JHVEPhoto

I upgraded my thesis on Fortinet, Inc. (NASDAQ:FTNT) in late November 2023, because the market battered it following its disappointing third-quarter earnings launch. I argued that FTNT dropped to its long-term help ranges, which attracted the curiosity of dip-buyers, who seemingly noticed a major alternative given the capitulation.

That thesis panned out, as FTNT has outperformed the S&P 500 considerably, powering forward with a complete return of practically 30% since my earlier replace. Based mostly on its November lows, FTNT gained greater than 50% by way of final week’s highs, gorgeous the bearish traders with no religion within the wide-moat cybersecurity market leader.

It is essential to think about that Fortinet is a extremely worthwhile SaaS chief, assigned a best-in-class “A+” profitability grade. Whereas the slowdown over its core networking enterprise seemingly led to the numerous selloff, the market additionally rapidly priced within the weaker development momentum. Moreover, administration supplied insights in an early December convention suggesting that Fortinet “anticipates a return to a normal environment for the firewall market.” Because of this, whereas the high-growth section spurred by the pandemic has seemingly dissipated, Fortinet stays well-positioned to consolidate its prowess within the fragmented cybersecurity market.

Accordingly, the corporate has a unified end-to-end SASE stack based mostly on a “universal” strategy. Because of this, it permits clients to “deploy SASE on-premise or in the cloud based on their preferences.” Coupled with its core networking benefit, the corporate is assured it could actually proceed gaining market share. Regardless of that, Fortinet additionally cautioned that switching prices are embedded, however its market management. Administration underscored that it nonetheless wants clients to “be willing to replace existing products for Fortinet to succeed in this regard.”

Because of this, whereas the community impact and scale benefits seemingly profit Fortinet and assist safe its aggressive moat, it additionally gives sturdy protection to vital gamers like Palo Alto Networks (PANW) and cloud-native leaders like CrowdStrike (CRWD). Given their embedded switching prices, it is no surprise that cybersecurity leaders typically commerce at a marked premium relative to the market.

Fortinet is slated to report its fourth-quarter and FY23 earnings release on February 6. Buyers are seemingly trying previous 2024 as a reset yr after a number of years of speedy development. Because of this, traders are urged to look additional forward and assess whether or not FTNT can proceed to get well its earnings development momentum.

Accordingly, analysts’ estimates recommend a reacceleration in income and adjusted EPS development for FY25. Fortinet is projected to put up income development of 15.1% in 2024, following an anticipated slowdown to 12.1% for FY24. Its adjusted EPS development cadence can also be anticipated to reaccelerate to 16.2% after a marked deceleration to 7.2%. Because of this, I urge traders to look additional forward when assessing whether or not FTNT continues to be priced appropriately when contemplating their thesis.

FTNT is valued at an FY25 adjusted EPS a number of of 34.2x, properly beneath its 10Y common of 47x. Because of this, it appears seemingly the market has but to cost in its restoration absolutely, suggesting an additional re-rating potential stays doable.

