Maskot

Summary

Following my coverage on Gartner, Inc. (NYSE:IT) in Feb’24, which I recommended a buy rating as the business showed great fundamental performance in 4Q23 and the outlook was positive for FY24/25, this post is to provide an update on my thoughts on the business and stock. I continue to rate IT as a buy, as I believe the sell-down is overdone. In my opinion, there are sufficient indicators to suggest that research contract value [RCV] can accelerate sequentially from here, and this, coupled with good cost management, should continue to drive earnings growth.

Investment thesis

On 30 April, IT released its 1Q24 earnings, which saw revenue growth of 4.5% to $1.473 billion, in line with consensus expectations. In terms of segment, Research revenue grew by 4.2%, while RCV grew by 6.9% on a constant currency basis. As for the other two segments, Consulting revenue grew by 6%, while Conferences’ revenue grew by 8.5%. In terms of profits, operating income came in at $273.8 million, adj. EBITDA came in at $382 million, and EPS saw $2.93, which beat consensus estimate of $2.53.

The market clearly did not like the 1Q24 results given that share price fell sharply (-8%) post-earnings, and I think the reason was the deceleration in RCV growth. RCV is a very important metric that investors monitor because it acts as a leading indicator of growth. In 1Q24, RCV growth decelerated to 6.9% vs. 7.8% in 4Q23 and 10.3% in 1Q23. The deceleration was driven by both Global Technology Sales [GTS] that grew 5.4% (vs. 6.3% in 4Q23 and 8.8% in 1Q23) and Global Business Sales [GBS] that grew 12.3% (vs. 12.9% in 4Q23 and 16.3% in 1Q23).

In my opinion, this softer RCV growth should not have come as a surprise, as management already mentioned that RCV in 1Q was going to be weak given the seasonally low quarter for new business sales and elevated tech vendor renewals in the quarter. I believe RCV is going to accelerate in the coming quarters due to a few factors. Firstly, enterprise functional leader contract value growth within Research remained robust at 10% despite macro uncertainty. Note that this represents the second consecutive quarter of double-digit growth. Enterprise functional leaders make up about three-quarters of total RCV, so this bodes well for FY24. Secondly, the normalization of tech vendor renewals is also a tailwind for sequential growth acceleration. Thirdly, the plan to expand the salesforce was reiterated during the call (sales force headcount growth of mid-single-digits in FY24), and importantly, IT’s sales force is increasingly becoming more productive. Average contract value per quota-bearing sales employee has sustained above the $1 million mark, which is ~22% higher than pre-covid (FY17–FY19) despite a seasonally softer quarter. When viewed together, an expansion of sales force headcount along with increased productivity should further drive sequential improvement in growth. Lastly, as I have noted previously, I see Conference revenue as a leading indicator of growth. The fact that management raised its full-year guide for Conference and Consulting revenue due to expanded conferences and an increase in labor-based consulting makes me feel even more optimistic that companies are opening their budgets, and this also bodes well for the coming quarters’ growth

IT has also shown again that they are good at managing costs. They managed to improve adj. EBITDA margins by 150bps vs 4Q23, despite having a smaller revenue base. This implies that IT has seen really strong operational efficiencies, which bodes well for further margin expansion as revenue accelerates sequentially. IT has a good history of expanding margins and sustaining them (margins went from low teens in the early 2000s to late 2000s and were sustained at that level for the next decade), showing that management knows how to keep costs under control while expanding the business.

