JazzIRT/iStock by way of Getty Pictures

I coated TransMedics Group, Inc. (NASDAQ:TMDX) in my e-newsletter for the primary time again in February 2021, when the inventory was at $26 per share, and TransMedics had not but launched its Nationwide OCS Program (NOP), which has been a recreation changer for the corporate, utterly remodeling it ever since.

A number of months in the past (September 2023), after virtually 2.5 years, I revealed a second deep-dive on TransMedics (7,000+ phrases) in my funding group, Fundamental Growth Investor, protecting every part from the corporate’s story and near-term/long-term catalysts to the current acquisition of Summit Aviation and the 3-5 12 months worth targets based mostly on my funding mannequin.

Right now, TransMedics is one in all my top 5 positions, and on this mini-writeup, I’ll present an replace after the current quarter (Q3 2023) and clarify why I’m nonetheless bullish on the corporate.

Thesis

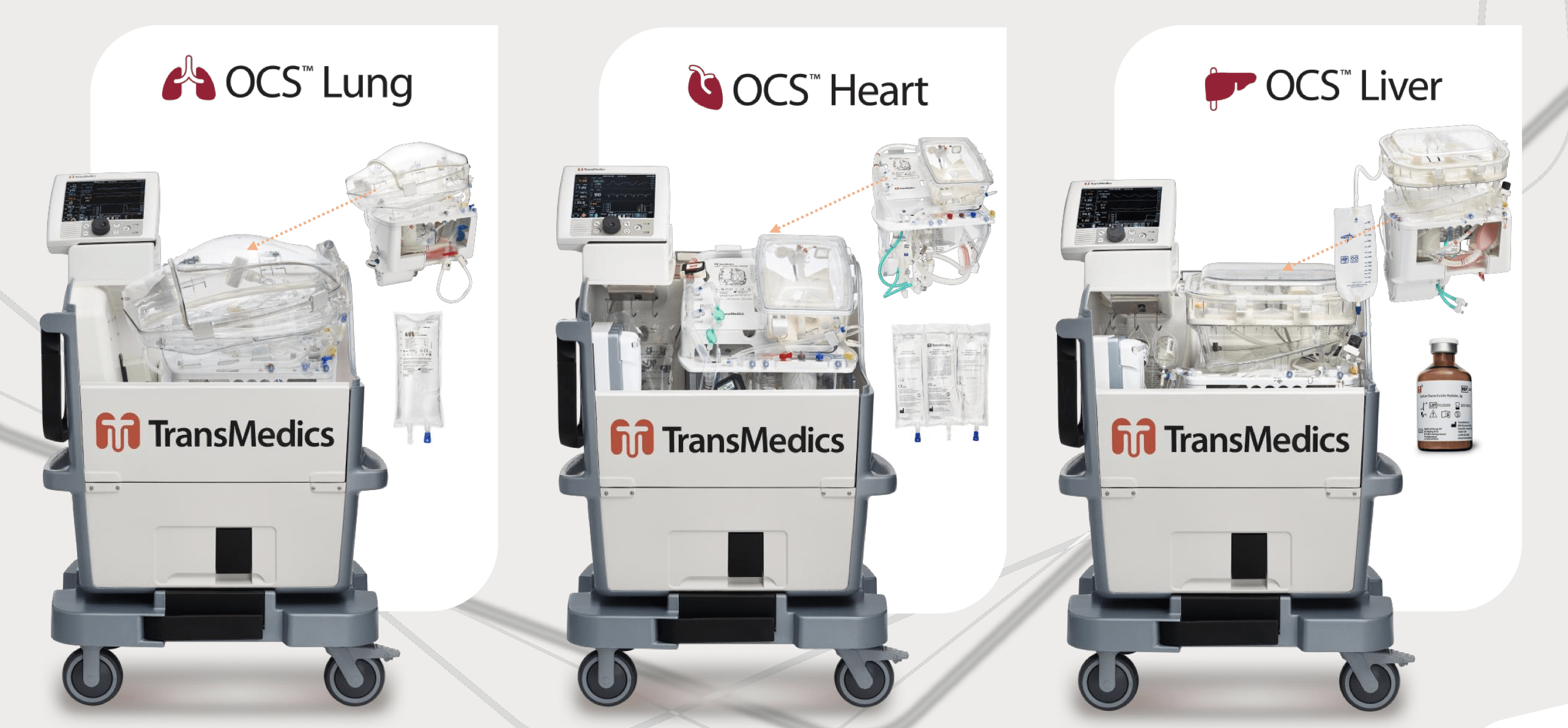

My funding thesis for TransMedics is centered round its modern Organ Care System (OCS), a expertise that has the potential to really revolutionize organ transplantation. OCS expertise represents a major development over conventional static chilly storage strategies used for organ transplantation and a a lot superior various to different heat perfusion storage options, comparable to XVIVO and OrganOx.

This positions TransMedics as a frontrunner within the area of organ transplants, with a major first-mover benefit, significantly as they maintain FDA approvals for coronary heart, lung, and liver transplantation – the one FDA-approved machine for a number of organs.

TransMedics Investor Presentation

The important demand for organ transplants, an area the place provide and utilization are extremely mismatched, highlights the necessity for such expertise. OCS is nicely positioned to bridge this hole, offering TransMedics with years of steady development.

