Marco VDM/E+ through Getty Photos

Genesco (NYSE:GCO) is a retailer of footwear and attire. GCO lately posted weak Q3 FY24 outcomes. Its margins had been below stress, and gross sales development struggled as a consequence of macroeconomic headwinds. I consider its margins would possibly proceed to stay below stress, and contemplating the opposed market setting, it’d wrestle to develop its revenues. Therefore, contemplating these elements, investing in GCO will be dangerous. Therefore, I assign a maintain ranking on GCO.

Monetary Evaluation

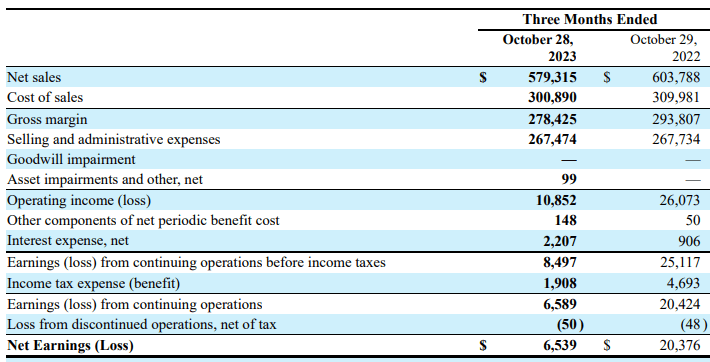

GCO lately posted its Q3 FY24 results. The online gross sales for Q3 FY24 had been $579.3 million, a decline of 4% in comparison with Q3 FY23. The foremost motive for the drop was a weak efficiency in its Journeys Group and Genesco Manufacturers Group segments. The Journey and Genesco Manufacturers Group gross sales declined by 8.2% and 21.5% in Q3 FY24 in comparison with Q3 FY23. Decreased spending as a consequence of inflationary pressures affected the corporate’s gross sales. Its gross revenue margin for Q3 FY24 was 48.1%, which was 48.7% in Q3 FY23. The decline in margins was as a consequence of elevated warehouse prices and elevated promotional exercise.

Searching for Alpha

The online earnings declined to $6.5 million in Q3 FY24, which was $20.3 million in Q3 FY23. The impact of the difficult retail setting will be seen within the outcomes. The decreased shopper spending remains to be affecting the corporate. Though there are some positives, just like the hike within the rates of interest being stopped, even the present charges are excessive, which can proceed to have an effect on them. So, to sort out the decreased shopper spending, the administration may need to spend closely on promotional actions, which might stress its margins. As well as, its long-term debt on the finish of October 2023 was $128.1 million, which was $85.9 million in October 2022. The rise in debt turns into much more regarding due to the opposed market situations. Wanting on the macroeconomic headwinds, I consider they may proceed to wrestle to spice up their gross sales. The administration’s gross sales steerage additionally reveals weak spot. They anticipate their FY24 gross sales to be down round 2% in comparison with FY23. So, contemplating the weak outlook, stress on margins, and elevated debt, GCO will be dangerous.

