Maliflower73/iStock through Getty Photos

Worth Investing Is At Its Core The Marriage Of A Contrarian Streak And A Calculator.

– Seth Klarman

I had recalled a quote in regards to the market that I could not fairly place that mentioned one thing to the impact of “Everyone has a calculator” suggesting with the ability to do fundamental math is not a lot of a bonus in markets. After I looked for the origin I discovered the above quote by Seth Klarman as a substitute. Because it seems, I like that one rather a lot higher as a result of I’ve made an investing profession out of making use of fundamental frequent sense and a calculator to my selections, and likewise as a result of Seth Klarman is an investing legend. And for anybody who does not know, I strategy markets as a set of chances. I weigh the proof I’ve and the likelihood of varied occasions occurring and attempt to estimate what the affect will be on the share value. I am hardly ever trying greater than a 12 months out, and for that, a calculator may be fairly helpful, particularly when enjoying in corners of the market with much less competitors.

The bigger the corporate, after all, the much less probably you might be to make out nicely with only a calculator. Everybody else does have them too, and if not one of the 25 analysts following a inventory can see what you possibly can see in your calculator, there’s a respectable likelihood you are the one which’s incorrect. Luckily, the corporate I need to focus on right now is a tiny firm with barely a 100 million greenback market cap. My calculator and a few fundamental evaluation inform me there’s a terrific alternative right here. It is no assure, after all, neither is every other investing thought, nevertheless it’s probably the greatest danger/reward performs I see proper now. I am guessing no person else has pulled out the calculator but, however could be dusting it off by the point earnings are reported, presumably in March.

The corporate in query is Frequency Electronics (NASDAQ:FEIM).

Frequency Electronics is basically a protection contractor, promoting overwhelmingly to prime contractors like Lockheed Martin, but additionally to the US authorities. Actually, US authorities gross sales both straight or not directly account for roughly 95% of the corporate’s enterprise.

Their merchandise embody precision timing gear, particularly varied types of atomic clocks, in addition to frequency era units. The corporate’s gear has been used on the house shuttle in addition to the voyager missions and has functions in satellites, safe communications, digital weapons methods, UAVs, and many others. Their enterprise is split largely into house/satellite tv for pc and non-space authorities enterprise, with every tending to run within the ballpark of fifty% of gross sales, with some fluctuations round that vary.

Getting out my calculator, I will counsel why I believe the inventory is prone to re-rate from its present stage over the subsequent 12 months.

Let’s begin with income. I am going to go into extra element on a few of this under, however I’m assuming their base income close to time period primarily based on their current backlog ought to proceed to be within the latest vary of the final 9 months between $12 and $13.6 million. Backlog has been a reasonably dependable indicator of income, as I am going to element a bit under.

There may be cause to consider revenues will truly be considerably increased. That is as a result of the corporate introduced a collection of contracts in November of $25 million, $19 million, and $9 million, equal to roughly their final 12 months’ income in a single month. The primary two contracts, amounting to $44 million, have an aggressive supply schedule and are slated to be delivered within the subsequent 2 years. These contracts aren’t included within the backlog above. If these are delivered as supposed, it might add $5.5 million in income per quarter over the contract’s lifetime. If one assumes a gentle state of enterprise of $12 million quarterly primarily based on current backlog, and provides the $5.5 million quarterly from latest contracts, quarterly income would common $17.5 million.

As well as, there was an necessary nugget embedded within the most recent conference name that means not solely will income be ramping up considerably, however will probably be doing so at a lot increased margins than the present 30%.

I believe that we really feel fairly strongly that our gross margin goes to proceed an upward pattern. In fact, that is not going to go on indefinitely. However we’re focusing on gross margin of round 50% and we predict that we are able to get there inside the subsequent six months to a 12 months.

-Thomas McClelland (CEO) 12/12/2023 Conference call

A 20% improve in margins on prime of an almost 50% improve in income can be game-changing. Particularly in mild of what the corporate expects can be reasonably nominal will increase in overhead. Once more from that very same name.

So SG&A on a greenback worth quantity goes to run pretty constant. I imply, once more, if we develop considerably, sure, there will be some extra prices in there. However percent-wise, as you see, it went down for getting the proportion to {dollars} whilst a method of earnings is down. So we count on it to remain at that present stage the place it’s now except issues considerably develop.

-Steve Bernstein (CFO) 12/12/2023 Convention name

We have now an organization anticipating important will increase in income, important will increase in margins, and comparatively flat overhead. It does not take a rocket scientist to see what assembly these targets would imply for earnings. Since I’m most assuredly not a rocket scientist let me take a stab at what I believe quarterly numbers would possibly appear to be someday within the subsequent 12 months.

Income: $17.5 million

COGS: $8.8 million

SG&A/R&D: $4 million (assumes 15% development from present ranges)

That leaves me with pre-tax earnings of about $4.4 million {dollars}, or EPS of $0.47 per share. Notice the corporate has substantial NOLs that ought to defend it from most taxes close to time period and there aren’t any actual curiosity bills. So what’s an organization exhibiting enormous development in revenues, margins, and sporting almost $2 a share in annualized EPS value? I am unsure, however I believe it is fairly a bit greater than the present share value, hovering a bit beneath $11 per share.

All of that’s, after all, primarily based on a complete bunch of future assumptions derived from the statements of the present administration workforce, and a few latest knowledge. That leaves the query of how probably is it that some or most of this involves cross. I believe there’s good circumstantial proof it’ll. Let me undergo these merchandise by merchandise. I will break this into 3 components suggesting why the prevailing income run charge needs to be sustainable, why the brand new contracts will probably be additive as anticipated, and why these margin targets are believable.

Base income

My base income assumptions for the subsequent 12 months, excluding the just lately signed batch of contracts in November, is roughly 12 million {dollars} 1 / 4, which is under the low level of 12.4 million {dollars} during the last 9 months. The first argument right here is that backlog has been pretty predictive of 12-month revenues. This is sensible as this can be a funded backlog the place cash has already been dedicated.

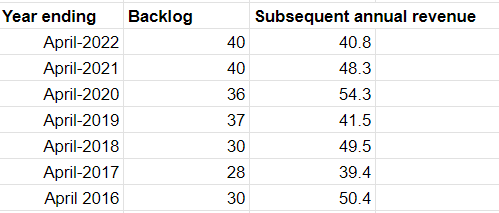

Going again to 2016, you possibly can observe the year-ending backlog versus the income for the next 12 months and see that revenues have constantly exceeded the tip of 12 months backlog. With backlog sitting at $49.7 at quarter finish, a base charge of $12 million {dollars} quarterly would put them under each earlier order conversion stage going again to 2016.

Firm filings

Whereas no assure, orders do get canceled, issues occur, I believe anticipating conversion charges barely decrease than historic ranges is affordable.

I might additionally level to what appears to be not less than secure to rising demand within the house enterprise. The U.S. House Power requested a 13% finances improve for fiscal 2024 which is broadly supportive of federal funding in areas that may profit the corporate.

On their fourth quarter conference call, Northrop Grumman, one of many firm’s massive clients, indicated they see mid-single digit development trying ahead of their house phase.

House gross sales are actually anticipated within the mid-to-high $14 billion vary, with margins of roughly 9%. The mid-single digit development charge in house displays declines in a restricted program attributable to shifts in authorities precedence, that are greater than offset by development in different components of the house portfolio.

Total, I believe assuming the bottom relationship between order backlog, and revenues is sustainable, and affordable close to time period particularly in mild of constant messaging from main clients and priorities of the US authorities.

New contracts

The acknowledged assumption right here is that the corporate will obtain its acknowledged income targets on the batch of huge contracts introduced in December, and that this might be additive to the bottom income ranges described above. I am going to level to a few objects right here that counsel that is moderately probably.

First, the corporate has indicated the work was lengthy in coming, in order that they had been well-prepared to begin. Having been anticipated a while in the past, the groundwork was laid, staff had been employed and many others. In addition they indicated as of the December earnings convention name that this work had already begun after a couple of million {dollars} of the funding was launched.

In addition they describe this work as being on an aggressive timeline.

that is type of a take a look at to see if we and naturally, our buyer can ship on this shortened time period. Sometimes, a program like this could take roughly three years to do the identical factor.

Finally, work has begun instantly on contracts with an deliberately unusually quick timeframe. This does not assure that issues will proceed on the tempo, nevertheless it does counsel the work is progressing as anticipated as of now and may transfer shortly. Not less than by way of this contract, it appears to be your complete level of the work.

Gross margins

In the newest convention name, administration acknowledged and reiterated they count on to reach at 50% margins within the subsequent 12 months. That is notably increased than their historic targets of 35% to 40%. So what has modified right here? In the event you consider present administration, there was a philosophical shift in how they bid work.

Once more from the December name.

I believe that if we glance traditionally, we have had quite a lot of issue with what we check with as NRE applications, non-recurring engineering or quite a lot of new growth exercise. Traditionally, when these flip into in a while into manufacturing, we have been in a position to do these very profitably, however we’ve got been challenged with the event. And I believe one factor that I’ve made an actual effort to do otherwise, is we’re bidding these items otherwise. And I believe to some extent, my expertise right here over a few years, I’ve been concerned in an terrible lot of those growth applications. And I do know the pitfalls and the difficulties. And I believe we’re pushing again actually arduous, and we’re ensuring that we bid these in a approach that we really feel assured that we may be worthwhile. And so I believe that is one of many parts. I believe then the remaining is simply type of the devils within the particulars. I believe if we have a look at the precise applications which have simply come on-line in November, I believe these have a smaller non-recurring engineering element to them. They’re much extra manufacturing and people traditionally, we’ve got been very efficient on.

The declare right here is twofold. First, they don’t seem to be bidding on contracts with out enough margin. Second, is that it’s growth and engineering contracts which have been problematic, whereas the latest batch of labor is extra manufacturing work. The implication there’s each extra self-discipline in how contracts are bid, and an order e book that tends to mirror increased margin manufacturing work over decrease margin engineering work.

At this stage, we’re counting on feedback from administration greater than anything that these margin targets are achievable, which results in administration credibility as a key think about evaluating the chance that they will obtain these reasonably formidable targets.

This looks like time to delve into firm historical past and take my finest stab on the credibility of present administration.

The present CEO is Thomas McClelland, who has been the corporate’s chief scientist for many years. He holds a PhD in physics from Columbia. He was named interim CEO in July 2022, changing Stanton Sloane who took over in Could 2018. The earlier CEO’s tenure can solely be pretty described as an utter catastrophe, racking up over 20 million {dollars} in working losses between 2019 and 2022. Working margins collapsed to -17% in his ultimate full 12 months on the helm.

There are two issues I might observe about this transformation. First, the brand new CEO has been far more credible in his commentary, and second, he appears to have turned the ship round.

Since taking on in July 2022, revenues have elevated from $8.2 million {dollars} within the quarter ending July 2022 to $13.6 million {dollars} or 65% within the quarter ending October 2023. In that very same time, working earnings has gone from a $3.1 million greenback quarterly loss to a $0.8 million quarterly revenue. Gross margins have expanded from -0.06% to a constructive 31.9%, monitoring in direction of that fifty% goal. Backlog has elevated from $40 million to $50 million or 20% excluding the just lately introduced contracts. So far, the operations communicate to the competence and credibility of present administration.

Attending to precise commentary, I went again by the convention name transcripts going again to July 2022 to guage the credibility of earlier statements on the corporate outlook. As a comparatively new CEO, there is not a ton to guage, however credibility thus far appears to be like good.

This is the rundown.

At the moment, we anticipate the upcoming award of a number of important contracts.

On this case, I believe he was referring to the batch of labor reported this November. I might describe this as correct however slower than anticipated.

There have been two separate statements about profitability in fiscal 2023, first in Q1.

we’re working arduous to get worthwhile as shortly as doable. Our purpose is to interrupt even not less than, if not be worthwhile by the tip of the fiscal 12 months.

And once more in Q2

Effectively, I would not say as probably that this fiscal 12 months might be break-even. However I believe the final quarter and going ahead after that we do anticipate being break-even or maybe a bit bit higher.

By the fourth quarter of 2023 the corporate hit precisely what was described within the first quarter of 2023, and reiterated in Q2, producing $13 million {dollars} in income and $0.2 million {dollars} in web earnings. This was proper on the cash.

My web take right here is that given the latest adjustments in operations, and their predicted course, I am skating to the place the puck is prone to be. The corporate has indicated what needs to be a speedy ramp in income and earnings from a CEO who has carried out fantastically over lower than 2 years whereas being pretty correct in his forward-looking assessments. On the similar time, they function in a distinct segment associated to house and protection that’s each attractive from an investor standpoint, and is a crucial focus of federal spending. It is believable they may re-rate on each earnings and a number of. The chance reward right here is compelling.

The draw back is protected by a strong steadiness sheet with no debt and virtually a greenback a share in money. There have been no latest insider sells and a flurry of small buys in 2022 and 2023 though at decrease costs.

I believe the last word inform right here on whether or not my thesis goes to be right is close to time period gross margins. Administration has clearly acknowledged they’ve modified their bidding philosophy to make sure revenue margins. At this level, many of the backlog acquired beneath earlier senior administration needs to be working off the books. If they’re right right here, we must always begin seeing gross margins and income begin to elevate in direction of that focus on within the upcoming quarter. Even when they do not attain my hypothetical numbers, strikes in that path ought to lead to upside for the value of the underlying fairness.

There are dangers, after all.

-

Federal spending schedules are infamous for adjustments and delays. That might, after all, occur right here and derail the ahead outlook.

-

They’ve important buyer focus, with virtually all of their work deriving from federal spending and 4 clients accounting for greater than 10% of income.

-

Engineering and venture issues are all the time a danger, and can lead to low and even unfavorable margins. The characterization of their present batch of contracts being extra manufacturing and fewer growth oriented does mitigate that danger.

- Upcoming finances negotiations and the potential of a authorities shutdown might weigh on supply schedules.

I’m making an attempt to rearrange a dialogue with administration to get a stronger really feel for the enterprise. I could do a follow-up put up as soon as that dialogue is organized. Within the meantime, the chance/reward appears to be like glorious right here. We must always get a greater really feel for whether or not I’m proper or whether or not this may blow up in my face when earnings are launched once more someday in March.