Mrkit99/iStock Editorial through Getty Pictures

Assicurazioni Generali (OTCPK:ARZGF) has strong fundamentals and an extra capital place, a backdrop that will result in an enhanced shareholder remuneration coverage within the brief time period.

As I’ve lined in a previous article, whereas Generali has an attention-grabbing dividend yield, its premium valuation was not warranted provided that Generali’s progress prospects aren’t spectacular, and I’ve really helpful ageas SA/NV (OTCPK:AGESY) as a greater earnings different.

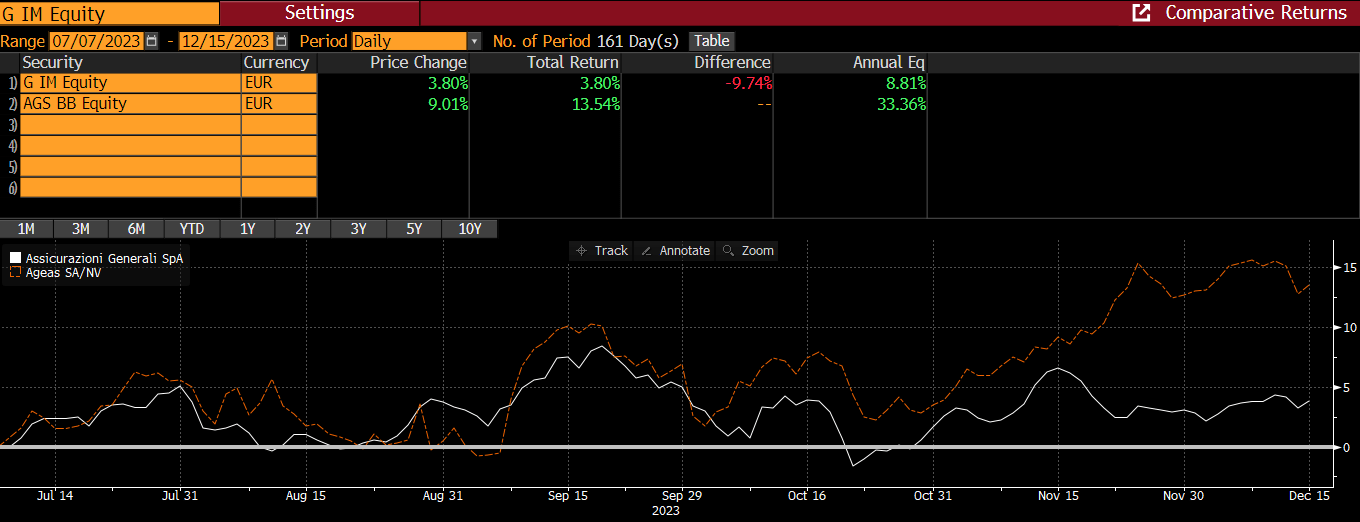

As proven within the subsequent graph, this suggestion to play out nicely, provided that ageas SA/NV has outperformed Generali since then, up by 13.5% vs. lower than 4% for Generali.

Worth efficiency (Bloomberg)

On this article, I assessment Generali’s most up-to-date earnings and replace its funding case, to see if it’s presently a extra attention-grabbing earnings choice inside the European insurance coverage sector or not.

Earnings Evaluation

Generali has reported some weeks in the past its financial results for the primary 9 months of 2023 (9M 2023), which have been forward of expectations, particularly concerning its bottom-line.

In 9M 2023, Generali’s gross written premiums elevated by 4.7% YoY to €60.5 billion, supported by the optimistic momentum within the Property & Casualty (P&C) phase. Certainly, P&C premiums elevated by greater than 11% in comparison with the identical interval of 2022, whereas the life phase reported a extra modest efficiency.

Provided that Generali’s enterprise is extra geared to the Life insurance coverage phase, this may be thought-about a very good working efficiency, provided that rising rates of interest makes different funding alternate options extra enticing to clients, similar to time deposits from the banking sector, placing some stress on web inflows to life insurance coverage merchandise.

Its consolidated working revenue elevated to €5.1 billion in 9M 2023, a rise of 16% YoY, justified by sturdy earnings from the P&C phase as a result of decrease climate prices than in 2022. This phase elevated its working end result by 50% YoY to €2.15 billion, whereas then again the life phase reported an working earnings of almost €2.8 billion (-1.1% YoY), and the asset administration enterprise had an working earnings of €728 million (+3.8% YoY).

Its sturdy outcomes from the P&C phase are justified each by higher pricing, as the corporate raised costs throughout a number of insurance coverage strains in the previous few quarters, to mirror inflationary pressures and better claims prices within the latest previous. Certainly, Generali elevated pricing in motor and different private strains, resulting in common premiums rising by 6.9% YoY in 9M 2023. One other optimistic issue for its working end result was additionally contained claims prices, which led to a mixed ratio of 94.3% in 9M 2023, in comparison with greater than 97% within the earlier 12 months.