Technical Evaluation

Buying and selling View

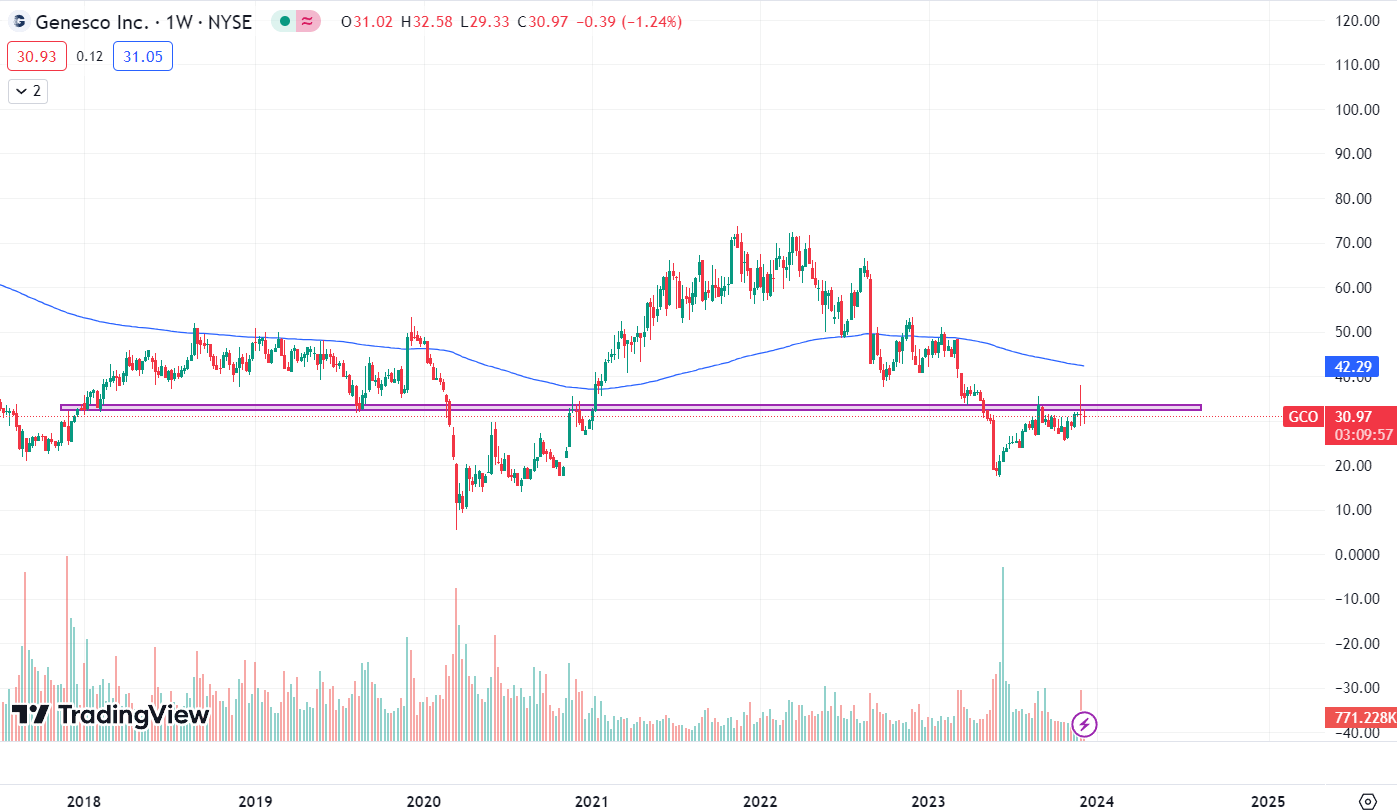

GCO is buying and selling at $30.9. The earlier week’s candle broke out of the resistance zone of $34, but it surely turned out to be a fake-out. The inventory instantly reversed after crossing the $34 degree, which reveals that sellers are lively. Therefore, one ought to keep away from shopping for it proper now as I consider, wanting on the current candles, that the inventory worth would possibly proceed its downtrend. Even when it breaks the $34 degree, there may be another barrier that it wants to interrupt, and that’s its 200 ema, which is at $42.3. So, shopping for GCO proper now will be dangerous as there are two main boundaries to the inventory worth, and the newest candles are proof of this. Therefore, making any new shopping for positions within the inventory is perhaps dangerous. So it could be higher to keep away from it.

Ought to One Make investments In GCO?

First, take a look at GCO’s valuations. GCO has a P/E [FWD] ratio of 18.48x in comparison with the sector median of 15.33x and has an EV / EBITDA [FWD] ratio of 11.95x in comparison with the sector median of 9.87x. Contemplating its present efficiency and future outlook, I believe GCO would not need to commerce at a better valuation. Its EPS [FWD] is round $1.75, and I consider it could possibly commerce round a P/E of 15.3. So, this offers us a share worth of $26.8. So, I consider GCO would not present a lot worth proper now. Therefore, contemplating elements like weak outcomes, weak technical chart, excessive valuation, and weak outlook, I believe investing in GCO will be dangerous. Therefore, I assign a maintain ranking on GCO.

Danger

Fast adjustments in shopper tastes are a problem for the trade during which they work. For his or her footwear and attire to stay widespread and develop and select new traces and kinds that entice a variety of customers, they have to precisely acknowledge and interpret shifting shopper traits and preferences and act rapidly to deal with them. Demand and market acceptability for each new and outdated objects are unpredictable and depend on large-scale investments in product design, growth, and innovation, steady dedication to product high quality, and large-scale, persistent advertising and marketing initiatives and prices. They usually have to guage product designs and advertising and marketing budgets months forward of when actual public acceptance will be measured to gauge their response to predicted shifting shopper traits and preferences. In consequence, they may not be capable to develop new objects which can be accepted by the market in response to altering buyer traits and preferences. They danger having extra stock, higher-than-normal markdowns, returns, order cancellations, or the shortcoming to promote their product profitably if they’re unable to acknowledge and analyze shifting shopper preferences and traits or to promptly develop or supply merchandise that meet market acceptance in response to those adjustments.

Backside Line

Its quarterly outcomes confirmed weak spot, and I consider its gross sales and margins would possibly proceed to stay below stress as a consequence of macroeconomic headwinds. Moreover, its weak outlook and excessive valuation make it unattractive. Therefore, contemplating these elements, I assign a maintain ranking on GCO.