monsitj

Funding Thesis

Fortune Manufacturers Improvements, Inc.’s (NYSE:FBIN) inventory is up barely since my previous buy rating in September. The tip-market outlook has meaningfully improved since then and, with lower-than-expected inflation, analysts have began betting on a rate cut as quickly as the center of subsequent yr. The enhancing end-market demand given moderating inflation and potential restoration in single-family housing ought to profit the corporate’s income in 2024. Additional, the corporate’s gross sales also needs to profit from retail stock destocking coming to an finish, energy within the Linked product enterprise, new product improvements, and market share positive aspects.

On the margin entrance, the corporate ought to be capable to develop margins with the assistance of working leverage from gross sales progress, a good value setting, and cost-saving initiatives. The valuation can be affordable. Therefore, I proceed to have a purchase score on the inventory.

Income Evaluation and Outlook

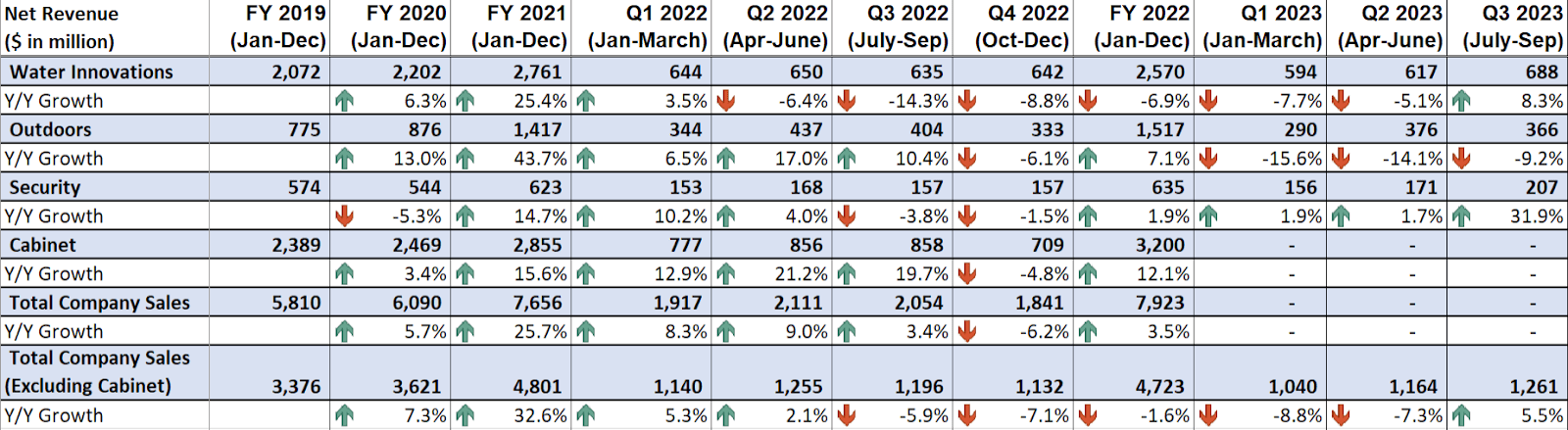

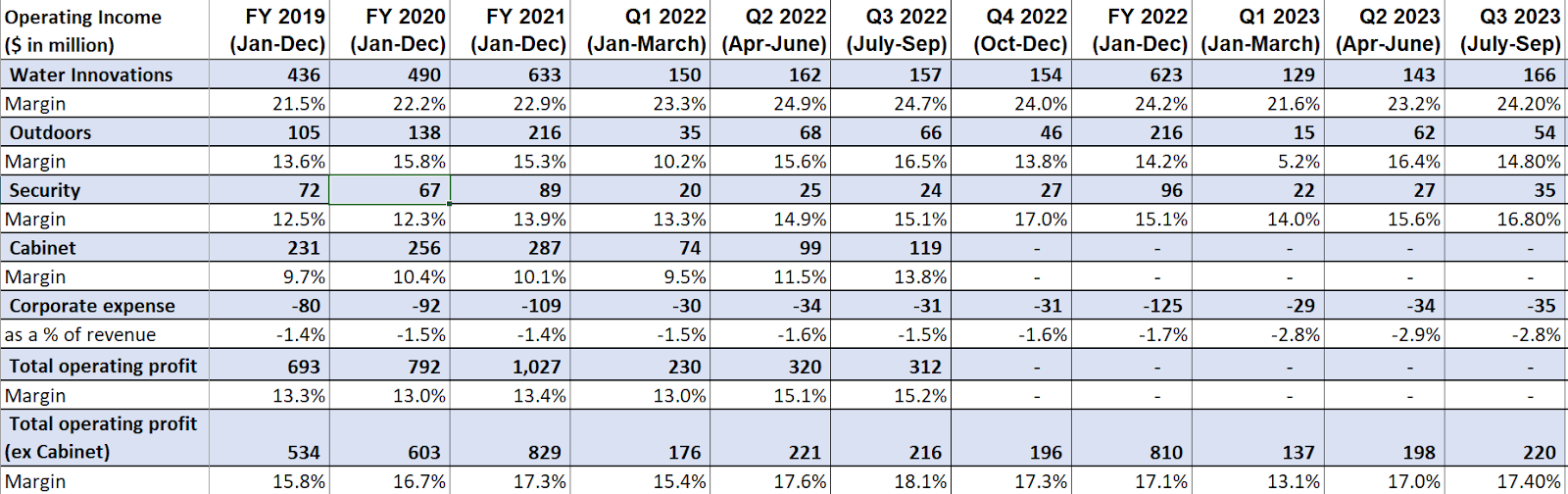

After going through challenges from stock destocking over the previous yr, Fortune Manufacturers’ income progress has began to see sequential enchancment in its gross sales progress within the final couple of quarters due to the normalization of stock destocking and simpler comps. Within the third quarter of 2023, along with the normalization of retail stock destocking, good contributions from the corporate’s latest acquisition of Emtek and Schaub Enterprise, Yale and August Enterprise, and Aqualisa Holdings additionally benefited the income progress within the quarter. Furthermore, worth will increase additionally helped the corporate in partially offsetting quantity decline on account of softness in end-markets given the inflationary setting. This resulted in a 5% YoY improve in gross sales to $1.26 billion. Excluding the good thing about $119.3 million or ~9% from acquisitions, natural income declined 4% YoY. The natural income declines replicate a mid-single-digit quantity decline which greater than offset the low single-digit profit from worth will increase.

FBIN Revenues (Firm Knowledge, GS Analytics Analysis)

Trying ahead, I’m optimistic in regards to the firm’s income progress prospects.

