Kawisara Kaewprasert

Franklin Road Properties (NYSE:FSP) is a REIT targeted on workplace properties within the U.S. that’s presently buying and selling a lot decrease than its e book worth. Within the final couple of months, the corporate’s inventory worth skilled a sluggish decline, making it extra enticing for traders.

The final time now we have covered the corporate, we analysed the Q3 report and reiterated our purchase ranking primarily based on these outcomes. Since our final article, the corporate’s inventory worth has declined by round 13%. The decline in inventory worth, mixed with the corporate frequently following their plans diligently, creates a compelling funding alternative.

Since Our Final Report

Since our final report, the corporate has shared their Q4 2023 financials, which present a continued concentrate on inclinations and debt repayments.

Concurrently, the corporate has additionally introduced a sweeping debt modification, affecting all the firm’s debt. With the debt modification, the corporate has repaid a considerable quantity of the overall debt and likewise modified maturities throughout the board.

Debt Modification Desk (This fall 2023 SEC Submitting)

In gentle of the debt modification, the corporate repaid a complete of $102m in debt utilizing money available. All of the debt sequence’ maturity dates have additionally been moved to April 1, 2026, making the corporate have zero maturities for the subsequent 2 years.

With a wholesome steadiness sheet, debt hasn’t been an issue even earlier than this modification. Nonetheless, the amendments put the corporate in a good higher spot, giving them 2 worry-free years with out maturities to execute on their present technique and solely $303m of debt maturities on April 1, 2026.

With constructive money stream and at the least $40m in money available, the principle concern now could be, whether or not the corporate can proceed to eliminate their actual property at beneficial costs and, if the corporate shall be ready to finally be capable to return capital to their shareholders.

On the disposal entrance, the corporate makes regular progress. Since our final article, the corporate has made public 2 extra disposals, bringing them nearer to the CEO’s communicated purpose

to extend shareholder worth by persevering with to (…) pursue the sale of choose properties the place we imagine that quick to intermediate time period valuation potential has been reached.

Property Gross sales

On December 6, 2023, the corporate has accomplished the sale of “Blue Lagoon” in Miami, Florida for ~$68m in gross proceeds. Money proceeds from this disposal have evidently been used as a part of the continuing debt discount, executing on the corporate’s long run said technique of utilizing disposal proceeds for debt discount.

On January 26, 2024, the corporate has accomplished the sale of “Collins Crossing”, an workplace property in Richardson, Texas for ~$35m in gross proceeds. Because the earlier than talked about debt discount was accomplished in February and will have been lined with money available on FY2023, the money proceeds from this disposal can be found to pay for operations and/or additional debt reductions.

Up to date Valuation

Following our valuation in our final article, we are able to replace our assumptions primarily based on the newest gross sales and additional info shared by the corporate within the FY23 launch. First, we are able to replace our earlier estimation of worth per sq. ft of all of FSP’s actual property holdings.