The corporate is projected to achieve substantial income development, anticipating to surpass $1 billion by 2030 from an estimated $228.9 million in 2023. I anticipate TransMedics to achieve $1 billion in income earlier, perhaps two years earlier, as a result of its growing involvement within the rising variety of transplants. In truth, TransMedics, with its OCS expertise, is a major enabler of elevated donor utilization. The corporate, basically, creates the marketplace for itself.

Proper now, TransMedics is unprofitable, however at this charge of development, it ought to turn into adjusted EBITDA optimistic in 2024 earlier than turning worthwhile on a web revenue foundation in early 2025. I imagine TransMedics might be worthwhile in 2025; nonetheless, it’ll rely on hiring prices, R&D, S&M, and extra bills associated to constructing out their aviation and logistics enterprise.

The corporate’s strategic transfer into aviation, constructing its personal fleet of small airplanes to move donor organs, ought to solely speed up the expansion within the coming years.

My thesis additionally acknowledges some potential dangers, together with the complexities concerned in integrating an aviation division, the corporate’s indebtedness, shareholder dilution, operational readiness in assembly growing demand, and some others I cowl extensively in my TransMedics deep dive.

Nonetheless, a mix of TransMedics’ technological innovation, market management, development potential, and aggressive benefits make my thesis robust sufficient to justify a place within the high 5 in my funding portfolio.

I additionally put religion in Waleed Hassanein, TransMedics’ founder and CEO, who not solely has pores and skin within the recreation however can also be some of the revered folks within the area. He anticipates 10,000 transplants yearly in 5 years’ time, a major improve from the two,000 transplants scheduled for 2023. With a monitor report of beating and elevating its projections, I’m assured that TransMedics will efficiently obtain that focus on.

TransMedics

Quarterly Replace

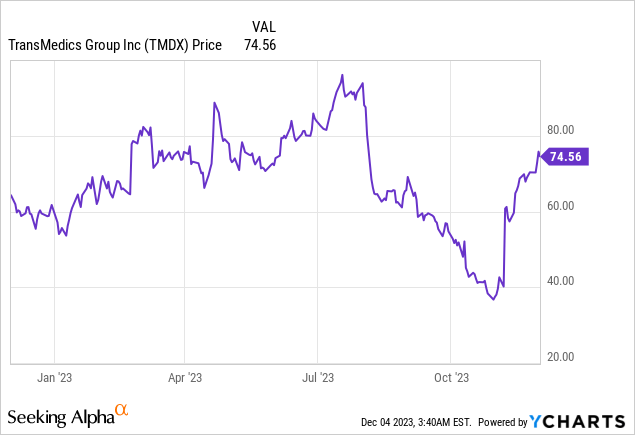

Talking about beating and elevating, TransMedics delivered one more excellent and, to some extent, shocking quarter. EPS in Q3 2023 got here at $0.07, beating estimates by $0.20, whereas income was $66.43 million, a whopping 158.65% year-over-year improve, surpassing expectations by $17.25 million.

