JHVEPhoto/iStock Editorial through Getty Photographs

Shares of Further Area Storage Inc. (NYSE:EXR) have had a booming rally over the previous two months, rising about 50%, which has introduced them again to the flatline over the previous 12 months with this rally unwinding what had been a major weak point. Whereas the corporate operates a really defensive enterprise, until traders count on long-term rates of interest to say no, I might benefit from the restoration to cut back holdings.

Looking for Alpha

Within the firm’s third quarter, adjusted funds from operation fell by 8.6% to $2.02 from $2.21 a 12 months in the past. These outcomes do embody the dilutive influence of its Life Storage acquisition. After being $0.10-$0.15 dilutive this 12 months, it ought to increase FFO by 1% throughout Q1 2024 when $100 million in synergies are met. That is solely marginally accretive, and EXR might want to generate elevated income from these properties to make this transaction a really worthwhile one.

Unadjusted FFO was $1.69 within the quarter. This $0.33 distinction included $0.07 of non-cash gadgets regarding its alternate of Life Storage debt and amortization of intangibles. Moreover, there was $0.26 or $54 million of integration bills regarding the merger. Given this was a multi-billion greenback transaction and that Life Storage is now absolutely built-in into EXR’s programs, it is a cheap expense stage, and as we take into consideration valuing the enterprise, I might look previous this one-time expense.