Concerning its funding earnings, it was additionally a lift to its earnings from greater bond yields, plus it additionally took some income from its equities publicity benefiting from the sturdy efficiency of shares within the 12 months.

As a result of this optimistic working momentum, its adjusted web end result within the first 9 months of 2023 elevated to €2.9 billion, up by near 30% YoY. Its solvency ratio was 224% on the finish of final September, sustaining a really sturdy capitalization degree inside the European insurance coverage sector.

These optimistic outcomes don’t embody the corporate’s latest agreements to purchase Liberty Mutual insurance operations in Portugal, Spain, Eire, and Northern Eire, plus its pending acquisition of Conning Holdings within the asset administration unit. These two offers have been introduced some months in the past and are anticipated to be accomplished throughout 2024, thus they’ll improve Generali’s publicity to the P&C and asset administration segments, as a part of its technique to diversify its enterprise and cut back its reliance on life insurance coverage.

Nonetheless, life insurance coverage is predicted to stay the corporate’s most essential phase over the subsequent few years, except Generali carry out some comparatively giant acquisition in different enterprise models. Whereas I don’t anticipate this to occur, Generali’s sturdy capital place permits it to carry out acquisitions and if the chance arises it could determine to develop its enterprise within the P&C or asset administration segments in a big approach by way of a possible acquisition.

Nonetheless, Generali will carry out an investor day on the finish of subsequent January, when it can replace traders about its technique for the subsequent few years and supply new monetary targets, most likely for the interval 2024-26. I don’t anticipate the corporate’s technique to alter a lot from its present one, targeted primarily on natural progress, and to make use of its extra capital place to return capital to shareholders.

That is clearly optimistic for its dividend, which is more likely to be the popular approach to distribute earnings and extra capital to shareholders within the coming years, whereas a share buyback program may additionally be introduced. This expectation is supported by Generali’s capital ratio that’s nicely above its peer’s common, which have Solvency ratios round 200%, plus the corporate’s good capital era capability.

Which means Generali doesn’t have to retain a lot earnings going ahead and could be due to this fact extra aggressive concerning its capital return coverage within the coming years.

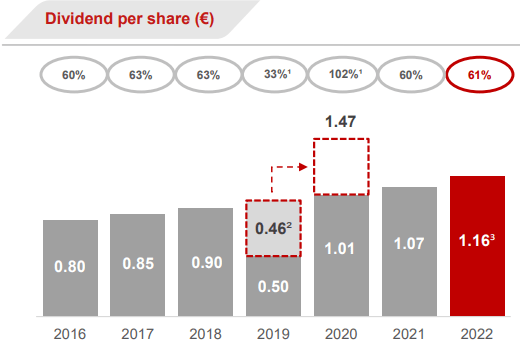

Nevertheless, this doesn’t appear to be presently anticipated by the road, provided that its dividend is predicted to develop from €1.16 per share associated to 2022 earnings, to just about €1.40 per share by 2026 (associated to 2025 earnings).

Dividends (Generali)

This represents an annual progress charge of solely 6.2% over the subsequent three years, which appears to be fairly conservative, although is near Generali’s historic progress charge over the previous three years. Nonetheless, its final annual dividend of €1.16 per share represented an annual improve of 8.4%, which was a lift in comparison with the earlier years when its dividend elevated at an annual charge of 5.2% and 5.9%, respectively.

Provided that present dividend estimates is for Generali to develop its dividend to €1.25 per share associated to 2023 earnings, its dividend is predicted to extend by 7.8% YoY, thus it doesn’t make a lot sense to cut back its annual progress charge within the following years. Due to this fact, Generali clearly appears to have some room to beat present sell-side expectations concerning its dividend within the coming years, which might be a optimistic catalyst for a better share value within the brief time period.

Its dividend coverage is more likely to be up to date at its upcoming investor day, being an essential occasion for Generali’s traders to observe, because it might probably be nicely obtained by the market if the corporate decides to turn into extra aggressive concerning its shareholder remuneration coverage.

Conclusion

Whereas Generali has sound fundamentals, this was mirrored in its valuation some months in the past and for that cause my suggestion was to purchase ageas SA/NV as a substitute of Generali. Whereas I nonetheless want the Belgian firm over the long run, I believe that taking a speculative place on Generali is smart as a result of the corporate could have an essential occasion subsequent month that might transfer its share value.

Provided that Generali has a strong capital place, it could determine to be extra aggressive concerning capital returns, making it an attention-grabbing speculative play within the brief time period.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.