izusek/E+ through Getty Pictures

Whenever you begin studying about finance, one of many first misconceptions that you simply stumble throughout is that the market is completely environment friendly or fairly near it. Legendary buyers like Warren Buffett, Peter Lynch, and numerous others who observe the worth college of investing ideology, have confirmed this concept to be fallacious. Over home windows of time, typically lasting years, the market might be inefficient, significantly in relation to particular person securities. One good instance of this may be seen by GE HealthCare Applied sciences (NASDAQ:GEHC), the healthcare enterprise that was spun off from industrial conglomerate Basic Electrical (GE) earlier this yr.

The final article that I revealed relating to GE HealthCare Applied sciences inventory got here out in July of this yr. It was one of many few corporations that I had rated a ‘strong buy’. Such a designation displays my perception that shares ought to, over the long term, considerably outperform the broader market. As I wrote about early this yr, my total observe file for ‘strong buy’ prospects is fairly stable. However not everybody of those performs seems the best way that I would really like. To this point, GE HealthCare Applied sciences has woefully underperformed the broader market because the publication of my final article. Throughout this window of time, the inventory is down 16% at a time when the S&P 500 has inched up by 0.6%.

Vital upside exists

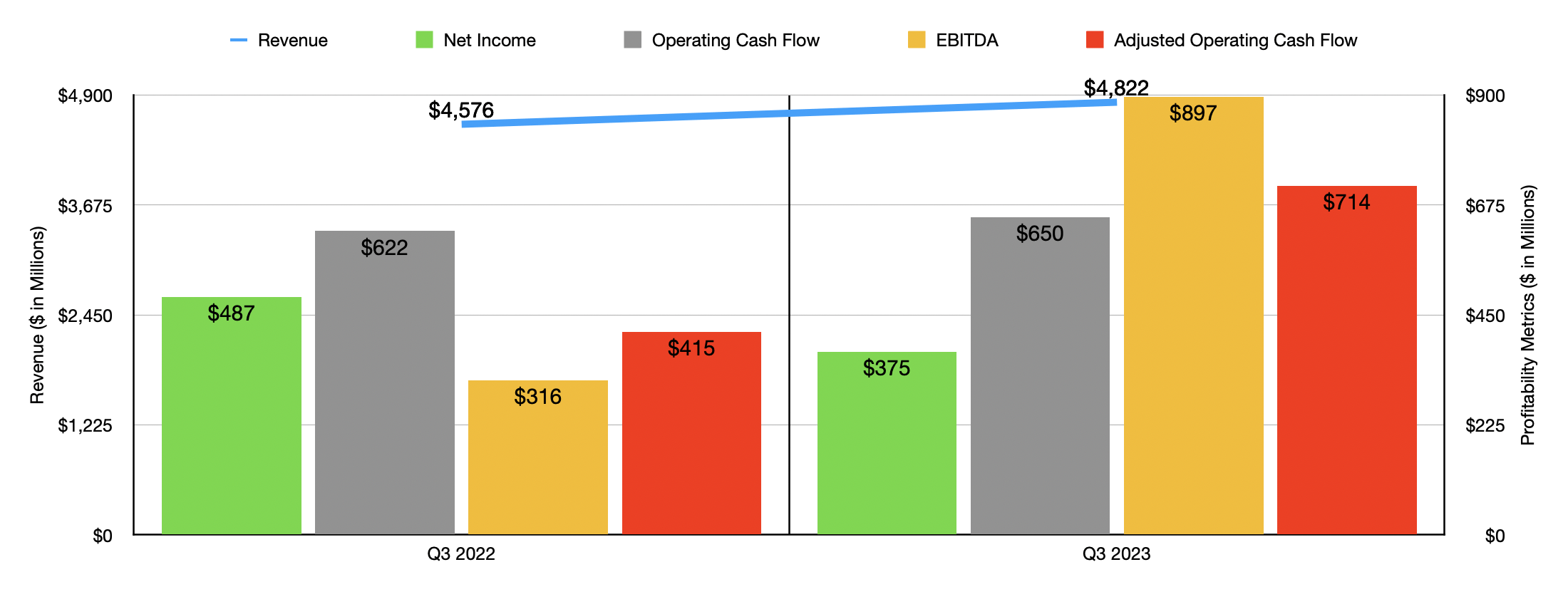

Latest weak point from a share value perspective has been pushed not by fundamentals, however has as a substitute been pushed by market sentiment. I say this as a result of the most recent financial data supplied by administration has been encouraging. This information covers the third quarter of the 2023 fiscal yr. Throughout that point, income for the corporate got here in at $4.82 billion. That is 5.4% above the $4.58 billion generated one yr earlier. The best upside, from a yr over yr development perspective, has been from the corporate’s PDx section. That is the a part of the enterprise that focuses on the pharmaceutical diagnostics area. This unit operates largely as a provider of diagnostic brokers for the worldwide radiology and nuclear medication area. These brokers are complementary to the agency’s gadgets beneath different segments, so it stands to cause that the extra that these segments develop, the extra that this specific section will develop over the lengthy haul. Through the quarter, income for this unit was $589 million. That is 12.8% above the $522 million generated the identical time final yr. Administration attributed this to greater pricing and better demand for sure areas just like the EMEA (Europe Center East and Africa) and Remainder of World areas that it operates in.

Writer – SEC EDGAR Knowledge

The corporate skilled development somewhere else as nicely. The PCS, or Affected person Care Options, skilled gross sales development of 9%, with income rising from $701 million to $764 million. That is the a part of the enterprise that gives prospects with medical gadgets, consumable merchandise, providers, and digital options, that each one focus on bigger organizations and groups. This enhance in gross sales was attributable to development throughout some product traces comparable to Monitoring Options, Consumables, and numerous associated providers. Administration chalked this development as much as robust demand enhancements in provide chain success and better pricing.

And lastly, the Imaging section, which is answerable for numerous scanning gadgets and related applied sciences comparable to these involving CT scans, MRIs, X-rays, and extra. Income beneath this unit managed to rise by 4.7% from $2.52 billion to $2.64 billion because of development and demand for molecular imaging and computed tomography gadgets and magnetic resonance gadgets, in addition to due to provide chain success enhancements, greater pricing on the merchandise that the corporate offered, and the introduction of recent merchandise. In truth the one weak point for the quarter got here from the Ultrasound section, which noticed income dip by 1% from $823 million to $815 million. This drop, administration stated, got here from easing of provide chain constraints final yr that briefly boosted income then.