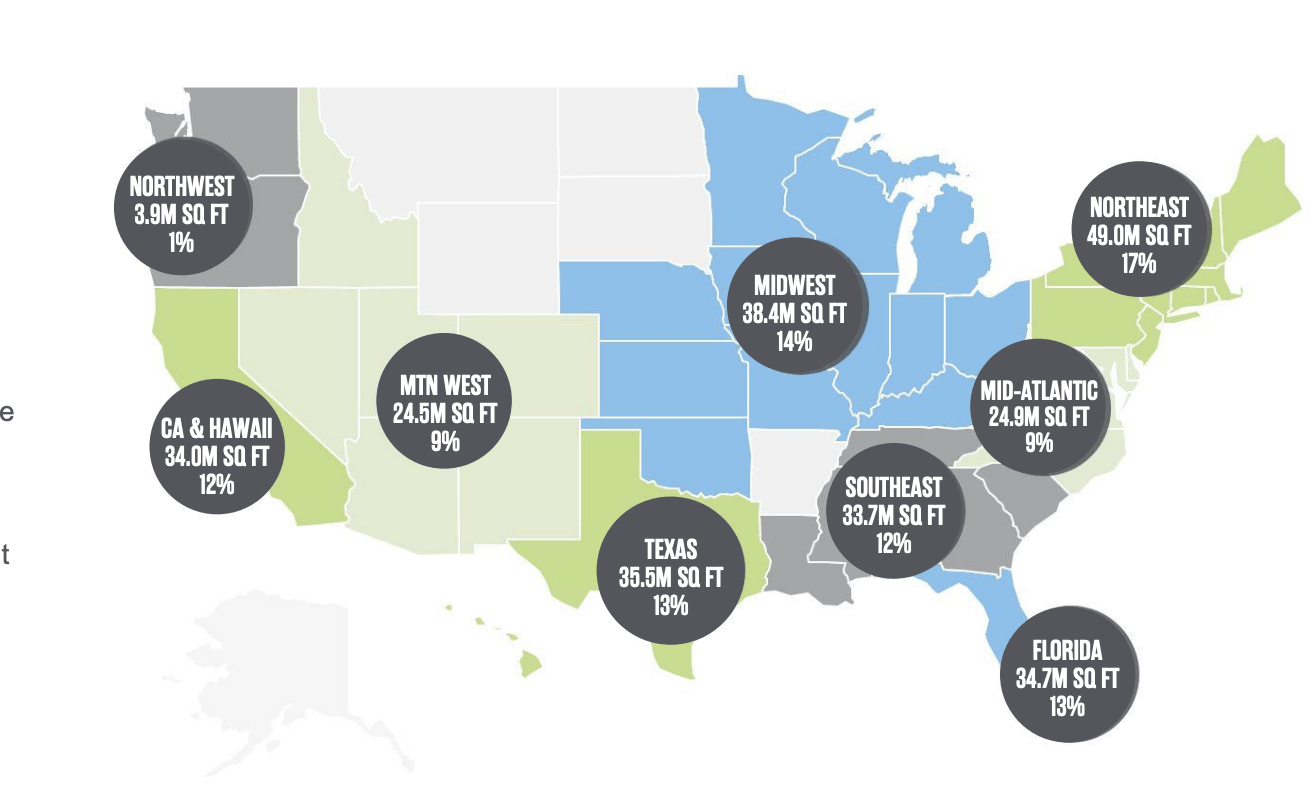

Further Area is now the main self-storage firm within the nation with about 14% market share in what’s a extremely fragmented business. Given its massive scale, EXR operates throughout the nation, as you may see under. California, Texas, and Florida are its largest markets, every comprising about 1/eighth of the enterprise.