With inflation trending in the proper course and the talks of a possible reversal within the rate of interest cycle in mid-2024, I anticipate 2024 to be a a lot better yr for the corporate.

On the restore and transform (R&R) aspect, the corporate started experiencing stock destocking within the latter half of 2022, a pattern that endured till mid-2023. This resulted within the firm witnessing decrease income in comparison with the precise point-of-sales (POS) demand throughout this era. With stock destocking now full, the corporate’s gross sales ought to see enchancment. Even within the absence of a considerable enchancment in POS demand, simply the corporate’s gross sales aligning with POS demand ought to contribute to year-over-year (YoY) progress.

Additionally, I anticipate the broader macroeconomic setting to enhance shifting ahead with inflationary headwinds diminishing which ought to assist enhance client confidence and improve POS demand. Additional, after the divestiture of its Cupboards enterprise, FBIN’s present R&R portfolio consists of largely smaller ticket objects, and often, spending on smaller ticket objects sees a a lot faster restoration in comparison with the big ticket objects when the financial system improves. So, the corporate is well-positioned going into 2024.

The long-term underlying demand drivers within the R&R market are additionally strong with excessive residence fairness ranges on account of appreciation in housing costs post-COVID and the rising median age of properties within the U.S. which ought to assist the R&R market within the medium to long run.

The basics of the single-family housing market are additionally strong and this market has held up higher than anticipated regardless of mortgage charges at multiyear highs. This may be attributed to the significant underbuilding of recent properties after the nice housing recession of 2008 which has resulted in a decent demand-supply state of affairs available in the market. Because of pent-up demand on this market, I anticipate it to submit a fast restoration as soon as the rate of interest cycle begins reversing. The corporate additionally faces simpler comparisons on this market subsequent yr which ought to assist Y/Y progress.