The very best a part of this earnings is that TransMedics has considerably raised its 2023 outlook. Annual income steerage for 2023 elevated to between $222 million and $230 million, representing 138% to 146% development over 2022, from a previous vary of $180 million and $190 million.

It’s the foremost cause why the inventory bounced again from its October lows when it reached its 52-week low at $36.42 per share, primarily as a result of traders’ skepticism across the firm’s acquisition of Summit Aviation and its capacity to efficiently handle and function an aviation fleet – one thing that’s completely out of TransMedics’ scope and one thing that may considerably strain gross margins any more.

Within the third quarter, TransMedics accomplished the acquisition of eight planes and outlined plans to broaden its fleet to 15-20 by the second half of 2024. This quarter, the corporate initiated a restricted launch of the transplant logistics service, leading to $2.1 million from the brand new, transplant-related aviation and logistics choices.

The NOP (Nationwide Organ Preservation) program continued to considerably contribute to income development, and the corporate is on monitor to finish over 2000 NOP transplants in 2023.

On the not-so-bright aspect, the corporate has seen a substantial lower in gross margin, from 70% in Q2 2023 to 61% in Q3 2023. This lower is attributed to a number of elements, primarily as a result of transient inefficiencies – the previous constitution enterprise is phasing out, whereas the brand new transplant enterprise is simply beginning, with neither working at full scale through the quarter. As soon as logistics is totally operational, the gross margin is anticipated to enhance, although to not the earlier stage.

The acquisition-related prices and the acquisition of eight jets influenced the rise in complete working bills, dragged down web loss to $25.4 million from the $7.4 million loss in the identical quarter of the earlier 12 months and $1 million within the prior quarter of 2023, and resulted in a major lower in free money circulation, from destructive $7 million in Q2 2023 to destructive $114 million in Q3 2023.

TransMedics nonetheless maintains a powerful money place, ending the third quarter with $427.1 million. The corporate’s important investments in acquisitions and logistics infrastructure exhibit a strategic effort to broaden its service capabilities and infrastructure, which can ultimately begin to repay.

Development Drivers

TransMedics has quite a lot of close to and long-term development drivers that may profoundly influence its income development and profitability.

A key focus for the corporate is the growth of its Nationwide OCS Program (NOP), which is crucial for growing the adoption and use of its Organ Care System expertise by transplant facilities. Solely a small proportion of U.S. transplant facilities presently make the most of this expertise on a relentless foundation, offering important room for development. Increasing the NOP is especially necessary as a result of it’s anticipated to be a serious supply of quantity and income for the corporate within the coming years.

To facilitate the Nationwide OCS Program additional, the corporate is constantly bettering its OCS expertise. TransMedics is already engaged on next-generation OCS expertise, which can carry improvements like cloud connectivity, automation, and distant management. This new expertise, which incorporates new perfusion techniques for hearts and lungs, is anticipated to enter scientific trials by 2025.