Further Area Storage

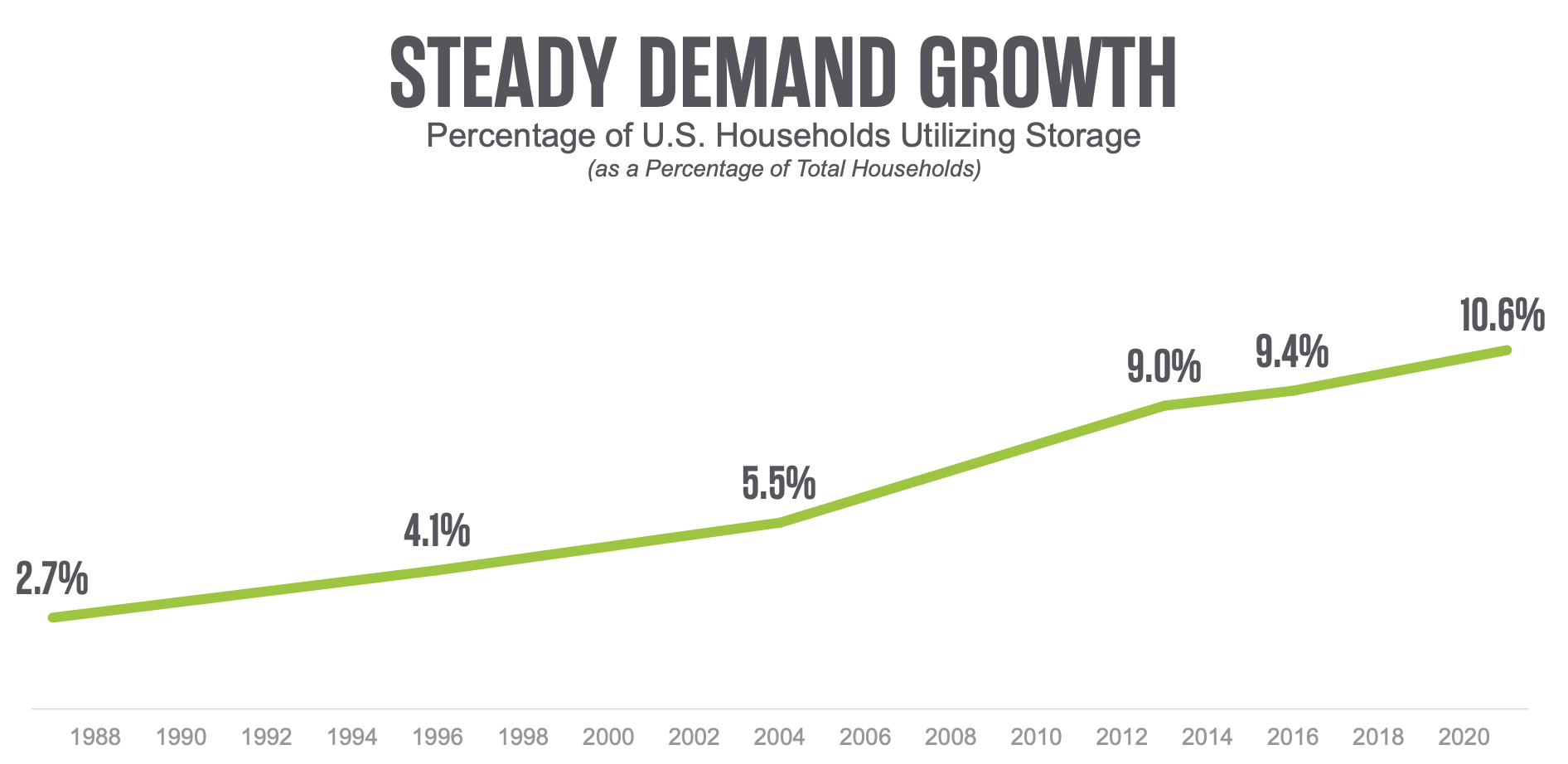

Due to its geographic diversification, EXR will not be excessively uncovered to any market; fairly, it’s tied to nationwide tendencies in self-storage, working 3,651 areas, 52% are wholly-owned, 13% are joint ventures, and 35% are managed. That is an business that has confirmed its sturdiness with income that has been secure throughout downturns and elevated penetrations with 1 in 10 households utilizing a storage unit. Thanks to those favorable dynamics, Further Area has grown its dividend for 13 years, and over the previous 5, it has delivered a 14% dividend progress charge.

Further Area Storage

Whereas there are lots of short-term use circumstances for self-storage; as an example, a university scholar storing their furnishings in the course of the summer season between semesters or a household between strikes, a major share of Further Area’s enterprise comes from extra everlasting customers. 61% preserve their unit for over a 12 months and 45% over two years. The common tenant has held their unit for 34.4 months, up 1 month from final quarter. Particularly as individuals become old, there might be gadgets which are onerous to half with for sentimental causes however do not have to be stored in a home. With the growing old of the child boomer inhabitants, this has made self-storage an more and more interesting product, driving comparatively low turnover. This has additionally helped preserve rental charges elevated for current prospects.

Whereas the present buyer base has been strong, we’re seeing some slowing in new-customer signups because the COVID increase in self-storage fades. Whereas same-store income is up 3.9% year-to-date, it has been decelerating all 12 months, coming in at 1.9% in the course of the third quarter. Occupancy averaged 94.4% in the course of the quarter, a wholesome stage, however 100bps decrease than final 12 months with the enterprise now working on a extra normalized footing.

