champpixs/iStock by way of Getty Photos

Funding Thesis

Freshworks (NASDAQ:FRSH) is a comparatively new entrant within the Buyer Relationship Administration (CRM) business. The corporate was listed within the markets in 2021, however like a lot of the youthful corporations available on the market, it obtained a impolite awakening in 2022 because the markets re-rated the fairness threat premiums and money flows wanted to be prioritized. Final yr, the corporate unveiled its multi-year working plan in its Investor Day presentation, showcasing its product roadmap and its margin enlargement technique to attain sturdy progress.

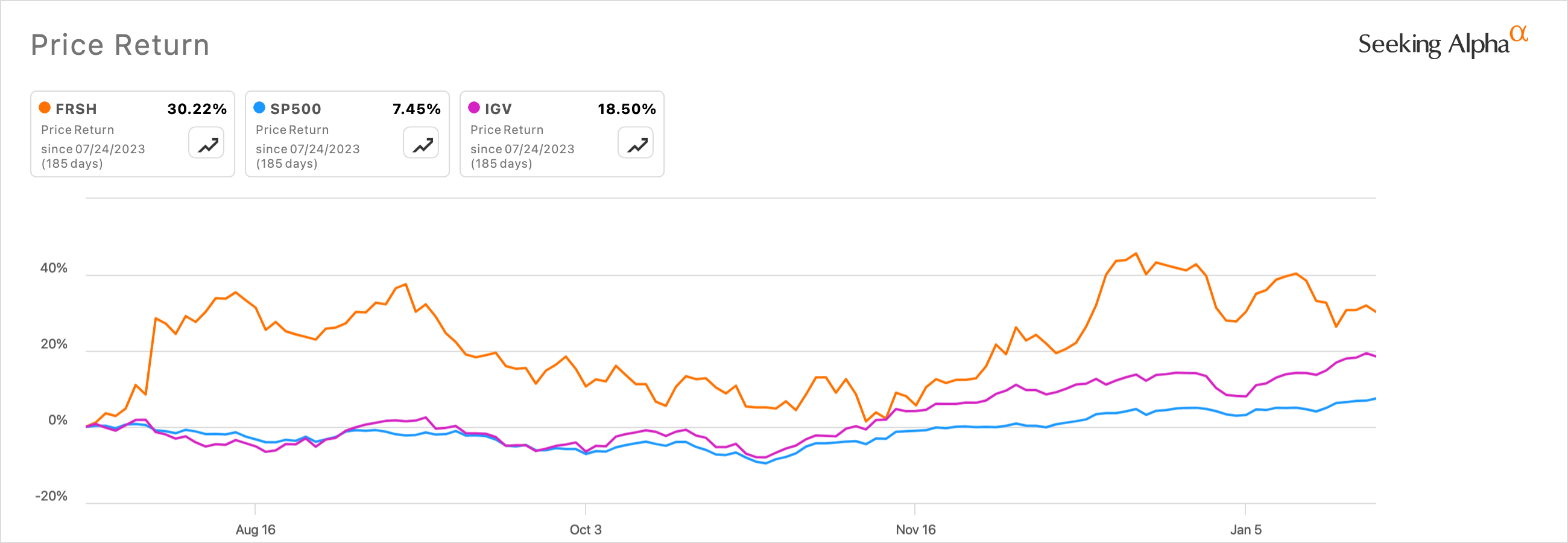

Because the presentation, Freshworks inventory has picked up tempo to beat the S&P 500 Index (SP500) and the iShares Expanded Tech-Software program Sector ETF (IGV) that I exploit as a benchmark for cloud-based know-how shares.

In search of Alpha

I consider traders are discounting the worth of Freshworks’ market cap as of at present relative to the present margin enlargement historical past and future targets of the corporate.