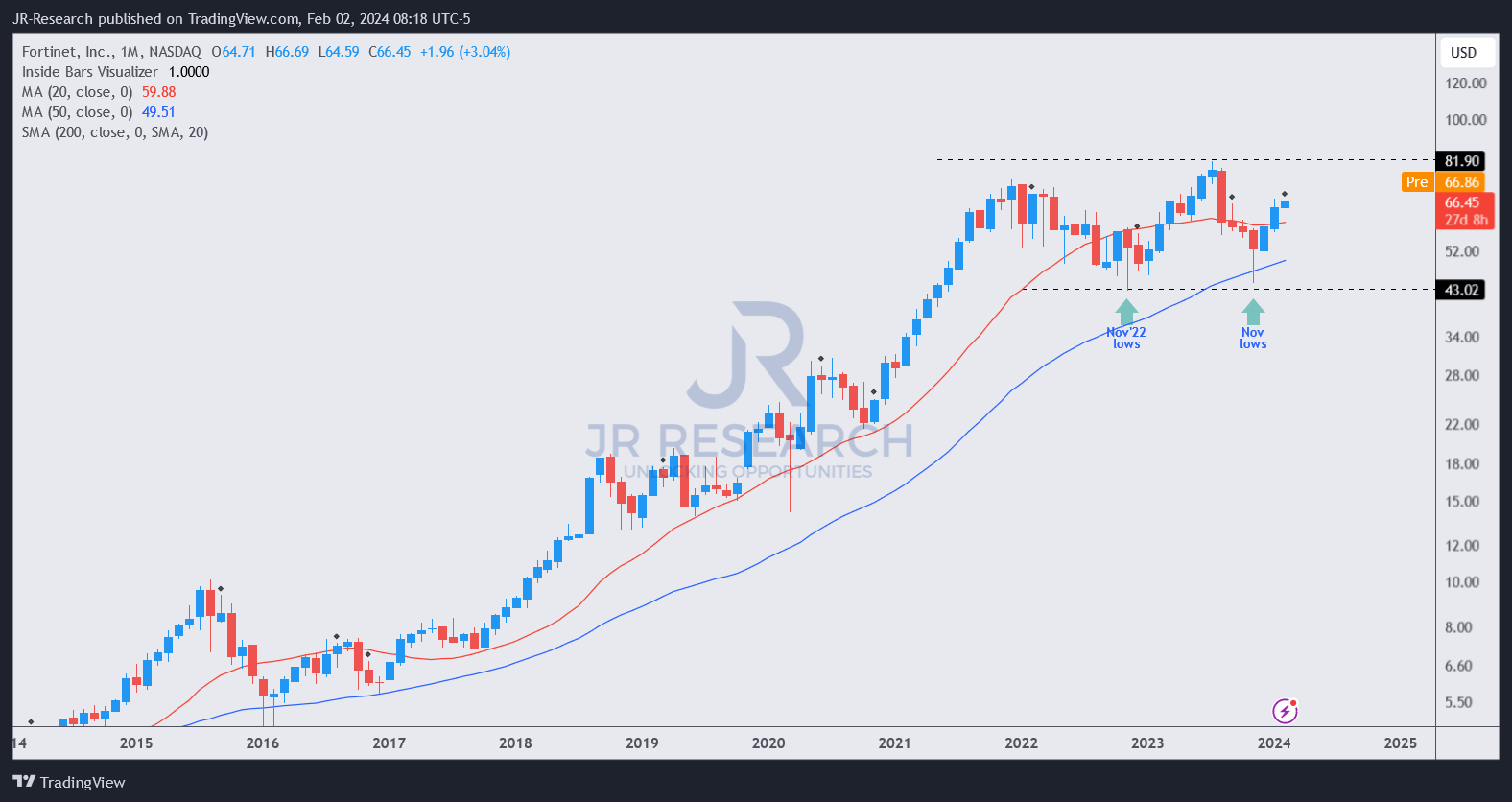

FTNT value chart (month-to-month, long-term) (TradingView)

Moreover, FTNT’s long-term uptrend bias remained undefeated regardless of the steep selloff in 2023. In truth, the low $40 ranges are well-supported, as dip-buyers returned aggressively to defend, seeing a extremely enticing danger/reward profile as FTNT weak holders capitulated.

I assessed that FTNT’s long-term value motion signifies an uptrend continuation bias is in play, though essentially the most enticing purchase ranges are seemingly over.

With that in thoughts, I gleaned it is apt for me to retain my bullish tilt on FTNT, though it is now not affordable to take care of my Robust Purchase ranking.

Score: Downgraded to Purchase.

Necessary word: Buyers are reminded to do their due diligence and never depend on the data supplied as monetary recommendation. Please at all times apply unbiased considering and word that the ranking isn’t meant to time a particular entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a vital hole in our view? Noticed one thing essential that we didn’t? Agree or disagree? Remark beneath with the intention of serving to everybody locally to be taught higher!