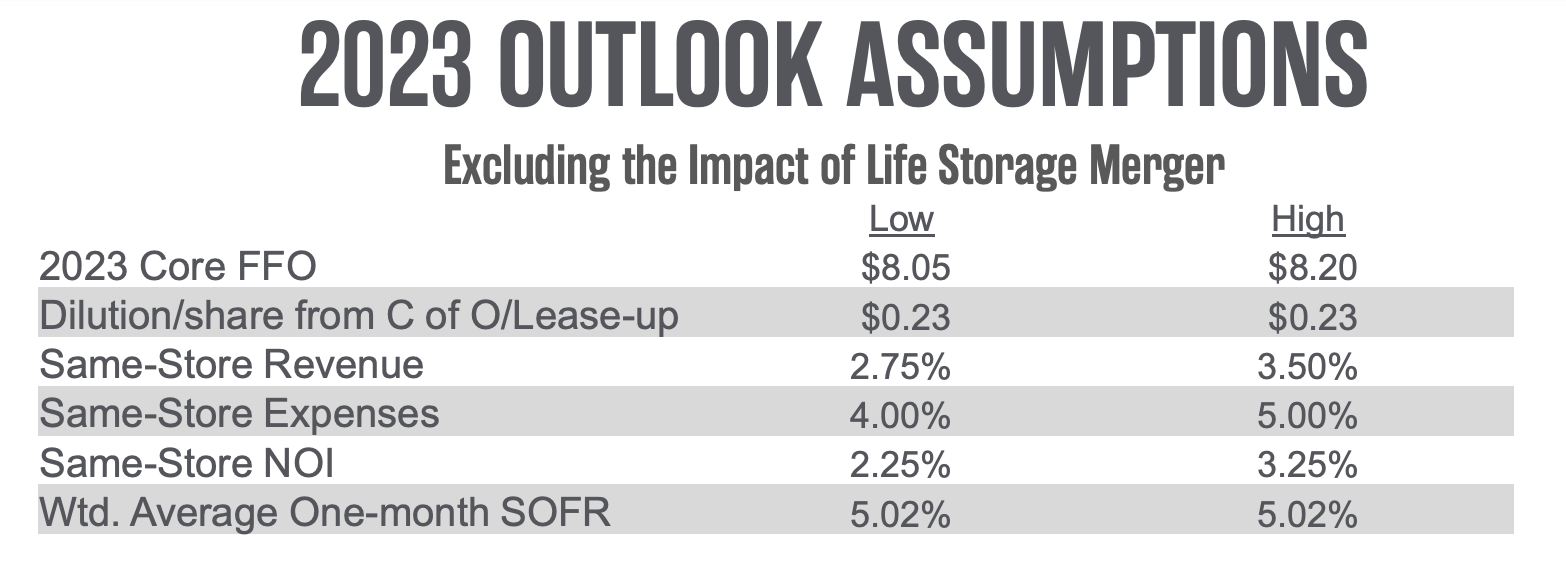

Alongside Q3 outcomes, administration refreshed steering, trimming its EPS vary by $0.05 on each ends whereas growing the low-end of its same-store income steering by 0.25%. This steering implies that same-store income progress will stay constructive in Q4, doubtless up by about 0.8%. That factors to continued deceleration, although not as unhealthy as had been feared, serving to to contribute to the share value restoration.

Further Area Storage

One problem for the enterprise is that the two.2% hire progress will not be maintaining with bills. On a same-store foundation, bills rose by 5.7%, resulting in a modest 0.7% improve in internet working revenue. Payroll and property working bills rose by 1.7%. Property taxes rose by 4.9% whereas advertising rose by 20% and insurance coverage rose by 31%. Whereas insurance coverage is lower than 5% of bills, it’s driving about 20% of the expense progress, negatively impacted by the enterprise’s massive publicity to Florida the place insurance coverage charges have risen materially.

We’re prone to see some moderation in expense progress subsequent 12 months, due partially to raised comparisons, however an elevated stage of bills is prone to proceed to constrain NOI progress. To offset this, Further Area will now must ship on income synergies from its Life Storage buy in 2024, having already absolutely built-in it into their programs in the course of the quarter. Most notably, Life Storage areas have greater than 100bp decrease occupancy than EXR areas. Closing this hole ought to drive FFO will increase. Moreover, rents at Life Storage are 15% under Further Area. EXR underwrote the monetary rationale for the merger assuming it may possibly recoup half of this gap-if it may possibly shut extra of this hole over time, FFO accretion ought to enhance. It will doubtless be a multi-quarter course of to keep away from extreme attrition.

As we stay up for 2024, we now have seen occupancy present indicators of stabilizing within the low-to-mid 94% space. With some profit from Life Storage, we should always not see additional deterioration right here. I might search for hire progress to stay within the low 2% space, fairly than decelerate materially additional. That’s as a result of provide is slowing with simply 18% of locations facing a new competitor from 28% in 2019. Moreover, its buy of Life Storage expands its managed-not-owned platform, a capital-light approach to develop operations. In opposition to this, we’re prone to see non-wage price pressures run hotter than rents, constraining FFO progress.

One tailwind for the corporate could possibly be decrease rates of interest. EXR carries $11.3 billion in debt, and it has $3.35 billion in variable-rate debt. With the Federal Reserve forecasting three charge cuts subsequent 12 months, curiosity expense might decline considerably. EXR additionally has no 2024 maturities with $1.8 billion in debt due in 2025, decreasing its must refinance any low-cost debt in a better charge setting. With Life Storage ceasing to be dilutive by Q1 2024, this factors to about $8.30-$8.60 in 2024 FFO. Shares provide a 4.2% yield, and EXR has a protection ratio of 1.3x. That may be a safe however not extreme protection stage, which suggests the payout is protected, however that dividend progress is unlikely to be considerably quicker than FFO progress, in my opinion. General, shares have a 5.6% ahead FFO yield.