Along with end-market enchancment, the corporate ought to profit from good execution and concentrate on product improvements which helps it acquire market share and outperform the end-markets. A very good instance of it’s the firm’s linked product choices the place it noticed gross sales tripping from FY20 to FY22 regardless of the disruptions within the chip provide which restricted the corporate to succeed in its full gross sales potential. Together with latest Yale and August acquisitions, the corporate’s linked merchandise gross sales have reached ~$250 million with 4.5 million activations for its linked merchandise. The corporate expects linked merchandise to be a major progress driver within the coming years and is specializing in scaling and introducing new merchandise in classes like Sensible residential locks, Grasp Lock linked entry for enterprise, and Moen’s Sensible Water Community. On its last earnings call, speaking in regards to the potential alternative within the sensible water enterprise, the corporate’s CEO Nicholas Fink stated:

I imply if you take a look at the Sensible Water alternative from numerous totally different lenses, it’s fairly staggering, proper? Simply to begin with simply the pure — how a lot preventable water injury is there right this moment. We expect that is $15 billion of claims a yr. It is larger than Hearth and Housebreaking mixed, proper, so $15 billion of preventable water injury. I really imagine we will develop that addressable market as a result of we will give you extra merchandise that may handle extra kinds of preventable water injury. We will take that just about to zero. I imply we did a research with LexisNexis in 10,000 properties. We decreased 96% of the claims to zero, and the opposite 4% of claims, I imagine, we decreased by over 70%. So just about going to zero.

There’s an ESG lens to it, proper? Along with saving, we predict doubtlessly trillions of gallons of water, there’s an enormous vitality element to processing and cleansing water. And so you are taking Mission Moen, which is basically primarily based on what we have now available in the market right this moment, our dedication to save lots of 1 trillion gallons by 2030, that in line with the maths obtainable on the EPA web site, so equal to us taking a million automobiles off the highway for a yr, proper? And so you can begin to see (inaudible) municipalities, proper? It has an enormous greenback worth impression. And so the chance is big”

I believe a recovery in the end market coupled with the company’s above-market growth opportunity through innovating and scaling connected products should help it deliver good growth in the coming years.

Margin Analysis and Outlook

In the third quarter of 2023, the company’s margins continued to face headwinds from sales deleveraging due to volume decline. The company was able to partially offset it through price increases, cost-saving initiatives, and deflation in input costs. This resulted in a 70 bps YoY decline in adjusted operating margin to 17.4%.

On a segment basis, the Water innovations segment adjusted operating margin declined 50 bps YoY due to volume deleveraging partially offset by cost-saving measures. The outdoor segment’s operating margin declined by 170 bps YoY due to lower volumes resulting in sales deleveraging. However, the Security segment was able to increase its operating margin by 170 bps YoY due to price increases, high-margin product mix, and operating leverage from higher sales.

FBIN Operating Margins (Company Data, GS Analytics Research)

Looking forward, the company’s margins should benefit from operating leverage from sales recovery as end markets improve. On its earnings call in October, management talked about seeing a path to margin improvement even if the end market is down to low single digits in 2024. The end-market situation has improved since then as inflation data reported in November was better than expected and this led to an increased probability of rate cuts next year. With my expectations of end-market growth next year, I believe the company can post good margin improvement next year. The medium to long-term outlook is also good with management targeting 300-500 bps operating margin improvement through initiatives like productivity improvement, near-shoring, site consolidation, etc. So, I am optimistic about the company’s near to medium-term margin growth prospects.

Valuation and Conclusion

Fortune Brands is currently trading at ~17.54x FY24 consensus EPS estimate of $4.19 and 15.06x FY25 consensus EPS estimate of $4.87. Over the last five years, the stock has traded at an average forward P/E of 15.89x. However, one needs to note that the company spun off its low-margin and more cyclical Cabinet segment late last year, and the remaining company has higher-margin and more stable businesses. Hence, I believe FBIN’s valuation multiples deserve a re-rating compared to its 5-year average. I believe the stock can continue to trade at a forward P/E in the high teen range. If we apply a 18x P/E multiple to the FY25 consensus EPS estimate of $4.87, we get a one-year forward target price of ~$87 which implies ~19% upside over the next year.

I imagine the corporate has good progress potential over the approaching years. The income outlook appears favorable due to the completion of stock destocking and a extra aligned gross sales progress with POS demand, enhancing finish markets, energy within the linked merchandise enterprise, and product improvements and market share positive aspects. As well as, margins also needs to broaden with the assistance of working leverage from gross sales restoration. Therefore, given the nice progress prospects and affordable valuation, I charge the inventory a purchase.