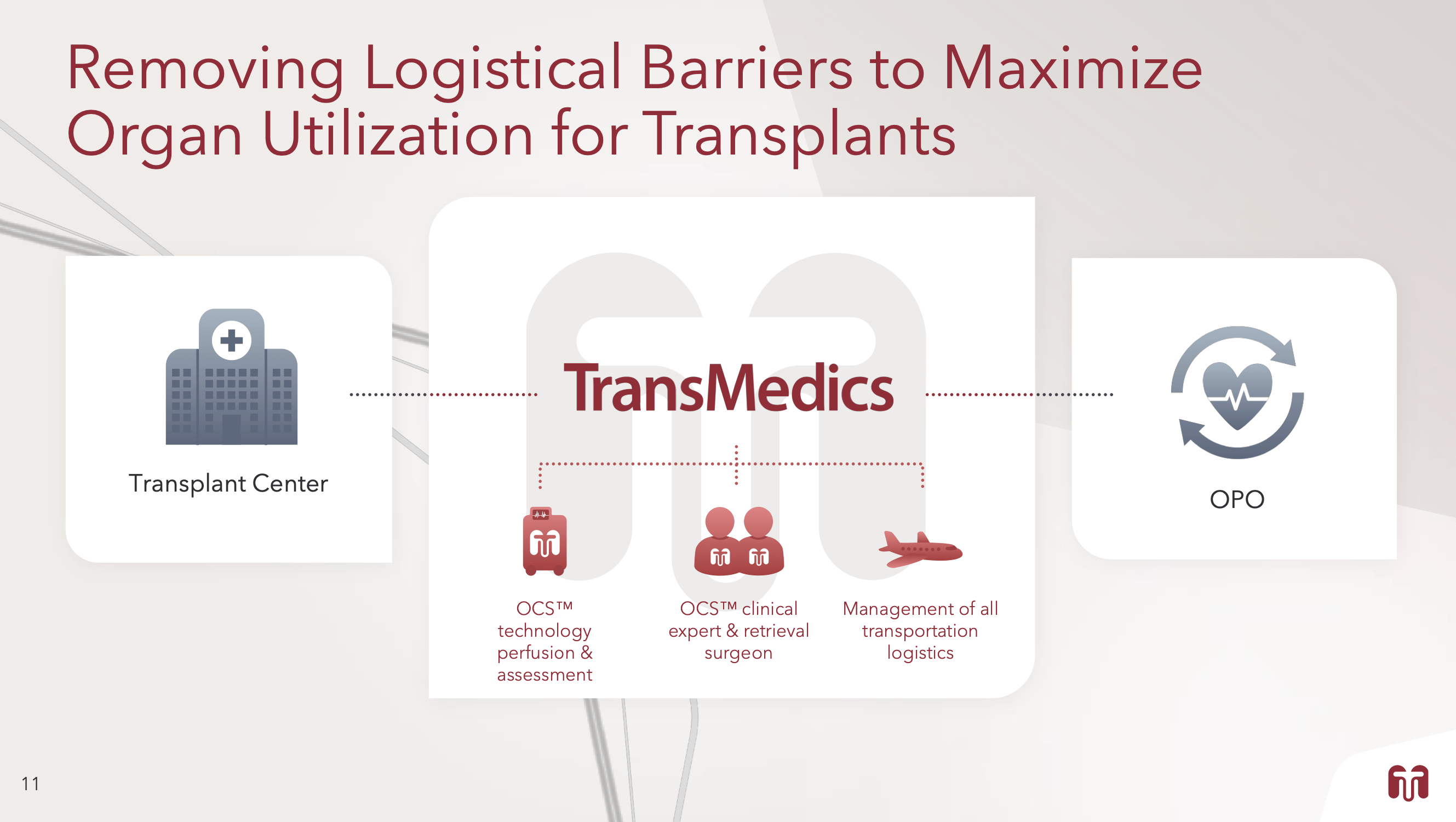

One other main catalyst for TransMedics is the event of its aviation operations. The corporate is now establishing its personal air transportation fleet, which marks a strategic shift from counting on personal jet brokers. The goal right here is to regulate your complete logistics course of from donor to recipient to immediately handle all NOP transplant quantity within the U.S. by the second half of 2024.

TransMedics Investor Presentation

This integration will assist TransMedics handle transplant volumes extra effectively and overcome earlier logistical challenges. Most significantly, it’ll additional cement TransMedics’ aggressive benefit, making the competitors at this stage virtually out of date.

Lastly, TransMedics is trying to broaden globally, significantly in Europe and Asia-Pacific markets. Regardless of being current in Europe for over a decade, the corporate has had a restricted success charge there thus far as a result of manner reimbursements work in these areas. I imagine there may be important untapped potential, particularly if reimbursement insurance policies like these within the U.S. are ultimately adopted. TransMedics is presently growing supplies and conducting scientific trials to facilitate this growth. If profitable, this can present a further increase to income, which isn’t projected within the present estimates.