About Freshworks

Freshworks is a decade-old SaaS firm that originally started promoting cloud software program for the Buyer Relationship Administration (CRM) area however expanded this providing into the broader Buyer Expertise (CX) area to incorporate advertising and marketing, gross sales, and automation instruments. Over time, the San Mateo, CA-headquartered firm leveraged their backend CX platform to additional department out into the higher-margin Info Know-how Service Administration (ITSM) and Operations Administration (ITOM) cloud software program markets.

All three cloud software program markets are closely aggressive, with some massive, profitable incumbent corporations already present in every market, which I’ll cowl within the Dangers part later. But, Freshworks believes its merchandise differentiate from its rivals by appealing to Small & Medium-sized Businesses (SMBs) by delivery merchandise and options that concentrate on lowering prices and rising time-to-value for SMBs.

Investor Presentation

Being a SaaS enterprise, metrics resembling Annual Recurring Income (ARR) and Web Greenback Retention (NDR) can be essential in evaluating the expansion prospects of the enterprise. After reviewing their most up-to-date FY23-Q3 quarterly filing, I discovered that the corporate screens ARR from prospects contributing greater than $5,000 in ARR as a share of complete ARR, so I’ll particularly assessment this metric shifting ahead.

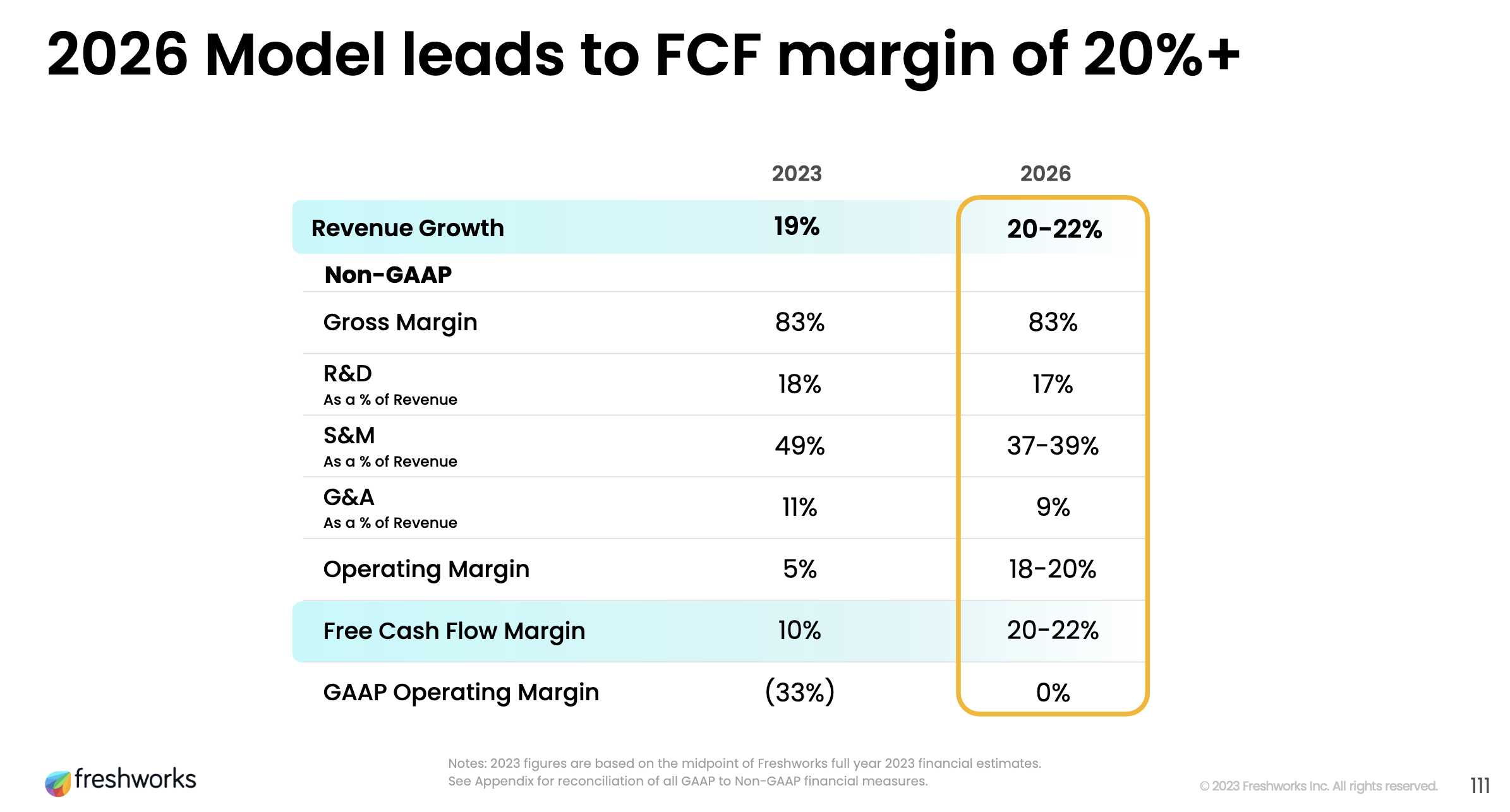

A re-prioritization of progress goals with a lift of margins

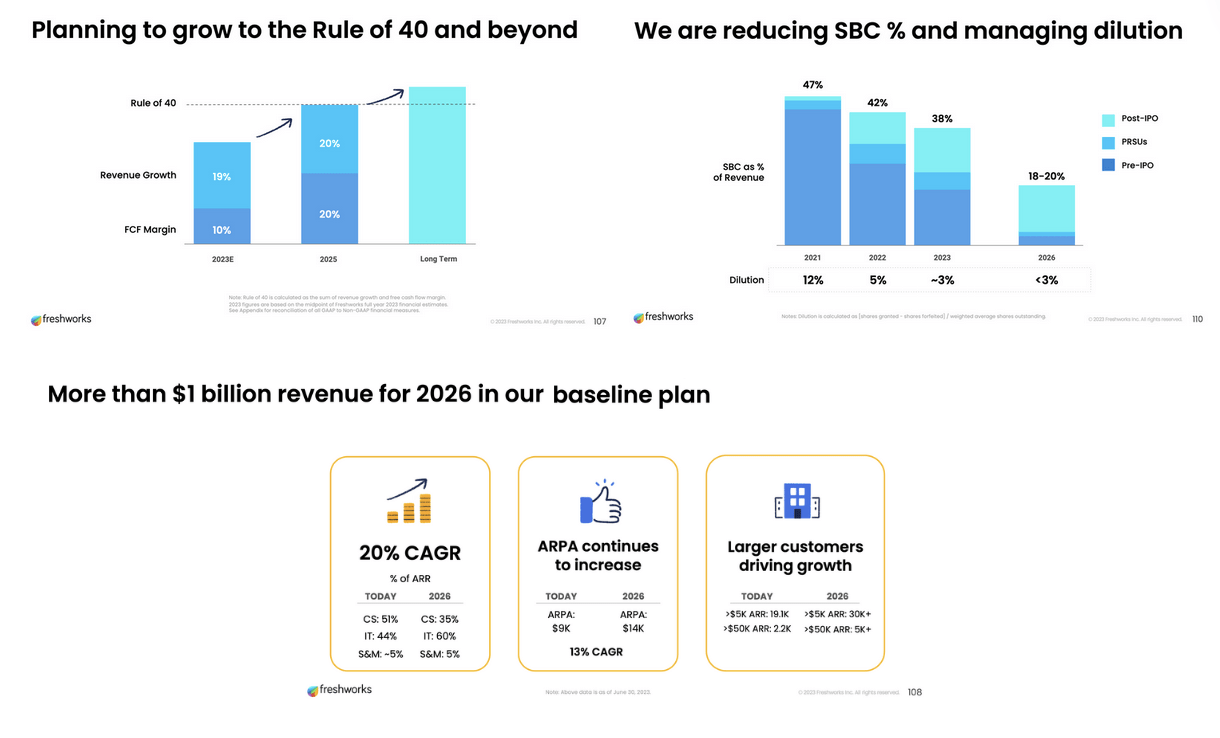

Of their Investor Day presentation in July final yr, Freshworks laid out its three-year working plan for prioritizing margins along with its progress targets, as proven within the screenshot under.