Valuation

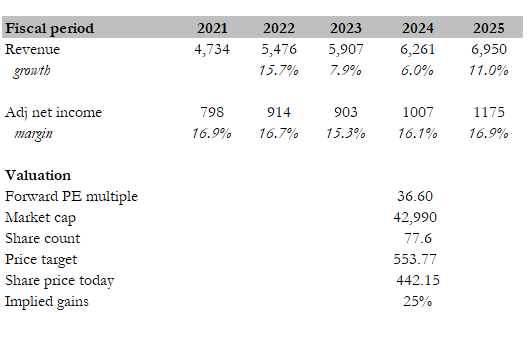

Own calculation

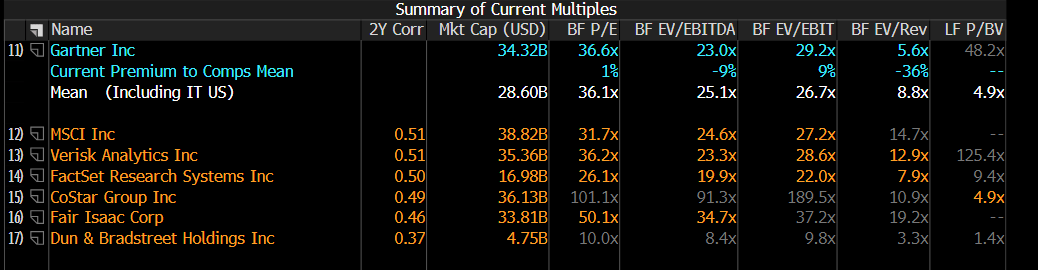

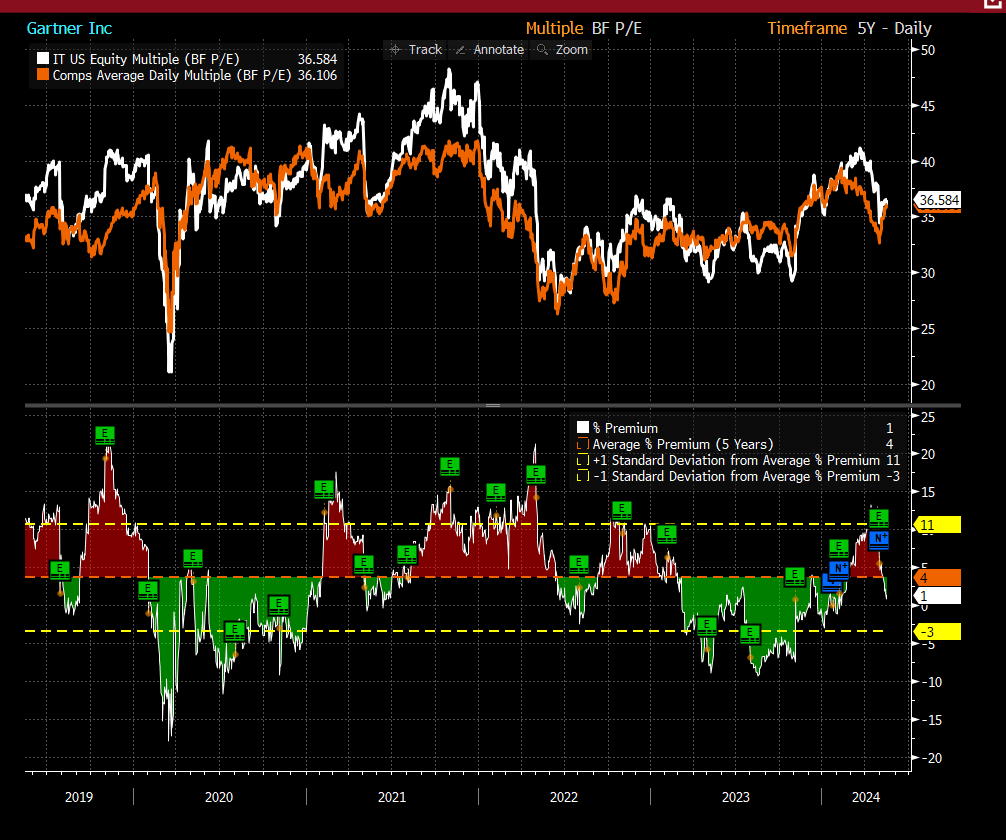

My target price for IT based on my model is $594 as opposed to $578 previously. Although I remained positive about the sequential growth acceleration ahead, I have tapered my growth expectations down by 400 bps, assuming that growth will accelerate from 4.5% in 1Q24 to 8% in 4Q24 (assuming growth to accelerate back to FY23 levels, and this translates to 6% full-year growth), to reflect the soft 1Q24 performance. Accordingly, I adjusted FY25 growth downward by the same magnitude. As for net margin expectations, although I am very encouraged by management’s ability to manage costs, I am keeping a conservative view as they are going to increase headcount. New hires are typically less productive since they need time to mature, which may represent near-term headwinds to margins. Regarding valuation (forward PE), the good news is that it has come down from the high end of its 5-year trading range to its average of 36.6x, and I believe valuation will continue to trend around this average multiple. When compared to peers, IT’s valuation also doesn’t sound expensive, as it is trading in line with them.

Bloomberg

Bloomberg

Risk

Although there are various indicators that suggest a positive growth outlook, I would not dismiss the fact that RCV continued to decelerate. If this metric does not accelerate in 2Q24, I believe it will have a heavy impact on the market’s expectations. Specifically, consensus is likely going to revise their estimates downward, and the market will follow through by derating valuation downwards as the near-term earnings outlook is bad.

Conclusion

In conclusion, my rating for IT remains unchanged (buy). While the market overreacted to the slight deceleration in RCV growth in 1Q24, there are compelling reasons to believe it will pick up in the coming quarters. Strong growth in enterprise functional leader contracts, normalization of tech vendor renewals, and a planned expansion of the productive sales force all point towards this. Additionally, IT’s commitment to cost control and history of margin expansion instills confidence that margin can continue to expand.