Valuation

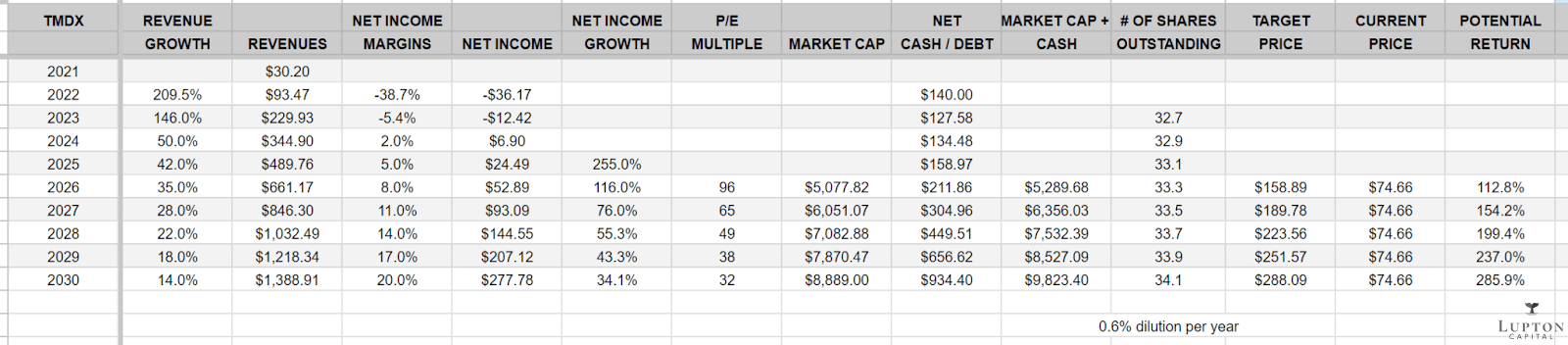

Now that TransMedics is getting ready to profitability (it could have been worthwhile in Q3 2023 if it wasn’t investing within the aviation and logistics enterprise), the inventory will commerce at a premium a number of as a result of EPS development must be within the triple digits for the following 3-4 years as web revenue margins enhance from destructive 5% in 2023 to optimistic 8% in 2026 to 14% in 2028 and even perhaps 20% by the tip of the last decade. If you happen to take a look at different extra mature MedTech corporations, most have web revenue margins north of 20% by the point income development has slowed into the teenagers, and I count on TransMedics might be no completely different.

TransMedics could be very a lot a hypergrowth inventory that’s nonetheless investing within the enterprise and constructing its moat, a lot completely different than Medtronic (MDT) or Intuitive Surgical (ISRG), which makes it a bit more durable to provide you with a good market valuation for TransMedics for the reason that subsequent 5-6 years is much less predictable. Under is my funding mannequin going out to CY2030 with my revenues and web revenue margin estimates, which will get us to some tough worth targets. Based mostly on my funding mannequin and estimates, I do imagine TransMedics has 100% or extra upside over the following 2-3 years and 200% upside over the following 4-5 years.

Creator’s Funding Mannequin

Conclusion

TransMedics is among the largest positions in my funding portfolio as a result of it has all of the attributes of a long-term winner, assuming continued income development (5x over the following six years) and increasing margins, which results in substantial EPS development, which is a very powerful ingredient when looking for the very best inventory outperformers.

TransMedics has elevated revenues virtually 10x over the previous few years, however that is simply the tip of the iceberg now that coronary heart, lungs, and liver are all accredited. We should always see OCS Kidney accredited within the subsequent couple of years, which might be one other catalyst for the inventory.

Simply a few months in the past, traders had been giving up on TransMedics due to the corporate’s choice to push into aviation and logistics. Nonetheless, after an unimaginable Q3 earnings report, those self same traders are flocking again to the inventory as a result of they perceive that strategic choices would possibly trigger some near-term margin compression, however over the long run, it offers TransMedics a dominant place and permits it to assist its aggressive development objectives.

Suppose the CEO is right and TransMedics can go from ~2,000 OCS procedures in 2023 to ~10,000 OCS procedures. In that case, the one manner that occurs is with its personal aviation fleet, to not point out in some unspecified time in the future, we’d see TransMedics surgeons doing the precise procedures, which simply will increase the entire addressable market, or TAM, even additional.

As soon as I determine a possible multi-bagger and construct out a big place, I not often wish to see that firm get acquired as a result of it places a ceiling on the upside. Nonetheless, I’ll point out it right here as a result of I feel there is a 30-40% likelihood that TransMedics might be acquired within the subsequent 18-24 months. If it does occur, I am hoping it isn’t till 2025, and the worth is north of $150+ per share, which nonetheless leaves a 100% upside from the present worth.