- Is Crude Oil Futures a Buy or Sell today (06 Jan, 2025)?

- Is Gold Futures a Buy or Sell Today (06 Jan, 2025)?

- Bank of America see potential for a strong China equity rally in H2 2025

- PBOC is set to issue a record volume of offshore yuan bills in Hong Kong this month

- Goldman Sachs trim its gold forecasts, gold not to reach US$3000 in 2025

- North Korea has fired another ballistic missile

- Trudeau likely to resign, but has not yet made a final decision

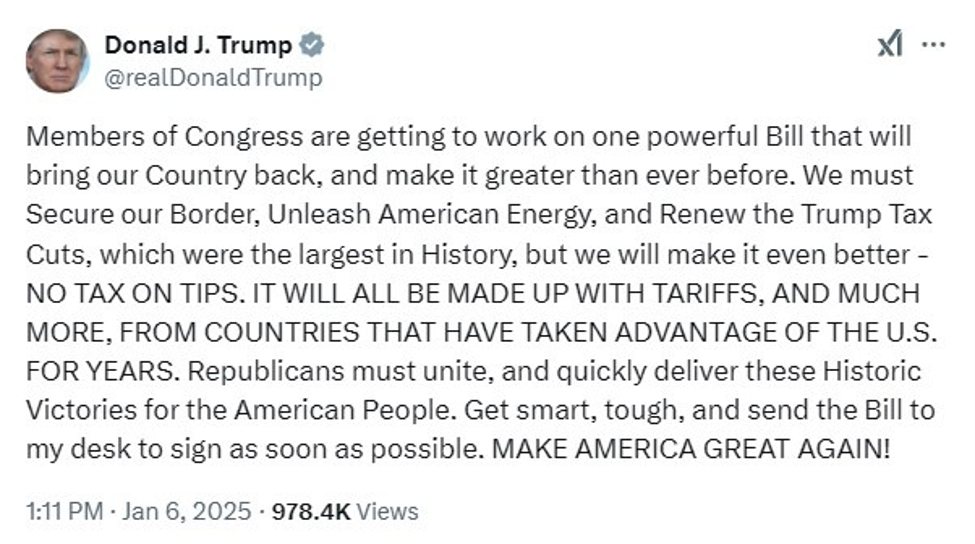

- Trump insistent on tariffs, tax cuts, US energy

- Bank of Japan Governor Ueda gives little clue on timing of rate hikes – data dependent

- CAD is pumping stronger to open the new week

- China December Caixin Services PMI 52.2 (vs. 51.5 in November)

- Shanghai Stock Exchange vows to deepen capital markets opening

- CAD PM Trudeau expected to announce resignation before national caucus meeting Wednesday

- China financial media says PBoC statement sends stronger signal on stable yuan FX rate

- PBOC sets USD/ CNY reference rate for today at 7.1876 (vs. expectations of > 7.20)

- All eyes on the PBoC yuan reference rate today – will it be above 7.20?

- MUFG expect EUR/USD under parity – Trump tariffs to hit quickly

- Japan final services PMI (December 2024 ): 50.9 (prior 50.5)

- UBS says take a cautious view of Chinese equities – consumption weak, upcoming US tariffs

- MUFG bearish GBP, cite Bank of England cuts to come, gas price vulnerability

- UK news – Over half of businesses plan to raise prices in the next three months.

- Weekend – People’s Bank of China pledged more stimulus to boost consumption

- RBA Australian dollar intervention potential getting some attention (ps. not gonna happen)

- Australia Judo Bank Services PMI for December 50.8 (prior 50.5)

- China’s services PMI data due: What to expect & how its likely to impact equities and yuan

- Trade ideas thread – Monday, 6 January, insightful charts, technical analysis, ideas

- Monday morning open levels – indicative forex prices – 06 January 2025

- Weekly Market Outlook (06-10 January)

- Trudeau expected to resign ‘by Monday’ – report

- Fed’s Kugler: Job not done on inflation

- Newsquawk Week Ahead: US NFP, FOMC Minutes, ISM Services PMI, China and EZ inflation

Over

the weekend we had comments from Federal Reserve Board Governor

Adriana Kugler along with Federal Reserve Bank of San Francisco

President Mary Daly saying that while progress had been made on

bringing down inflation there was still work to be done. The

assessment seemed to weigh on gold during the session here, keeping

it under US$2650.

The

impact on FX, though, was hard to pinpoint. EUR, AUD, NZD, GBP all

rose.

CAD

responded more to an indication that Canadian Prime Minister Justin

Trudeau appears likely to step down. An announcement could come as

soon as Monday. USD/CAD dropped under 1.4400.

USD/JPY

was a mover, to highs just over 157.80. Today was the first session

of the year for Japanese markets after holidays on January 1, 2 and

3. Data from Japan today were Services (up from November) and

Composite (down from November) PMIs, a bit mixed. Bank of Japan

Governor Ueda spoke but did not give a clear indication of rate hike

timing to come. Dai-ichi Life company’s president, Toshiaki Sumino,

expects a BoJ rate hike this month (the BoJ meet January 23 and 24).

China

was interesting. On Friday USD/CNY crossed above 7.3, leading to much

speculation that the People’s Bank of China was trimming back its

support for yuan and that Monday’s reference rate fixing would be

above 7.2. Indeed, USD/CNY climbed above 7.3275 (CNY hit a 16 month low). The People’s Bank

of China, however, set the USD/CNY reference rate at 7.1876, well

under 7.2. Further, a PBOC-backed newspaper, Financial News,

reaffirmed the central bank’s “resolute” support for the

yuan. News also that the PBOC is set to issue a record volume of

offshore yuan bills in Hong Kong this month, aiming to stabilize the

yuan’s exchange rate amid the growing pressures. Issuing offshore

yuan bills is a strategy for absorbing excess liquidity in the

offshore market, reducing downward pressure on the currency.

Data

from China today was the Caixin Services PMI, reported at a 7 month

high of 52.2 (vs. expected 51.7 and November’s 51.5). Composite

dipped to 51.4, from November’s 52.3, weaker manufacturing output

slowed overall growth to its lowest level since September.

Trump yelled out his main policy planks once again today: