Klaus Vedfelt/DigitalVision by way of Getty Photographs

Thesis

Leveraged loans have confirmed themselves because the ‘go-to’ asset class throughout this financial tightening cycle. With an aggressive Fed that raised charges repeatedly, however an financial system that refused to bend and has confirmed resilient, leveraged loans have been one of the few locations the place traders may have made very engaging threat/reward returns.

We’ve got repeatedly praised the asset class, particularly when the market began pricing in aggressive fee cuts, and thus some market pundits began speaking in regards to the ahead unattractiveness of floating fee loans.

In at the moment’s setting, although, we’re witnessing a distinct dynamic. Whereas we consider charges will keep larger for longer, with a primary Fed reduce in mid-2024, we’re nonetheless witnessing document tight credit score spreads.

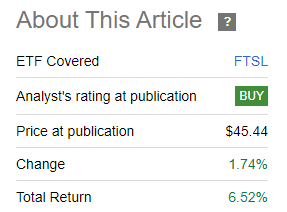

We first began protecting the First Belief Senior Mortgage Fund ETF (NASDAQ:FTSL) in mid-2023 with a purchase score, and are actually re-visiting the title given the prolonged transfer in leveraged mortgage spreads. Since our score, the ETF is up considerably:

Score (In search of Alpha)

The fund is up over +6.5% with a low volatility and customary deviation and is at the moment yielding over 8% on a 30-day SEC yield foundation.

We’re seeing a variety of ‘alarmist’ articles being printed round this asset class, and we strongly disagree with them. Whereas we’ve got seen a tick-up in default charges and a big tightening in spreads, we consider FTSL now not represents a sexy shopping for alternative, however on the identical time, it’s a strong fund to carry. On this article, we’re going to define what has occurred since our final protection of the title and our view on transferring the score to ‘Maintain’ on the title.

Charges have stayed larger for longer

Charges have stunned many pundits by staying larger for longer. Not that way back, again in December 2023, the market was pricing aggressive cuts, with the primary one beginning in March 2024. It’s now not the case, with most analysts at giant banks penciling in mid-2024 fee modifications from the Fed. That interprets to larger SOFR charges till that time, which in flip means leveraged loans will preserve yielding excessive returns.

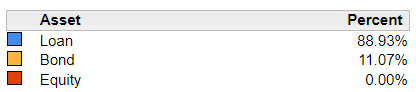

Leveraged loans are floating charges, and so they normally pay 1- or 3-months SOFR plus a ramification. The fund holds 89% of its collateral in leveraged loans and, thus is most uncovered to this asset class:

Fund Composition (Reality Sheet)

The collateral has a mean yield to maturity of 8.3%, thus equal to a tough 300 bps over SOFR when it comes to holdings. A lot of the fund holdings are ‘B’ rated, with solely 4% of the collateral in CCC names.

The mathematics could be very easy for FTSL. So long as charges keep excessive, the fund will ship a excessive money stream to holders. Even when the Fed aggressively cuts charges to 4% this yr, the fund will nonetheless have the ability to ship a yield of over 7% given its present collateral composition.