Investor Day Presentation, August 2023

I’ll come again to this screenshot later since I’ll use administration’s targets in my valuation mannequin, however for now, I’ll be aware that a few of the line gadgets, resembling Working Margin and FCF margins, have fairly an aggressive ramp up in a span of three years. When reviewing a few of the earlier administration commentary, I see that administration has prioritized just a few initiatives of their working technique, resembling renegotiating infrastructure spend with AWS, their major infrastructure supplier, and adopting cost-effective Go-To-Market methods resulting in decrease Gross sales & Advertising and marketing spend. Within the FY23-Q2 earnings call, administration famous:

All this (these initiatives) led to a big outperformance for non-GAAP working revenue of $11.7 million and non-GAAP working margin of 8% in Q2. Given the numerous adjustments we have revamped the previous yr, I am happy with the tangible enhancements we’re making in our effectivity.

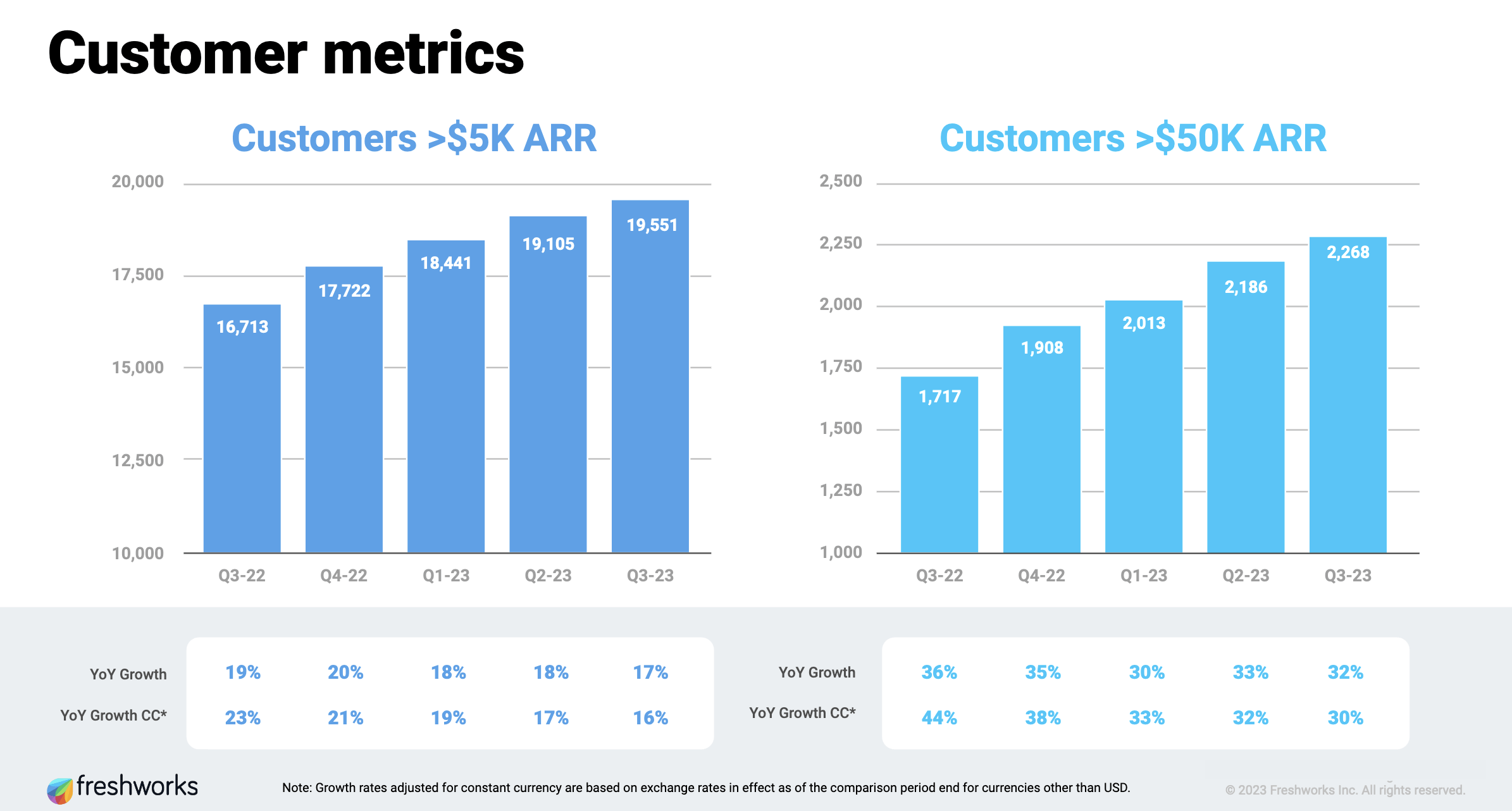

Nevertheless, one thing that caught my consideration was the corporate’s pivot to amass bigger prospects whereas additionally specializing in their present SMB prospects. Check out the chart under, which compares progress in Prospects >$5K ARR (SMBs) vs. Prospects >$50K ARR (Giant Enterprises):

FY23 Q3 investor presentation

Within the chart above, which will be discovered of their FY23-Q3 investor presentation (Slide 11), I see that y/y progress from their enterprise prospects is rising a lot sooner than that from their SMB prospects, rising at +30% progress charges, now for the fifth quarter in a row. I do suppose that is an accretive pivot for Freshworks in order that it might cease leaning utterly on SMBs. Furthermore, enterprise prospects often have bigger budgets, and the acquisition of enormous prospects like enterprises will assist Freshworks climate any seasonalities which are related to smaller prospects.

As well as, I consider enterprise prospects may also assist in boosting adoption of Freshworks’ AI merchandise, resembling customer support chatbots, copilots, and insights AI instruments constructed on Freshworks’ Freddy AI platform. Administration plans to launch these AI instruments as add-ons to the prevailing subscription plans and supply them to all prospects beginning this quarter, per administration’s commentary within the FY23-Q3 earnings call.