Writer – SEC EDGAR Knowledge

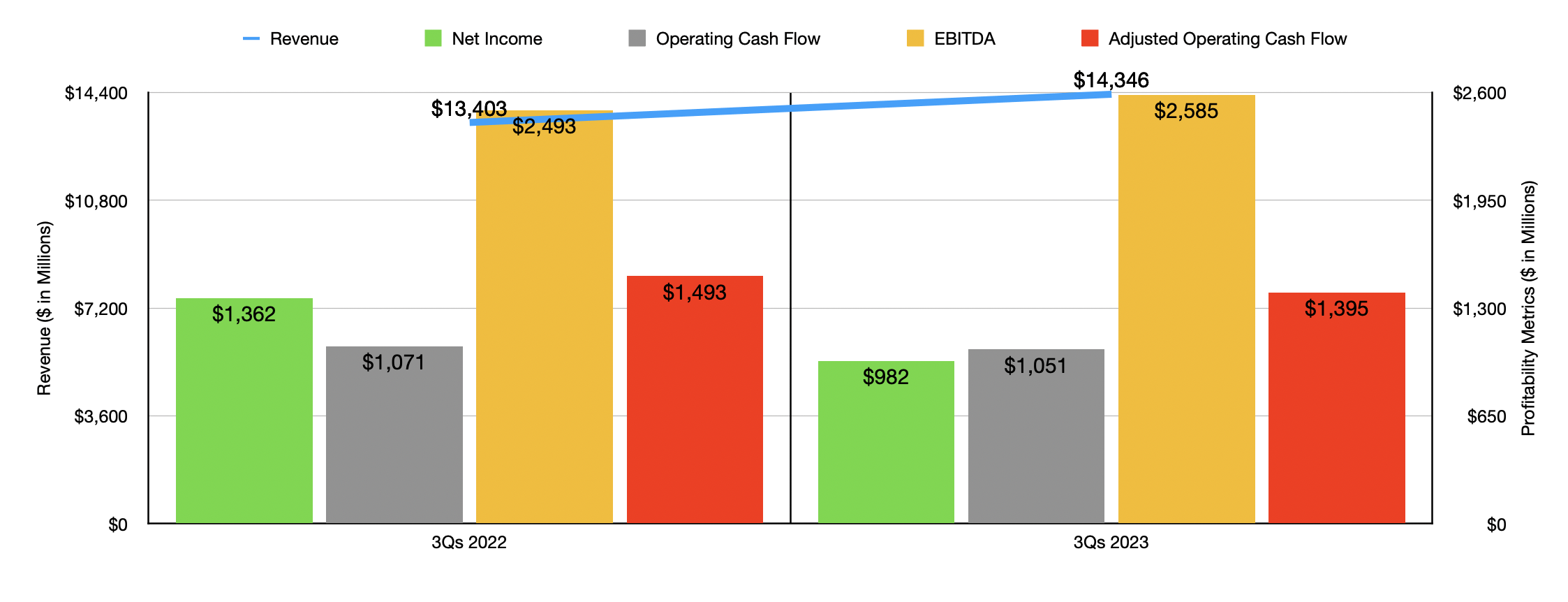

The rise in income for the corporate didn’t, sadly, end in greater income. Internet revenue truly managed to fall from $487 million to $375 million. Whereas the corporate did endure from greater curiosity expense and a reasonably significant rise in analysis and growth prices, income nonetheless would have been greater yr over yr had it not been for a near-doubling in revenue tax expense from $129 million to $250 million. Different profitability metrics, fortuitously, managed to come back in fairly a bit stronger. Working money circulation inched up from $622 million to $650 million. But when we modify for modifications in working capital, we get a reasonably sizable enhance from $415 million to $714 million. And eventually, EBITDA skyrocketed from $316 million to $897 million. Because the chart above illustrates, monetary efficiency for the primary 9 months of 2023 relative to the identical time final yr have been largely much like the third quarter of this yr in comparison with the identical quarter final yr. Nevertheless, money circulation figures in some respects have been weaker this yr than final yr.