Credit score spreads are extraordinarily tight, not a sexy entry level

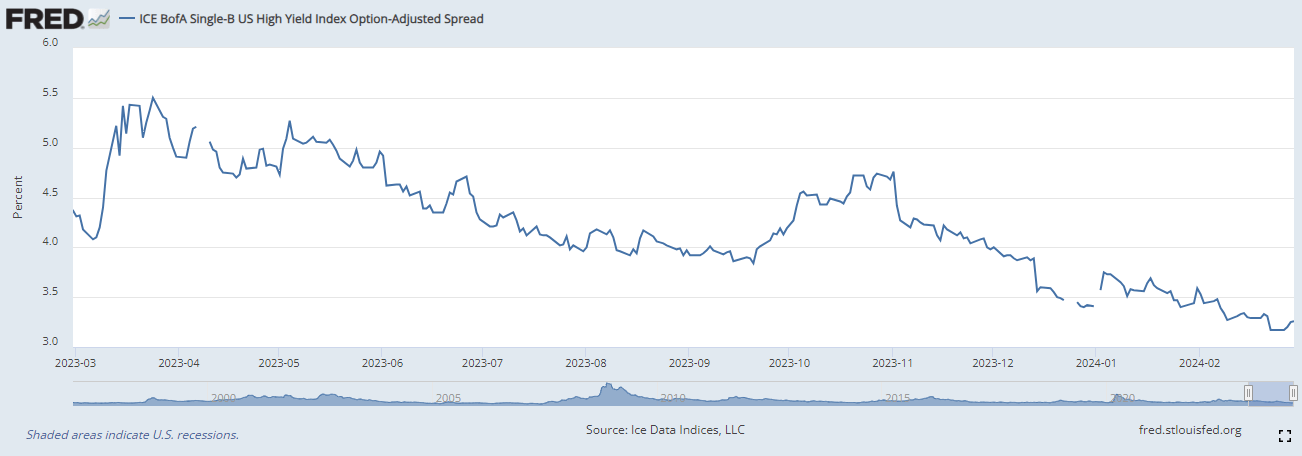

We’re revisiting this title at the moment given the big tightening in credit score spreads and the dissemination of some ‘alarmist’ analysis relating to this title. Spreads have certainly compressed:

Single-B Spreads (The Fed)

The above represents the ICE BofA single-B excessive yield index OAS, a proxy that we are able to use for the leveraged mortgage area as properly. We are able to observe from the graph an excessive tightening to three.2%, from highs of 5.5% throughout the regional banks disaster in April 2023.

The markets are telling us a delicate touchdown is coming, and credit score spreads are actually pricing such a story. If a delicate touchdown does materialize, then count on credit score spreads to remain low, all whereas charges will transfer decrease because the Fed cuts.

FTSL has a length of 0.5 years, therefore its low volatility, thus a gradual lower in SOFR shouldn’t have any materials influence on its worth. Only a lower in dividend yield.

Conversely, if we do get a credit score occasion and a widening in spreads, we are able to pencil in a -2% drawdown for this title, in line with its historic efficiency.

Whereas credit score spreads are tight, and thus they don’t symbolize a sexy entry level, the fund is nonetheless a valiant maintain for an investor, given its restricted drawdown profile even throughout risk-off eventualities.

1st lien loans have seniority within the capital construction

One forgotten side of funds like FTSL is their composition. The ETF incorporates principally 1st lien leveraged loans, devices which might be senior within the capital construction. A ‘lien’ means a safety is roofed by exhausting belongings owed by a sure firm, and bondholders or fairness holders have to see the first lien loans absolutely paid earlier than getting any recoveries in case of a default.

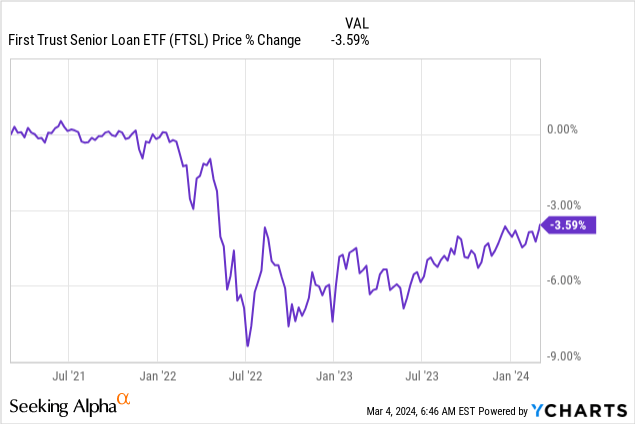

This seniority within the capital construction accounts for the low volatility related to leveraged loans, and their propensity to backside out at excessive worth ranges. If we take a look at FTSL’s worth efficiency prior to now years, we are able to observe the advantages of being invested in leveraged loans:

The fund is now very near its pre-Fed tightening worth, and extra importantly, had a most drawdown of solely -9% throughout the preliminary levels of the Fed cuts. Thoughts you that treasury funds had drawdowns exceeding -15% throughout the identical time interval as a consequence of their length profile.

Because the preliminary shock from larger charges, the fund has solely exhibited a -3.5% most drawdown profile, a really low quantity that speaks volumes relating to the robustness of the underlying asset class.

Conclusion

FTSL is a leveraged mortgage ETF. Not like CEFs, exchange-traded funds don’t run leverage of their construction outright (except designated as a 2x fund by way of swaps), thus exhibiting decrease volatility. We first began protecting the title in August 2023 with a purchase, and the fund has delivered since then. We don’t count on Fed cuts till mid-2024, however credit score spreads are certainly very slim at the moment. We just like the title and maintain it, however don’t suppose the present worth level represents a sexy entry level anymore, thus our downgrade to ‘Maintain’ for the title. We’re of the opinion retail traders ought to ignore alarmist analysis on the title, and proceed holding the fund till the Fed begins slicing charges, and we are able to reassess the time horizon and predicted dividend yield on the fund.