections remain significant, especially considering the influence of the U.S. dollar and differing fiscal policies between the U.S. and the eurozone. Notably, the U.S. maintains a lower unemployment rate despite more costly fiscal measures. The decision on future rate cuts by the ECB will hinge on various factors, including wage trends and potential adjustments in financial markets

In the US, Federal Reserve Bank of San Francisco President Mary Daly, who is a voting member, has shared her insights after the recent FOMC rate decision, reflected on the complexities and uncertainties in the current economic landscape, particularly concerning inflation. Daly noted that the past three months have injected considerable uncertainty about the inflation outlook for the upcoming months. She highlighted a range of potential scenarios the Fed is currently considering, mentioning mixed signals from businesses about consumer demand and input prices.

Daly emphasized that the Fed’s balance sheet provides no clear indications about future monetary policy directions and that while the trajectory of the economy is uncertain, the Fed is prepared to respond to various potential developments. Despite concerns, she remarked that there is no current evidence suggesting that the labor market is reaching a problematic stage. Instead, she sees a robust labor market coupled with persistently high inflation, and she cautioned against relying on productivity gains alone to curb inflation.

Further comments detailed that while Fed policy remains restrictive, it may take some time to effectively reduce inflation. Daly pointed out that while the labor market is showing signs of cooling, this is expected and aligns with a return to more normal conditions. She acknowledged ongoing disinflation, though progress is slower than last year, and noted improvements in supply chains. Daly concluded by underscoring the absence of any necessity for drastic measures to depress the economy, as the current indicators do not warrant such actions.

Technically, the EURUSD is closing near the highs for the day at 1.0781 and is just a few pips away from its 50% midpoint of the move down from the March high. That level comes in at 1.07906. The 200-day moving average is also just above at 1.0793. In the new trading day getting above those levels would increase a bullish bias. Staying below, could lead to more selling.

The GBPUSD is also stretching to new highs at the close and testing a key cluster of technical levels. The 100 and 200-hour moving average and 38.2% retracement of the move down from the March high comes in at 1.25255. Above that is the 200-bar MA on the 4-hour chart at 1.2535 and the 200 day moving average of 1.25421. In the new day, that area will be resistance and a potential risk defining level for sellers looking to sell a rally. Remember, the BOE was more dovish.

The USDJPY retraced its earlier gains slowly during the US session, and is closing near unchanged on the day. On the downside, the 200-hour moving average comes at 155.227 (the current price is trading at 155.469). It would take a move below that MA level to give the seller more confidence in the new trading day.

In the US stock market, the Dow industrial average rose for its seventh consecutive day, the S&P index closed at its highest level in over a month and the NASDAQ index snapped it’s 2-day decline.

- Dow industrial average rose 0.85%

- S&P index rose 0.51%

- NASDAQ index rose 0.27%

In the US treasury market today, yields are closing lower after trading higher earlier in the day. Also helping the bullish tone in the bond market was a solid 30-year bond auction (I gave it a B grade). At the end of day:

- 2-year yield 4.817%, -2.5 basis points

- 5-year yield 4.472%, -2.9 basis points

- 10 year yield 4.459%, -2.4 basis points

- 30-year yield 4.612%, -1.9 basis points

Thank you for your support. Traders in the Asian-Pacific market, wishing you a happy and healthy weekend.

Tomorrow the Michigan consumer sentiment will be released (final).