Writer – SEC EDGAR Knowledge

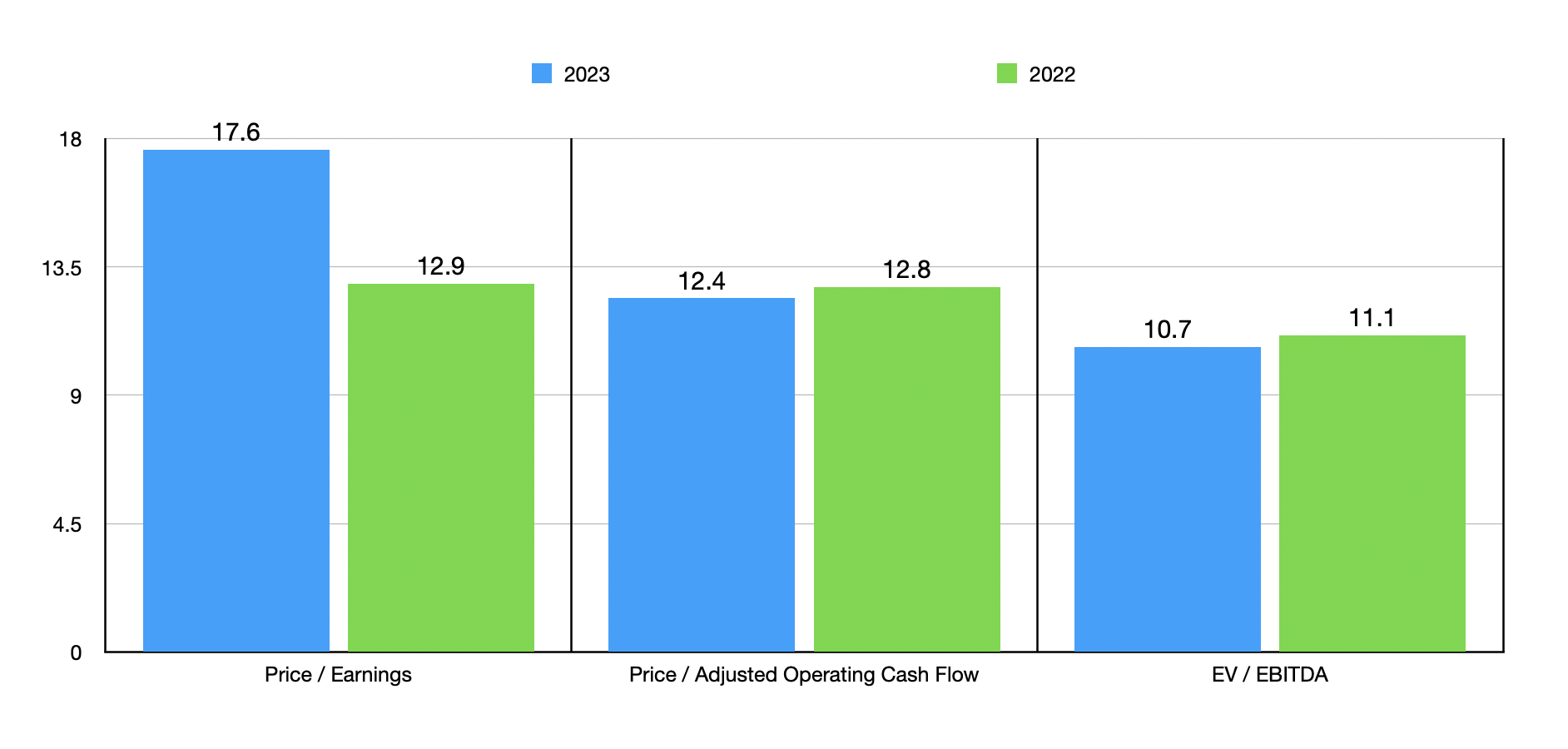

For this yr in its entirety, administration is anticipating natural income to be between 6% and eight% greater than it was final yr. Administration additionally elevated earnings steering, with income now anticipated to be between $3.75 and $3.85 per share. That is $0.05 per share greater than what was beforehand anticipated on the low finish of the dimensions. This could translate to web income of about $1.74 billion. Based mostly alone estimates, adjusted working money circulation must be round $2.48 billion, whereas EBITDA ought to are available in someplace round $3.62 billion. Assuming that these estimates are appropriate, the corporate must be priced as proven within the chart above. As you may see, the inventory is a little more costly relative to final yr on a value to earnings foundation. However in relation to the opposite two profitability metrics, it must be a bit cheaper.

| Firm | Value / Earnings | Value / Working Money Move | EV / EBITDA |

| GE HealthCare Applied sciences | 17.6 | 12.4 | 10.7 |

| Danaher (DHR) | 27.6 | 20.1 | 18.6 |

| Thermo Fischer Scientific (TMO) | 32.4 | 23.5 | 20.0 |

| Agilent Applied sciences (A) | 30.6 | 21.5 | 22.8 |

| Mettler-Toledo Worldwide (MTD) | 28.1 | 24.7 | 20.4 |

| Siemens Healthineers AG (OTCPK:SMMNY) | 39.4 | 28.1 | 15.1 |

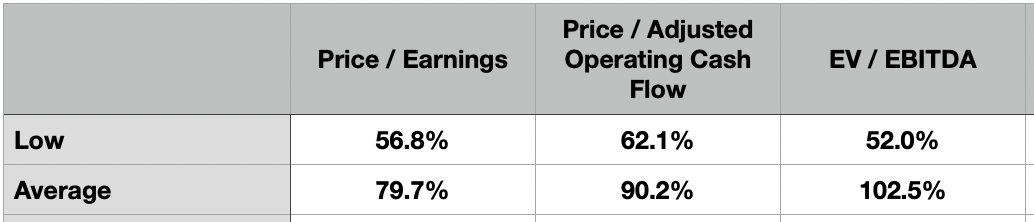