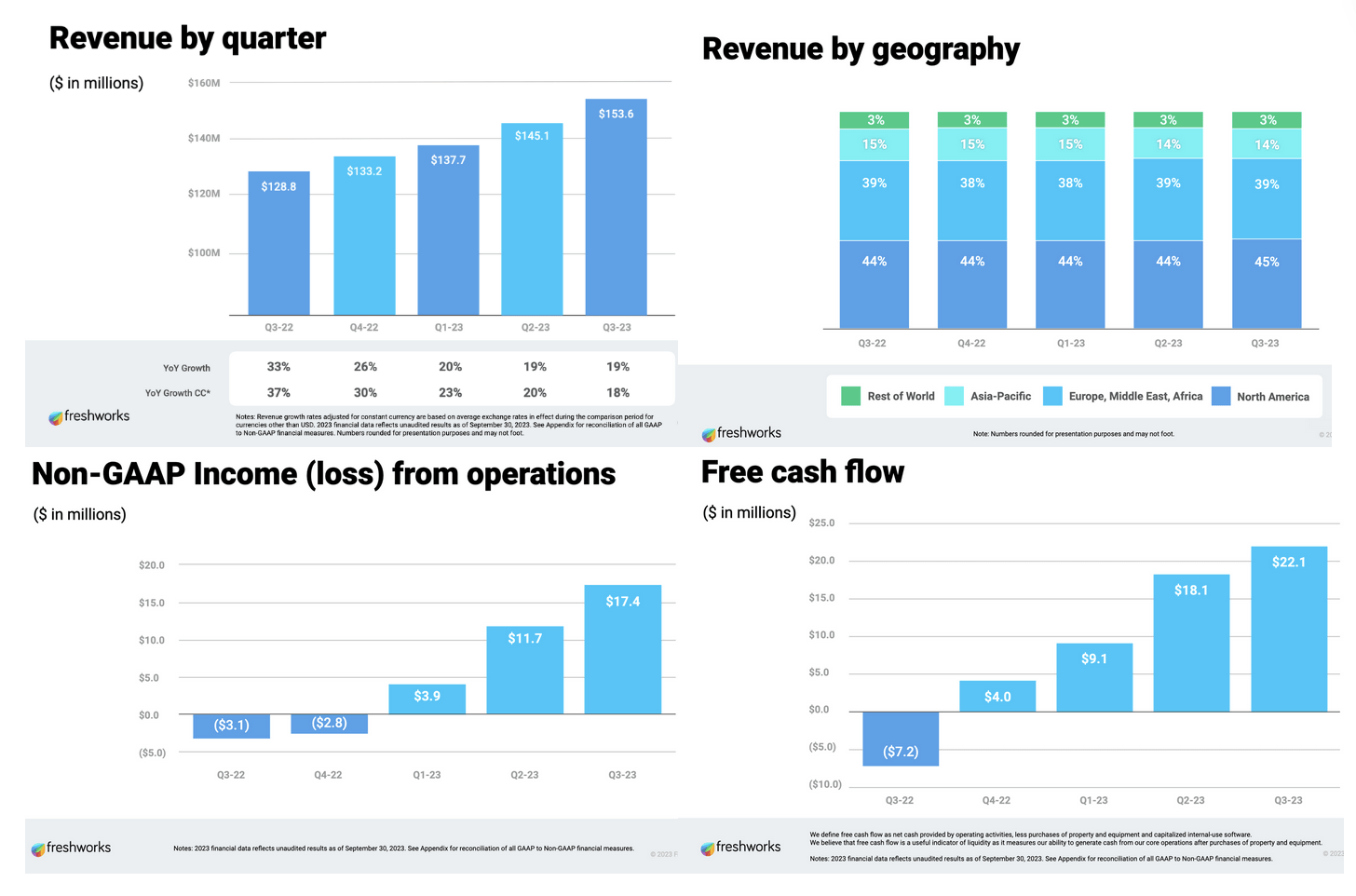

On reviewing their monetary metrics, I discover it encouraging to see robust progress in Freshworks’ numbers, as will be seen under.

FY23 Q3 investor presentation

I additionally noticed the large bump of their FY23 Q2 working revenue and free money, which coincides with the rise within the Prospects >$50K ARR (Giant Enterprises) that was seen in the identical FY23 Q2 quarter as we noticed earlier.

Valuation Fashions counsel robust upside

Transferring on to estimating the worth of Freshworks, I’ll use a few of the targets that administration had issued of their long-term steering that I known as out within the earlier part. Administration has instructed earlier that they are going to be utilizing the Rule of 40 enterprise metric that’s often seen in SaaS enterprise corporations as Freshworks’ north star targets.

FY23 Q3 investor presentation

Earlier than I transfer on to the precise valuation, I do need to be aware that the one debt the corporate carries is within the type of a long-term working lease for workplace areas. The current worth of those working leases quantities to $30.8 million, however with over 1.2 billion in money and money equivalents, I don’t see any threat from excellent money owed.

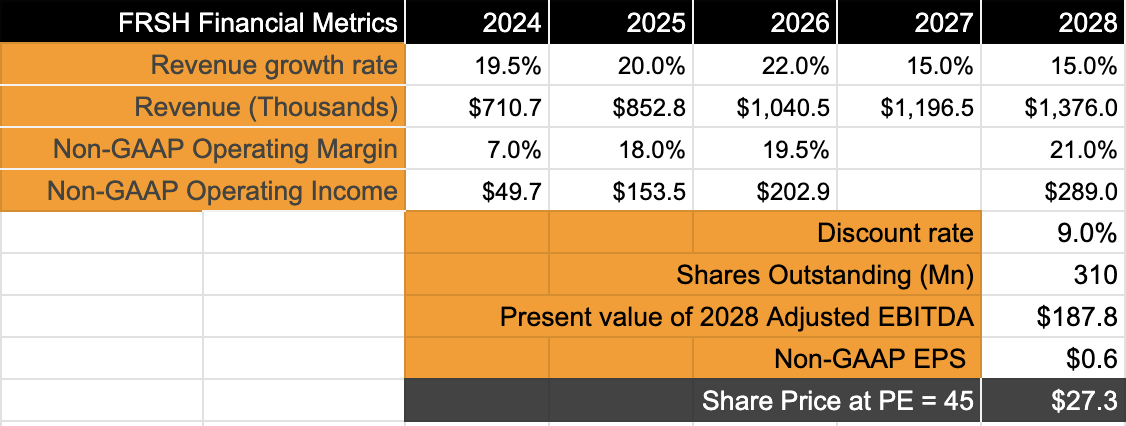

Consensus estimates put Freshworks income at 19.4%, which I’ll take as my base case assumption. Assuming income to develop at a median annual tempo of 20.5% to $1.04 billion in FY26, I’ll put my estimates in keeping with Freshworks’ inner targets to develop to a $1 billion firm by FY26. After that, I count on progress to taper off barely in my base case. I count on working margins to develop considerably from their 7% projected margins in FY24 to administration’s base case of 20% in FY26. After that, I count on continued positive aspects in working revenue pushed by sustained give attention to producing free money.

Creator

Primarily based on these assumptions, I count on working revenue to develop at a CAGR of 55%, which may be very spectacular. These progress charges name for a PE of not less than 45 since Freshworks can be rising its revenue virtually 7 instances sooner than the S&P 500’s common 8% revenue progress charge. I see not less than 23% upside from present ranges.

Dangers & Different Components to Take into account

I had talked about earlier in regards to the ITSM, ITOM, and CX markets that Freshworks operates in. These markets are fiercely fought by some massive and profitable incumbents, resembling Salesforce (CRM), HubSpot (HUBS) within the CRM area, ServiceNow (NOW), and Atlassian (TEAM) within the ITSM/ITOM area. Furthermore, new entrants like Klaviyo (KVYO) instantly compete with Freshworks. Whereas Freshworks focuses on SMBs, its enlargement into the bigger enterprise market could also be troublesome because of the success of enormous corporations that already maintain management positions. However the rising tendencies in Freshworks’ bigger enterprise prospects we noticed a pair sections earlier together with Freshworks’ product differentiation technique encourage me.

One other threat that Freshworks faces is the potential for financial downturns. Since a big a part of Freshworks’ person base remains to be SMB prospects, it does face the chance of cyclical tendencies in its gross sales cycles in circumstances of recessions and financial downturns. Nevertheless, right here once more, I consider these fears are overstated for the reason that macroeconomic scenario is getting higher, and economic projections for 2024 are looking up. Furthermore, Gartner’s projections for worldwide IT spending to extend by 8% will give Freshworks an extra enhance.

Conclusion

In abstract, the present worth of Freshworks doesn’t replicate the projections that its administration is guiding primarily based on its FY26 targets. Their enterprise-focused buyer acquisition technique, along with their margin enlargement plans, is sufficient for me to consider that there’s extra room for the valuation to develop. I charge Freshworks as a robust purchase.