As an analyst, I’m usually looking for a ten+% return. To attain that, EXR would wish to generate about 5-6% annual dividend progress, which I view as considerably optimistic, at the least for the following two years contemplating hire progress is working considerably under this stage. It additionally stays to be seen if it may possibly convey Life Storage outcomes to EXR ranges or if there will probably be any cannibalization from geographic overlap. Furthermore, it appears to me that rates of interest, not EXR’s personal efficiency, are the first driver of shares.

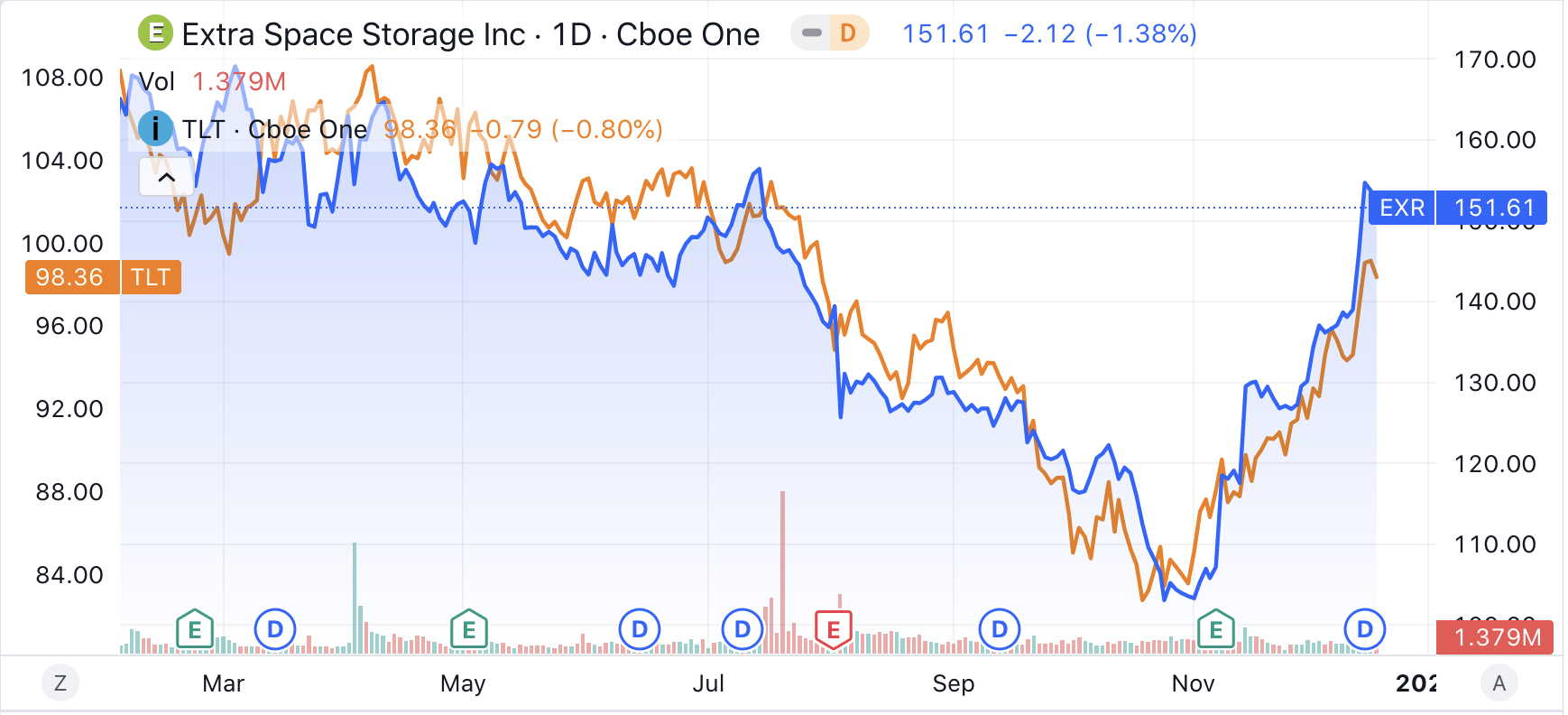

The under chart compares EXR to TLT, the ETF that tracks long-dated treasury bonds. Lengthy-dated treasuries assist set the low cost charge for actual property valuations. The correlation is uncanny, although EXR might have overshot treasuries considerably on this newest rally.

Looking for Alpha

Whereas it appears more and more doubtless the Federal Reserve will probably be chopping charges, with 30-year treasury yields having fallen by 100bps in only a few weeks, a lot of that is now discounted into markets. Certainly, whereas the Fed projects 3 rate cuts subsequent 12 months, the market has gone so far as pricing in 6 cuts. This leaves me involved that if charges do rise again in any respect as a result of markets have gotten overly optimistic about Fed easing, EXR, alongside different REITs, might underperform.

Now if you happen to count on long-term yields to proceed to say no, I think EXR can carry out fairly nicely. Nevertheless, given restricted FFO progress, excluding the merger influence, I might emphasize you’re largely making a charge guess. At a 4.2% yield, EXR has a reasonably full valuation, reflecting the standard of the self-storage business’s long-term fundamentals. If it yielded 6%, I consider traders could be compensated for the danger of charges heading again up, however not at 4%. I might benefit from this restoration to take some EXR off the desk, and if shares fall again under $140, that may present a greater entry level.