As a part of my evaluation, I then created the desk above. In it, you may see how GE HealthCare Applied sciences is priced in comparison with 5 related corporations. To avoid wasting you a while, I seemed on the numbers myself and concluded that, no matter which valuation metric we use, GE HealthCare Applied sciences is the most cost effective of the group. To see what sort of upside potential the agency may supply, I then created the desk beneath. In it, you may see how a lot upside shares would have beneath every of the valuation approaches if the inventory have been to commerce on the similar a number of as the following least expensive participant within the area. Along with this, I additionally averaged out the multiples of the 5 corporations I in contrast it with and calculated what sort of upside shares would expertise in that situation. Even within the worst case, we’d be upside of 52%. After which one of the best case, upside could be 102.5%. So you may perceive why I’m as bullish concerning the enterprise as I at the moment am.

Writer – SEC EDGAR Knowledge

Takeaway

Based mostly on all the info supplied, I need to say that I’m extremely optimistic about the way forward for GE HealthCare Applied sciences. Whereas it’s true that among the money circulation figures might look higher than they at the moment do that yr, the inventory appears to be like attractively priced, each on an absolute foundation and relative to related corporations. Income continues to develop and even administration elevated steering for earnings on the midpoint. Absent one thing vital altering concerning the enterprise, I’d say that additional upside is probably going from right here. And due to that, I’ve determined to maintain the corporate rated a ‘strong buy’ for now.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.