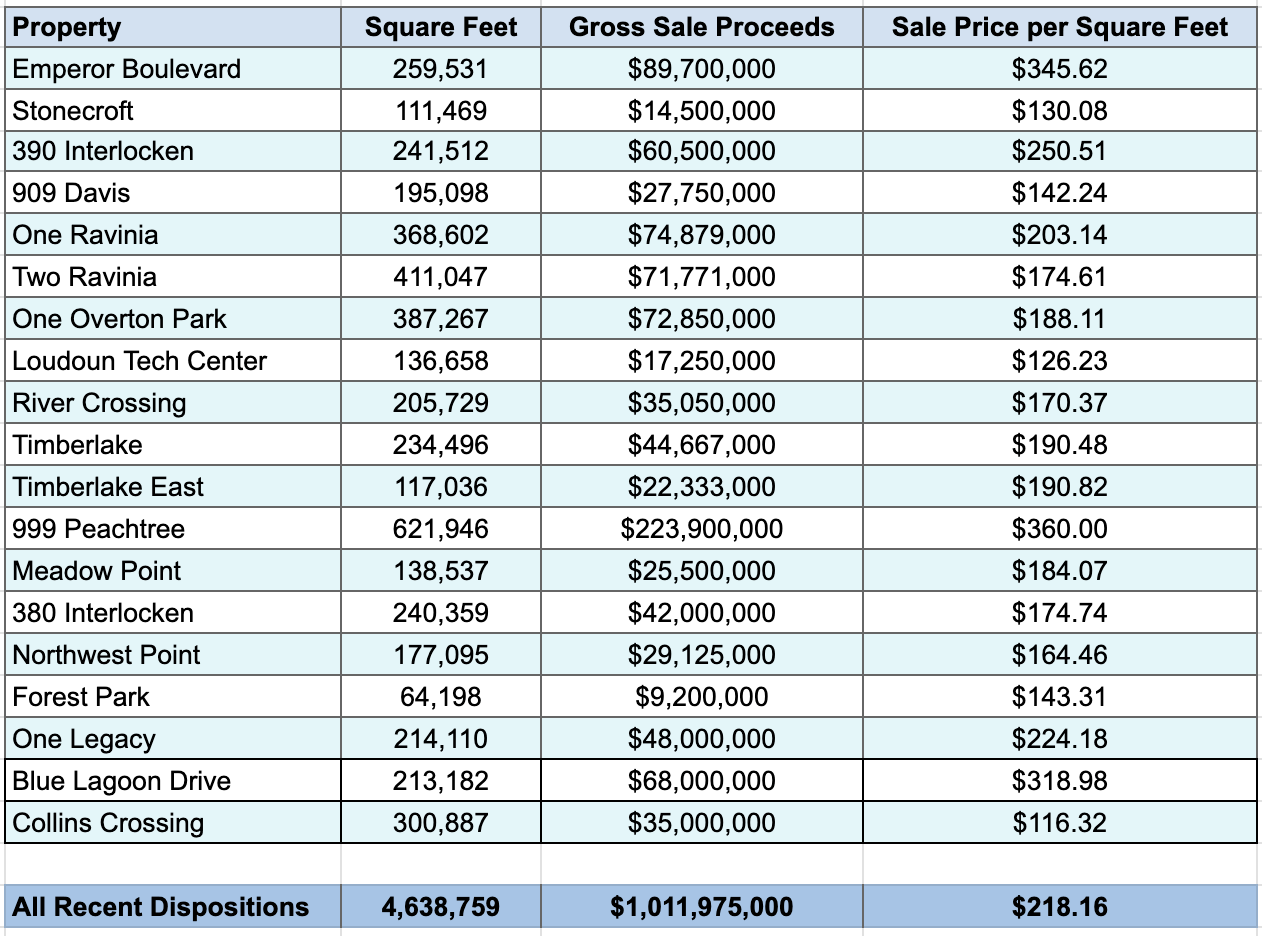

Worth per sq. ft of current inclinations (Asset Alchemist)

By updating our spreadsheet calculating the common worth of earlier property gross sales, we are able to embrace the most recent closed gross sales in our calculation. Up till now, FSP has offered 19 properties throughout the U.S. since December 2020, at a mean sale worth per sq. ft of $218.16. The 2 newest inclinations have been priced near our earlier common of $220.37.

After the current inclinations, the corporate’s actual property holdings now whole a sq. footage of 5,478,281. Making use of the common worth per sq. ft calculated, we are able to provide you with an up to date, however nonetheless very tough worth of ~$1.21b for FSP’s remaining actual property holdings.

Including our pessimistic estimate of at the least $40m money available and drastically lowered debt, the tough web worth of the corporate’s property is just below $1b. As a result of ongoing disposals and accomplished debt discount, though our up to date estimate is barely decrease than from our final report, the corporate seems to be a lot more healthy with a extra beneficial maturity construction.

Dangers

We need to reiterate the dangers talked about in our final Article on FSP. Specifically, the 2 principal dangers are:

- A powerful decline in industrial actual property costs going ahead, considerably impacting the corporate’s web asset worth.

- The lack of administration to “close the gap” between the corporate’s web asset worth and the worth of the widespread inventory.

The comparatively low worth the corporate acquired for his or her Collins Crossing property additional confirms that threat number one is to not be underestimated. We’re intently following additional developments within the industrial actual property business and what costs FSP will be capable to promote their different properties at.

The absence of any cost-cutting measures may also verify that threat quantity 2 is to not be underestimated. In principle, the corporate ought to be capable to cut back their workforce now, since they’ve offered loads of properties within the final couple of years and thus ought to want much less manpower to handle them. Nonetheless, to date, the corporate has not performed thorough cost-cutting measures.

With the continued execution of the corporate’s said objectives for disposing actual property and decreasing debt, the query of the long-term future for the corporate turns into extra vital. In some unspecified time in the future, shareholders must ask themselves if they may ever obtain capital returns from their funding into an organization managing a dwindling actual property portfolio.

Conclusion & What To Look Out For

Primarily based on the continuing efforts of the corporate to promote properties and unlock shareholder worth, we imagine the factors introduced up in our final evaluation are nonetheless legitimate. We welcome the constructive updates concerning profitable property gross sales.

Primarily based on our estimations, the inventory remains to be buying and selling at undervalued ranges. Factoring in a ~13% decline in inventory worth since our final article, we imagine this to be a sexy funding alternative and a good higher entry level in comparison with 6 months in the past.

We’re nonetheless searching, primarily for updates on the deliberate property gross sales and potential updates on the corporate efficiently renting out extra of their owned house. We’re persevering with to look out for any feedback on attainable share repurchases or clarification for long-term plans of the corporate.