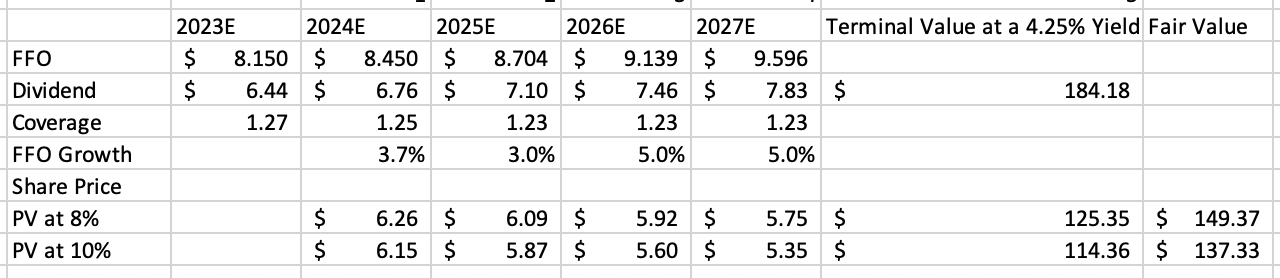

I attain this valuation primarily based on my expectation for ~3-4% FFO progress over the following two years as it really works by way of its Life Storage buy and faces slower new rental exercise, earlier than it returns to a extra trend-like 5% progress charge thereafter, given favorable long-term fundamentals. I assume it exits 2027 at the same dividend yield and low cost at each 8% and 10% (my most popular charge). At 10%, I might begin to see worth at round $140. Shares at $154 are north of even an 8% low cost charge truthful worth.

my very own calculations

As for dangers to my valuation, the primary upside threat could be if charges proceed to fall. There could possibly be a scenario the place traders settle for even a 6 or 7% return on equities, which might improve truthful worth. If we noticed a rise in lease charges or if EXR might seize the complete 15% hire differential on Life Storage properties extra rapidly, its progress might exceed my forecast.

On the draw back, Further Area is benefitting from comparatively little new development. If decrease charges convey extra development exercise, there could possibly be elevated provide within the self-storage sector, decreasing both occupancy or charges and decreasing money flows. Moreover, if charges rise once more, traders might demand a better ahead return, decreasing current worth.

Based mostly on my evaluation, for now, given the magnitude of the speed transfer and its sensitivity to charges, alongside present valuation, I might be a vendor of Further Area.